Мем-токены — один из главных трендов на этом буллране. Они известны невероятной волатильностью, из-за чего стоимость такого актива может прыгнуть в разы буквально за несколько часов или даже минут, после чего так же быстро падает. Воспользоваться данной особенностью решил основатель Barstool Sports Дейв Портной. Несмотря на наличие у него миллионов долларов, он решил поставить на кон свою репутацию ради пары десятков тысяч.

Дейв Портной и монета MONTOYA

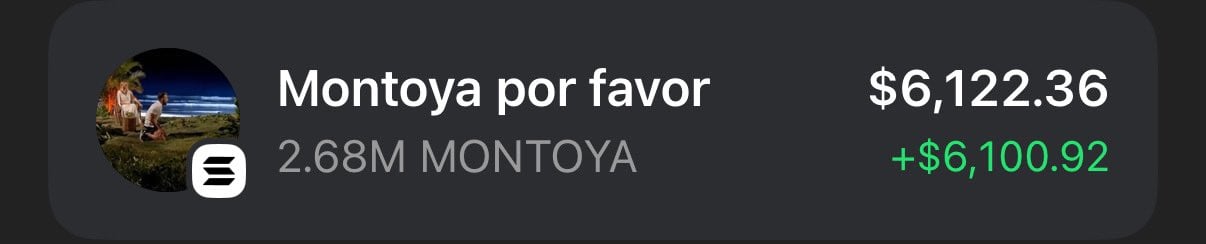

Вчера вечером Портной опубликовал скриншот собственного криптокошелька Phantom, на котором находилось 2.68 миллиона монет MONTOYA. Свой пост предприниматель сопроводил следующей подписью, которую приводит Decrypt.

Оу. Дейви научился торговать шиткоинами и уже получил миллиард процентов прибыли на первой сделке.

Скриншот мем-токена MONTOYA на кошельке Дейва Портного

Интерфейс кошелька дал понять, что этот мем-токен резко вырос за последний день. А это вполне предсказуемо привлекло трейдеров из числа подписчиков Портного, которые взялись покупать MONTOYA в попытке заработать.

Из-за таких операций рыночная капитализация мема довольно быстро прыгнула с 2.8 до 10 миллионов долларов.

Однако основатель Barstool Sports не учёл один важный момент: пользователи блокчейна довольно быстро определили кошелёк Дейва с помощью точного количества не самого популярного токена — речь идёт об адресе, который начинается с 5rkPD. Ну а это позволило им следить за операциями Портного с только что пропиаренным им криптоактивом.

Оказалось, что спустя пять минут Портной продал все 2.68 миллиона токенов за 118 SOL. Эквивалент операции составил приблизительно 24 тысячи долларов. Предприниматель прокомментировал ситуацию в следующей реплике.

Чёрт. У меня слишком много власти. Я заработал 25 тысяч долларов случайным образом. Это настоящая азартная игра, причём мой твит за секунды поднял капитализацию проекта с 2 до 10 миллионов долларов.

Продажа крупной суммы токенов в одной транзакции вполне предсказуемо сказалась на курсе токена. Он снизился в несколько раз, причём транзакция Портного действительно привела к обвалу графика.

Операция по продаже MONTOYA Дейвом Портным на графике криптовалюты

Представитель Barstool отреагировал на публикацию и посоветовал Дейву быть осторожнее, поскольку он знает адрес кошелька предпринимателя. Впрочем, Портного это не смутило — в ответ он вспомнил о прозрачности блокчейна.

Я хочу, чтобы люди знали, чем я занимаюсь. Я не пытаюсь что-то скрывать. Вот почему мне это нравится — все могут видеть каждый мой шаг.

Как бы там ни было, с тех пор курс MONTOYA не восстановился. А значит покупатели мем-токена после твита Портного скорее всего находятся в минусе — и в первую очередь из-за соответствующей рекламы миллионера.

15-минутный график мем-токена MONTOYA

На этом приключения Дейва с мем-токенами не закончились. Спустя час он купил мем-токен MVP на 152 SOL, однако уже через десять минут избавился от накоплений. Прибыль по данной позиции составила 48 тысяч долларов. Реплика была следующей.

Я выхожу. Сегодня с помощью шиткоинов я превратил 10 тысяч долларов в 75 тысяч. Это всё равно что играть в ракеты на DraftKings. Я в восторге!

После раскрытия блокчейн-адреса Портного некоторые поклонники взялись отправлять монеты на его кошелёк. Вдобавок энтузиасты начали создавать мемы по мотивам собаки Дейва или компании Barstool Sports.

Стоит отметить, что дебютный опыт Портного с криптовалютами был неудачный. В начале августа 2020 года он потратил миллион долларов на покупку биткоинов. Однако спустя несколько недель Дейв слил монеты после обвала рынка, зафиксировав минус в 25 тысяч долларов.

По итогу дня Портной опубликовал новое видео и спросил, отправится ли он в тюрьму за это. По словам предпринимателя, подобное не должно нарушать законы.

Эксперты не смогли дать однозначный ответ по поводу произошедшего. И хотя многие инвесторы наверняка потеряли деньги на криптоактиве, прорекламированным Дейвом, его блокчейн-адрес был известен. Соответственно, Портной не скрывал своих действий и по сути действовал открыто. А значит привлечь его к ответственности за такое может не получиться.

Канье Уэст и мем-токен

Тему криптовалют ночью также затронула другая знаменитость — исполнитель Канье Уэст. На протяжении суток он публиковал неоднозначные твиты, которые вызвали непонимание подписчиков рэпера. В частности, он затрагивал темы антисемитизма, сексизма и даже Гитлера.

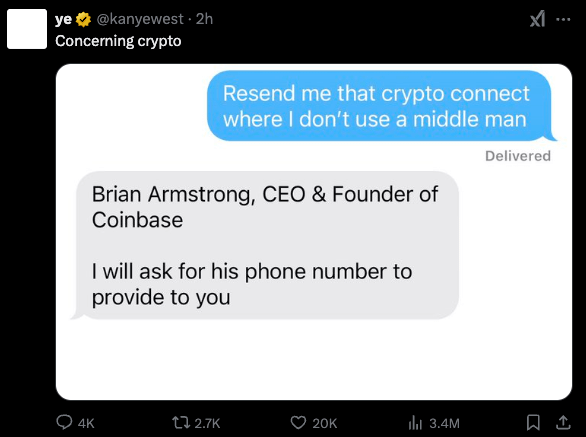

Публикации также затронули цифровые активы. Судя по одной из записей Уэста, он планирует связаться с руководителем криптовалютной биржи Coinbase Брайаном Армстронгом, сообщает The Block. Вот скриншот публикации, в которой ему обещают раздобыть контакты предпринимателя.

Твит Канье Уэста о криптовалютах

Уэст написал следующее.

Когда люди зарабатывают все эти деньги с помощью монет, это является наличными или концепцией?

Также исполнитель рассказал, что кто-то предложил ему 2 миллиона долларов за участие в рекламе фейкового токена. Судя по всему, схема предполагала публикацию адреса контракта криптоактива 32 миллионам его фолловеров, причём затем Уэст должен был заявить, что его учётная запись якобы была взломана.

Вот реплика.

Мне предложили 2 миллиона долларов за мошенничество с моим сообществом. Оставшимся его членов. Я сказал «нет» и прекратил работать с тем человеком, который это предложил.

Исполнитель Канье Уэст

Оба случая показывают, что мем-токены действительно являются одним из главных хитов этого буллрана. Впрочем, у них есть и обратная сторона. Всё же число таких монет исчисляется десятками миллионами, из-за чего капитал инвесторов размывается. А это не позволяет рынку выдать продолжительный рост и тем самым мешает продолжению нынешнего буллрана.