1. BTC shrinkage adjustment or in place

In the 4-hour K line chart of BTC, after the price fell back from the middle track of Bollinger Line, the continuous low consolidation and the closing price further declined. In terms of trading volume, it also reached the lowest level in September, indicating that the adjustment of BTC has come to an end, and investors' enthusiasm for short-term trading has dropped to the freezing point. From the current point of view, BTC is in the key position of the steering wheel.

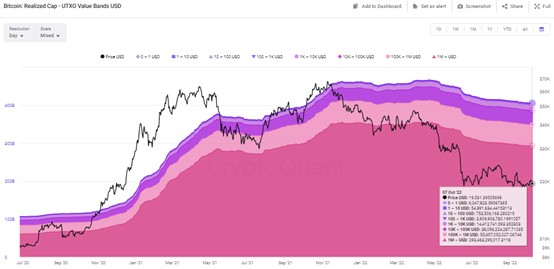

2. BTC has realized the value transfer to the main force

From the perspective of BTC's realized UTXO value, the proportion of investors holding currency funds is still high. At present, the number of investors holding currencies worth more than 100 million dollars accounts for a very large proportion. On October 7, 2022, the total market value of these investors' currency holdings was US $293.4 billion, an increase of 400% compared with US $58 billion in March 2020. Although BTC is in the adjustment stage, the market value of these investors has not decreased significantly. This shows that whales with a large amount of money still have a great impact on BTC prices. As long as Jujing holds coins stably, BTC will still maintain its current running rhythm.

3. The number of BTC non-zero addresses stagnates

The number of non-zero addresses of BTC remained stable. On October 8, the number was 43.36 million, which was very small compared with 43.38 million on August 5. This shows that the recent enthusiasm of small and medium-sized investors for entering the market is very low, and BTC has not changed hands to retail investors. At the same time, it shows that BTC investors are in a very obvious wait-and-see stage. The divergent trend of BTC in the hands of investors has not expanded, and the market is facing greater uncertainty.

4. ETH preliminary support is still effective

In terms of daily K line, ETH completed an oversold rebound at the bottom during the fall in June 2022, and the three bottom patterns during this period still support ETH. Although the current ETH trading volume is shrinking, the change still needs further high intensity volatility to really prompt the trading direction. Spot trading volume hit the lowest level in four months. At the same time, it is estimated that the leverage ratio has soared to a new historical high, and ETH has great potential for volatility. The higher the leverage ratio, the greater the volatility potential.

5. ETH estimates that leverage ratio reaches a new high

As the number of ETH in the exchange continued to decline, the estimated leverage ratio reached the highest value in history, reaching 0.296 on October 2. It is estimated that the leverage ratio remains above 0.282 in the near future, which means that ETH has a high leverage ratio and a high volatility potential before the change. The estimated leverage ratio that continues to grow shows that the trading risk of investors is still soaring rapidly, making it more likely that a large number of positions will explode.