Автор оригинала: Е Чжэнь

Источник оригинала: Wall Street Insights

Индустрия частного кредитования США сталкивается с двойным давлением — сокращением ликвидности и переоценкой активов. Поскольку инвесторы спешат вывести средства, а крупные финансовые институты Уолл-стрит сокращают кредитные линии, этот огромный рынок объемом 1,8 триллиона долларов находится в шатком положении.

Согласно отчету Financial Times, гиганты частного кредитования Cliffwater и Morgan Stanley недавно ввели ограничения на выкуп своих фондов объемом в десятки миллиардов долларов. В первом квартале эти полуликвидные фонды столкнулись с резким увеличением количества запросов на вывод средств. Масштабы оттока капитала вынудили руководство активировать «шлюзы», чтобы избежать продажи базовых неликвидных активов со скидкой.

В то время как сторона финансирования испытывает давление, кредитные учреждения также сталкиваются с ужесточением условий со стороны крупных банков. JPMorgan Chase недавно уведомил соответствующие учреждения о снижении стоимости залога по некоторым кредитам для программного обеспечения в их инвестиционных портфелях. Хотя эта мера не привела к немедленным уведомлениям о внесении дополнительного обеспечения, она напрямую сократила объем будущего финансирования для соответствующих фондов, что свидетельствует о полной переоценке рисков данного сектора традиционной банковской системой.

В основе этого двустороннего давления лежит логика арбитража чистой стоимости активов (NAV). Поскольку стоимость связанных активов на публичных рынках резко упала, частные кредитные учреждения не синхронно скорректировали оценку своих активов, что побудило инвесторов спешить с выводом средств по балансовой стоимости, превышающей справедливую рыночную стоимость. Эта цепная реакция, аналогичная банковской панике, не только усиливает давление на ликвидность фондов, но и заставляет рынок заново оценить истинную стоимость активов частного кредитования.

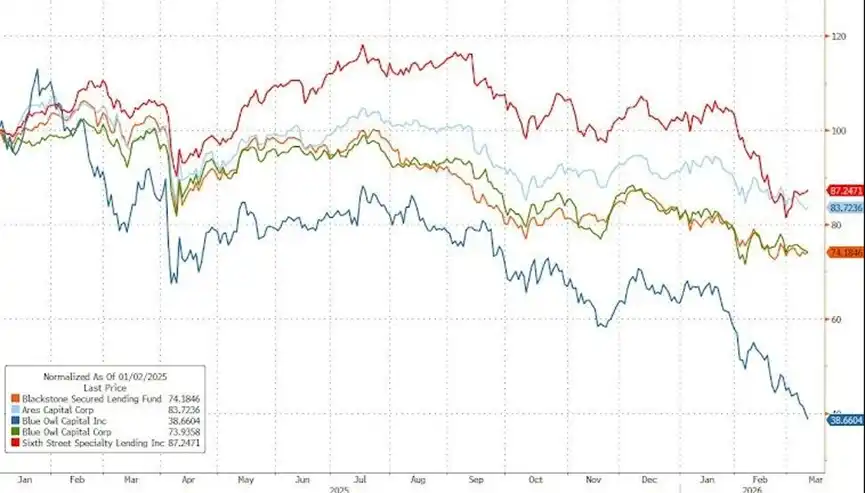

(Акции компаний частного кредитования продолжают снижаться)

Волна выкупов распространяется, полуликвидные фонды проходят серьезное испытание

Согласно отчету Financial Times, Cliffwater в первом квартале ограничил выкуп своего флагманского фонда объемом 33 миллиарда долларов (CCLFX). Фонд получил запросы на выкуп, составляющие 14% от общего объема долей, и в конечном итоге удовлетворил лишь около половины, выкупив 7% долей.

Спустя несколько часов после действий Cliffwater, Morgan Stanley также уведомил инвесторов своего фонда North Haven Private Income Fund объемом 7,6 миллиарда долларов об ограничении вывода средств. Запросы на выкуп в первом квартале выросли до 10,9%, и в конечном итоге было удовлетворено лишь 45,8% от этого объема.

В последние месяцы эта тенденция распространилась по всей отрасли. HPS недавно установила лимит выкупа в 5% для своего флагманского фонда для состоятельных клиентов. Фонд Bcred под управлением Blackstone выполнил запросы на выкуп в полном объеме после того, как они достигли 7,9% от чистой стоимости активов, в то время как Blue Owl и Ares ранее также удовлетворили высокие запросы на выкуп, хотя Blue Owl в этом году уже ввел постоянное ограничение на выкуп для другого фонда.

Cliffwater привлек 16,5 миллиарда долларов в прошлом году, и темпы его роста были наравне с отраслевым гигантом KKR. Однако эта модель, зависящая от независимых брокеров, управляющих деньгами розничных инвесторов, делает ее более уязвимой перед колебаниями рыночных настроений.

Для решения проблемы, согласно отчету, Cliffwater привлекает 1 миллиард долларов за счет продажи кредитных портфелей и ожидает привлечения 3 миллиардов долларов новых обязательств в этом квартале, чтобы компенсировать отток средств. В письме к инвесторам компания подчеркнула, что фонд принес доходность 8,9% в 2025 году, а чистый леверидж составил всего 0,23x, что значительно ниже, чем у большинства аналогичных инструментов.

Этот отток капитала подчеркивает риски, с которыми сталкиваются многие новые полуликвидные фонды, которые изначально рекламировались как способ вложения в частный кредит, но из-за того, что их базовые активы редко торгуются, они могут предлагать возможности для продажи лишь время от времени.

Завышенная оценка провоцирует арбитраж, highlighting риск паники

Основной движущей силой спешки инвесторов к выводу средств является арбитраж чистой стоимости активов.

Согласно анализу колонки Bloomberg, акции программного обеспечения и связанные с ними долги на публичных рынках уже значительно упали в этом году, но учреждения частного кредитования, как правило, держат кредиты до погашения и не синхронно корректируют оценку своих портфелей.

Это отставание в ценообразовании создает арбитражное пространство. Если фонд заявляет, что его кредит стоит 100 долларов, а инвесторы считают, что его реальная рыночная стоимость составляет всего 98 долларов, инвесторы попытаются выкупить его по балансовой стоимости в 100 долларов.

Эта логика действий спровоцировала динамику, аналогичную банковской панике: если фонд выплачивает 100 долларов, стоимость активов оставшихся инвесторов будет дополнительно размыта, что побудит больше людей присоединиться к очереди на выкуп. Это создает огромное давление на интервальные фонды, обещающие частичную ликвидность, перед лицом инвесторов.

Чтобы развеять опасения по поводу непрозрачности оценки, некоторые учреждения пытаются повысить прозрачность. Джон Зито, со-президент подразделения по управлению активами Apollo Global Management, заявил, что компания готовится начать ежемесячно сообщать о чистой стоимости активов своих кредитных фондов, а конечной целью является переход на ежедневную отчетность по NAV и привлечение第三方 оценки.

JPMorgan переходит в наступление, ужесточает leveraged финансирование

В то время как внутренние средства утекают, внешние источники leverage частных учреждений также подвергаются проверке. Согласно отчету Financial Times, JPMorgan主动 снизил оценку некоторых корпоративных кредитов в портфелях частных учреждений, эти кредиты в основном сконцентрированы в секторе программного обеспечения, который считается особенно уязвимым на фоне冲击 искусственного интеллекта.

JPMorgan имеет специальный пункт в своем бизнесе по финансированию частного кредитования, который сохраняет за ним право переоценивать активы в любое время, в то время как большинство других банков обычно ждут触发条件, таких как дефолт по процентам, чтобы предпринять действия. Аналитики СМИ指出, эта мера旨在 заблаговременно сократить доступные кредитные линии для этих фондов, чтобы при необходимости действовать своевременно, а не ждать кризиса.

Это ужесточение早有预兆. Генеральный директор JPMorgan Джейми Даймон ранее неоднократно公开 выражал осторожную позицию в отношении сектора частного кредитования. Высокопоставленный руководитель банка Трой Рорбауэр в феврале этого года заявил, что по сравнению с коллегами по отрасли JPMorgan становится более консервативным в отношении рисков частного кредитования. Один управляющий фондом также подтвердил, что JPMorgan за последние три месяца стал «заметно жестче» в предоставлении backend leverage.

Логика扩张 отрасли нарушена, существуют сомнения относительно последующих рисков

Быстрое расширение индустрии частного кредитования в высокой степени зависит от leveraged финансирования, предоставляемого регулируемыми банками. С конца 2020 года частные учреждения привлекли сотни миллиардов долларов и быстро приобрели способность напрямую конкурировать с банками в финансировании крупных leveraged выкупов.

Однако большое количество базовых активов сформировалось в период бума удаленной работы, когда оценки компаний программного обеспечения были высоки. Поскольку ожидания денежных потоков компаний пересматриваются в сторону понижения, соответствующие долги будут постепенно погашаться в ближайшие годы, и рыночные условия к тому времени будут сильно отличаться от условий эмиссии.

В настоящее время учреждения частного кредитования настаивают на том, что корпоративные software компании продолжают расти, и ожидают, что кредиты будут продолжать обслуживаться в обычном режиме. Хотя никакие другие банки пока четко не последовали ужесточающей позиции JPMorgan, по мере того как крупные банки率先 переоценивают стоимость активов, а давление со стороны розничных инвесторов на вывод средств остается высоким, ожидается, что внимание рынка к ликвидности и прозрачности оценки в этой отрасли будет продолжать расти.