Автор оригинала: Махэ, Foresight News

28 мая, после многократной борьбы за уровень в 75 000 долларов, цена биткоина в конечном итоге не удержалась и опустилась до отметки около 74 000 долларов. ETH колеблется в районе 2000 долларов. Ранее сильно выросшие NEAR, WLD и ONDO также подверглись коррекции.

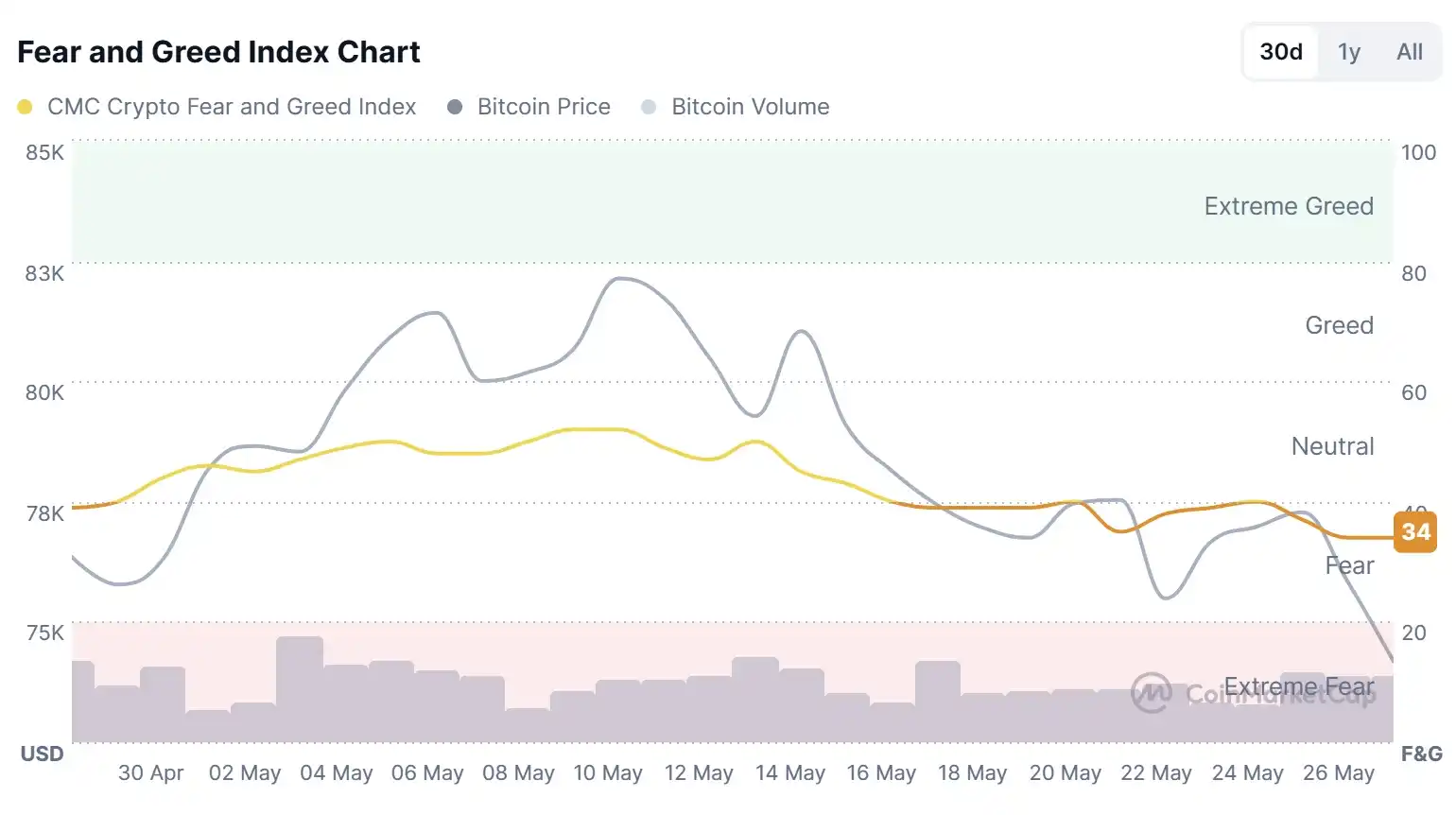

Индекс страха на рынке в настоящее время упал до 34, что свидетельствует о панических настроениях.

Данные Coinglass показывают, что за последние 24 часа на всех платформах было ликвидировано неисполненных контрактов на сумму 470 миллионов долларов, из них лонгов — на 420 миллионов долларов.

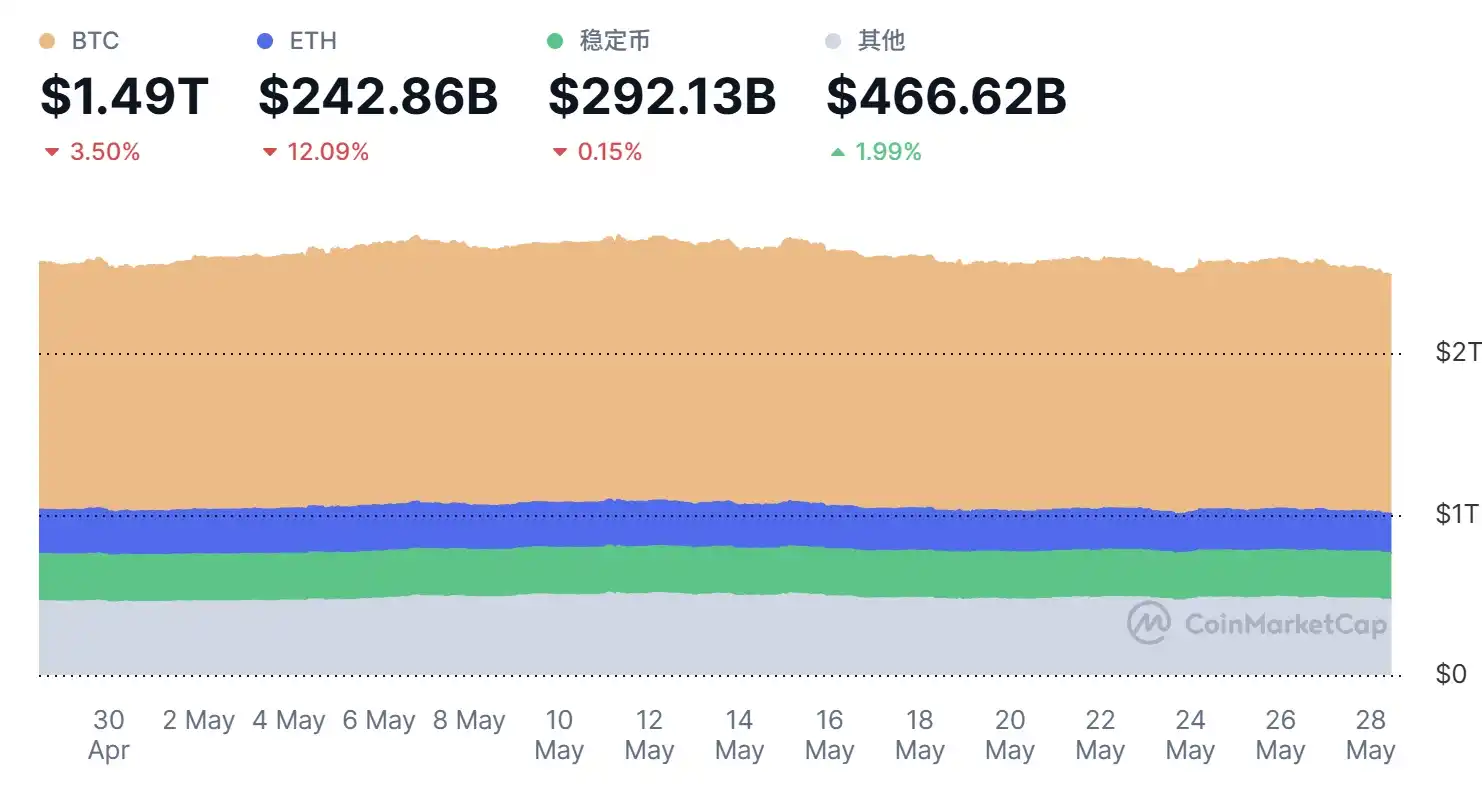

В течение последних нескольких недель биткоин колебался в диапазоне 75 000 - 80 000 долларов, кратковременно пытался пробить уровень 78 000 долларов, но не смог закрепиться. За последние 30 дней на крипторынке BTC упал на 3,5%, ETH — примерно на 12%, стейблкоины также снизились на 0,15%.

С точки зрения макроэкономических данных: нефть марки Brent незначительно выросла до 97 долларов за баррель, серебро слегка упало до 73 долларов. Индекс Dow Jones вырос на 182,60 пункта (+0,36%), достигнув нового рекордного максимума. Индекс S&P 500 вырос на 1,24 пункта (+0,02%). Композитный индекс Nasdaq: 26 674,73 пункта, рост на 18,55 пунктов (+0,07%). Спотовое золото не удержалось на уровне 4400 долларов за унцию, впервые с 27 марта, потеряв за день более 50 долларов, падение составило 1,25%.

«Возобновление» военного противостояния между США и Ираном

Геополитические риски на Ближнем Востоке стали еще одной важной внешней переменной. С 2026 года напряженность вокруг иранских ядерных объектов, безопасности судоходства в Ормузском проливе и других вопросов между США, Ираном и связанными сторонами неоднократно обострялась и сменялась разрядкой. За последние месяцы США применяли стратегию, сочетающую военные действия с дипломатическим давлением, сопровождавшуюся слухами об авиаударах, блокаде портов и периодическими переговорами о прекращении огня.

Даже в периоды прекращения огня или дипломатического прогресса рыночная оценка риска «возобновления» конфликта полностью не исчезла.

28 мая в предрассветные часы президент США Трамп заявил, что США продолжат контролировать активы Ирана. Иран начал предоставлять нам то, что мы хотим. Если дела пойдут не так, министр обороны США Хеггесит завершит эту работу. Мы можем быстро закончить войну с Ираном, возможно, это даже необходимо. Однако я не думаю, что нам нужно это делать.

Около 5 часов по пекинскому времени, согласно сообщениям иранского информационного агентства Fars News, местные жители заявили, что в порту Абас на юге Ирана раздались звуки взрывов.

Американский официальный представитель сообщил Reuters, что военные США нанесли новый удар по иранской военной базе, представлявшей угрозу для американских войск и коммерческого судоходства в Ормузском проливе. Американские военные также перехватили и сбили несколько иранских беспилотников, представлявших угрозу для американских войск и коммерческого морского транспорта.

Новое обострение напряженности вокруг Ормузского пролива вновь оказалось в центре внимания, волатильность цен на нефть усилилась, глобальные рисковые активы оказались под давлением. В этих условиях биткоин в большей степени демонстрирует свойства рискового актива, а не традиционную функцию «цифрового золота» в качестве убежища — геополитическая неопределенность повышает спрос на доллар США и казначейские облигации США, одновременно подавляя аппетит к риску, что приводит к оттоку средств с крипторынка.

Чистый отток из ETF свидетельствует о фиксации прибыли институциональными инвесторами

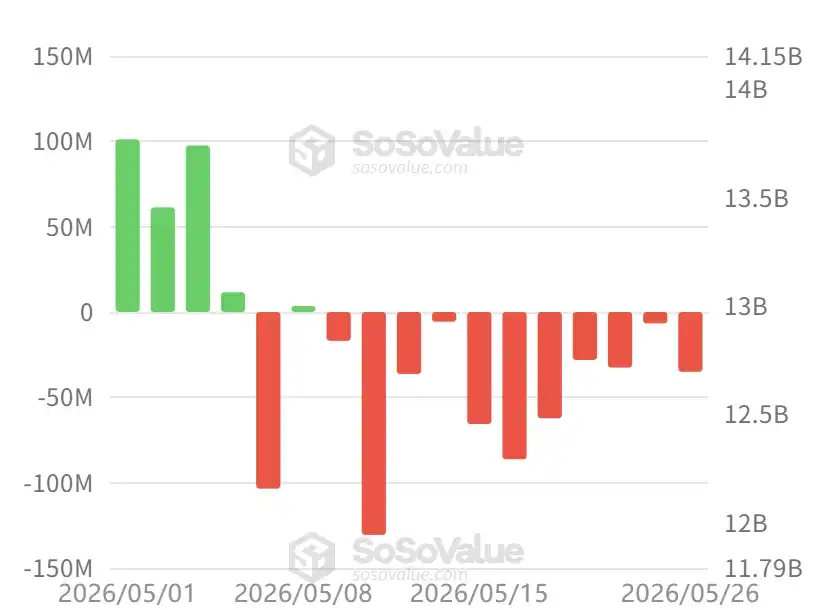

С момента запуска в начале 2024 года американские спотовые ETF на биткоин привлекли совокупный чистый приток более 570 миллиардов долларов, став одним из основных каналов институционального размещения биткоина. Однако с начала мая 2026 года тенденция явно изменилась на противоположную.

Согласно данным отслеживания SoSoValue, в период с 5 по 26 мая американские биткоин-ETF зафиксировали последовательный чистый отток средств, при этом размер ежедневного оттока увеличился с нескольких десятков миллионов долларов до максимума в 6 миллиардов долларов, причем такое случалось дважды.

Ситуация со спотовыми ETF на эфириум также не выглядит оптимистично: аналогично биткоину, с начала мая наблюдается значительный чистый отток.

Возможно, это не просто «паническая распродажа», а скорее системная фиксация прибыли ранее купившими инвесторами. Держатели ETF включают традиционные управляющие активами, семейные офисы и хедж-фонды, которые после восстановления биткоина с низов до диапазона 75 000 - 80 000 долларов выбирают механизм погашения для фиксации прибыли. Часть средств может перетекать в акции технологических компаний, связанных с ИИ, которые показывают более сильную динамику — индексы S&P 500 и Nasdaq в тот же период достигли новых максимумов, в то время как крипторынок в целом отставал, что подчеркивает перераспределение капитала внутри рисковых активов.

Последующая динамика

Wintermute в своем сообщении заявила, что отток средств из ETF на BTC в течение двух недель подряд превысил 1 миллиард долларов (после шести недель притока), что говорит о том, что институциональные инвесторы используют силу рынка для фиксации части недавних положительных доходов. Более пристального внимания заслуживает ИИ. Nvidia продемонстрировала образцовые результаты, превзошедшие ожидания, но после закрытия торгов практически не было движения. Дополнительное превышение ожиданий больше не может сдвинуть стрелку. Если импульс ИИ иссякнет, макроэкономическая картина (рекордно низкая уверенность потребителей, устойчивая инфляция, Вольш, возглавивший ястребиный ФРС) получит больший вес, и криптовалюты не останутся в стороне.

Долгосрочная структура BTC остается неповрежденной (резервы на многолетних минимумах, долгосрочные держатели продолжают накапливать, CLARITY продвигается, HYPE делает то, что должны делать на ранних этапах крупные токены). Но краткосрочные потоки капитала движут ценой, и в настоящее время они негативные. Уровень 75 000 - 76 000 долларов является ключевой линией для BTC: удержание здесь позволит BTC вновь атаковать 80 000 долларов; пробитие этого диапазона может быстро привести к скольжению к 70 000 - 72 000 долларам.

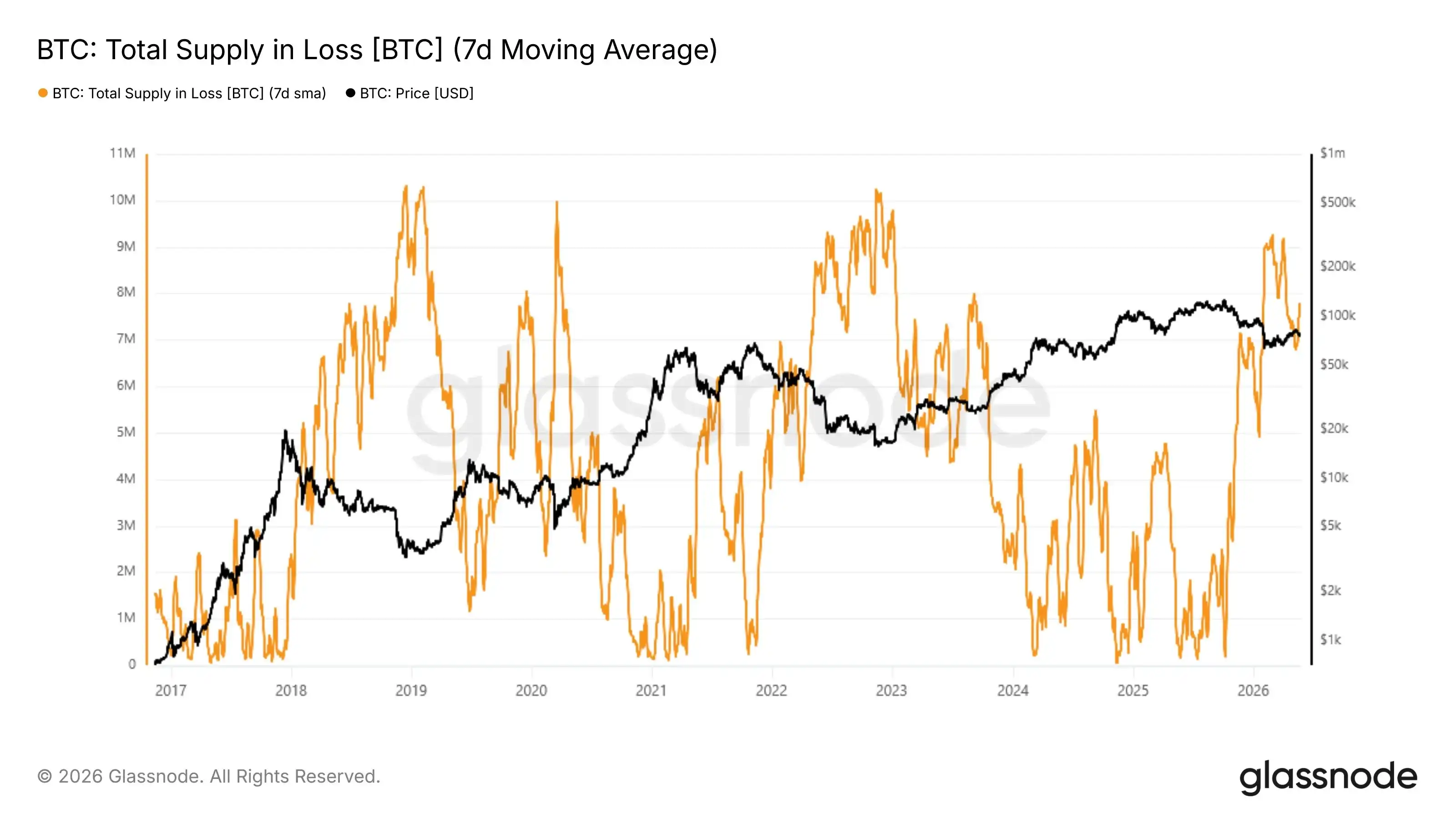

glassnode в твите заявила, что при цене 76 000 долларов примерно 7,75 миллиона BTC находятся в убытке. Такой избыток предложения является структурной особенностью медвежьего рынка и обычно разрешается только после капитуляции слабых рук.

BIT в твите заявила, что, что касается биткоина, непрерывный рост цен в последний период во многом зависел от соотношения институционального спроса и доступного рыночного предложения. За последний год биткоин-ETF и Strategy стали важным источником такого спроса. Когда приток средств в ETF ускорялся, а Strategy продолжала наращивать позиции в биткоине, цена биткоина обычно продолжала расти.

BIT заявила, что в настоящее время совокупный чистый объем покупок ETF и Strategy снизился до всего 870 миллионов долларов, главным образом из-за значительного оттока средств из ETF и перехода от чистых покупок к чистым продажам. До тех пор, пока приток средств в ETF не стабилизируется и не возобновится рост, в краткосрочной перспективе биткоин, вероятно, останется в состоянии консолидации.

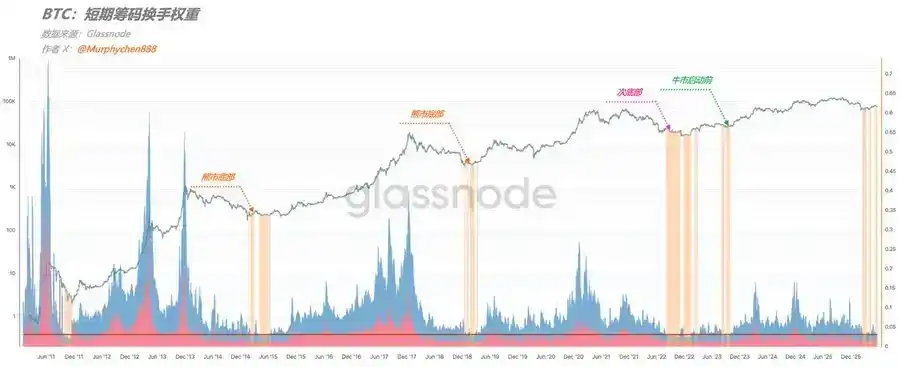

Аналитик Murphy заявил, что с помощью индикатора на основе блокчейна «вес краткосрочного капитала в активности на блокчейне» (т.е. доля долларовой стоимости, приходящейся на оборот краткосрочных монет) можно наблюдать текущее состояние рынка BTC. Этот индикатор отражает последние краткосрочные торговые действия, такие как спекуляции, арбитраж, фиксация прибыли или панические распродажи. В настоящее время этот вес снизился до экстремально низкого исторического уровня, наблюдаемого только в зонах самого дна медвежьего рынка за последние 15 лет, что означает значительное охлаждение краткосрочного оборота, экономическая стоимость переходит к долгосрочным монетам, и рынок находится на этапе с низкой волатильностью, накопления или с явными признаками дна.

Murphy считает, что на этом основании текущий рынок может находиться на одной из трех стадий: дно медвежьего рынка; вторичное дно, возможно, с последним падением; накопление перед запуском бычьего рынка. Однако рациональный анализ позволяет временно исключить стадию накопления перед бычьим рынком. В настоящее время не рекомендуется полностью вкладываться в один сценарий, рекомендуется использовать стратегию диверсификации позиций для различных исходов, относительное положение долгосрочного основного тренда уже указывает на то, что биткоин находится вблизи дна.