С момента закрытия Ормузского пролива 2 марта глобальные потоки нефти объемом около 17,8 млн баррелей в день были перекрыты. За один только март Brent подорожал почти на 60%, а WTI — примерно на 53%. Это самый резкий месячный рост для контрактов Brent с момента их появления в 1988 году, побивший рекорд в 46%, установленный во время войны в Персидском заливе в 1990 году.

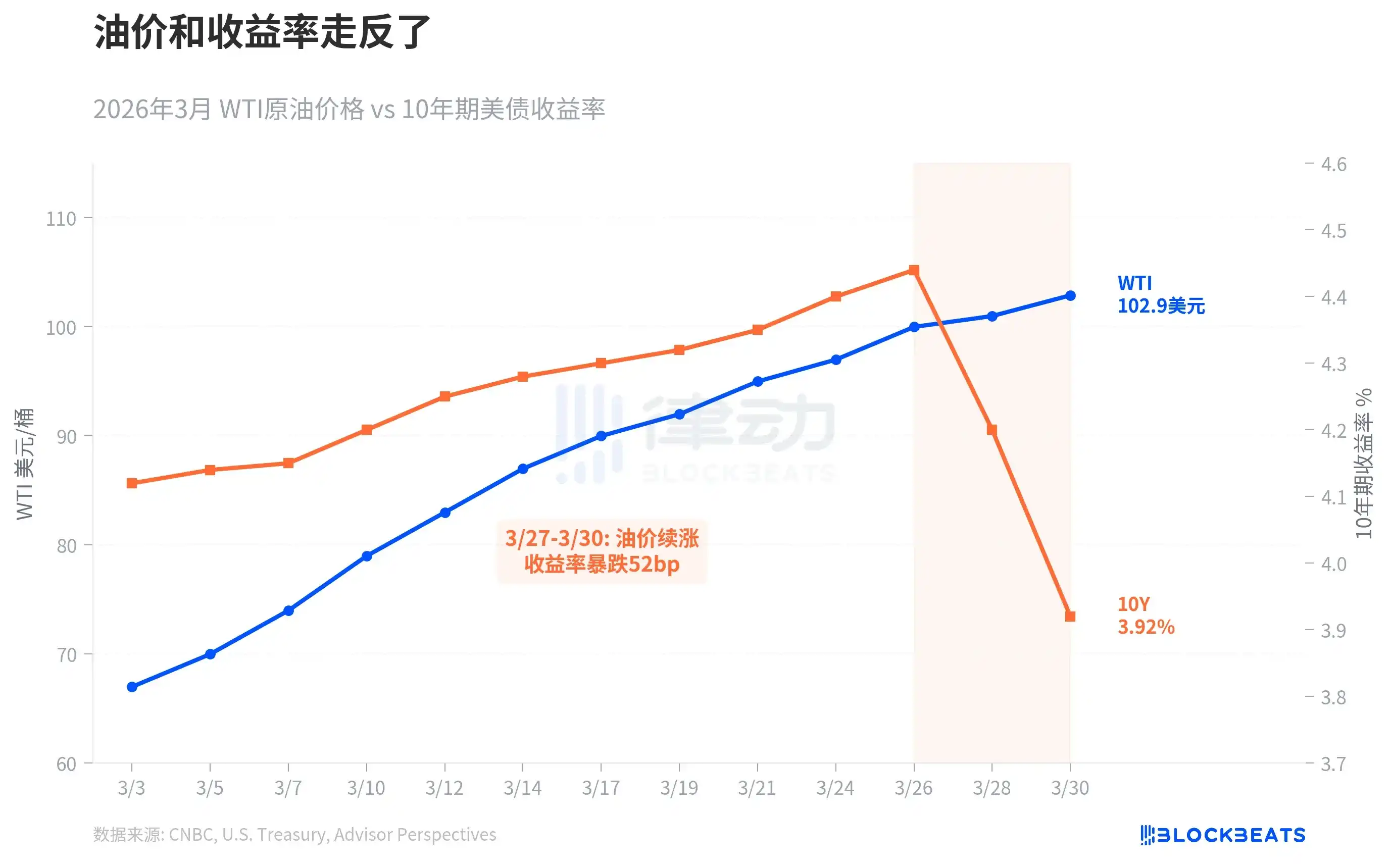

По логике, резкий рост цен на нефть подстегивает инфляционные ожидания, и доходность облигаций должна расти. Большую часть последних двадцати лет цены на нефть и доходность 10-летних казначейских облигаций США действительно имели положительную корреляцию. Но на этот раз они пошли вразрез.

В первые три недели марта они еще двигались синхронно вверх. WTI вырос с 67 до 100 долларов, а доходность 10-летних облигаций поднялась с 4,15% до 4,44%. Перелом произошел между 27 и 30 марта: цены на нефть продолжили расти, а доходность обрушилась с 4,44% до 3,92%, упав на 52 базисных пункта за три торговые сессии и пробив психологически важную отметку в 4%.

Это типичный «приток в убежище», рынок облигаций делает вывод: риски для роста开始 перевешивают инфляционные риски. Исследовательская компания Oxford Economics прямо заявила: «Риски для экономического роста开始 перевешивать инфляционные риски». Другими словами, рынки боятся не меньше инфляции, а больше боятся рецессии.

Такое расхождение встречается нечасто, но каждый раз, когда оно появляется, последующая история оказывается не очень хорошей.

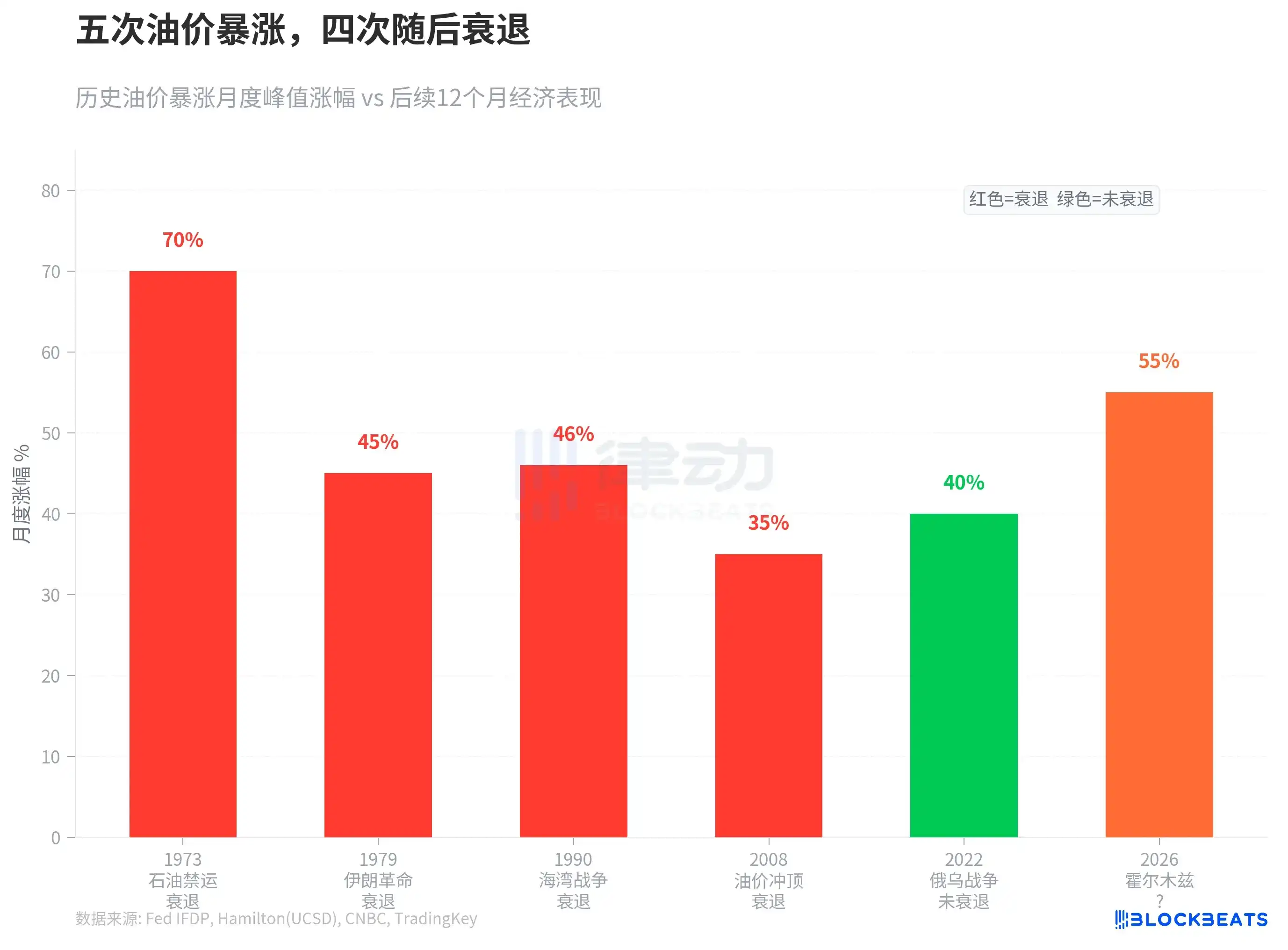

За последние полвека было пять случаев, когда цены на нефть резко росли более чем на 35% за короткий период. После нефтяного эмбарго 1973 года ВВП США упал на 4,7%. После иранской революции 1979 года глобальный ВВП отклонился от трендового роста на 3 процентных пункта. Во время войны в Персидском заливе в 1990 году США вступили в кратковременную рецессию. В 2008 году цены на нефть достигли пика в 147 долларов, и хотя основной причиной той рецессии был финансовый кризис, нефтяной шок ускорил экономический спад. Единственным исключением стал скачок цен на нефть из-за войны в Украине в 2022 году, который не спровоцировал рецессию, но代价 — это инфляция, самая сильная за 40 лет.

Рост в марте 2026 года превысил все вышеперечисленные случаи. Согласно исследованию экономиста ФРС Джеймса Гамильтона, между нефтяным шоком и рецессией不存在 механической связи, но «чем больше читый рост цен на нефть, тем значительнее сдерживающее влияние на потребление и инвестиции». Goldman Sachs уже повысила вероятность рецессии в США до 30%, а консалтинговая компания EY-Parthenon дает цифру в 40%.

Скорость реакции рынка также оказалась на удивление быстрой.

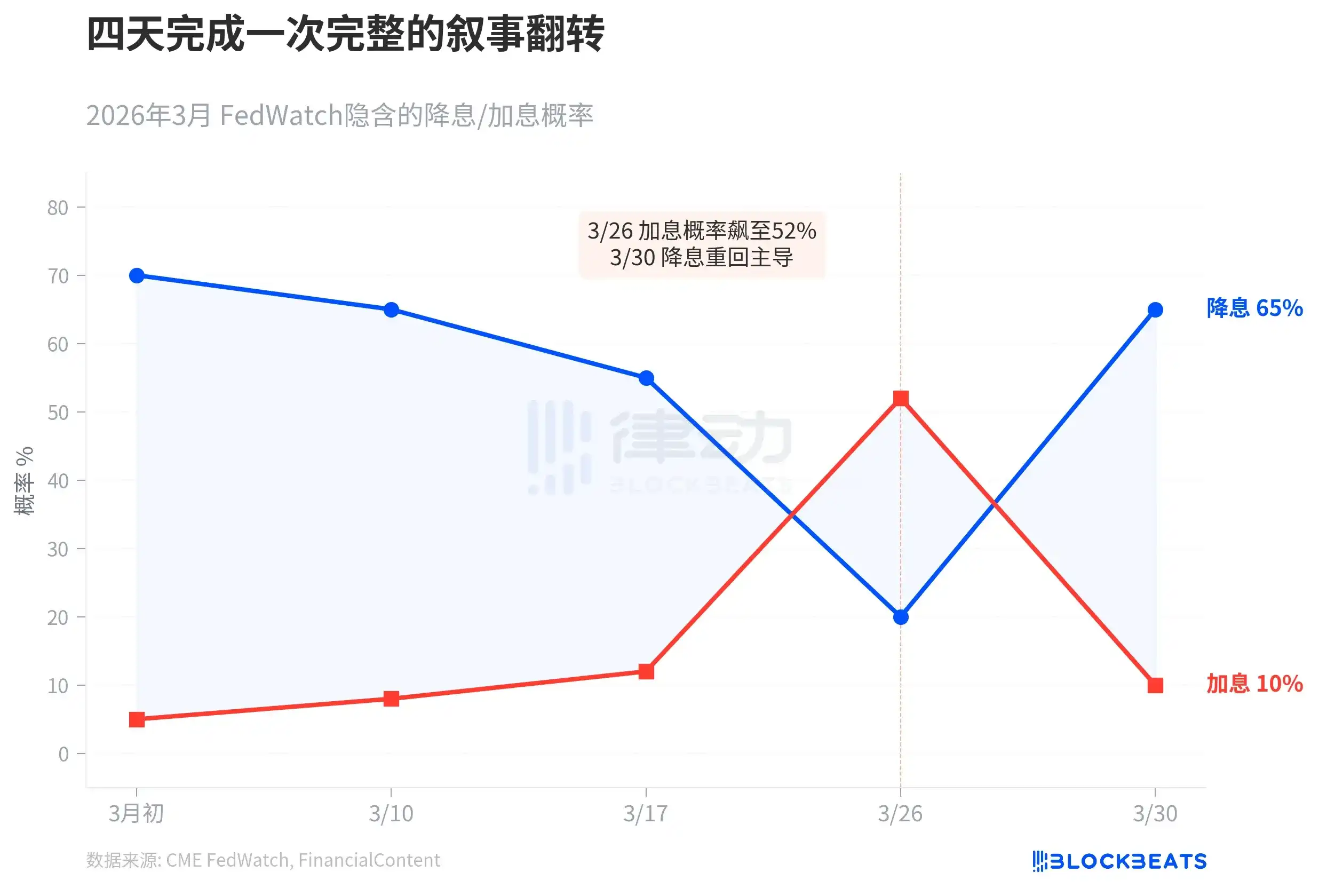

В начале марта инструмент CME FedWatch показывал, что рынок ожидает трех снижений ставок в течение года, с вероятностью снижения в июне на 70%. Затем цены на нефть продолжали расти, 26 марта индекс цен на импорт США подскочил на 1,3%, а будущий председатель ФРС Кевин Уорш намекнул, что нейтральная ставка может быть выше. В тот же день вероятность повышения ставки в течение года взлетела до 52%, а доходность 10-летних облигаций достигла 4,35%. FinancialContent определил этот день как «Великий ястребиный разворот» (The Great Hawkish Pivot).

Четыре дня спустя нарратив полностью перевернулся. 30 марта данные о доверии потребителей резко ухудшились, производство неожиданно сократилось, а доходность 10-летних облигаций обрушилась до 3,92%. Согласно报道 FinancialContent, ставки рынка на поворот ФРС в сторону смягчения (鸽派转向) в мае выросли до 65%. Goldman Sachs заявила, что рынок ошибся в направлении ставок. В тот же день Пауэлл в Гарвардском университете сказал студентам, что ФРС «еще не дошла до момента, когда必须 решать, игнорировать ли шок от войны» (look through), но подчеркнул, что «ключевым является закрепление инфляционных ожиданий».

Согласно报道 Axios, заявление Пауэлла было воспринято рынком так: ФРС не хочет ни повышать ставки для борьбы с инфляцией, ни спешить с их снижением для спасения экономики, а ждет, чтобы увидеть, является ли этот шок предложения временным или持久性的. Но рынок облигаций уже не может ждать.

Если история является ориентиром, то стратег Citigroup Маккормик выразился最直白: впереди стагфляция,这对债券不好, 对股票也不好.

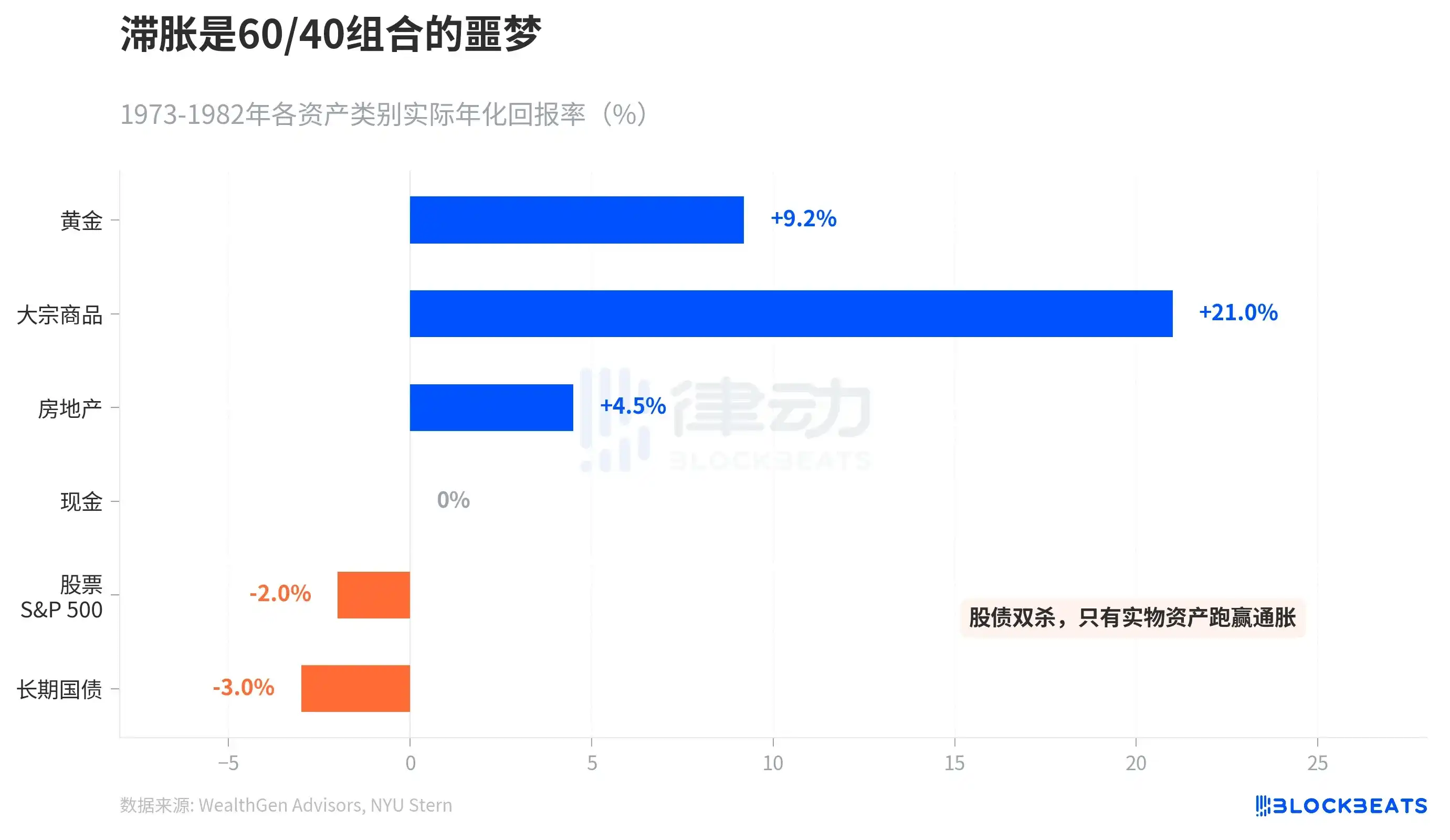

Великая стагфляция с 1973 по 1982 год дала отчет о доходности активов. Золото показало реальную годовую доходность +9,2%, индекс сырьевых товаров (S&P GSCI) вырос на 586% за десять лет, недвижимость — на +4,5%. А реальная годовая доходность S&P 500 составила -2%, долгосрочных гособлигаций — -3%. Согласно историческим данным NYU Stern, в 1979 году долгосрочные гособлигации показали убыток в -8,6%.

Традиционный инвестиционный портфель 60/40 (60% акций + 40% облигаций) был раздавлен в стагфляции. Обежать инфляцию смогли только实物资产. Societe Generale прогнозирует среднюю цену Brent в апреле на уровне 125 долларов, а «достоверный пик» может достичь 150 долларов. Goldman Sachs настроена稍温和一些, ожидая среднюю цену в 115 долларов в апреле, но предполагая, что если Ормузский пролив восстановит навигацию в течение шести недель, то к концу года цена упадет до 80 долларов.

Рынок облигаций уже сделал выбор за всех: между инфляцией и рецессией он ставил на рецессию.