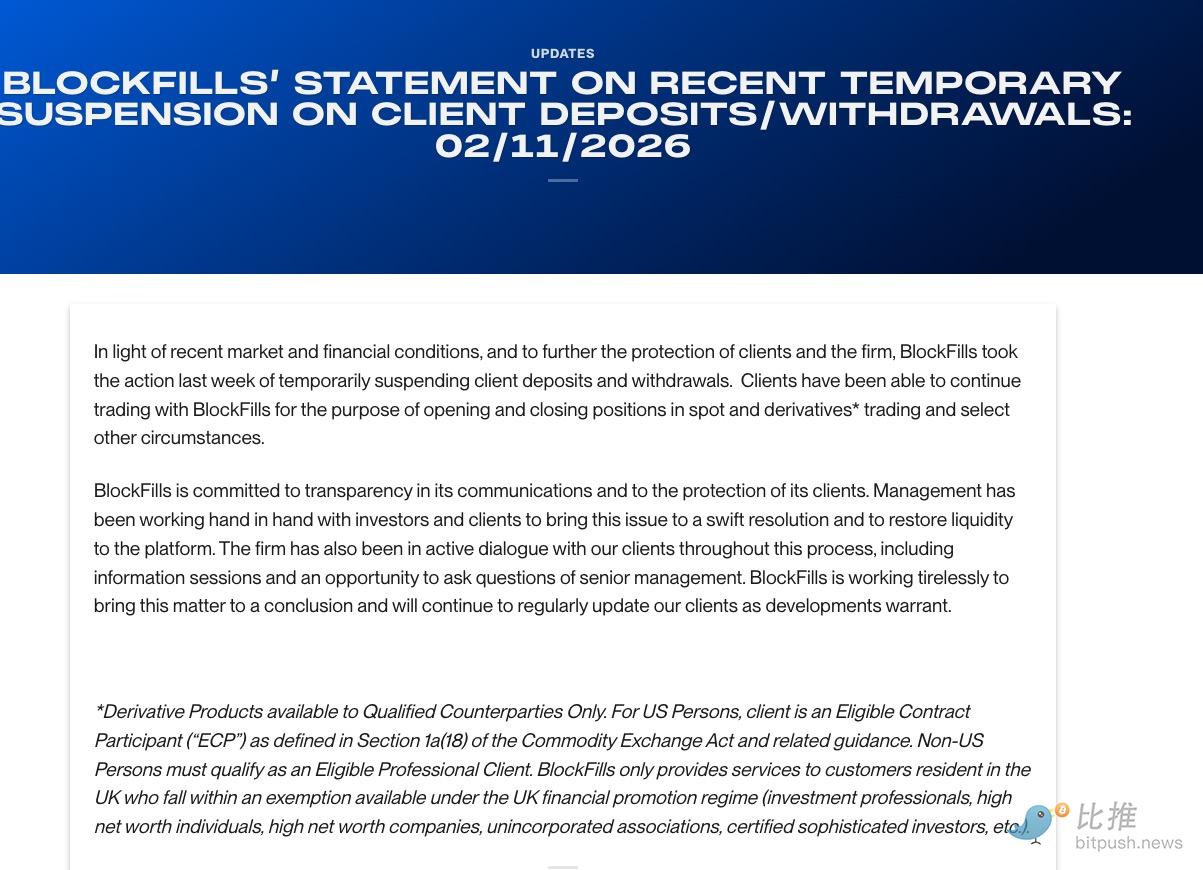

The day Celsius halted operations, it also used the phrase "temporary liquidity adjustment." Four years later, BlockFills has turned to the exact same page in the same playbook.

This lending platform, which claims to serve over 2,000 institutional clients and processed over $61.1 billion in trading volume in 2025, has initiated an internal circuit breaker. The official statement was measured in its wording: not a default, not bankruptcy, but a "temporary measure taken to protect the interests of clients and the company." Clients can still open and close positions, but funds cannot be withdrawn.

How familiar it smells. When Celsius collapsed in 2022, its opening line was also "temporary liquidity adjustment."

BlockFills' move immediately triggered collective market anxiety: Are we about to witness a repeat of the 2022 tragedies of Celsius and Genesis?

Who is BlockFills?

Founded in Chicago in 2018, this company is not a grassroots project, nor a Dubai-based exile exchange. It's based in Chicago—the Jerusalem of derivatives markets, home to the CME. Its core team comes from traditional finance market making and trading backends. Two names are written on its early investor list: CME Ventures and Susquehanna International Group (SIG).

What caliber of player is Susquehanna? A top-tier Wall Street market maker, accounting for over 30% of annual US options trading volume, and also an early investor in TikTok's parent company, ByteDance. It's not the kind of Crypto VC that chases hot trends and sprays money around; it's old money that stations actuaries upstairs at the exchange.

In 2021, BlockFills completed a $6 million seed round; on the eve of FTX's collapse in 2022, it counter-trend completed a $37 million Series A round. The lead investor was again Susquehanna Capital, with the follow-on list including CME Ventures, Simplex, C6 Ventures, and even Nexo.

Therefore, BlockFills is a "regular army" piece placed by traditional financial giants in the crypto lending arena. Its clients aren't the retail investors who rushed in during 2021, but miners, hedge funds, family offices, market makers, payment processors—over 2,000 institutions across 95 countries. Last year, the payment processor C14 alone processed billions of dollars in onboarding business through it.

Such a company initiating a "voluntary circuit breaker" is more worrying than the blow-up of any retail lending platform in 2022.

Who is BlockFills' largest client group?

Most likely, miners.

According to the official company disclosure, as of 2025, BlockFills provided approximately $150 million in financing and asset management solutions for global miners. As for which specific mining companies received this money, BlockFills did not say. As a platform serving 2,000 institutional clients, publicly disclosing a client list violates both commercial惯例 and privacy red lines. We can only find some clues from scattered public information: it has partnered with payment processor C14, integrated with Fireblocks and Zodia Custody, but those are ecosystem partners, not the borrowers.

The borrowers are silent, but their balance sheets don't lie.

Bitcoin fell from $120,000 to just over $60,000 in less than four months. In early February, "shutdown" warnings began circulating in mining circles. The breakeven line for Antminer S19 series models is around $70,000, and the coin price had been lying below that number for two weeks.

When an industry benchmark like MARA was monitored transferring over 1,300 BTC to an exchange—when the industry benchmark chooses to cut its losses and exit at the $60,000 mark—how many within BlockFills' miner client group were already in technical default?

Is it a "Protective Mechanism" or a "Precursor to Collapse"?

Fintech consultant Dr. Anya Sharma points out that such suspensions are essentially an extension of the "circuit breaker" mechanism in traditional finance. In the digital asset space, the lag of blockchain settlement and potential price flash crashes can lead to collateral valuation failures. Suspending services allows the system to recalibrate, preventing a complete meltdown caused by asset-liability mismatches.

Furthermore, compared to the retail platforms that failed in the 2022 bankruptcy wave, BlockFills has two significant "moats":

-

Top-Tier "Blue-Blood" Background:

BlockFills is backed by CME (Chicago Mercantile Exchange) and Susquehanna (SIG). These traditional financial giants not only provide credit endorsement but are also more likely to provide liquidity support (bailout) at critical moments.

-

Institutionalized Risk Control:

Celsius/BlockFi (Retail High-Yield Model): They attracted funds by promising high interest rates (10%-20% APY) to ordinary retail investors, then invested in high-risk projects (like Three Arrows Capital). This is a typical "high-cost liability" model, extremely fragile. BlockFills is more like a "cryptocurrency bank trading desk." Its funding sources are primarily institutional clients, and its business focus is providing hedging for miners and trading liquidity for hedge funds. BlockFills' business logic is closer to traditional finance, and its accounts are theoretically more transparent than the more Ponzi-esque model of Celsius.

Therefore, if BlockFills can resume services shortly (e.g., within 72 hours or a week) and transparently disclose its asset status, it will become a model of "risk management," proving that institutional-grade infrastructure is indeed more resilient than the previous generation of platforms. Conversely, if the suspension is prolonged, it will inevitably become the first giant domino to fall in this bear market, triggering a credit collapse in the institutional lending space.

Author: Little Bear Biscuit | Bitpush

Twitter:https://twitter.com/BitpushNewsCN

Bitpush TG Discussion:https://t.me/BitPushCommunity

Bitpush TG Subscription: https://t.me/bitpush