Автор: Хлоя, ChainCatcher

Вчера Opinion официально представила токеномику и дорожную карту нативного токена OPN, а Binance официально объявила о включении Opinion в качестве 72-го проекта Launchpool. Согласно официальной дорожной карте, TGE Opinion состоится в первом квартале этого года, а во втором квартале основное внимание будет уделено развитию экосистемы и децентрализованному управлению.

Однако вместе с радостной новостью о листинге пришли не всеобщие аплодисменты, но и множество данных, вызывающих сомнения у рынка, низкий процент эирдропа, который назвали «обдираловкой», а также критика в адрес «быстрого пути» проекта на Binance.

Почему сейчас? Факторы, стоящие за переходом от роста пользователей к выпуску токена

На глобальном рынке прогнозов Polymarket, несомненно, является признанным лидером, но, несмотря на высокий трафик во время глобальных выборов и спортивных событий, новостей о выпуске токена не было. В этом году спрос на рынке прогнозов достиг пика, и Opinion,抢先 выйдя на Binance, четко намерена воспользоваться всплеском внимания и ликвидности после бума рынка прогнозов, вызванного Polymarket, и, используя ожидания пользователей относительно эирдропа, создать огромное конкурентное преимущество.

Кроме того, для широких масс розничных инвесторов OPN, получивший поддержку Binance, стал предпочтительным выбором для спекуляций на этом нарративе. OPN, как первый токен рынка прогнозов, вышедший на CEX, своей稀缺ностью подогрел сегодняшний интерес в криптоиндустрии.

Согласно данным RootData, 4 февраля Opinion объявила о завершении раунда А финансирования на 20 миллионов долларов при участии Hack VC, Jump Crypto, Primitive Ventures, Decasonic и других. Однако @cryptobraveHQ указал, что, по информации осведомленных лиц, подавляющее большинство этих инвесторов имеют условия обратного выкупа/гарантии возврата инвестиций, что по сути аналогично финансированию с гарантией возврата BeraChain, и по сути является «раундом оценки» или «раундом листинга».

Более того, по общению с коллегами из VC и сотрудниками, ответственными за листинг на биржах,普遍反馈 заключается в том, что это типичный раунд «раздувания», «оценки», «оплаты листинга». Для VC, вместо того чтобы играть в неизвестное будущее, лучше воспользоваться моментом наибольшего ажиотажа вокруг нарратива AI+рынок прогнозов, чтобы завершить весь процесс листинга и обеспечить выход капитала.

Огромные объемы данных вызывают сомнения: огромная разница между количеством сделок и объемом торгов

Возможно, желая стать «первым проектом рынка прогнозов, вышедшим на биржу», впечатляющие данные Opinion сразу же вызвали сомнения рынка.

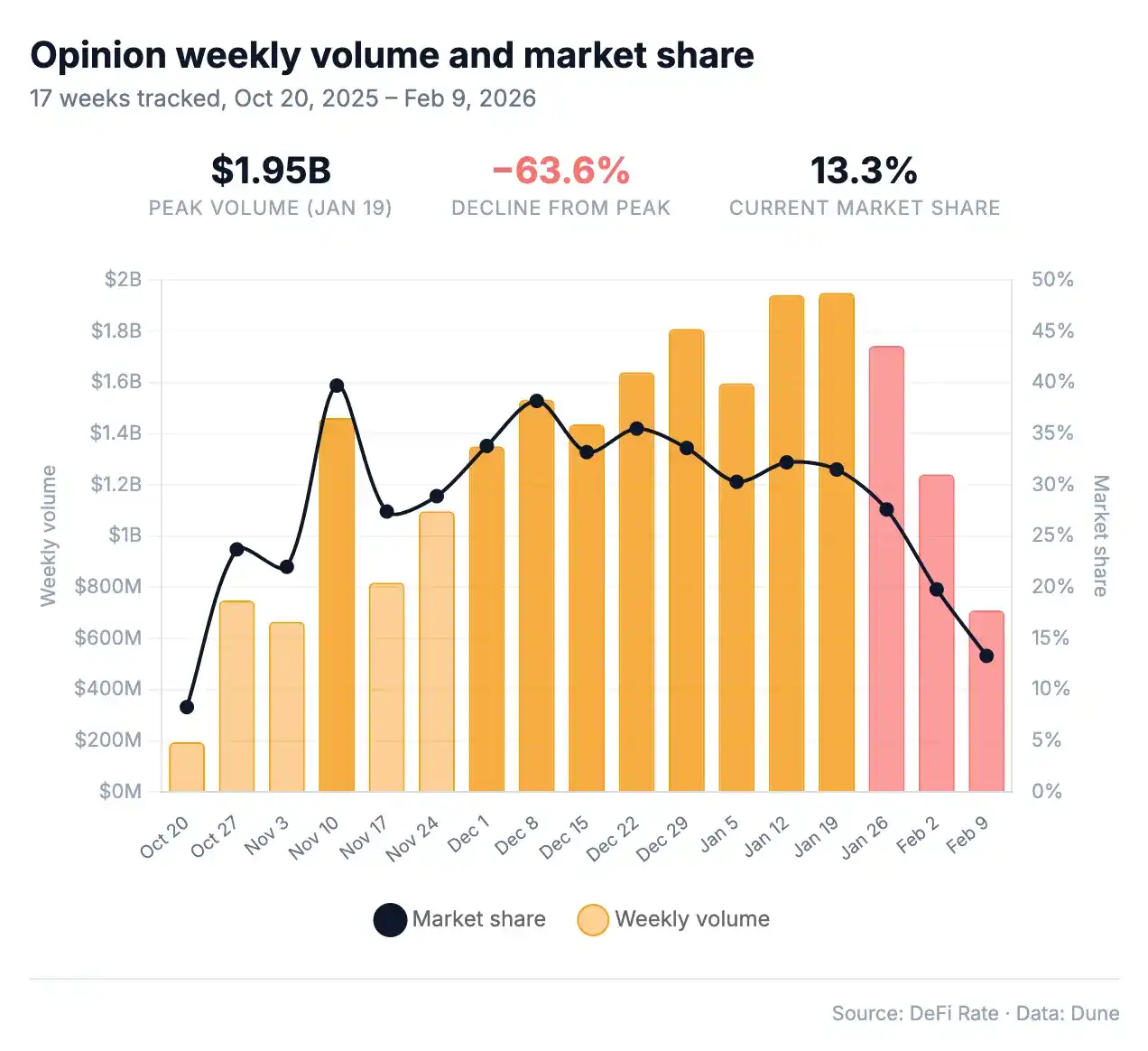

Согласно публичным данным Opinion, в январе 2026 года месячный объем торгов составил 8,08 миллиарда долларов, что составляет 31% от всего рынка прогнозов. Платформа, запущенная только в октябре 2025 года, всего за несколько месяцев объем торгов превысил показатели Kalshi и Polymarket, которые работают на рынке多年, и была названа «самой быстрорастущей платформой в истории рынков прогнозов». DeFiRate, изучив данные链上数据 Dune Analytics за 17 недель подряд (с октября прошлого года по февраль этого года), обнаружил множество аномалий, которые нельзя объяснить нормальной логикой роста платформы.

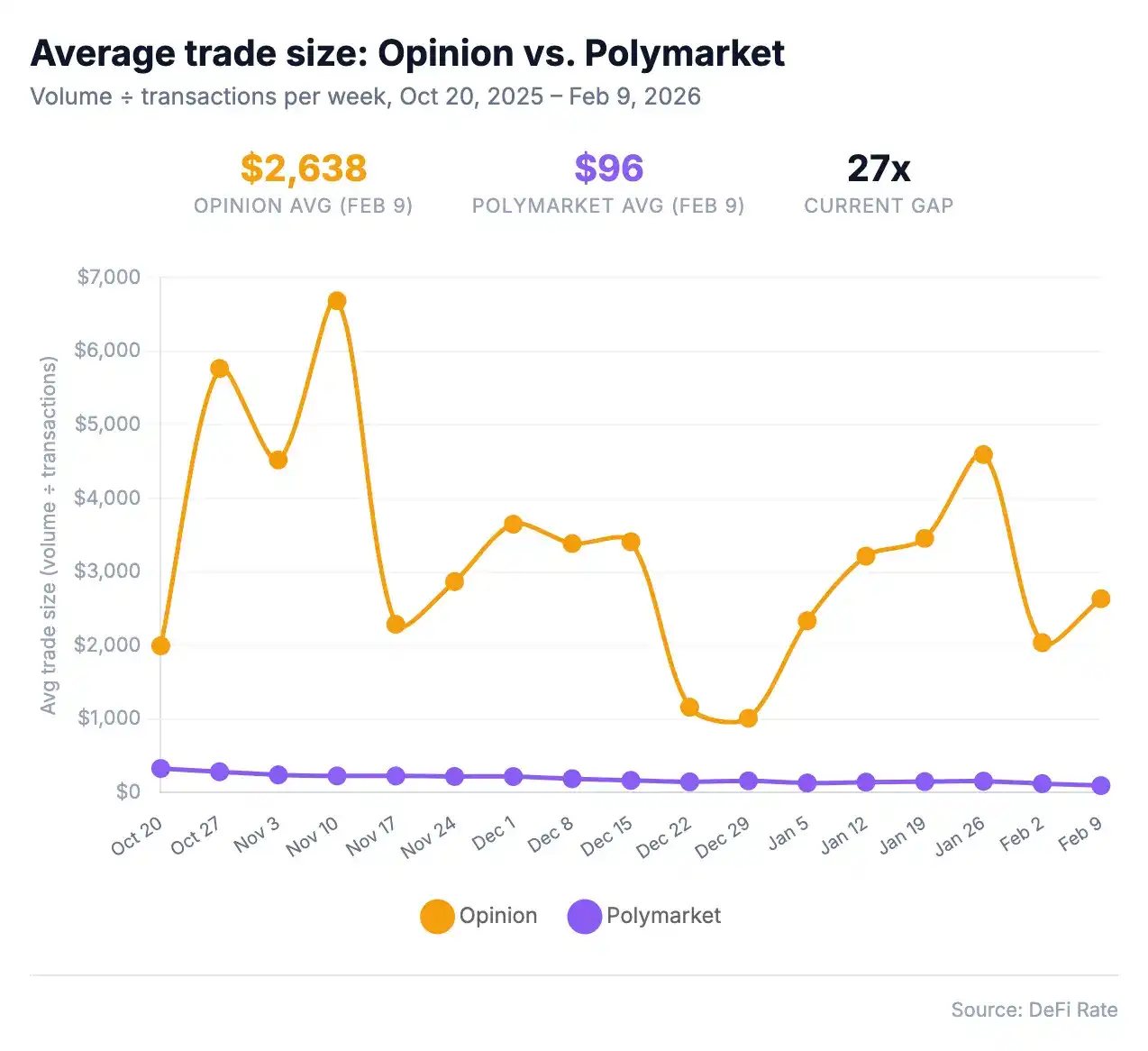

1. Огромная разница между количеством сделок и объемом торгов:

Ключевая проблема заключается не в размере объема торгов, а в соотношении между объемом торгов и количеством сделок. В январе 2026 года объем торгов Opinion в 8,08 миллиарда долларов был получен от 3,2 миллиона сделок, в среднем около 2525 долларов за сделку. За тот же период Kalshi произвела 5,45 миллиарда долларов при 54,5 миллиона сделок, в среднем 175 долларов за сделку; Polymarket произвела 7,66 миллиарда долларов при 52 миллионах сделок, в среднем 147 долларов за сделку. Проще говоря, Opinion, используя менее 3% от общего количества сделок в отрасли, произвела 31% отраслевого объема торгов.

Это соотношение никогда не было нормальным в течение более десятка недель подряд. Самая экстремальная неделя была 10 ноября: Opinion произвела 1,46 миллиарда долларов объема торгов при 218 582 сделках, в среднем колоссальные 6688 долларов за сделку; на той же неделе Polymarket произвела 952 миллиона долларов при 4,19 миллиона сделок, в среднем 228 долларов за сделку. Количество сделок Opinion было в девятнадцать раз меньше, чем у Polymarket, но объем торгов был на 53% больше.

К 9 февраля Opinion произвела 13,2% от общего объема торгов в отрасли, но внесла только около 0,7% от общего числа сделок. Это соотношение 19:1, и ни одна прогнозная платформа даже не приблизилась к этой цифре.

2. Аномальный объем торгов на пользователя: новые пользователи反而 повышают средний объем торгов платформы?

Нормальная логика роста платформы такова: база пользователей расширяется, новые мелкие инвесторы снижают средний объем торгов на пользователя. Траектория Opinion прямо противоположна. По данным DeFiRate, при запуске в октябре 20 534 пользователя произвели в среднем 38 537 долларов на человека в месяц; к январю число пользователей выросло до 101 954 человека, а средний объем торгов на человека反而 удвоился до 79 241 доллара, при этом размер платформы вырос в 5 раз.

Обычно новые пользователи снижают средний объем торгов на платформе. Но на платформе Opinion объем торгов каждой новой партии пользователей反而 увеличивается? Это резко контрастирует с естественным ростом таких платформ, как Polymarket, где средний объем торгов на пользователя растет стабильно, но медленно (в августе 4852 доллара/пользователь, в январе 11817 долларов/пользователь, количество пользователей выросло в 2,9 раза, объем торгов вырос в 2,4 раза).

3. Резкие колебания числа пользователей: только в праздники看起来正常но?

Сама пользовательская база Opinion также является еще одним красным флагом. За 17 недель еженедельные активные пользователи выросли с 11 124 человек до 67 913, а затем упали до 18 098, с колебаниями до 6 раз. Самый большой скачок произошел между 2 и 9 февраля: за одну неделю число пользователей упало с 67 804 до 18 098, сократившись на 73% за неделю. За тот же период пользовательская база Polymarket колебалась в пределах всего в 1,5 раза за 17 недель и демонстрировала стабильную восходящую тенденцию.

Особенно примечателен период аномального возврата к нормальным значениям: праздничный интервал с 22 декабря по 4 января. В эти две недели количество сделок Opinion внезапно выросло с обычных 300–600 тысяч до 1,4–1,8 миллиона сделок, при этом средний размер сделки одновременно упал до 1000–1163 долларов. Это был единственный момент, когда данные Opinion выглядели как данные нормального рынка прогнозов. Однако, как только праздники закончились, данные immediately вернулись к прежнему аномальному состоянию.

Эти аномалии не беспричинны. Система баллов Opinion четко определяет размер сделки как один из весовых коэффициентов для начисления баллов, что напрямую поощряет пользователей делать более крупные ставки. В сочетании с ожиданиями эирдропа перед TGE и средой без KYC это создает мощный стимул для накрутки объемов.

Стоит отметить, что исследователи из Колумбийского университета в ноябре 2025 года подсчитали, что около 25% от общего объема торгов Polymarket за три года приходилось на сделки с накруткой (wash trading), а на спортивных рынках этот показатель достигал 45%, при этом у Polymarket даже не было системы баллов и явного вознаграждения based on размеру сделки. Opinion, имея эти базовые условия плюс механизм начисления баллов, поощряющий крупные сделки, имеет очевидный стимул для накрутки объемов.

Крайне низкий процент эирдропа, пользователи жалуются на «обдираловку»

Кроме того, вчерашнее распределение эирдропа вызвало сильный backlash в сообществе. Хотя официально заявлено, что общий эирдроп составляет 23,5%, а начальный объем обращения при TGE, как ожидается, достигнет 19,85%, при запуске будет разблокировано только 3,5% (около 8,2 миллиона монет), остальное будет высвобождаться линейно в течение 7 месяцев. Остальное — это либо «крысиные норы», либо подношение Binance.

По сравнению с высокими комиссиями Opinion и сложной системой баллов, многие пользователи, прошедшие месяцы реальных сделок и высоких затрат, получили крайне скудное распределение, что заставило многих активных участников заявить, что их просто «официально ободрали».

Влияние этой пропорции выходит далеко за рамки backlash настроений сообщества. Это также повлияло на проекты рынка прогнозов в экосистеме Binance. Пользователи, которые все еще присматриваются к PredictFun, Probable, не могут не задаться вопросом: действительно ли есть ожидания отдачи от рынка прогнозов экосистемы Binance?

Opinion, выйдя抢先, должна была обеспечить поддержку последователям в этом сегменте, но 3% эирдропа и данные сомнения, скорее всего, отпугнут потенциальных пользователей PredictFun и Probable.

Наконец, нельзя否认, что Opinion действительно инновационна на техническом уровне. Традиционному рынку прогнозов для открытия рынка требуется ручная модерация, ручная установка условий расчета. Opinion с помощью AI oracle делает этот процесс почти мгновенным. Это означает, что она может охватывать гораздо больше сценариев, чем конкуренты, не только выборы и спортивные события. Изменения TVL DeFi-протокола, время листинга токена — все это может превратиться в ликвидный рынок прогнозов в течение нескольких минут.

Кроме того, независимый исследователь Хаотянь также отметил, что даже если объем торгов Opinion, несомненно, содержит значительную долю накрутки для получения баллов OPN, «но если отбросить накрутку, если в профиле пользователей платформы институциональные инвесторы и арбитражеры занимают значительную долю, это фактически косвенно подтверждает пропускную способность ее базовой инфраструктуры».

«Возможность для крупного капитала проводить точное хеджирование на рынке прогнозов, как на рынке деривативов, а не просто азартные игры на уровне розничных инвесторов, — вот на что должна быть направлена будущая цель рынков прогнозов 2.0».

Можно сказать, что после TGE Opinion ждет суровое испытание на удержание: после отмены стимулов в виде баллов, сколько человек готовы остаться и действительно использовать эту платформу? Сможет ли макро-рынок прогнозов привлечь достаточное количество институциональных пользователей, чтобы поддержать органический объем торгов?