Written by: angelilu, Foresight News

Original title: Crude Oil Surges 25%, Hyperliquid Stages On-Chain Life-and-Death Game

"Friends shorting crude oil are completely fired up."

When on-chain analyst Ai Yi sent this tweet on the morning of March 9, WTI crude oil touched $108 per barrel. The account at the top of Hyperliquid's holdings leaderboard was facing a floating loss approaching $3.4 million, with the liquidation price set at $120.76.

As of publication, the WTI crude oil contract price reached an intraday high of $119.5 and is currently reported at $114.5, accumulating a gain of over 25% since last Friday's closing price.

Due to a Strait, Crude Oil Surges Over 40% in a Week

The story begins with Iran's Strait of Hormuz.

By March 9, the Strait of Hormuz had been almost completely blocked for seven consecutive days. The shutdown of this choke point, which carries about 20% of the world's oil supply, triggered a market quake. By March 9, the WTI crude oil price had surged dramatically within just a week, setting a rare volatility record in recent years, accumulating a gain of over 40% compared to pre-conflict levels.

The shockwaves spread rapidly. The Nikkei index fell 5.4% in a single day, its largest drop since the tariff turmoil; South Korea's KOSPI plummeted 7%; Germany's DAX fell over 3%. Bitcoin was not spared either, falling below $66,000, with the crypto market seeing $120 million in liquidations within an hour. The Crypto Fear & Greed Index dropped to 12, entering the "extreme fear" zone.

But on Hyperliquid, another war was raging.

Three Stories of Shorting Crude Oil

In the on-chain circle, CBB (@Cbb0fe) is not an unfamiliar face. A few months ago, he publicly formed a team specifically to "hunt" another whale, @qwatio. This time, he himself became the prey.

https://x.com/lookonchain/status/2030817006107369727

According to Lookonchain monitoring, CBB shorted 127,175 xyz:CL (WTI crude oil mapping contracts) at an average price of $78.37, with a notional value of approximately $13.78 million. As oil prices soared, his floating loss reached $3.81 million, with the liquidation price hanging at $120.76.

Only a few tenths of a dollar away from that number. But no one knows when the situation in Iran will cool down.

Another account, "2 frères 2 fauves," is in equally dangerous territory. He entered a short position at $78.36, currently holding 12,717 CL with a notional value of approximately $13.37 million, ranking first in CL contract holdings on Hyperliquid. His floating loss is $3.4 million, with the same liquidation price of $120.76.

More dramatic is the experience of whale 0x8Af7. He shorted 72,179 CL (approx. $7.8 million). As oil prices rose, his short position was entirely force-liquidated, resulting in a loss exceeding $1.55 million.

Yet, just hours after the liquidation, he immediately reopened a position—60,166 new short contracts, with a notional value of $6.48 million.

Was it a misjudgment or inherent gambling tendencies? Perhaps both. But this choice itself speaks to a certain ethos of on-chain high-leverage trading: liquidation is not the end, just the conclusion of the previous round.

There Are Also Winners, The Other Side of a Sky Co-Founder

On the same Hyperliquid, during the same period, Sky (formerly MakerDAO) co-founder Rune Christensen was laughing on the other side, watching the storm.

On-chain analyst EmberCN disclosed that RuneKek (Rune's on-chain account) went long on approximately $7.82 million worth of crude oil contracts, with an entry cost around $93. As of today, with oil prices touching $109, his floating profit has exceeded $1.36 million.

More noteworthy is his portfolio strategy: while going long on crude oil, he also shorted some ETH and XYZ100 (US stock index mapping contracts). This makes his strategy more like a hedge against geopolitical conflict—crude oil benefits from war premiums, while stocks and cryptocurrencies suffer from risk-off sentiment. By positioning on both sides, he hedges out the risk of a one-way bet.

Rune Christensen, a DeFi protocol founder, used on-chain perpetual contracts to build a macro hedging portfolio. This fact itself is more noteworthy than how much money he made.

On-Chain Commodities: New Tools, Old Lessons

This round of oil行情 pushed a previously inconspicuous topic to the forefront: on-chain commodity trading.

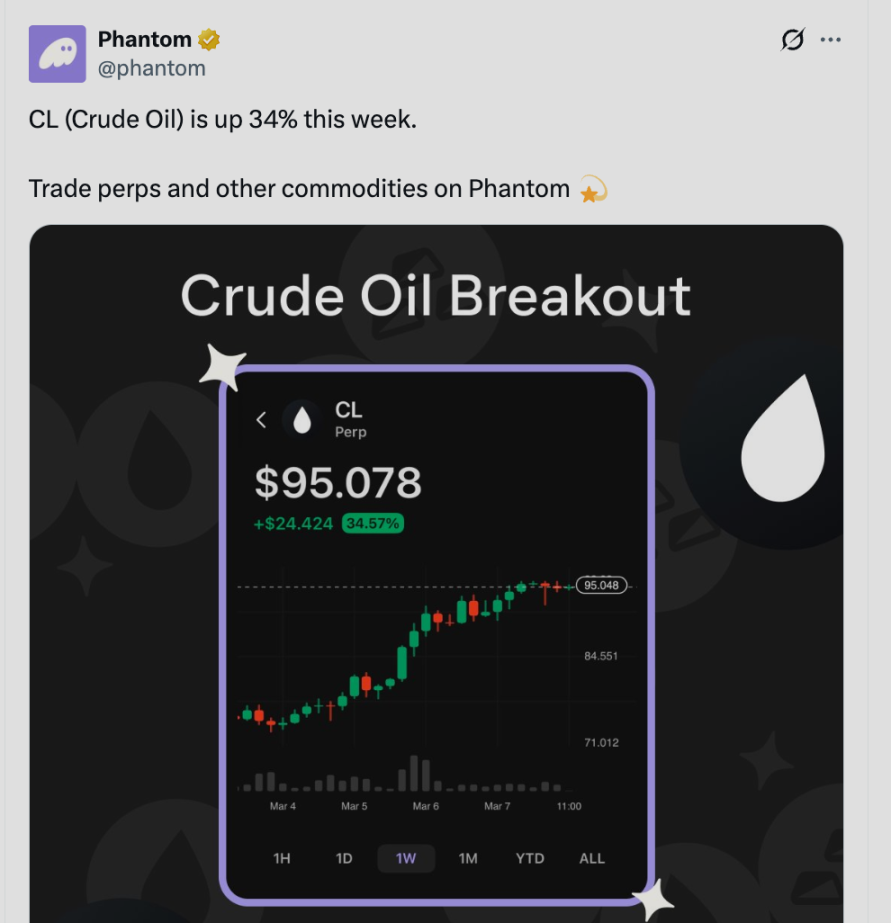

The crude oil on Hyperliquid was launched by the Felix protocol (HIP-3 market deployer on Hyperliquid) on January 9, 2026, about two months ago. The initial parameters were a maximum of 5x leverage and an open interest cap of $2.5 million, representing an early small-scale launch. Trading volume only truly exploded after Iran blocked the strait.

Platforms like Phantom have also陆续 launched perpetual contracts for traditional commodities like crude oil and gold. Theoretically, anyone with a wallet can trade crude oil futures like they trade Bitcoin, without opening a traditional futures account or needing a broker.

This is genuine financial democratization. But the other side of the coin is equally real.

Traditional commodity futures markets have strict margin systems, circuit breakers, position limits, and are backed by risk control teams from brokers constantly monitoring the screens. The rules of on-chain perpetual contracts are much simpler: if the position value falls to the liquidation line, the system automatically force-closes it. There are no phone call reminders, no manual intervention.

The liquidation prices for CBB, "2 frères 2 fauves," and others are all set near $120.76—this number isn't random; it's the "safety margin" they calculated when initially building their positions. In normal oil price fluctuations, having over fifty dollars of room from the entry price of $78 seemed quite ample.

But what they didn't anticipate was that a geopolitical crisis could push oil prices up 50% within 72 hours.

This isn't a strategy error; it's a black swan arrival. The problem is, on-chain, there is no mechanism to let you catch your breath when the black swan lands.

When DeFi Meets Hormuz

The connection between the crypto market and traditional geopolitics is happening faster than anyone anticipated.

Hyperliquid users now need to watch the latest developments in Iran's Strait of Hormuz; while DeFi OGs are using on-chain derivatives to hedge war risks.

As the variety of on-chain commodities and on-chain US stock mapping contracts continues to expand, on-chain players will only be increasingly exposed to macro risks. In the traditional financial world, this is called "global macro strategy," requiring professional teams and robust risk control systems. On-chain, it's called "one person's position."