Why Do Crypto Projects Keep Changing Their Names?

**Why Do Crypto Projects Keep Changing Names?**

In the crypto world, changing a project's name is common—over 16% of projects have done so, including major ones like Polygon (formerly Matic Network). This contrasts sharply with traditional businesses, which fiercely protect brand equity.

The core reason is that in crypto, brand loyalty is often weak. Users are frequently investors, airdrop hunters, or yield seekers, not traditional consumers. A name associated with price crashes, hacks, or failed narratives becomes a liability, not an asset. Renaming can be a strategic reset to shed this baggage.

Name changes serve as a potent marketing tool. They can signal a genuine pivot in strategy or scope (e.g., EthSign dropping "Eth" as it expanded). However, they are often used to "narrative surf," rebranding to align with hot trends like AI, RWA, or the metaverse (e.g., Elrond → MultiversX). Critically, renaming is also a PR tactic to distance a project from past failures like security breaches (e.g., Anyswap → Multichain).

The most significant risk emerges when a name change is coupled with a token migration or swap. This process can allow projects to reset exchange price charts, erase visible historical downtrends, and create an illusion of a fresh start. It often facilitates liquidity resets, where low float can be exploited for pumps. More alarmingly, migrations sometimes mask overhauls to tokenomics, introducing substantial new token supply through "ecosystem funds" or "node rewards," effectively diluting existing holders.

The fundamental issue isn't renaming itself, which can be valid for strategic evolution. The problem is when it functions as an escape from history—a way to avoid accountability for past mistakes, failed promises, and poor performance. When a project announces a rebrand, the critical questions are: What tangible new capability or strategy does it represent? Has the tokenomics changed? And what part of its past is it most trying to make users forget?

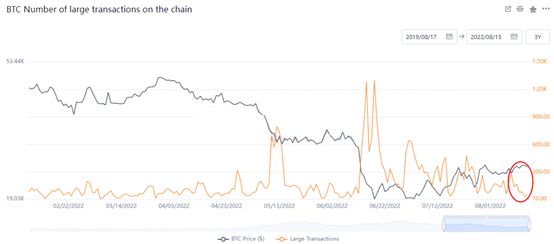

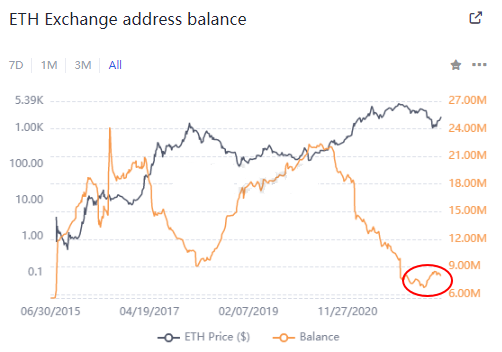

marsbit31 dk önce