想象一下,一个计算机能够像人类一样学习和适应的世界。它们可以自主决策、识别模式,并不断提升任务效率。这一切都源于人工智能,AI正在彻底改变各个行业,提高效率、推动创新和发展。

但问题是:AI并非魔法。它需要大量数据来学习,而原始数据本身并没有太大价值。数据必须经过组织、分类和解释,才能对机器有意义。这个过程被称为AI数据标注。

AI数据标注类似于教机器如何看、听和理解事物。举例来说,如果你想让自动驾驶汽车在遇到行人或红灯时停下来,在AI的训练过程中,你需要在用于训练的图片和视频中标注这些对象。这需要手动识别并标记图像和视频中的行人和红灯。通过提供这些注释数据进行AI模型训练,汽车才能在现实中学会识别和响应行人和红灯。

图1. 此图为数据标注示例,行人用蓝色标记,车辆用橙色标记,用于训练AI模型进行物体识别。

市场分析

AI数据标注在医疗、零售、汽车和银行等各个行业中,对创造新产品和服务至关重要。随着需求的增加,行业收入显著提升,未来预期还会继续增长。随着更多公司采用AI并开发新的学习方法,数据标注的需求不断上升。

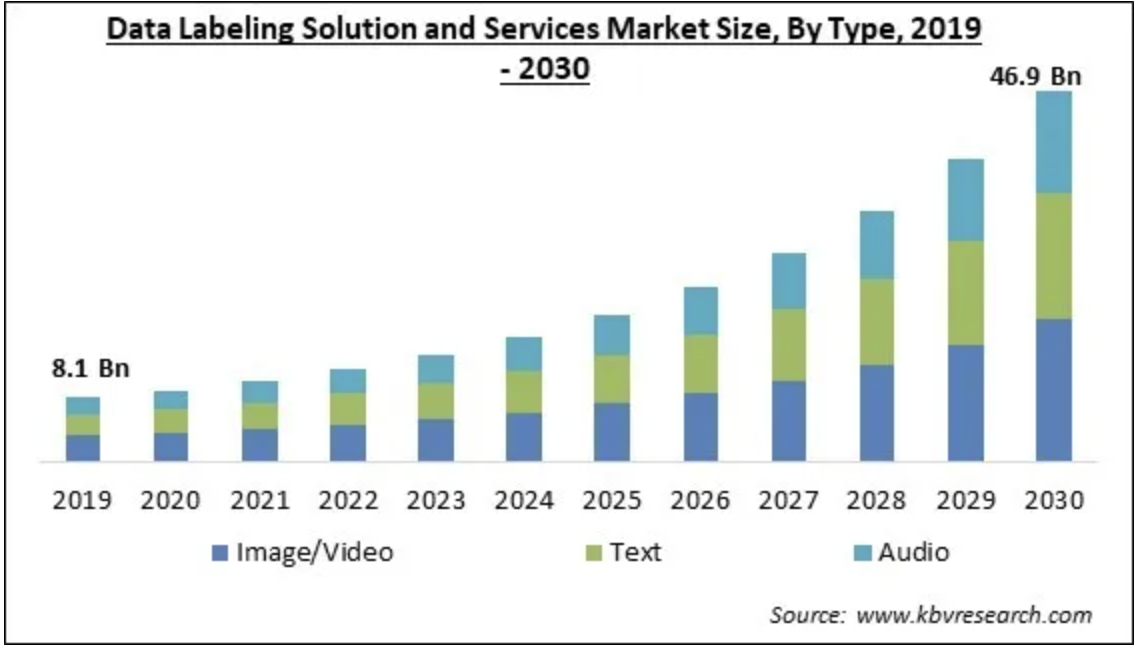

全球数据标注解决方案和服务市场预计将从2022年的116亿美元增长到2030年的469亿美元,年均复合增长率(CAGR)预计为19.5%。

(数据来源:https://www.kbvresearch.com/data-labeling-solution-and-services-market/)

图2. 数据标注市场规模

OORT Datahub 如何革新数据标注行业

图3. OORT Datahub 的工作原理

注释:

a. OORT Storage:企业级去中心化存储解决方案。

b. Olympus 区块链:OORT 的Layer-1区块链,用于记录和验证数据收集和标注过程。

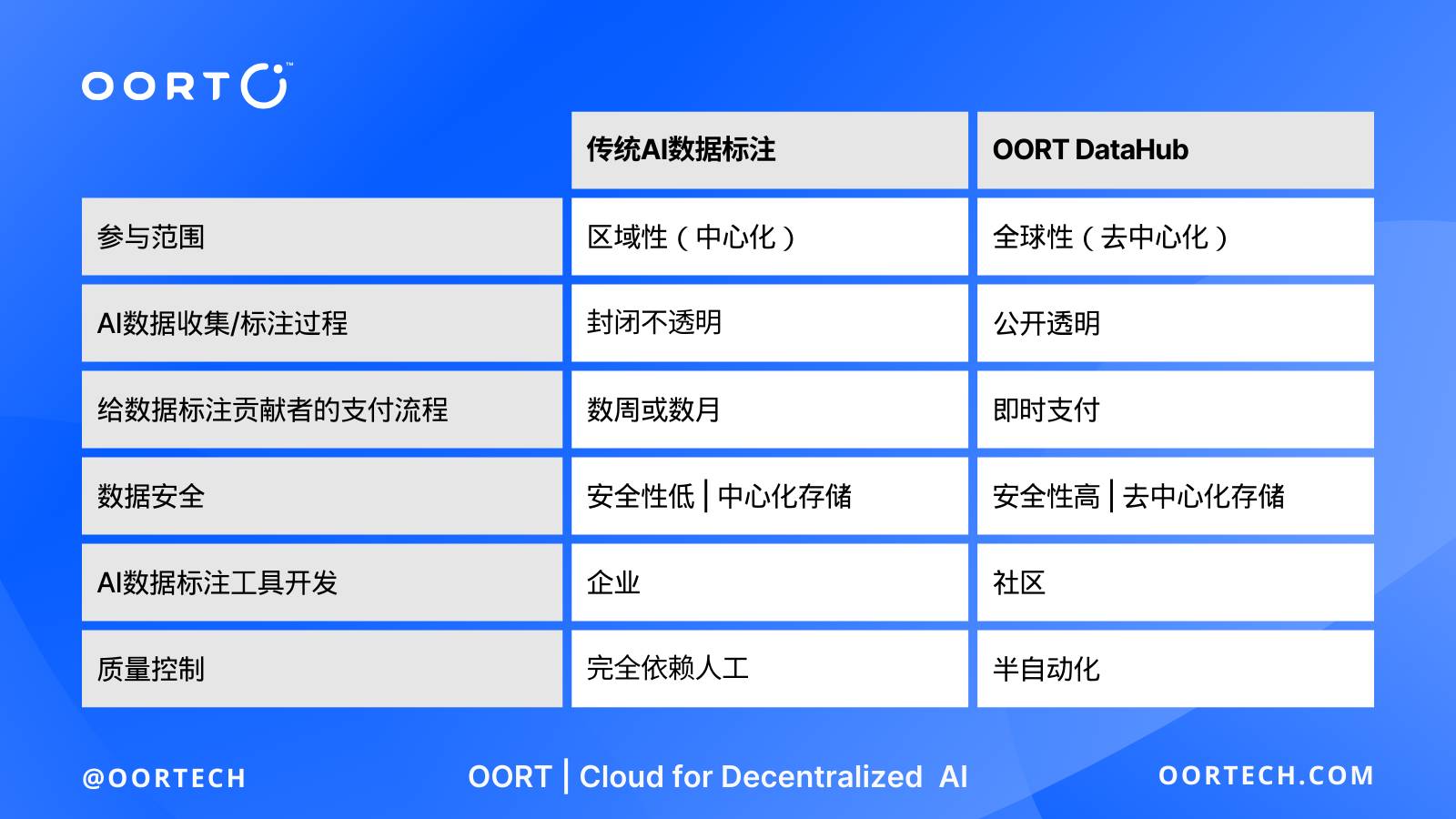

传统的数据标注行业高度依赖人工且缺乏透明度,导致工人报酬极低。利用区块链和加密货币可以显著改善这些问题。通过区块链技术和加密货币,AI数据标注在全球范围内变得更安全、更便捷。OORT Datahub开创了这一新方法,称之为去中心化数据标注。图4详细比较了 OORT Datahub 和传统数据标注行业。

图4. OORT Datahub 与传统数据标注产品的比较

全球参与

去中心化的数据标注让世界各地的人都能参与进来,并通过工作赚取加密货币。这种方法打破了传统平台的限制,比如 Toloka 只在特定国家招聘数据采集和标注人员,并且对这些人员的跨境支付困难。类似于个人通过比特币进行无国界的交易,OORT Datahub贡献者可以在世界任何地方轻松赚取额外收入。

公开透明

区块链增强了AI数据标注流程的透明度。从任务完成到支付的每一步都记录并验证在区块链上。这种透明度有效减少了数据标记的错误和争议,增加了AI项目与参与数据标注用户之间的信任。在OORT Datahub中,OORT使用其高性能的Layer-1区块链——Olympus Protocol——来保障数据预处理流程的透明度。

数据安全

DataHub上的所有AI数据都将存储在OORT Storage中。OORT Storage是OORT企业级的去中心化存储解决方案。原始数据和标注数据都会被加密并分片存储在不同位置,确保它们不会被篡改或未经授权访问。相比之下,集中式云平台管理的数据更容易因为漏洞受到黑客攻击。

即时支付

使用加密货币支付加快了支付流程,使跨境支付更快且成本更低。智能合约确保任务的高效分配,并且完成任务后,对贡献者的支付在几分钟内即可完成。相比之下,传统方法既慢又复杂,通常需要数周或数月。更重要的是,OORT Datahub 引入了一种新的奖励机制,Datahub的参与者将收到NFT作为额外奖励。这些NFT使持有者拥有分享未来数据销售收入的权利,为用户提供了更高的收入潜力。

社区协作工具开发

OORT DataHub 鼓励社区成员,共同开发AI数据收集和标注的小工具。在开发者、数据专家和AI项目的参与下,这些小工具会更加高效和实用。

质量控制

采集和标注的数据质量一直是数据标注行业的痛点。低质量的数据将严重影响AI的训练效果。OORT DataHub 的特色在于其诚实证明(PoH)共识算法,这是一种有人工参与的半自动化质量控制机制。该算法能够很快验证已提交的数据标签的准确性,而不像传统公司那样依赖手动验证,容易遗漏和造成人为错误。

总之,OORT DataHub通过简化和加速数据收集与标注过程,提高了效率。借助区块链技术和去中心化存储服务,还增强了数据预处理的安全性和隐私性,进而鼓励全球用户的参与和贡献。