Author: Azuma

Original Title: Eating Into the Hundred-Billion-Dollar Gambling Industry, Prediction Markets Are Being Chased Down by the Old Order

The booming prediction markets are now facing a real challenge.

On January 9, US local time, the Tennessee Sports Wagering Council (SWC) issued cease-and-desist orders to prediction market platforms such as Kalshi, Polymarket, and Crypto.com, demanding that these platforms stop offering sports event prediction contracts to residents of the state. The reason given was that these companies were engaged in illegal gambling operations without obtaining a license from the state government.

In the notice, the SWC accused these three companies of illegally offering sports betting products under the guise of "event contracts." Although these platforms are registered with the U.S. Commodity Futures Trading Commission (CFTC) as designated contract markets, according to Tennessee state law, any entity offering sports event betting services in the state must hold a license issued by the SWC.

The SWC demanded that Kalshi, Polymarket, and Crypto.com must cease all activities in the state by January 31, cancel open contracts, and refund resident deposits. Failure to comply by the deadline could result in civil penalties of up to $25,000 per violation and even criminal charges.

The Rapidly Growing Sports Betting Market

To understand why Tennessee is taking such a hard line against prediction market platforms, one must look at the current state of the U.S. sports betting market.

Since the U.S. Supreme Court overturned the federal law, the Professional and Amateur Sports Protection Act (PASPA), which had prohibited commercial sports betting, on May 14, 2018, individual states have gained the authority to decide whether to legalize sports betting within their jurisdictions. Currently, sports betting in the U.S. is regulated by state-level agencies responsible for licensing, compliance, and enforcement, with each state setting its own tax rates, market entry thresholds, and responsible gambling requirements.

According to a report by the sports betting media Legal Sports Report, as of now, 38 states (including Washington D.C. and Puerto Rico) have allowed the legal operation of sports betting services (both online and offline), with 30 states permitting online sports betting services — Tennessee is one of them and is the first state to allow only online sports betting while prohibiting physical betting venues.

Home to multiple popular leagues such as the NFL, MLB, NBA, and NHL, the United States is undoubtedly a sports powerhouse, and sports betting is a gambling service clearly defined and heavily taxed and regulated by state governments.

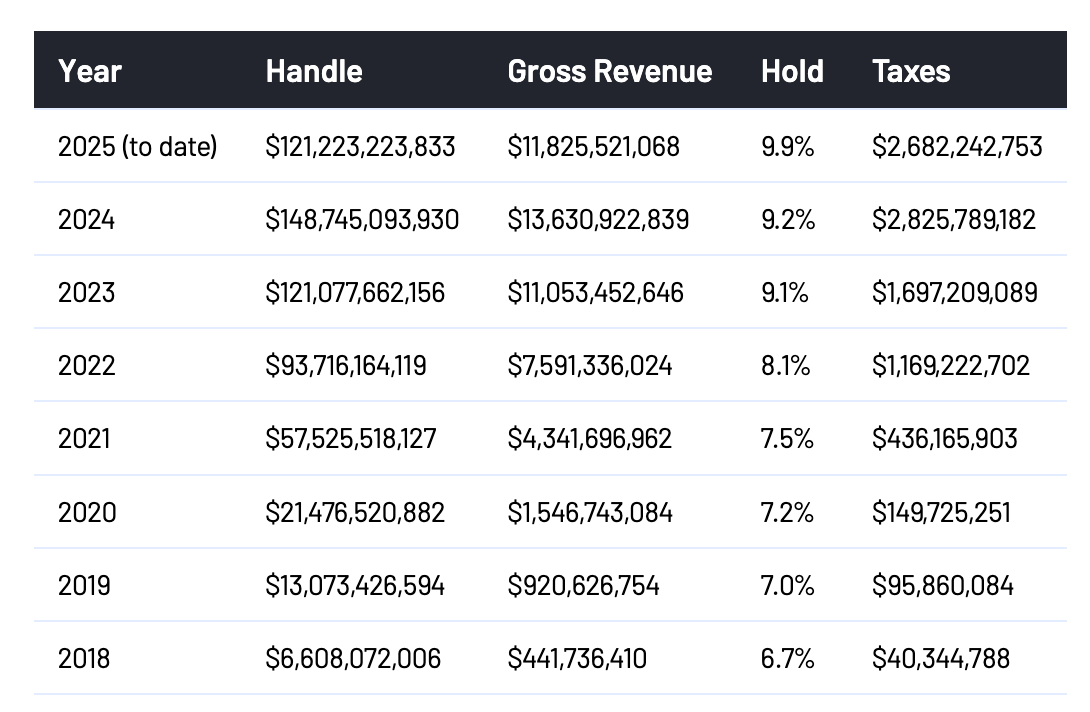

Statistics from another major sports betting media, Sports Book Review (chart below, data as of August 2025), show that since the regulatory relaxation in 2018, the total betting volume (Handle) and tax revenue (Taxes) of the U.S. sports betting market have shown a remarkably exaggerated growth trend over the past few years — the total market betting volume reached $148.74 billion in 2024, with tax contributions reaching $2.82 billion; in the first 8 months of 2025 alone, the total betting volume ($121.22 billion) and tax revenue ($2.68 billion) have nearly reached the full-year 2024 levels.

Focus on Tennessee: What Does Sports Betting Mean?

Now let's focus on Tennessee, the protagonist of this incident.

In 2019, Tennessee passed the Tennessee Sports Gaming Act, formally legalizing sports betting. Although the then-Governor Bill Lee had reservations about gambling, he still allowed the bill to pass without exercising his veto power. Between 2021 and 2022, the Tennessee state legislature passed laws establishing a dedicated regulatory council to be fully responsible for licensing and supervision. This council was initially called the Sports Wagering Advisory Council and was later renamed the Tennessee Sports Wagering Council, the SWC that issued the ban to Kalshi, Polymarket, and Crypto.com at the beginning of this article.

Currently, the SWC is Tennessee's sole sports betting regulatory body, responsible for operational licensing, compliance supervision, rule-making, and enforcement. The SWC stipulates that all sports betting providers must obtain a license from the SWC to offer services in the state. A total of 11 licenses have been issued so far (see chart above); only residents aged 21 and over can access related services, and they must pass geolocation verification to ensure bets are placed within the state. Regarding taxation, the state levies a 1.85% tax rate on the total betting handle — an income-based taxation scheme was used initially, but it was changed to taxation based on the total betting handle after 2023.

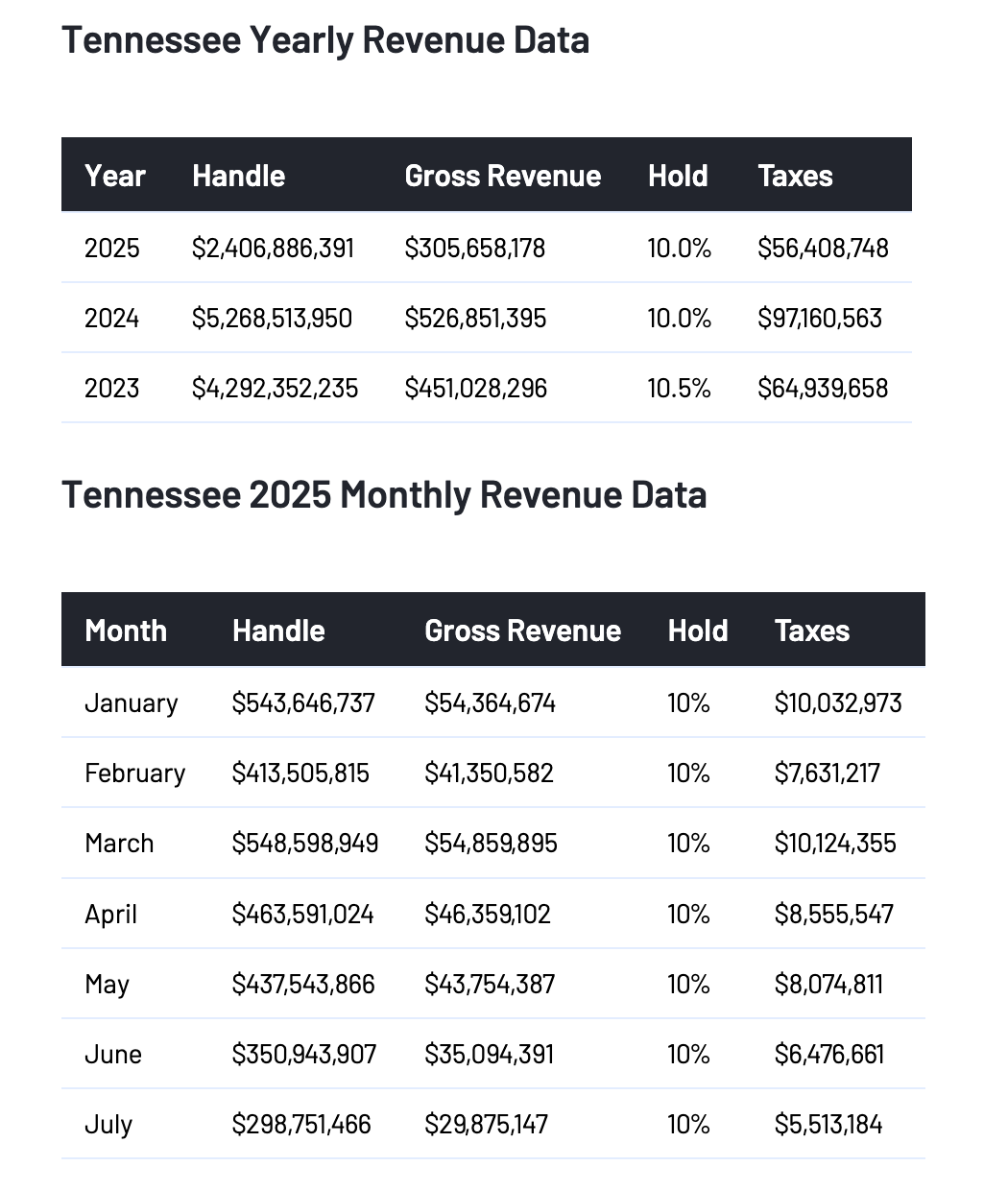

The sports betting market has contributed substantial tax revenue to Tennessee. Statistics from Sports Book Review (chart below, data as of July 2025) show that in 2024, the total sports betting handle in Tennessee reached $5.268 billion, with tax contributions reaching $97.16 million; the total betting handle for the first 7 months of 2025 has already reached $2.4 billion, with tax contributions reaching $56.4 million.

But this huge and still growing cake is now being gradually nibbled away by the likes of Polymarket.

How Are Prediction Markets Eating Into the Old World?

On December 3, 2025, Polymarket announced that it had obtained CFTC approval to return to the U.S. market after nearly four years; even earlier, Kalshi and Crypto.com's prediction market platform Truth Predict had already opened their doors to U.S. users under CFTC licensing.

The current regulatory situation is that sports betting is clearly classified as a gambling service, with regulatory authority belonging to the states. However, prediction market platforms like Polymarket are generally regarded as new entities providing "event contract" trading services, and "event contracts" are considered financial derivatives in terms of asset nature, falling under the regulatory purview of the CFTC. This allows prediction markets to bypass the stringent regulations of gambling services — no need for state-level licenses, no need to follow user protection regulations like addiction control, no need to pay high gambling taxes to the states; but at the same time, they can offer sports event outcome betting services similar to gambling,客观上 forming a certain "regulatory arbitrage."

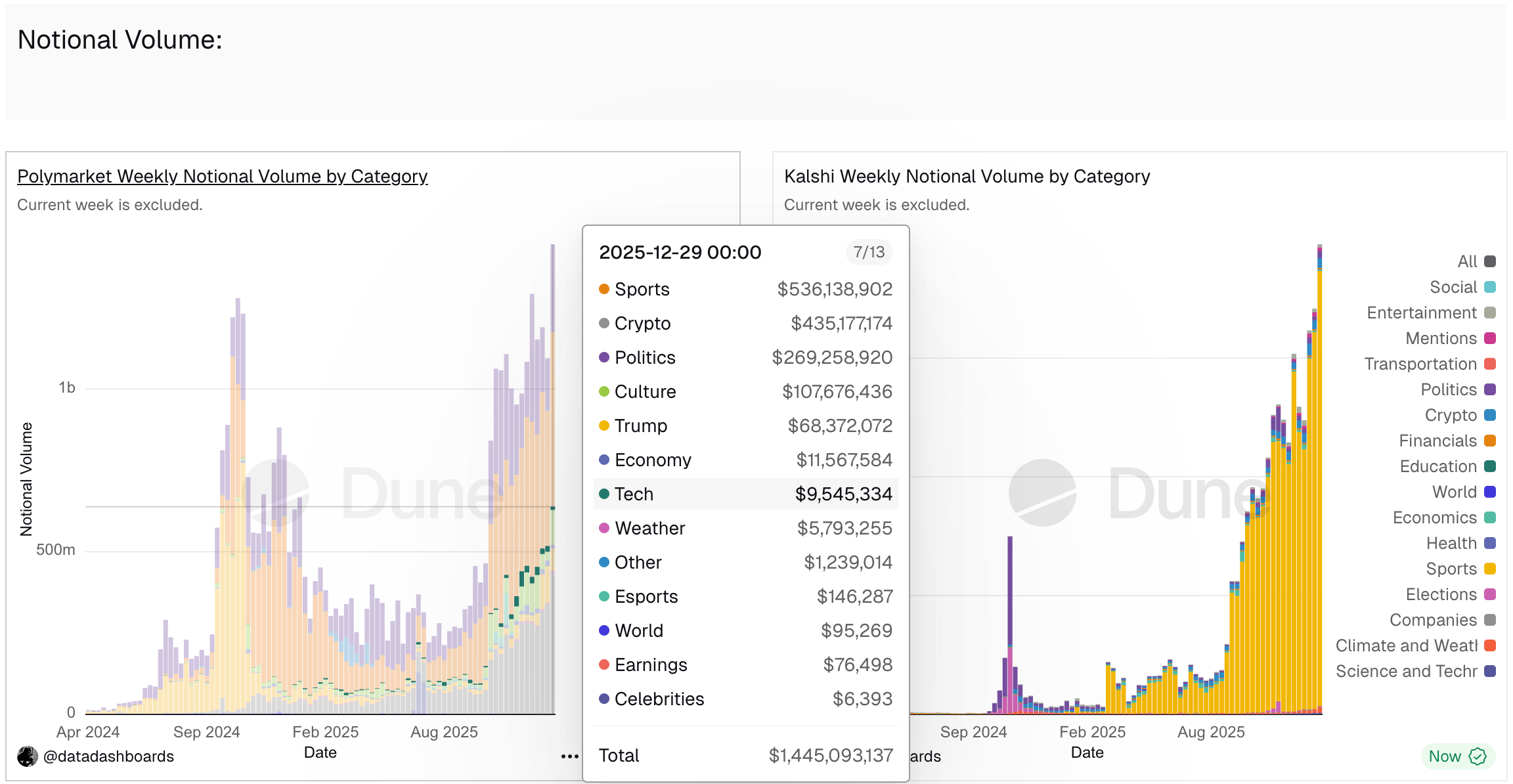

If prediction markets were still just small experimental fields, it might be one thing, but the fact is that the growth rate of prediction markets is even more outrageous than the already exaggerated sports betting market — in 2025, the total trading volume of prediction markets was approximately $40 billion, an increase of about 400% from $9 billion in 2024. A data dashboard compiled by Data Dashboards on Dune (chart below) shows that sports-related event contracts have long become the category with the highest trading volume share in the prediction market.

The capital market has long sensed the growing threat posed by Polymarket to traditional sports betting services. The two giants of the sports betting market, DraftKings and Flutter Entertainment, recorded declines of 11.7% and 16.1% respectively over the past year — during the same period, the US stock market was in a bull run, with the Dow Jones rising 12.97% for the year, the Nasdaq up 20.36%, and the S&P 500 up 16.39%; and the size of the sports betting market continued its eight-year upward trend.

Whether it's Tennessee, which needs sports betting as a source of tax revenue, or the capital forces that actually control the sports betting market, it is difficult to agree to let prediction markets, this new player, come and share the pie.

Friction Is Not an Isolated Case, How Do Prediction Markets Fight Back?

In fact, Tennessee's ban on prediction markets is not an isolated incident. Maryland, Ohio, Illinois, New Jersey, Nevada, Montana, Michigan, and Connecticut have all cracked down on prediction markets for similar reasons. And since Polymarket only returned to the U.S. market last December, Kalshi has borne the brunt of more regulatory impacts.

In response, Kalshi has filed lawsuits against three states — Nevada, New Jersey, and Maryland — on the grounds that it "already complies with higher-priority federal regulations and does not need to comply with state-level regulations." But the results have not been ideal.

-

The lawsuit in Nevada was the first to proceed. The district court initially supported Kalshi, but then turned around and ruled against Kalshi last November. Judge Andrew Gordon determined that sports event contracts on Kalshi were very similar to sports betting wagers and therefore fell under the regulatory scope of Nevada's gambling laws. Kalshi has appealed to the U.S. Court of Appeals for the Ninth Circuit;

-

In New Jersey, the district court chose to support Kalshi, but the state's gambling regulatory agency has appealed to the U.S. Court of Appeals for the Third Circuit;

-

In Maryland, the district court sided with the gambling regulatory agency's demands. Judge Adam B. reasoned that Kalshi failed to prove that "Congress has clearly and manifestly intended to deprive states of their power to regulate gambling." Kalshi has appealed this to the U.S. Court of Appeals for the Fourth Circuit.

The law firm Benesch commented on this, stating that as the national debate continues, similar divisions are expected at the appellate court level, which will lay the groundwork for the Supreme Court to resolve this issue in the coming years...... If the appellate courts happen to consistently support Kalshi's position, other prediction markets might emulate its model and proceed with similar businesses before the Supreme Court hears the matter; but if the appellate courts reach different conclusions, companies in similar situations might wait for clearer legal signals before taking action. In any case, Kalshi's lawsuit will create a precedent with direct and profound implications for the national sports betting and gambling industry.

In summary, whether prediction markets need to follow state gambling regulations remains an unresolved question for now, and the fundamental contradiction of this issue lies in the similarity of products and services between prediction markets and sports betting and the differences in regulatory requirements.

This is a tug-of-war over institutional adaptation. Before the appellate courts or even the Supreme Court give a final verdict, the gray area between prediction markets and sports betting will persist for a long time, and regulatory conflicts will be hard to avoid. In the short term, states will likely continue to defend their regulatory authority and tax base through enforcement and litigation; while prediction market platforms will try to use federal compliance and innovation narratives as a shield to fight for more living space.

Twitter:https://twitter.com/BitpushNewsCN

Bitpush TG Discussion Group:https://t.me/BitPushCommunity

Bitpush TG Subscription: https://t.me/bitpush