Original | Odaily Planet Daily (@OdailyChina)

Author | DingDang (@XiaMiPP)

In the stablecoin industry chain, Circle and Stripe used to be a pair of partners with very clear division of labor.

Circle was responsible for mapping US dollars from the real world onto the blockchain, minting them into the stablecoin USDC; Stripe, through its global internet payment network, enabled these digital dollars to flow in real business scenarios. One was responsible for producing money, the other for making it flow. This alliance was almost naturally complementary in the past few years.

However, two recent events, when viewed together, create a subtle feeling: these two companies seem to be slowly moving towards the same place.

On February 11th, Stripe announced the launch of x402 payment functionality on Base. This feature allows developers to charge AI agents directly using USDC. Stablecoins are no longer just pricing tools on exchanges; in the wave of AI Agents, they will become the payment medium for transactions between machines.

In the same week, Bridge, a stablecoin infrastructure company under Stripe, received preliminary approval for a trust bank charter from the U.S. Office of the Comptroller of the Currency (OCC). This means Bridge could potentially advance businesses like stablecoin issuance, custody, and reserve management as a regulated financial institution.

On one side, Stripe is building new payment scenarios using USDC; on the other side, it is building its own stablecoin financial infrastructure.

The Stablecoin Industry Chain of the Old Era

If we break down the stablecoin world, the industry chain is not very complicated.

The bottom layer is the issuance layer. Institutions like Circle are responsible for mapping real-world dollar reserves onto the blockchain, minting them into stablecoins, such as USDC. The layer above is the settlement layer, handled by blockchain networks which manage fund accounting and clearing. Moving up further is the payment layer. Internet payment infrastructure like Stripe embeds stablecoins into real business transactions, allowing on-chain funds to enter scenarios like e-commerce, SaaS, or cross-border trade. At the top is the application layer. Various specific financial activities happen here, from DeFi to AI Agent payments.

When stablecoins were just tools for the crypto market, participants in this industry chain always had their own clear responsibilities Issuers were responsible for "minting coins," payment platforms for "collecting money," blockchains for settlement, and developers focused on application scenarios.

As early as 2014, Stripe was one of the first mainstream payment processors to support Bitcoin payments. However, due to issues like excessive Bitcoin price volatility, long transaction confirmation times, and unpredictable fees, this business attempt was eventually discontinued in 2018. Bitcoin was more like a speculative asset than a currency suitable for internet payments.

The emergence of stablecoins恰好 filled this gap. The price stability, programmability, and on-chain settlement capabilities of USDC made it closer to Stripe's ideal "internet-native currency." In 2022, Stripe re-entered the crypto space, choosing to support USDC payments. This step not only brought stablecoins back into the mainstream payment system but also objectively drove the rapid growth of USDC's circulation scale, with its circulating market cap once exceeding $55 billion.

Under this synergistic relationship, Circle provided stable digital dollars, Stripe provided the global payment network, and together they propelled USDC from a crypto trading tool to a market approaching $70 billion.

On-chain data also confirms the scale effect brought by this synergy. According to Artemis data, in January, the scale of on-chain USDC transactions exceeded 8.4 trillion, while the total scale of on-chain transactions for the stablecoin market was 10 trillion. That is, in terms of transaction count, USDC accounts for 84% of the total market share.

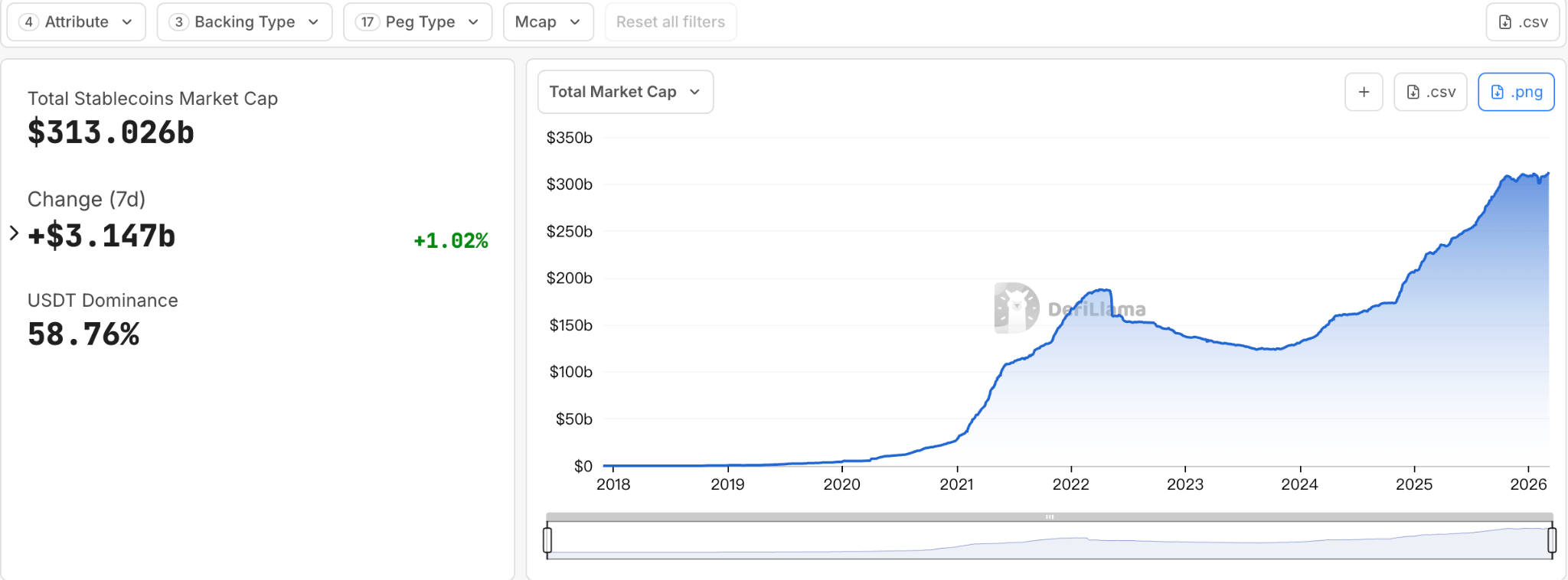

Meanwhile, the external regulatory environment has also undergone significant changes. With the formal enactment of the GENIUS Act, stablecoins—once a financial experiment in a regulatory gray area—are gradually being incorporated into the legal financial system. Today, the stablecoin market size exceeds $300 billion. In the future, the scale carried by this market could be a trillion-dollar financial network.

Stablecoins are no longer just internal tools for the crypto market but are beginning to be seen as part of the next generation of financial infrastructure. When a market evolves from a crypto tool into financial infrastructure, the industrial logic often changes accordingly.

When Stablecoins Become Infrastructure

In any financial system, truly stable profits often do not come from a single link but from control over key nodes. Whoever can control the轨道 (track) of fund flow can define the rules.

If stablecoins are merely the underlying asset, while payment gateways, developer tools, and business scenarios are all controlled by other platforms, the profits ultimately available to the issuer are actually quite limited. Conversely, if one controls the payment network or settlement system, they can continuously capture value at every stage of the fund flow.

Therefore, when stablecoins begin to evolve from a crypto asset into financial infrastructure, an almost inevitable trend emerges: originally dispersed industry roles at different levels begin to try to extend upstream and downstream, bringing more links into their own systems.

This process is not unfamiliar in financial history. From banking systems to credit card networks, to internet payment platforms, mature financial systems often eventually go through similar stages—from role dispersion to structural integration.

Now, this wind of industrial integration is also blowing into the world of stablecoins.

If we view the stablecoin industry chain as a vertical structure, then over the past few years, Circle and Stripe stood at opposite ends of this chain. Now, they are both moving towards the center.

Circle: Not Wanting to Be Just a "Money Printer"

In the on-chain ecosystem, the circulation efficiency and usage frequency of USDC can no longer be ignored. In the latest stablecoin flow report, the velocity of USDC circulation is almost 5 times that of USDT.

However, relying solely on issuing stablecoins is not a particularly imaginative business model in itself.

The main revenue sources for stablecoin issuers roughly consist of two parts: first, the interest income generated by the reserve assets, and second, the fees associated with the issuance and redemption of stablecoins. But as the stablecoin scale continues to expand, this income often still needs to be shared with ecosystem partners. For example, as one of the most important distribution channels for USDC, Coinbase receives nearly $1 billion in profit sharing from the USDC system annually. This means that even though the issuer undertakes the core "minting" role in the stablecoin system, its actual disposable profit space is still constrained by the ecosystem structure.

This also explains why, over the past two years, Circle's strategy has clearly extended towards the application layer: it is no longer satisfied with merely issuing stablecoins but is trying to build a complete stablecoin payment network.

Based on current public information, Circle's layout at the application layer is roughly a three-step process.

Step one: Arc, an L1 blockchain designed for enterprises. It plays a "coordination layer" role at the application level, helping developers build applications for payments, settlement, etc. Arc launched its testnet in October 2025, has attracted 100+ companies to participate, processed over 166 million transactions, and the mainnet is planned to launch within 2026.

Step two: With USDC at the core, use the Cross-Chain Transfer Protocol (CCTP) and gateway tools to solve liquidity fragmentation. At the application layer, help enterprises unify USDC from multiple chains onto Arc and CPN, enabling seamless distribution and application building.

Step three, and also Circle's core application layer product: CPN (Circle Payments Network). Launched in May 2025, it is an "open standard" payment coordination network specifically designed for programmable, compliant, and auditable payments. So far, 55 financial institutions have registered, with another 74 financial institutions undergoing资格审查 (qualification review).

This layout shows that Circle is evolving from a mere stablecoin issuer to gradually building a整套 (complete set) of application infrastructure capable of carrying fund flows.

Stripe: The "Checkout Counter" Also Wants to Control the轨道 (Track)

Stripe is at the other end of the stablecoin system. As one of the world's most important internet payment infrastructures, Stripe controls huge merchant gateways. In 2025, the total payment volume processed on the Stripe platform reached $1.9 trillion, a year-on-year increase of 34%, equivalent to about 1.6% of global GDP. From Shopify to Amazon, the payment systems of many internet merchants are built on Stripe's infrastructure. In a sense, Stripe does not produce currency, but it controls the entry point for currency flow.

But if in the future stablecoin issuers and blockchain networks jointly control the settlement layer, payment platforms might be compressed into mere technical service providers.

This is also why Stripe has systematically begun布局 (laying out) across the industry chain's upstream and downstream in recent years.

In February 2025, Stripe completed the acquisition of the stablecoin infrastructure platform Bridge for $1.1 billion. Finally, on February 12th this year, Bridge received conditional approval from the OCC, which is the most critical piece for Stripe's infrastructure ambitions.

At the same time, Stripe is also jointly incubating the L1 public chain Tempo with Paradigm, hoping to build a settlement chain specifically for internet finance. The public testnet went live in December 2025, and the mainnet is planned to launch within 2026.

Additionally, in 2025, Stripe acquired wallet infrastructure company Privy, providing users with embedded wallets and identity systems, thereby lowering the barrier for users to enter the on-chain financial system.

If we look at these actions together, a very clear trend emerges: Stripe is extending downwards from the payment entry point, trying to master the underlying轨道 (track) on which stablecoins run.

Two Companies Meet in the Middle of the Industry Chain

Circle is extending from the issuance layer towards the application layer, while Stripe is descending from the payment layer towards the infrastructure. When both paths move towards the center of the industry chain simultaneously, the originally clear boundaries inevitably begin to overlap.

Against the backdrop of the reshaping stablecoin industry structure, it serves more as a reminder: the competition for stablecoins is no longer just about "who issues more tokens." The truly important question in the future might be—who controls the轨道 (track) of stablecoin flow.

As issuance, settlement, payment, and application are gradually reintegrated, competition in the stablecoin world will also shift from "asset scale" to "financial network." And on this new track, Circle and Stripe, this pair of once highly complementary allies, have already begun to meet in the middle of the industry chain.

The story of stablecoins is also evolving from a crypto industry experiment to a reconstruction of financial networks.

Recommended Reading

《Latest Stablecoin Report: Real Distribution and Flow Are Far More Worth Attention Than Supply》

《Behind Circle's Strong Stock Rebound: AI, Prediction Markets, and Institutional Adoption》