TL;DR

Korea's export value and price per kilogram for multiple memory categories in the first 20 days of June showed significant year-on-year growth, sparking renewed market discussion on whether memory manufacturers are gaining a premium due to AI infrastructure bottlenecks.

The importance of this development lies not just in it being another set of semiconductor export figures, but in that it touches upon two variables of greatest concern to investors simultaneously: shipment value is rising, and the export value per unit weight is also rising. The former points to demand strength, while the latter points to a migration towards higher-value products in terms of pricing and product mix. For memory stocks, this holds more significance than simply "selling more," as it impacts revenue, gross margins, and the potential for EPS upgrades.

Over the past year, the market has already accepted HBM (High-Bandwidth Memory) as a scarce resource in AI servers. The debate is whether this scarcity is merely driving up prices for a few high-end products, or if it has begun to spill over into the broader DRAM, NAND, and SSD memory supply chain. If it's the former, memory stocks remain more akin to a cyclical recovery trade. If it's the latter, the valuation anchor for SK Hynix, Samsung, and Micron could partially shift from "inventory cycle" towards "AI infrastructure bottleneck."

The Korean data provides a strong signal, not a definitive conclusion. Especially the breakdown by category and price per kilogram for the first 20 days of June are, for now, better suited as preliminary observations from aggregated social media sources and cannot be directly treated as official, complete confirmation. Their value lies in moving a narrative-driven question to a stage where it can be cross-verified with trade value, price indicators, and company guidance.

Korean Exports Give the Market a Price Signal

The most direct implication of this dataset is that the memory upswing may not be just a shipment volume recovery; prices and product mix are also becoming more premium.

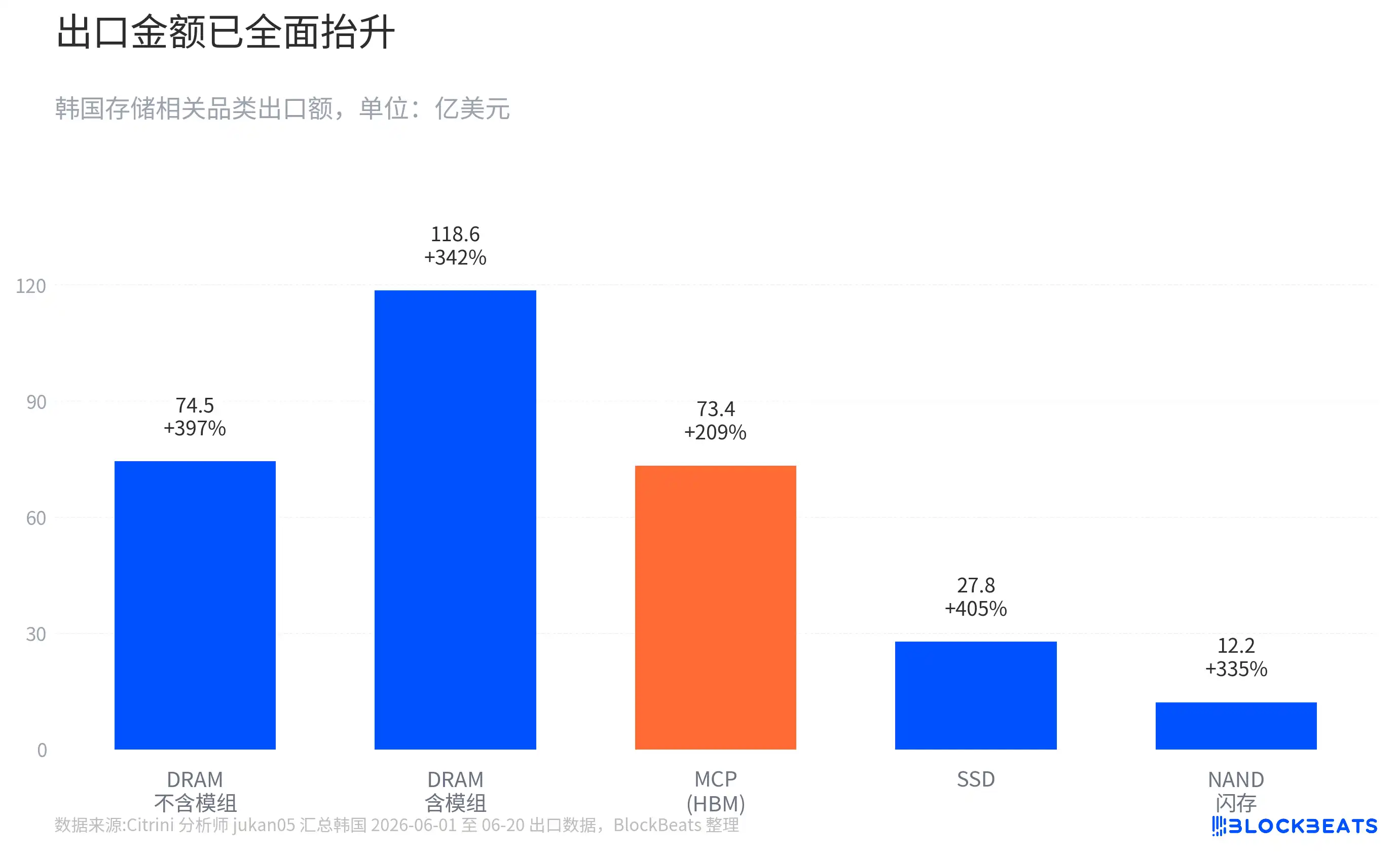

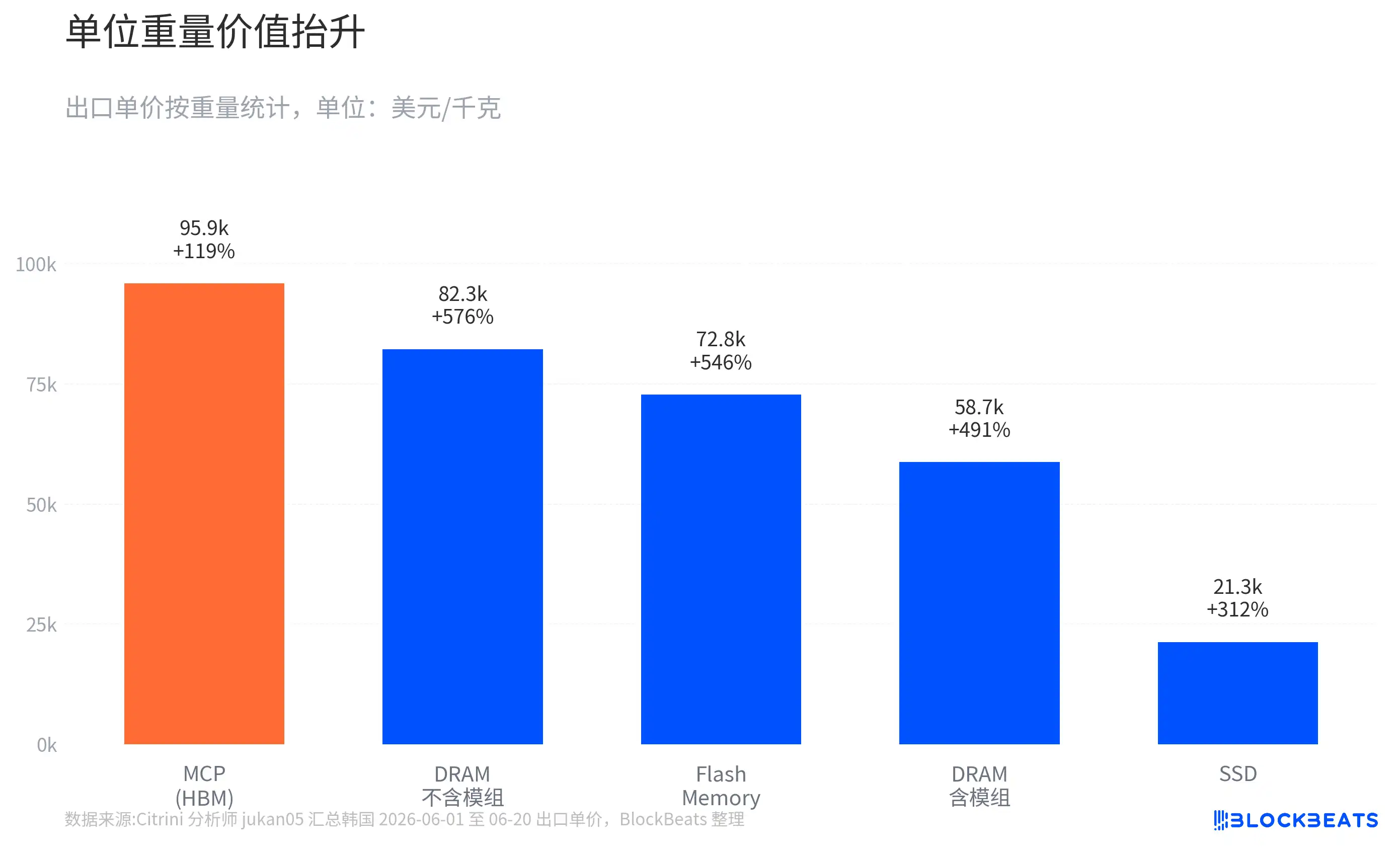

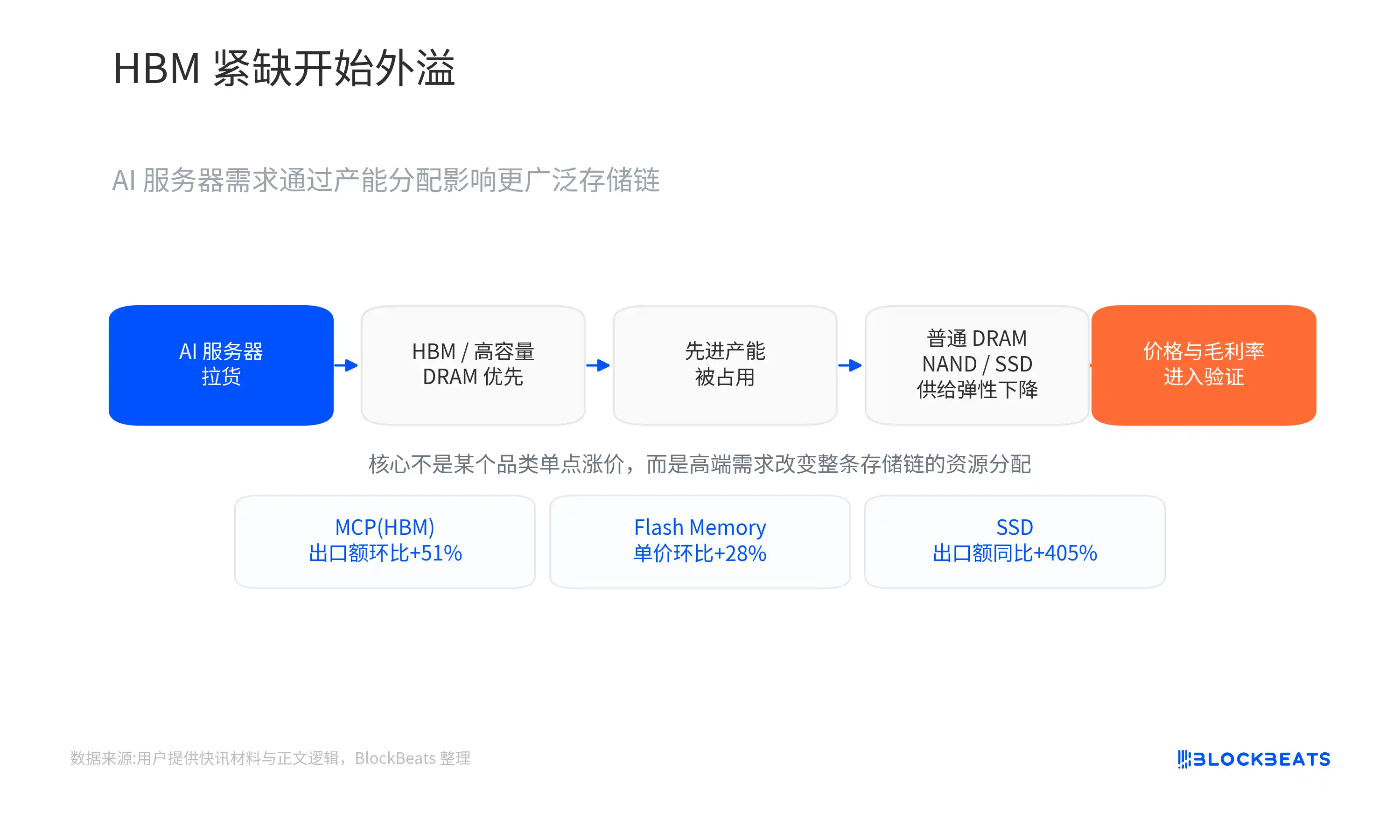

Preliminary export data for Korea from June 1 to 20 shows export values for multiple categories like DRAM, NAND/Flash, MCP, and SSD all in high year-on-year growth territory. Among them, export value for DRAM (excluding modules) increased nearly fourfold year-on-year, while DRAM (including modules) increased over threefold. Export values for NAND/Flash and SSD also grew significantly. Of greater market interest was the price per kilogram, with some DRAM and NAND-related categories showing year-on-year increases exceeding 500%.

These numbers need to be viewed with context. The first 20-day data is more like a mid-month snapshot of Korean trade data, useful for indicating direction and slope but not the final full-month figure. The classification of sub-categories may also not perfectly align with product definitions understood by investors, making direct extrapolation to full-year earnings models unsuitable.

A more stable reference comes from already published May data. According to Korean media reports based on official data, Korea's total exports in May reached $87.75 billion, up 53.2% year-on-year; semiconductor exports hit $37.16 billion, up approximately 169% year-on-year, a new monthly record, accounting for 42.3% of total exports. Exports of computers and related equipment also saw substantial growth, which media linked to demand for AI server SSDs. Preliminary exports for June 1-10 were also strong, with total exports at $28.6 billion, up 86% year-on-year, and semiconductor exports around $11 billion, up more than threefold.

This makes the social-media-aggregated data for the first 20 days of June more than just an isolated signal. It forms continuity with the prior official export trends. For investors, continuity is more important than a single-month spike, as it determines whether earnings upgrades can evolve from a one-time surprise into adjustments to models over multiple quarters.

Soaring Price Per Kilogram Does Not Mean Chips Got Five Times More Expensive

The most easily misinterpreted aspect of this data is directly translating the soaring price per kilogram into "each chip got several times more expensive." A more accurate description is that the price per kilogram reflects the combined effect of price increases, a shift towards more premium product mixes, and statistical definitions.

Some categories in Korean export data use weight to calculate average unit prices. For bulk commodities, this metric is straightforward. But for semiconductors, the value difference for the same kilogram of goods can be vast. One kilogram of low-end memory chips versus one kilogram of HBM, high-capacity DRAM, or complex packaging products are not on the same level in terms of value density. The rise in price per kilogram can come from price increases for the same products, or from a shift in export structure towards higher-value products.

This is precisely the core of the AI trade. AI servers require memory systems with higher bandwidth, larger capacity, and lower latency; HBM and high-end DRAM have far greater value density than standard memory products. When the share of these products in the export structure rises, the average export value per kilogram is pushed higher. What the market is seeing is not a uniform fivefold price increase for all memory chips, but rather a combination of rising high-end product share and price increases that is changing the revenue quality of the memory chain.

The MCP definition also requires particular caution. The market often uses MCP as a proxy indicator for observing HBM-related trends because HBM often involves multi-chip stacking and packaging. However, MCP (Multi-Chip Package) is not synonymous with narrow-sense HBM; it may also include other multi-chip packaging products. Strong MCP export value and unit prices can support the directional judgment of "strong demand for high-end packaged memory" but cannot be directly written as HBM export value.

This qualification does not weaken the data's value; on the contrary, it makes it more suitable for investment judgment. The truly useful conclusion is not exactly how much a specific product increased in price, but that multiple memory categories are simultaneously showing increases in both value and unit value, indicating that AI demand may no longer be confined to the isolated island of HBM. It is, through capacity allocation, product mix, and customer procurement, influencing the broader memory pricing system.

HBM Shortage Changes Memory Makers' Pricing Position

Looking at HBM alone, the market already knows it's tight. The new question is why an HBM shortage would affect DRAM, NAND, and SSD.

The mechanism is not complex. Memory manufacturers have limited advanced capacity, R&D resources, and customer qualification capabilities. When NVIDIA and cloud providers continuously lock in high-value products like HBM and high-capacity DRAM, manufacturers will prioritize allocating resources to directions with higher returns and stronger order visibility. This can keep supply of high-end products persistently tight and may also indirectly squeeze the supply elasticity for ordinary DRAM, NAND, and SSD.

SK Hynix is the most direct beneficiary of this logic. The market widely believes its HBM share is in a leading position. According to industry reports and brokerage research, SK Hynix has relatively high HBM capacity visibility for 2026, with customer demand exceeding supply capability and growth in high value-added product sales. For a memory maker, customer pre-booking of capacity and growth in high-value product sales changes not just next quarter's revenue but also the market's assessment of its pricing power. The core issue for traditional cyclical stocks is how long prices can rise; for bottleneck assets, the core issue is how much premium customers are willing to pay for secured supply.

The logic for Samsung and Micron differs slightly. Samsung has greater scale in NAND and overall memory capacity while still catching up on high-end HBM customer qualifications. Micron benefits from the expansion of high-end memory demand and supply chain diversification. For these two companies, the market is trading not on them having fully replicated SK Hynix's HBM pricing power, but on the premise that if HBM tightness spills over to high-end DRAM, enterprise SSD, and NAND prices, their gross margin leverage could be stronger than in the previous cycle.

Intel CEO Pat Gelsinger (Note: Correction based on provided text - "陈立武" is likely a phonetic translation for "Pat Gelsinger" in this context) mentioned in a No Priors interview, in essence, that AI infrastructure bottlenecks are spreading from GPUs to areas like memory, CPUs, optical interconnects, power conversion, advanced packaging, and materials. The key point here is not to reframe the issue as Intel's strategy, but to illustrate a larger backdrop: constraints in AI data centers are no longer just about a single GPU; any component limiting cluster expansion and efficiency may gain new pricing power.

Memory is one of the earlier segments observed through trade data. No matter how powerful the GPU, it needs sufficient memory bandwidth and capacity to feed data. As inference and intelligent agent tasks increase, system requirements for memory, storage, and scheduling resources become more complex. The value of the Korean export data lies precisely in grounding the macro-level judgment of "AI infrastructure bottleneck diffusion" into observable changes in memory export value and unit value.

Memory Stocks Still Face Cyclical Constraints

For investors, this memory rally resembles a combination of "accelerating real-world demand plus future earnings re-rating," rather than a pure narrative play. The export data shows there is real-world support for demand and prices; what the market is truly buying is whether 2026 revenue, gross margins, and EPS will continue to be revised upwards.

If subsequent earnings reports validate this line, SK Hynix's valuation premium is the easiest to explain: leading HBM share, customer lock-ins, and high-value product ramp jointly constitute higher visibility. For Samsung, the key lies in whether catching up in high-end HBM translates into actual orders, and whether NAND and SSD prices gain broader support. Micron needs to demonstrate that price increases for high-end DRAM and data center storage can translate into gross margins and guidance.

The risk lies precisely here. Memory remains a strongly cyclical industry; supply expansion, inventory changes, and customer procurement rhythms all affect prices. Preliminary 20-day export data can signal a steeper slope but cannot prove full-year certainty. Rising price per kilogram can indicate higher value density but cannot fully separate the proportion attributable to average selling price increases versus product mix changes. Strong MCP data can serve as a proxy signal related to HBM but cannot be directly equated to HBM exports.

Another risk comes from AI capital expenditure itself. If the pace of investment in power, cooling, packaging, or overall compute infrastructure slows, memory demand would also be affected. Bottleneck diffusion is both the reason for memory gaining a premium and a potential constraint. When other parts of the system become bottlenecks first, the pace of memory demand release could also be delayed.

Earnings Reports Will Determine Whether the Valuation Anchor Can Shift

Ultimately, this re-rating must land on company financials, not remain at the trade data level. The official full-month June export data will first give the market a more complete confirmation: whether the high growth in the first 20 days continues, whether price indicators remain elevated, and whether the strength in NAND and SSD is merely driven by short-term large orders.

More critical verification will come from the Q2 and Q3 earnings reports of SK Hynix, Samsung, and Micron. The market needs to see continued delivery on HBM shipments and prices, simultaneous improvement in DRAM and NAND average selling prices, and data center SSD demand driving gross margin improvement—not just showing up in revenue scale. If gross margins and guidance fail to match the slope suggested by the export data, the re-rating could quickly revert to a cyclical trade.

A more prudent judgment at present is that Korea's first 20-day memory export data is strong enough to support the market in upgrading profit leverage estimates for memory makers and revisiting the discussion on AI infrastructure bottleneck premium. However, it is not yet sufficient to prove the memory industry has decoupled from its cycle. What determines whether the valuation anchor can shift is not how high a single year-on-year number is, but whether prices, product mix, and profit margins can all hold up simultaneously over the coming quarters.