Автор: Thejaswini M A

Компиляция: Deep Tide TechFlow

Введение от Deep Tide: Fidelity, Euronext, Tradeweb и еще 6 ведущих институтов Уолл-стрит начали публиковать рыночные данные напрямую в блокчейне через Pyth, и любой разработчик может использовать их бесплатно. Это разрушает 44-летнюю монопольную модель таких посредников, как Bloomberg — больше не нужно заключать двухлетние контракты, платить 27 000 долларов в год или использовать специальные клавиатуры. Что еще важнее, это предпосылка для реального масштабирования RWA (реальных мировых активов) в DeFi: данные должны быть в блокчейне раньше активов.

В 1981 году Майкла Блумберга уволили из Salomon Brothers. Ему было 39 лет, он проработал там 15 лет и ушел с выходным пособием в 10 миллионов долларов, чувствуя глубокое недовольство тем, как Уолл-стрит обрабатывает информацию. Его реакция на увольнение, по любым разумным меркам, была безумной: он начал каждое утро появляться в офисе Merrill Lynch с кофе, бродить по коридорам, вручать кофе незнакомцам и объяснять, что собирается построить для них компьютер, который все знает. Трейдеры принимали кофе, но были не так уверены насчет компьютера.

Спустя 44 года каждый такой компьютер стоит 27 000 долларов в год. В мире их 350 000, и Bloomberg зарабатывает на этом бизнесе около 10 миллиардов долларов в год. Его гениальность заключается в следующем: он вставил себя между организациями, владеющими данными, и людьми, которым данные нужны, взимая плату за все, что проходит через него. Данные никогда не принадлежали Bloomberg — данные есть у Merrill Lynch, у Goldman Sachs, у каждой торговой компании на Уолл-стрит. Bloomberg просто построил пункт взимания платы, убедил всех, что этот пункт и есть пункт назначения, а затем ежегодно поднимал цены, потому что что еще остается делать — звонить брокеру?

Эта модель выдержала все технологические изменения за сорок лет, потому что никто не мог придумать лучший механизм распространения. До прошлой среды.

9 апреля шесть учреждений, которые наполняли этот пункт сбора данными, начали публиковать их в другом месте: Euronext, Fidelity, Tradeweb, OTC Markets Group, валютное подразделение Сингапурской биржи и Exchange Data International начали публиковать данные напрямую в блокчейне через новый рынок данных Pyth, доступный для любого разработчика в 100 блокчейнах. Вам не нужен контракт, двухлетние минимальные обязательства, специальная клавиатура с желто-зелеными кнопками.

Запомните это: забавная вещь в построении монополии на чужих данных заключается в том, что эти «другие» в конце концов замечают это.

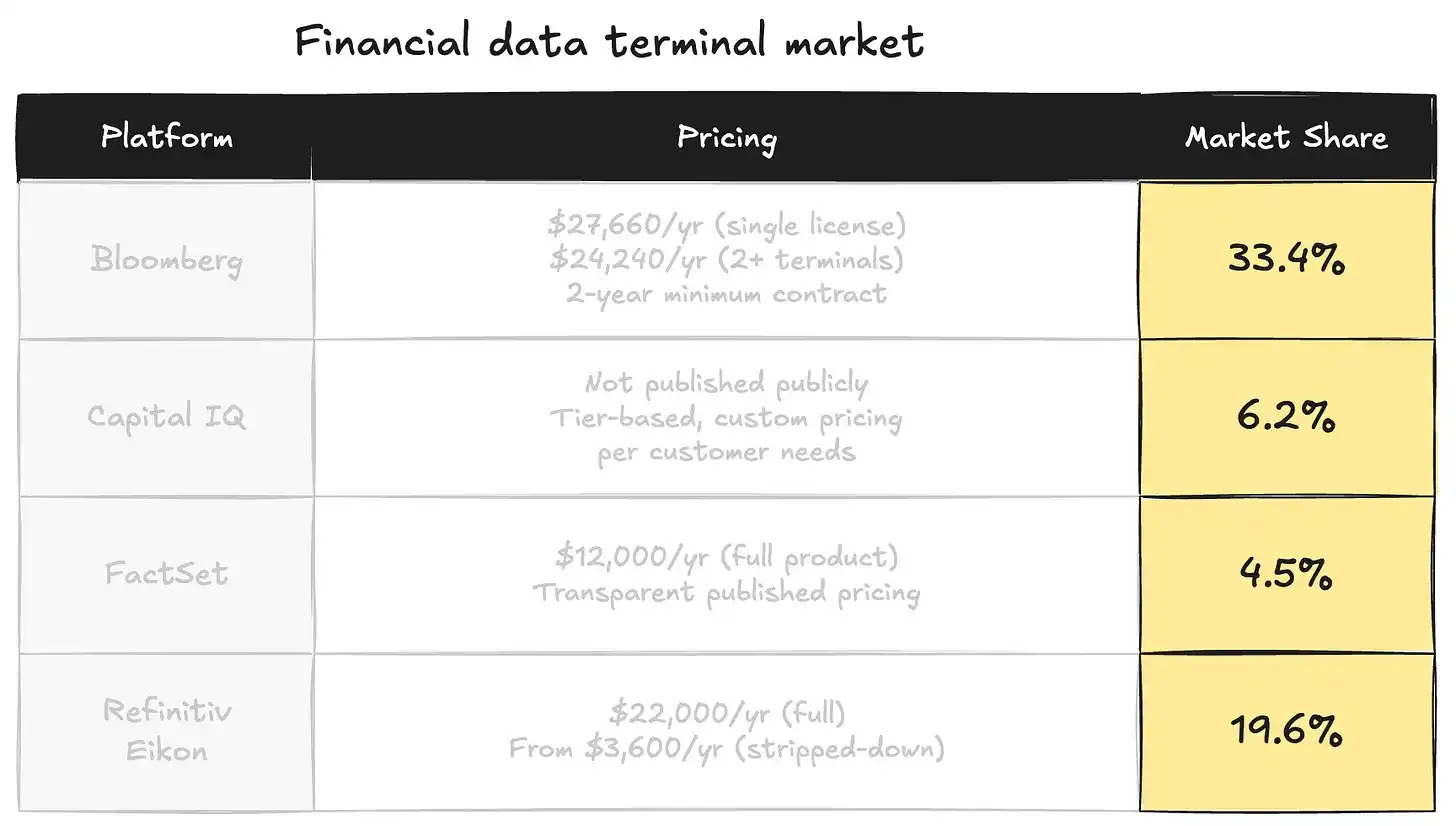

Индустрия финансовых данных стоит около 30 миллиардов долларов в год и является одной из наименее обсуждаемых монополий в мире, возможно, потому, что единственные, кто обращает на нее внимание, — это те, кто уже платит.

Bloomberg контролирует около 33% мирового рынка финансовых данных, только терминальный бизнес приносит более 10 миллиардов долларов годового дохода. Refinitiv, теперь приобретенный Лондонской фондовой биржей Group за 27 миллиардов долларов, занимает около 20% доли. ICE Data Services сообщает о доходах от рыночных данных в 2,8 миллиарда долларов. Далее следуют FactSet, S&P Global, Morningstar и некоторые региональные игроки, обслуживающие нишевые рынки. Четыре крупнейших поставщика вместе контролируют绝大部分 способов потока финансовых данных от генерирующих организаций к компаниям-потребителям.

Модель всех этих компаний одинакова. Биржи, торговые компании, банки и управляющие активами генерируют данные о ценах как побочный продукт своей работы. Они продают или лицензируют эти данные поставщикам. Поставщики упаковывают, стандартизируют эти данные, добавляют аналитические инструменты, а затем продают их всем остальным с значительной наценкой, заключая долгосрочные контракты и используя проприетарные методы доступа, чтобы сделать переход болезненным. Подписка Bloomberg блокирует вас на два года. Досрочная отмена требует оплаты 50% от оставшейся стоимости контракта. И все в опыте Bloomberg разработано так, чтобы уход казался сложнее, чем остаться. Клавиатура другая. Формат данных другой. Даже система обмена сообщениями, которую половина Уолл-стрит использует для общения друг с другом, работает на Bloomberg, что означает, что смена терминала также означает отказ от вашего списка контактов.

Эта практика сохранялась сорок лет, потому что поставщики решили действительно сложную проблему: получение данных из сотен источников, их очистка и стандартизация, доставка с низкой задержкой через глобальную инфраструктуру. Bloomberg заслужил свое место.

Но блокчейн — это лучший механизм распространения. Возможно, не для всего и еще не в полном масштабе. Но для конкретной проблемы соединения учреждений, владеющих данными, и разработчиков, желающих строить на их основе, программируемая публичная ончейн-инфраструктура структурно превосходит проприетарный терминал с двухлетним контрактом. Превращая данные в API без затрат на переход, вы предоставляете любому разработчику в любой цепи доступ без разрешений и самообслуживания. Это то, что делает Pyth.

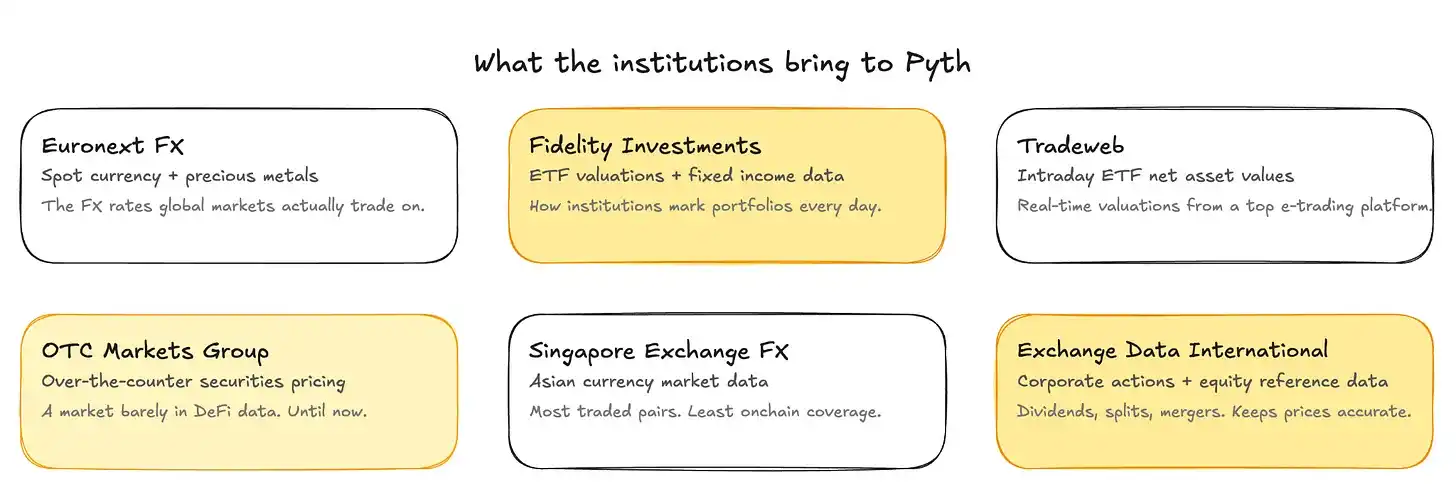

Euronext, Exchange Data International, Fidelity Investments, OTC Markets Group, валютное подразделение Сингапурской биржи и Tradeweb начали публиковать свои проприетарные рыночные данные напрямую в блокчейне через новый рынок данных Pyth.

Euronext Forex: спотовая валюта и драгоценные металлы. Обменные курсы валют, используемые для фактических операций на глобальных рынках.

Fidelity: оценка ETF и данные по fixed income. Данные, которые институты используют ежедневно для оценки рыночной стоимости портфелей.

Tradeweb: внутридневное ценообразование ETF. Реaltime-оценки от одной из крупнейших электронных торговых платформ.

OTC Markets Group: ценные бумаги внебиржевого рынка. Рынок, который почти отсутствует в сегодняшних данных DeFi.

Сингапурская биржа Forex: азиатские валютные пары. Валютный рынок с наибольшим объемом торгов, но наименьшим покрытием в ончейн.

Вместе эти шесть учреждений покрывают значительную часть классов активов, которые DeFi никогда не мог надежно построить, потому что данные, питающие эти активы, не были институционального уровня.

Почему данные должны быть перед активами

Все в криптосекторе говорят о волне токенизации уже два года: токенизированные казначейские обязательства, токенизированные облигации, токенизированные акции. Вся дискуссия предполагает, что сложная часть — это размещение активов в блокчейне.

Но сложная часть — это данные. Прежде чем вы сможете торговать токенизированными казначейскими обязательствами в протоколе DeFi, вам нужно знать, сколько они стоят сейчас, с точностью до секунды, с той же точностью, которую использует торговый стол Goldman Sachs для оценки этого инструмента. Прежде чем вы сможете построить кредитные протоколы вокруг реальных мировых активов, вам нужен непрерывный источник цен от институтов, которые фактически маркетмейкерят, а не парсинг с веб-сайтов, обновляемый каждые несколько минут.

Протоколам DeFi нужны точные данные традиционных финансов в реальном времени для деривативов, кредитов и структурированных продуктов, но исторически они полагались на ограниченные или более медленные источники данных. Вот почему DeFi от рождения до настоящего времени в основном представляет собой криптовалюту против криптовалюты. Данные, питающие эти продукты, были недостаточно надежными, недостаточно быстрыми и не от институтов с достаточной степенью доверия в регуляторных диалогах.

Pyth Pro — это уровень институциональной подписки, запущенный Pyth в сентябре 2025 года, предлагающий источники цен с задержкой 1 мс по более чем 2200 инструментам. Polymarket в апреле 2026 года интегрировал Pyth Pro для расчета новых рынков по традиционным активам, включая основные фондовые индексы, товары и акции США, заменив ручные или биржевые специфические источники данных стандартизированными агрегированными данными от более чем 125 торговых компаний. Hyperliquid теперь использует источники цен Pyth для запуска perpetual-контрактов на нефть и золото. Качество данных достигает уровня, на котором можно строить серьезные финансовые продукты, не извиняясь.

Волне токенизации нужен этот слой для работы в масштабе. Без надежного источника цен fixed income вы не можете построить надежный продукт fixed income в ончейн.

Война оракулов

Изначальная проблема оракулов в криптовалюте была простой: смарт-контракты живут в блокчейне, цены живут вне его. Что-то должно соединить их. Chainlink был доминирующим оракулом на протяжении большей части истории DeFi, решая эту проблему с помощью большой сети независимых узлов, которые получают цены из сторонних источников (биржи, агрегаторы, API данных) и отправляют их в блокчейн. Много независимых источников, много независимых узлов, разумная децентрализация, приемлемая задержка.

Pyth с самого начала采用了不同的方法, обращаясь напрямую к实际 торгующим институтам. Сейчас более 120 институтов публикуют данные через Pyth, включая глобальные биржи, торговые компании и маркетмейкеров. Jane Street не二手 описывает цену Биткойна для Pyth, а становится издателем. Данные поступают из источника, а не от того, кто описывает источник.

Это быстрее, точнее и более непосредственно привязано к реальной рыночной активности, чем агрегированные источники цен. В структурном смысле это также более централизованно: более узкий клуб издателей, которые в основном знают друг друга и проверяют свои собственные данные. У Pyth есть механизмы стейкинга и слэшинга (конфискации), предназначенные для создания экономических стимулов для точности. Но, возможно, лучше сказать, что Pyth выбрала скорость и качество данных вместо максимизации децентрализации. Для институциональных финансов это может быть правильный компромисс.

Цена централизации

Создание Pyth involved значительное участие Jump Crypto, организации, которая сыграла важную роль в событиях 2022 года, которые большинство в криптосообществе не хочет вспоминать. Сеть издателей — это узкий клуб, институты в основном знают друг друга и проверяют данные друг друга. Механизмы стейкинга и слэшинга создают экономические стимулы для точности, но Pyth одновременно и быстрее, и качественнее, чем предыдущие решения, и более централизована, чем может показаться из маркетинга. Вы не заменяете монополию общим достоянием. Вы заменяете одну централизованную систему другой, которая, как оказалось, работает на блокчейне.

Токен PYTH достиг исторического максимума в 1,20 доллара в марте 2024 года, в настоящее время торгуется около 0,046 доллара, что примерно на 96% ниже пика. Очевидная причина: для использования данных Pyth не требуется持有或购买 PYTH. Сеть может значительно расти, а токен оставаться в диапазоне, это известная проблема, которую пытается решить резервный план Pyth, который分配一部分 дохода протокола на обратный выкуп PYTH на открытом рынке.

Конец пункта взимания платы

Доставка данных от генерирующих организаций на столы тех, кому они нужны, требует оборудования, проприетарных сетей, отношений с продажами и постоянной поддержки. Bloomberg решил все это и взимает плату соответственно. У производителей данных не было альтернативного механизма распространения, поэтому они продавали данные посредникам, которые оставляли прибыль себе. Блокчейн устраняет это конкретное трение. Не анализ, не рабочие процессы, не клавиатуры. Только та часть, где кто-то должен был перемещать данные из одного места в другое и брать плату за эту привилегию.

Но Bloomberg продает рабочие процессы. Терминал, клавиатура, система сообщений, аналитика, команда поддержки. Трейдеры строят вокруг него всю карьеру. Pyth не продает ничего из этого. Это уровень данных, в который вставляется протокол. Единственная перекрывающаяся часть — это сами базовые данные, и эта часть только что переместилась.

Это важно, потому что если Fidelity публикует свою оценку ETF в блокчейне, любой разработчик в любом месте может прочитать эти данные без переговоров о лицензионном соглашении, без ежегодной оплаты 32 000 долларов, без ожидания стандартизации формата поставщиком. Данные становятся программируемой инфраструктурой, а не проприетарным продуктом. Учреждения сохраняют контроль над тем, что публикуют, и сохраняют авторство. Работа посредника — перемещение данных от источника к пользователю — становится ненужной.

Эти шесть учреждений выбирают Pyth в качестве основного канала распространения, что является обязательством иной категории, чем пилотный проект. Пилотный проект可以被关掉, когда advocating его的人 меняет работу. Основной канал распространения становится операционной зависимостью.

Токенизированные облигации, токенизированные акции, токенизированное все. Большинство из этого находятся в нескольких месяцах или годах от значительного масштаба. Но сырье, которое делает продукты реальных мировых активов возможными в DeFi, теперь доступно без контрактов, без терминалов, без двухлетних минимальных обязательств.

Майкл Блумберг потратил месяцы, разнося бесплатный кофе в коридорах Merrill Lynch, потому что нужные ему данные были locked в учреждениях, у которых не было причин给他 их. Он построил на этом трении весь свой бизнес.

Пункты взимания платы не исчезнут в одночасье. Каждая монополия в распространении данных заканчивается одинаково. Не битвой, не законом, не революцией. В основном кто-то где-то спрашивает, зачем они платят за то, чем уже владеют.