Amid the global wave of digital currencies, Singapore is emerging as an "overseas hub" for international crypto institutions. Whether it's stablecoin issuance, digital asset trading, or institutional-grade custody and payment clearing, global fintech companies are seeking compliant and stable landing paths here.

Behind this lies a systematic regulatory framework established by the Monetary Authority of Singapore (MAS): clear legal frameworks, comprehensive licensing systems, and a regulatory philosophy that balances risk and innovation, setting Singapore apart from major jurisdictions worldwide. Unlike the fragmented regulatory environment in the United States and the high compliance costs in Europe, Singapore offers a predictable and actionable compliance path.

This series of reports will systematically interpret Singapore's digital asset ecosystem from five dimensions: regulatory framework, licensed institutions, financial institution practices, international cooperation, and institutional advantages, showing how its system attracts global institutions while providing reference for the Asia-Pacific and global markets.

Regulatory Framework and Main Licensing System

(I) Core Regulatory Authority

The Monetary Authority of Singapore (MAS) is the unified regulatory authority for Singapore's digital asset and financial markets, fully responsible for the regulation of payment systems, digital currencies, fintech, and related financial services. MAS implements a management model combining functional regulation and risk-oriented regulation for digital asset activities through a combination of legislation and licensing systems.

(II) Regulatory Laws and Overall Framework

1. Payment Services Act (PSA)

The Payment Services Act is the foundational legal framework for digital asset regulation in Singapore. The act defines digital currencies/cryptocurrencies as "Digital Payment Tokens (DPTs)" and brings related services such as payment, exchange, transfer, and custody into the payment services regulatory system.

The act clarifies the following core requirements:

-

Digital Payment Token services require licensed operation;

-

Sets Anti-Money Laundering (AML) and Countering the Financing of Terrorism (CFT) obligations;

-

Clarifies compliance standards such as capital adequacy, customer asset segregation, and risk management;

-

Ensures financial stability and consumer protection through continuous supervision.

2. Financial Services and Markets Act (FSMA)

The Financial Services and Markets Act further expands Singapore's regulatory boundaries for digital asset activities on the basis of the PSA. Unlike the PSA's primary regulatory logic targeting "services provided to local Singaporean customers," the FSMA's regulatory scope extends to all institutions registered in Singapore or with business premises there, and which use Singapore as an operational base to conduct digital asset-related business, even if their service targets are located overseas. Specifically, any activity involving the issuance, trading, matching, custody, or related services of digital currencies through a Singapore entity falls under the FSMA's regulatory purview.

The act officially生效 (takes effect) from 2025. MAS has clearly required that any institution established in Singapore but providing digital asset services only to overseas customers must obtain the corresponding license within the specified period, otherwise facing high fines and even criminal liability, plugging the regulatory loophole of using Singapore as an "offshore channel" at the institutional level.

(III) License Types and Regulatory Division

Currently, the core licenses for the crypto asset field in Singapore mainly include the DPT (Digital Payment Token Service) license under the Payment Services Act and the DTSP (Digital Token Service Provider) license.

1. Licenses under the Payment Services Act (DPT System)

According to the Payment Services Act, entities involved in digital payments, remittances, e-money, or cryptocurrency services need to possess one of the following licenses:

(1) Standard Payment Institution (SPI) License – Applicable to payment service providers with smaller business scales;

(2) Major Payment Institution (MPI) License – Applicable to institutions with larger transaction volumes, involving cross-border payments or digital asset services.

It is particularly important to note that currently, only MPI license holders are permitted to conduct Digital Payment Token (DPT) related business; SPI license holders have not yet been granted this permission.

Therefore, the so-called "DPT license" in the industry essentially refers to an MPI license that includes the scope of digital payment token services.

2. DTSP License (Digital Token Service Provider)

According to the provisions of the Financial Services and Markets Act, entities without a DTSP license are prohibited from providing any digital token-related services to overseas clients through their business premises in Singapore. The DTSP license primarily targets digital asset institutions providing "external services," its regulatory scope is broader than the DPT system, and its compliance requirements are also stricter.

After the implementation of the new DTSP policy, Singapore systematically cleaned up crypto enterprises characterized by "establishing local entities but lacking substantive operations." Except for a few institutions with genuine business and compliance capabilities, most substandard enterprises needed to cease related business or relocate their entities away from Singapore before June 30, 2025, effectively forming a round of regulatory clearance.

According to industry analysis, if an institution is already under the following regulatory frameworks, it usually does not need to apply for a DTSP license separately:

(1) Already holds a license under the Payment Services Act;

(2) Has obtained an exemption under the Payment Services Act;

(3) Already holds a relevant license under the Securities and Futures Act or the Financial Advisers Act.

It should also be noted that what is referred to as "DTSP licensed institutions" in media reports, in MAS's public information system, mostly corresponds to "MPI license holders including digital payment token services," rather than independently published DTSP license holders.

As of now, MAS has not publicly released a complete list of DTSP license holders; related information is mainly reflected through regulatory documents and policy explanations.

Singapore's Digital Asset Licensing System

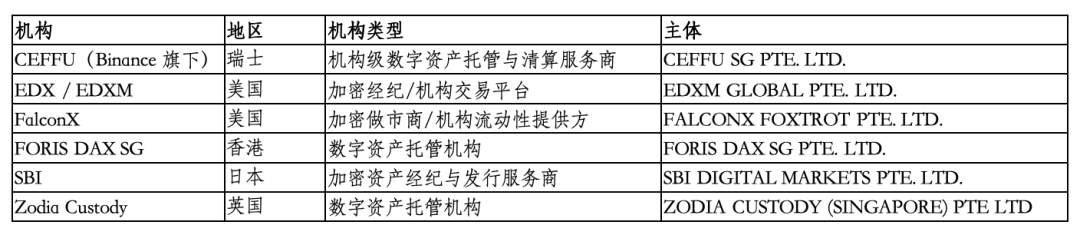

As of the writing date, MAS has issued MPI licenses including the Digital Payment Token Service business scope to 36 institutions with international backgrounds.

In terms of the composition of licensed entities, although some institutions have US or other overseas backgrounds, or are controlled by multinational groups, they must use locally registered legal entities as the licensed主体 (subject) when conducting related business in Singapore. Relevant compliance obligations, regulatory responsibilities, and business scopes are all borne by this Singapore entity to MAS in accordance with the Payment Services Act, reflecting Singapore's consistent regulatory principle of "territorial regulation, entity responsibility."

(I) MPI Licensing/Exemption Status of Global Institutions

1. Licensed Status (List sorted A-Z)

2. Exempt Status (List sorted A-Z)

3. Unique Business Situations

-

December 2025: Coinbase launched prediction market features in the US, not applicable to Singapore users.

-

November 2024: Paxos Singapore and DBS Bank issued the USDG dollar stablecoin.

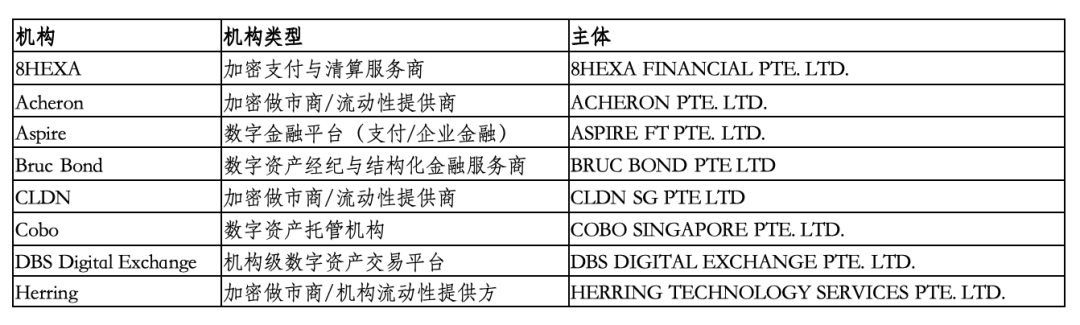

(II) MPI Licensing/Exemption Status of Local Singapore Institutions

1. Licensed Status (List sorted A-Z)

2. Exempt Status (List sorted A-Z)

3. Unique Business Situations

December 2025: Crypto platform Crypto.com announced cooperation with the largest local bank, DBS Group, to enhance fiat currency payment functions, allowing local users to more conveniently use SGD and USD deposit and withdrawal services. The same month, StraitX announced plans to launch its Singapore dollar stablecoin XSGD (issued in 2020) and US dollar stablecoin XUSD on the Solana public chain in early 2026.

-

November 2025: Grab and StraitsX developed a digital wallet supporting stablecoin payments.

-

September 2025: OKX Singapore launched stablecoin payment functionality at GrabPay merchants.

-

August 2025: Singapore's DBS Bank launched tokenized structured notes on Ethereum. The same month, Volkswagen Singapore cooperated with FOMO Pay to support digital currency payments.

So far, we have梳理 (sorted out) Singapore's digital currency regulatory framework, core laws, and licensing system, and also understood the composition of licensed institutions and market structure. It can be seen that Singapore is not simply "crypto-friendly," but has built a robust and attractive digital asset ecosystem through clear systems and strict license management.

In the next part, we will continue in-depth, taking you to understand how local financial institutions participate in digital asset practices, international cooperation and innovation trends, and the practical significance of Singapore's system for global institutions.

Twitter:https://twitter.com/BitpushNewsCN

Bitpush TG Discussion Group:https://t.me/BitPushCommunity

Bitpush TG Subscription: https://t.me/bitpush