Author: Thejaswini M A

Original Title: The Frozen Fortune

Compiled and Arrangement: BitpushNews

The house—your parents never saw it as an investment. They bought it because they needed a place to live, because the mortgage was affordable on a single income back then, because the schools in the community were excellent, because it was the default choice people made at the time. They painted the living room twice, replaced the roof once, and argued about renovating the kitchen for years without ever doing it. They raised children in it, grew old in it. In the process, without really meaning to, they built the most valuable asset they would ever own.

Now, they are struggling to pay medical bills, and that house is worth $1.2 million.

A number keeps recurring in financial research: $124 trillion.

This is the estimated value of assets expected to pass from the older generation to the younger one over the next 25 years. Analysts call it the "Great Wealth Transfer." In media portrayals, it sounds like pure good news for the heirs.

But is it really?

Much of this wealth being transferred is illiquid. A large portion is real estate. These are houses bought by Baby Boomers when prices were reasonable, paid down over decades, and appreciated in value, ultimately becoming the primary store of their wealth.

The generation inheriting these houses grew up watching those same prices put homeownership out of their reach. Now, these houses are about to them—illiquid, emotionally burdensome, legally complex, and increasingly impractical.

This is the problem the "$124 trillion" headline fails to capture.

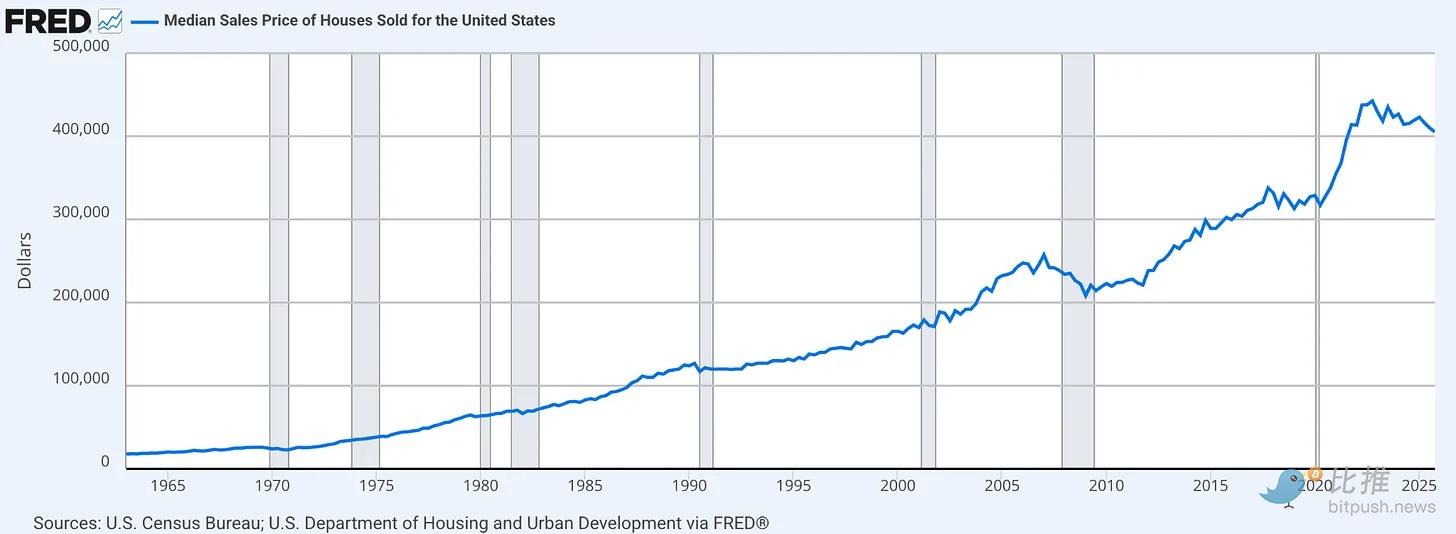

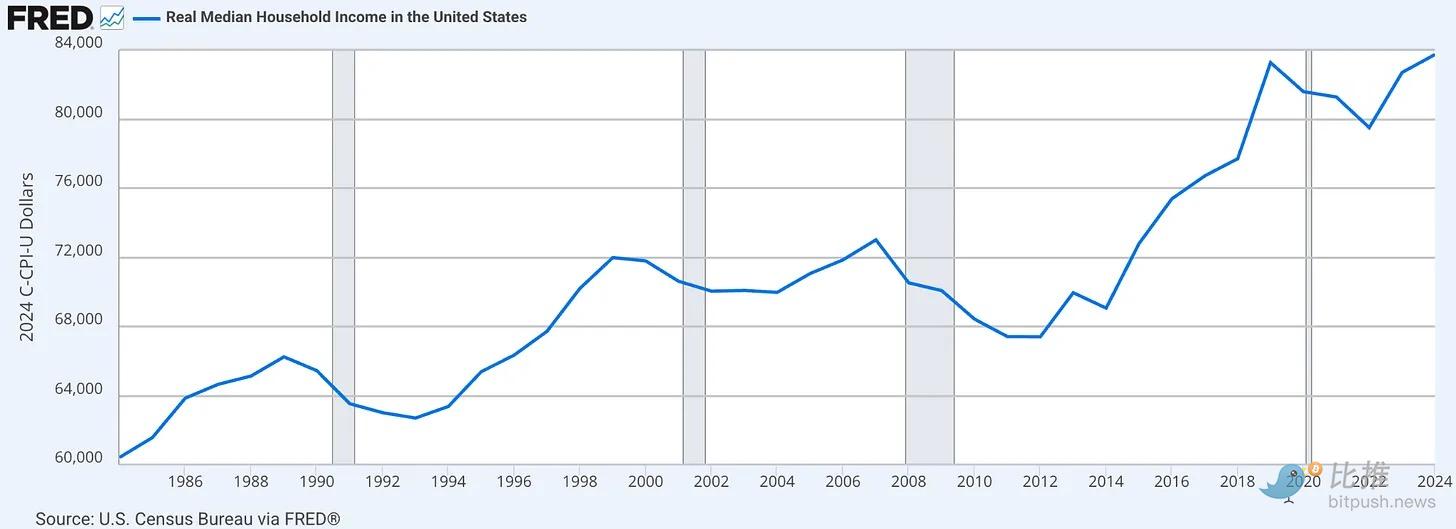

To understand why this matters, you must understand what happened to housing from the 1960s to now. It changed categories. It started as shelter, a place to live, and slowly became the primary financial instrument for the American middle class. For families outside the high-income bracket, a house isn't one asset among many; it is the only asset. Real estate equity represents the largest single item on the median American family's balance sheet, dwarfing the combined value of retirement accounts, stocks, and all other assets.

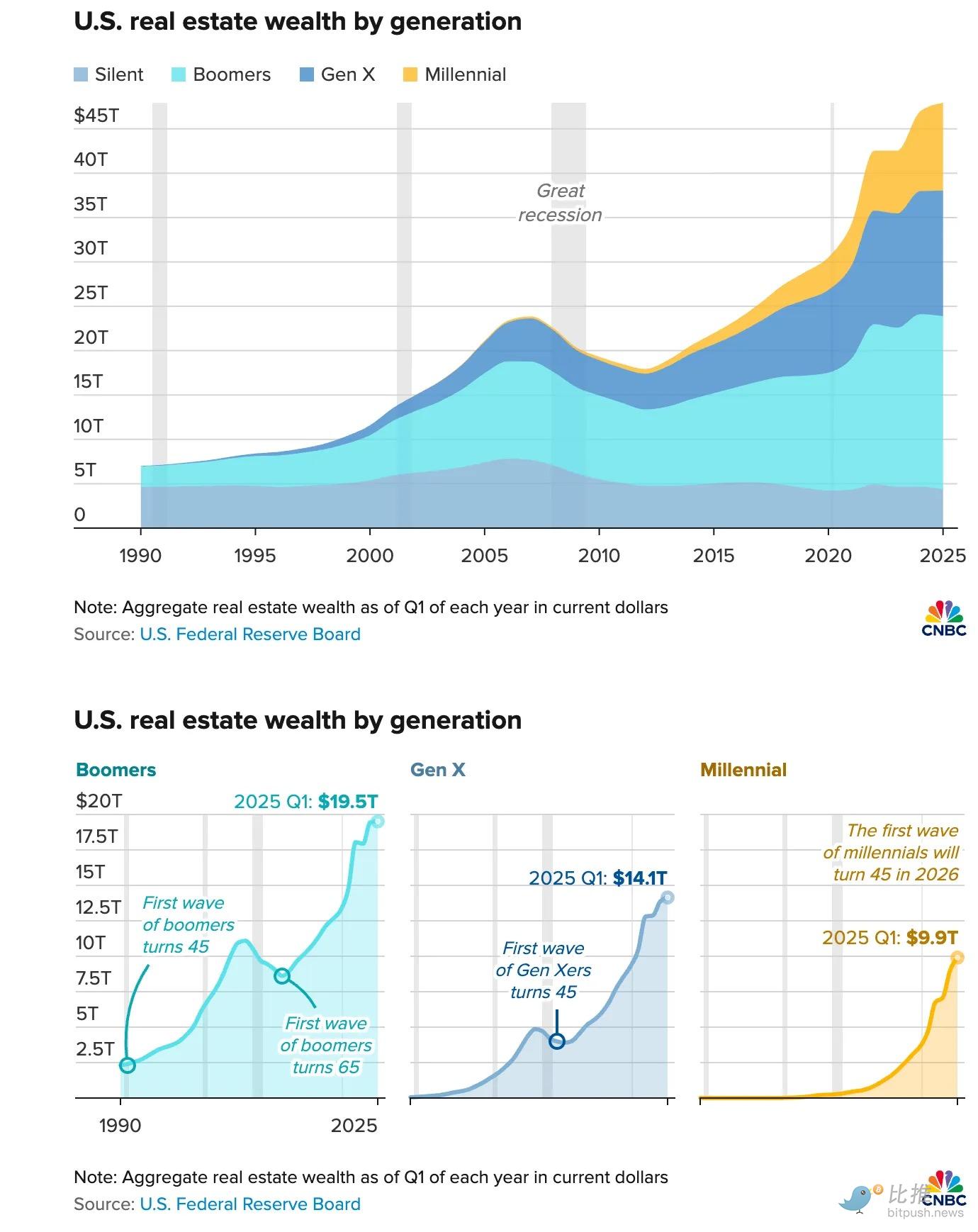

The Baby Boomers accumulated this wealth under conditions that no longer exist. They bought when the price-to-income ratio was between 2 and 3.5. They paid off their mortgages during decades of real wage growth. By Q1 2025, the real estate held by Boomers had reached $19.5 trillion, up from a fraction of that in 1990.

(Data from cnbc.com)

Millennials entering the market today face a price-to-income ratio more than double what their parents faced. They carry student loan debts their parents didn't have. They face mortgage rates that make the monthly payment on a median-priced home nearly unaffordable for a median-income family. The down payment alone—in a market where prices rise faster than savings accumulate—has become a trap.

The result is a generational rift that is no longer cyclical. The generation that could afford to buy, did. The generation that couldn't is poised to inherit.

Real estate is one of the most illiquid assets a person can hold.

When you need cash, you can't sell 10% of the house. When your job moves, you can't relocate it. You can't cleanly divide it among four siblings without triggering a legal process that can take 18 months and drain the estate's funds. Inheriting a million-dollar house in a city you can't afford to live in isn't good news; it's a dilemma: Sell it? Keep it and bear the maintenance costs? Rent it out and become a landlord? Or spend years negotiating with siblings over which option to choose?

Baby Boomers currently hold about 40% of U.S. housing wealth. 61% say they will never sell. When you see the incentive structure, this isn't stubbornness. Selling triggers capital gains taxes on decades of appreciation; it resets a 3% mortgage rate to 7%; in California, it could instantly multiply property taxes tenfold. And there are no affordable houses available for them to downsize into.

So they stay put. The houses stop circulating. Younger buyers are locked out, waiting for an inheritance that has become the only realistic path to homeownership in many cities. When the inheritance finally happens, the liquidity problem doesn't disappear; it just transfers to the next generation.

Nansen co-founder Alex Svanevik describes the coming situation as a "tsunami." He stated in January 2026 that about $100 trillion will be inherited over the next 20 years, and the force driving these funds into cryptocurrency is structural, not speculative. He estimates that if just 3% of these inherited assets flow into crypto, its market cap could double from its current size.

3% sounds small? Consider who is inheriting: According to a recent OKX survey, Gen Z trusts cryptocurrency five times more than Baby Boomers do. Millennials already hold more digital assets than their parents. We don't need to convince them crypto is real; they grew up using it the way previous generations used savings accounts. What they need is for inherited wealth to meet them in a form they understand.

This is the gap. And "Tokenisation" is the bridge.

Real World Asset (RWA) tokenization means representing ownership of a physical asset on a blockchain. Once tokenized, ownership can be fractionalized, transferred without intermediaries, held in a wallet, used as collateral, or traded without requiring consensus from all stakeholders. Friction costs that were once prohibitive become manageable.

Specifically for inheriting property, tokenization solves four currently intractable problems:

-

Liquidity: Tokenized property can be sold partially. An heir who urgently needs $50,000 but holds a $500,000 share of a house can sell 10% of their ownership instead of being forced to sell the entire house or get nothing. This also makes borrowing against it much simpler, as the underlying asset is liquid, allowing lenders to underwrite more easily.

-

Distribution: When four siblings inherit a property, tokenization allows each to digitally hold their exact share, enabling them to trade, sell, or keep it independently without requiring unanimous agreement on the disposition of the physical asset. When ownership is "programmable," the legal disputes that currently drain estates are significantly simplified.

-

Liquidity/Mobility: Tokenized property can sit in a portfolio alongside stocks, crypto, and other assets. It can be managed remotely, transferred across borders, and eventually used as collateral in DeFi (Decentralized Finance) protocols. The "geographic lock" of real estate ceases to be a constraint on the heir's financial flexibility.

-

Access: For heirs who can't afford a house but are destined to inherit one, tokenization allows for early participation. For younger members receiving smaller inheritance shares, fractional ownership allows them to hold a piece of a physical asset without being forced to liquidate immediately.

The market is already moving in this direction. By early 2026, the total value of tokenized real-world assets had reached $26 billion in on-chain assets and $388 billion in represented assets, with strong growth momentum. While real estate currently represents a small portion of this, the infrastructure being built—wallets, on-chain settlement, programmable ownership—is far more functional than it was just two years ago. Svanevik points out that the products Nansen is building today couldn't have existed two years ago because the underlying infrastructure wasn't ready. Now, it is.

This doesn't mean tokenization solves the housing affordability crisis. Prices won't drop just because ownership becomes more portable. The structural problems of the market—constrained supply, rate lock-in, the long-term decoupling of prices from wages—remain. And it's uncertain whether "financializing" the last non-liquid asset most families own improves their lives or just makes their troubles more tradable.

Tokenization solves a more specific, more urgent problem. It's about what happens when $25 trillion in housing wealth transfers from a generation accustomed to storing everything in real estate to a generation that believes wealth should be liquid, digital, and not tied to a specific physical address.

Currently, the tools for accessing home equity are broken for most holders. Cash-out refinancing means giving up a 3% rate for a 7% rate. Home Equity Lines of Credit (HELOCs) require income verification that retirees often can't provide. Reverse mortgages carry 30 years of stigma and create complex inheritance issues. Selling triggers both tax traps and rate resets. Every option comes at a cost the holder can ill afford.

The wealth transfer is already happening, at a rate of about $1.5 trillion per year and accelerating. The first Millennials will turn 45 in 2026. JPMorgan, BlackRock, and Franklin Templeton have all entered the tokenized asset space in the last two years, building infrastructure for this moment. Robinhood CEO Vlad Tenev wrote last year that this wealth transfer is happening alongside a technological shift that will make the coming years critical.

This generation inheriting wealth sees financial assets not as papers in a filing cabinet, but as digits living in a mobile wallet.

The real obstacle is that the current system for transferring title still relies on paper documents, on intermediary steps—a language they no longer think in.

Every generation accumulates wealth in the language it knows. The next generation must translate it before it can inherit it.

Twitter:https://twitter.com/BitpushNewsCN

Bitpush TG Discussion Group:https://t.me/BitPushCommunity

Bitpush TG Subscription: https://t.me/bitpush