Authored by: Foresight Ventures

TL;DR

- Tokenized stocks are the breakthrough sector in the current Real World Asset (RWA) cycle—the market has hit a new all-time high of $800 million, growing 30x year-to-date, with a monthly trading volume of $1.8 billion.

- Core value proposition: Bypass geographical restrictions and settlement delays of traditional brokers, enabling 24/7 global access to US stocks with near-instant settlement.

- Three architectures are vying for dominance:

- Instant Execution Model (Ondo, CyberAlpha)—leads in capital efficiency.

- Inventory Model (xStocks, Backed)—excels in DeFi composability through debt structures under Swiss law.

- Direct Ownership Model (Securitize)—offers the most complete legal rights but is constrained by transfer restrictions and has limited on-chain composability.

- The market has effectively formed a duopoly: Ondo leads with a 53% share, driven by liquidity engineering; Backed/xStocks hold a 23% share, leveraging regulatory arbitrage.

- Technology is no longer the moat—regulation is. Building a cross-border licensing system across the US, EU, and offshore jurisdictions is currently the most difficult-to-replicate competitive barrier.

- Platforms face a fundamental trilemma: they can only optimize two of the following three aspects simultaneously—Liquidity/Speed, Regulatory Security/Shareholder Rights, DeFi Composability.

- The industry is bifurcating into two paths: Incremental (DTCC integration, increasing efficiency) and Revolutionary (direct on-chain issuance, full disintermediation).

- Conclusion: The fusion of the $150 trillion global stock market with blockchain infrastructure is no longer just a thesis—it is happening.

1. Market Status Analysis: Deciphering the 'Silent Boom'

The Real World Asset (RWA) sector is undergoing structural transformation, with tokenized stocks emerging as the breakthrough sector of this cycle. The overall RWA ecosystem market cap has surpassed $800 million, growing 30x year-to-date. The integration of traditional equity assets with blockchain infrastructure signifies a fundamental shift in capital market design. This 'silent boom' is not merely an asset migration but a modernization of global liquidity—replacing fragmented traditional systems with a unified, programmable financial layer.

The following core data confirms this leap from experimental to institutional grade:

- Market Cap Achievement: As of December 2025, the sector's market cap has reached a historic high of approximately $800 million.

- Liquidity Velocity: Monthly trading volume has surged to $1.8 billion, indicating an active secondary market.

- Adoption Density: The network currently supports 50,000 monthly active addresses and 130,000 total holding addresses.

This growth trajectory is fundamentally supported by blockchain eliminating the settlement friction and access barriers that have long plagued traditional finance (TradFi).

As the capital market's need for settlement efficiency becomes increasingly urgent, how tokenization addresses the chronic problems of TradFi through technological means has become the core of strategic competition in the industry.

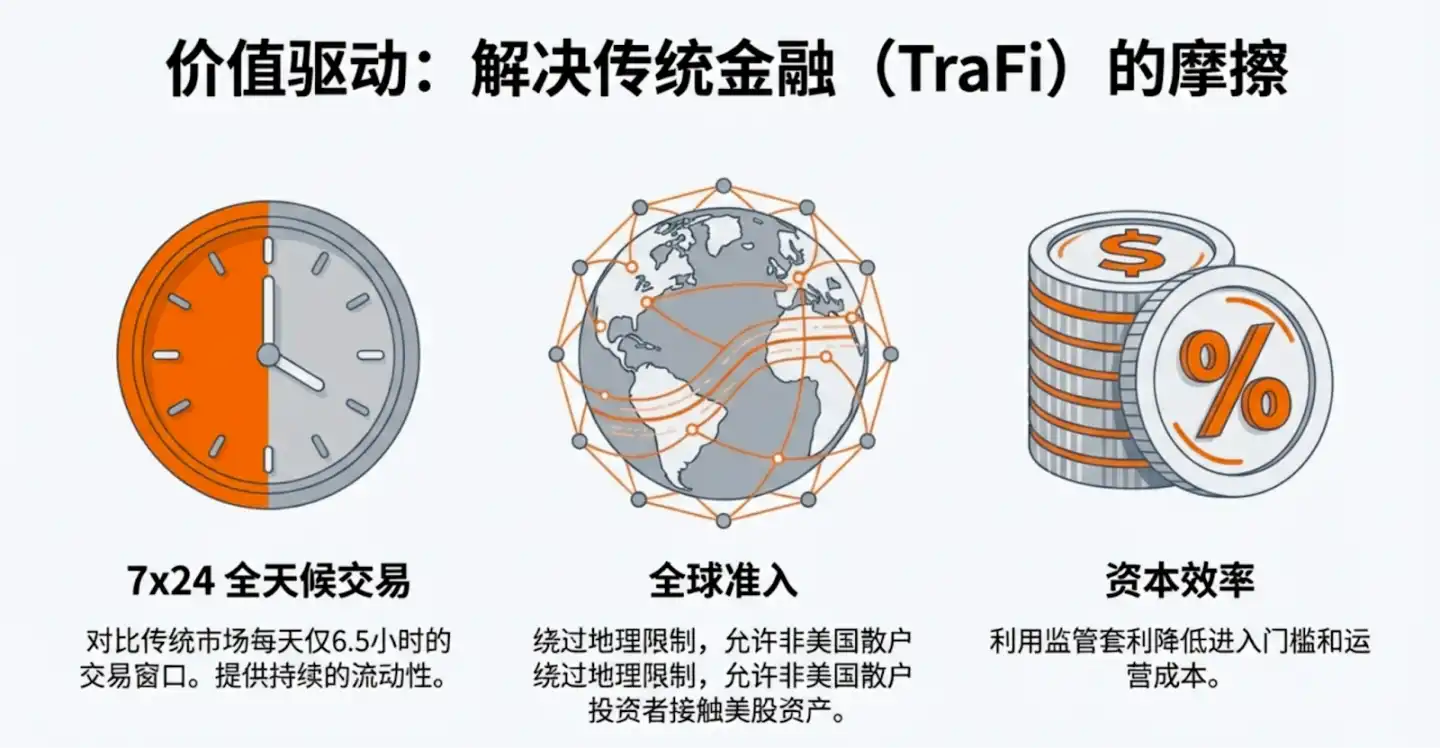

2. Strategic Value Drivers: Solving TradFi's Friction Points

Traditional equity markets have long been constrained by the physical boundaries of legacy systems: geographical silos, restricted trading hours, and lengthy settlement cycles. The failure of the T+2 settlement system during the 2021 Robinhood/GME event, which forced brokers to restrict trading due to margin shortfalls, is a classic case study of TradFi's 'efficiency短板' (efficiency shortcoming).

Tokenization offers strategic premium through an 'Efficiency Triple-Threat':

- 24/7 Trading: Traditional markets operate only 6.5 hours a day. Tokenization eliminates 'opening gap' risk, allowing investors to react in real-time to global macro events.

- Global Accessibility: Completely breaks down geographical and broker barriers, providing non-US retail investors seamless access to high-demand US stock exposure, achieving 'borderless capital'.

- Capital Efficiency: Enables T+0 settlement through digital infrastructure, reducing collateral tie-up and operational costs caused by settlement delays.

Tokenization is not just an optimization; it bypasses the administrative bottlenecks of traditional securities businesses by providing a global, 24/7 liquidity layer. In an era of 'capital efficiency scarcity', platforms that enable instant settlement and cross-border distribution will hold pricing power.

However, the path to realizing this value driver is not singular; different product architectures determine a platform's long-term moat and risk exposure.

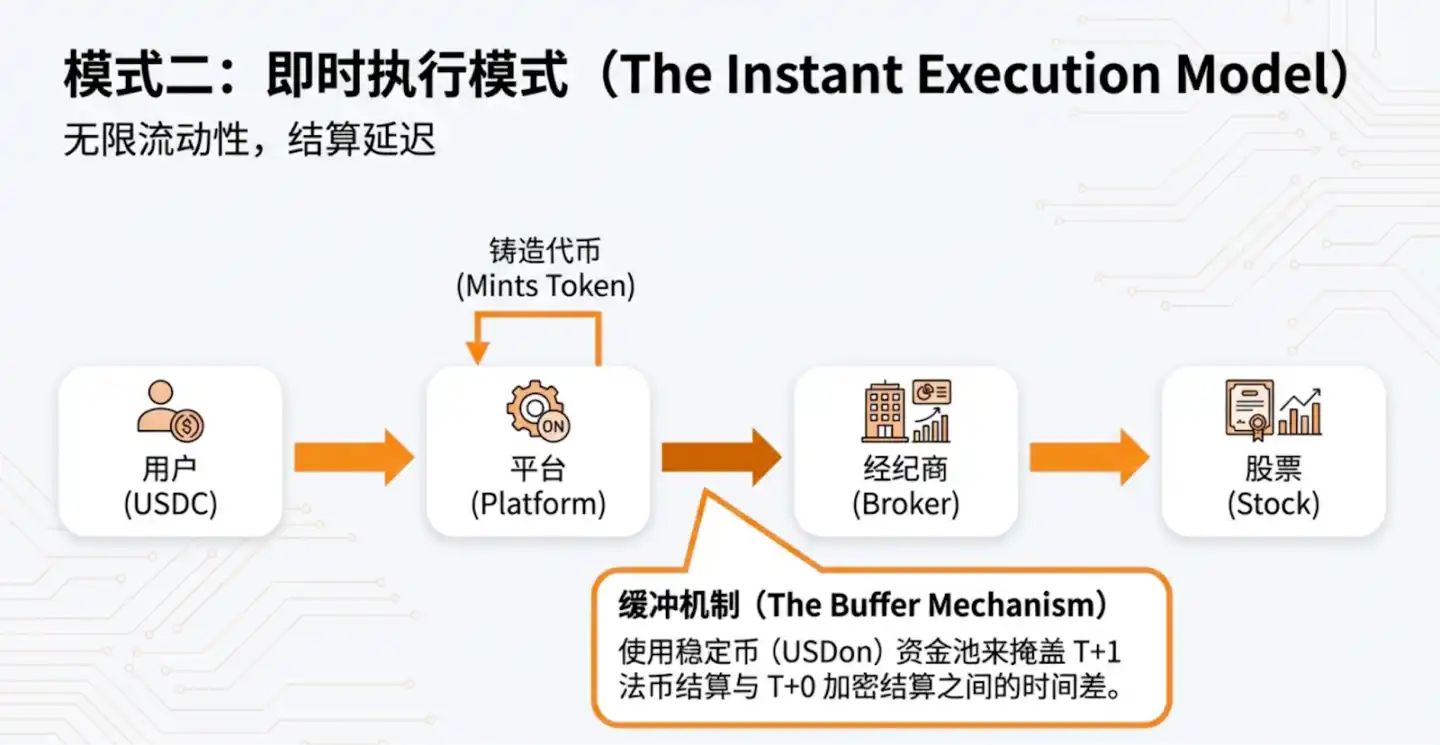

3. Tokenization Architecture Comparative Analysis: Three Core Models

The choice of product architecture is a strategic pivot determining scalability, DeFi composability, and systemic risk characteristics.

Three-Model Framework

- Inventory Model (e.g., xStocks, Backed): A 'pre-funded liquidity' solution. The issuer or market maker buys stocks in advance and mints tokens, depositing them in a warehouse ready for sale.

- Instant Execution Model (e.g., Ondo, CyberAlpha): An 'on-demand liquidity' solution. Stock purchase and token minting are only triggered when a user confirms an order.

- Direct Ownership Model (e.g., Securitize, Galaxy Digital): A 'purist' solution where the token *is* the legal share. Ownership is recorded directly on the company's cap table by a transfer agent, granting investors full shareholder rights including voting and dividends, but involves strict transfer restrictions.

Architectural Trade-off Comparison

As trading volumes advance to higher levels, the technical challenge shifts to effectively bridging the gap between traditional and digital settlement cycles.

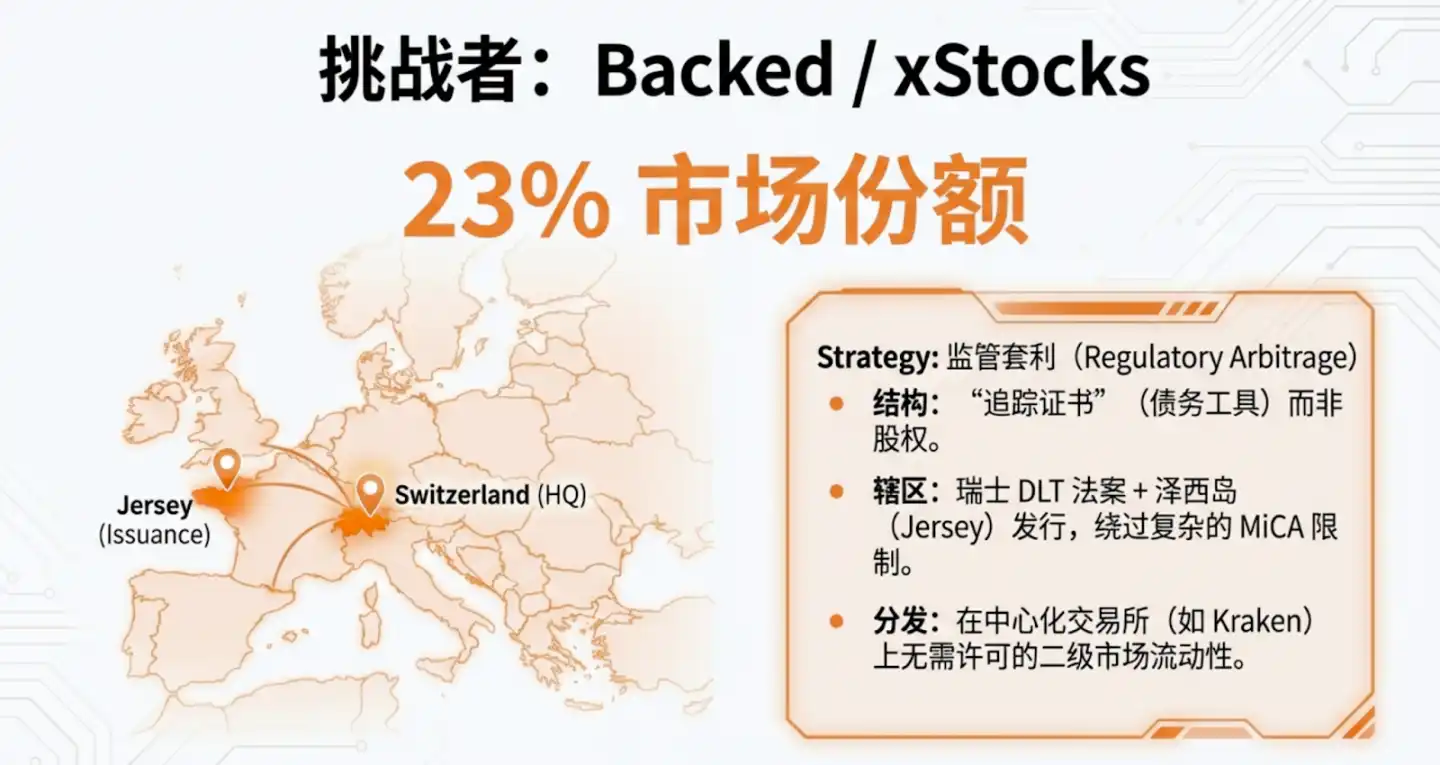

4. Competitive Landscape: Market Leaders and Challengers

The current competitive landscape shows a clear 'duopoly' and 'strategic differentiation'.

- Ondo Finance (53% share): The absolute dominator. Its revenue engine relies on a ~0.1% trading fee spread, with estimated annualized revenue of $30M-$40M. Its core moat is a highly sophisticated USDon buffer pool and an extensive network of licensed institutional partners.

- Backed / xStocks (23% share): Broke through using 'Legal Alpha'. By structuring products as tracker certificates (debt) under the Swiss DLT Act, they cleverly circumvented MiCA's restrictions on the transfer of direct equity tokens, enabling free flow and composition within the DeFi ecosystem.

- Robinhood (Walled Garden): Although it possesses the strongest combination of MiFID II and MiCA licenses, the lack of token extractability creates an isolated ecosystem, missing out on the open premium of DeFi.

'So What?' Level: Competition has shifted from 'user count' to a game of 'regulatory arbitrage' and 'capital efficiency'. Backed sacrificed direct equity rights through its debt structure in exchange for unlimited DeFi interoperability—a precise strategic trade-off.

5. Global Compliance Matrix: Building the Regulatory Moat

In the RWA space, 'license aggregation' is a more formidable moat than technology itself.

- US Model (Hard Mode): The cornerstone of success is the 'trident' combination of Broker-Dealer, ATS, and Transfer Agent licenses. Ondo acquired this full suite of capabilities through its acquisition of Oasis Pro, mastering the complete closed loop from onboarding to secondary market matching.

- EU Model (Passporting Mode): Leveraging the 'passporting' system of MiCA and MiFID II, companies obtaining licenses in Liechtenstein (e.g., Ondo approved by FMA) or Cyprus (e.g., xStocks approved by CySEC) can operate in 30 countries.

- Specialized Pilots: Securitize, through a DLT pilot license from Spain's CNMV, gained permission to operate as a trading and清算 system, directly challenging the role of traditional CSDs (Central Securities Depositories).

'So What?' Level: Ondo's compliance architecture is a 'masterclass in financial engineering': ensuring tax neutrality through a BVI-based issuing entity, accessing underlying assets through US-licensed entities, achieving bankruptcy remoteness through daily proof of reserves from Ankura Trust, and finally enabling global compliant distribution through **BX Digital (Switzerland)**.

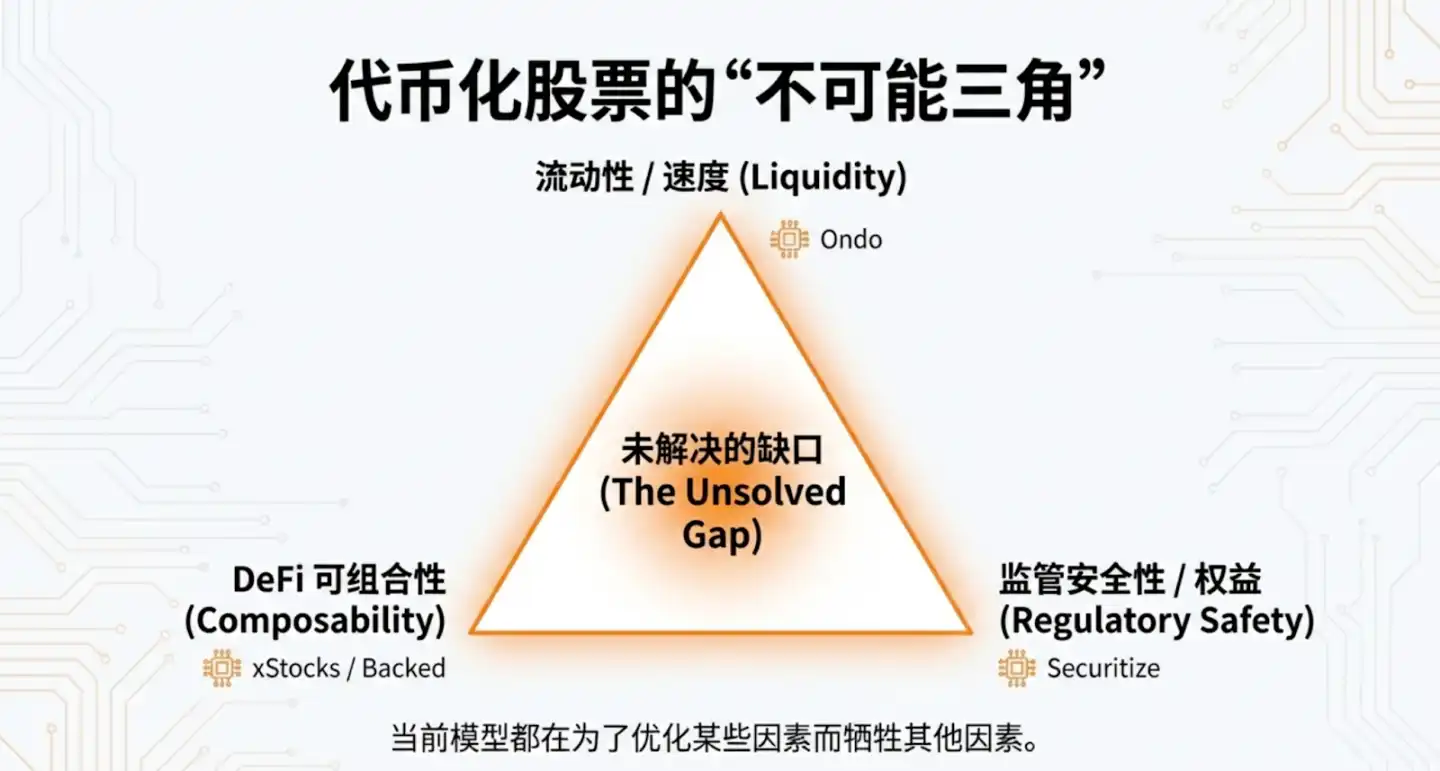

6. Strategic Outlook: Solving the Tokenized Stock 'Impossible Trinity'

The industry must balance the following three elements as it scales:

- Liquidity / Speed: Exemplified by Ondo, optimized through buffer mechanisms.

- Regulatory Security / Direct Rights: Exemplified by Securitize, pursuing SEC-compliant underlying direct ownership.

- DeFi Composability: Exemplified by Backed, achieving on-chain asset flow through debt structures.

The market is currently bifurcating into two paths:

- Evolutionary Path: Centered on DTCC integration, providing T+0 efficiency increments for incumbent financial institutions.

- Revolutionary Path: Native on-chain issuance, exemplified by Securitize/Galaxy Digital, aiming for complete disintermediation.

7. Summary and Core Insights

The migration of the global $150 trillion equity market onto the blockchain is now irreversible.

- Institutional Maturity: The 30x growth and milestones like Galaxy Digital mark the industry's transition from the conceptual phase into the deep waters of licensed competition.

- Model Superiority: The Instant Execution model, with its极高的 capital efficiency, has gained an early advantage in the current liquidity war.

- Licenses as Barriers: Platforms capable of navigating both US underlying asset access (ATS/BD licenses) and global (EU MiCA/Offshore BVI) compliant distribution will build an insurmountable long-term moat.

'Financial transformation is never overnight. Direct ownership is the ultimate goal, but integration and optimization with the DTCC is the necessary bridge to the future.'