Written by: Prathik Desai

Translated by: Chopper, Foresight News

Throughout the long history of banking, depositors have always been in a disadvantaged position. People deposit their funds in banks, which then lend these funds out, earning returns many times greater than the interest paid to savers. Depositors accept this model because there has historically been no better alternative: holding cash sees its value continuously erode over time.

Currently, the average interest rate for a standard U.S. savings account is only 0.6%, but investing in U.S. Treasury bonds or money market funds yields at least 4%. This traditional model has persisted for so long primarily because depositors have lacked convenient alternatives. However, every few decades, new choices emerge in the market.

Stablecoins, built on blockchain technology, enable 24/7 global circulation, settlement in seconds, and transfer costs of less than a penny. Although relevant laws prohibit stablecoin issuers from directly paying interest to holders, the composable nature of decentralized finance allows users to deposit stablecoins into lending protocols, earning annualized yields of 5% to 8%. This offers depositors a new destination for their funds without compromising on convenience.

In this article, we will analyze the various measures banks are taking to prevent deposit outflows and how this transformation will reshape the global banking industry and the flow of capital.

Depositor Behavior

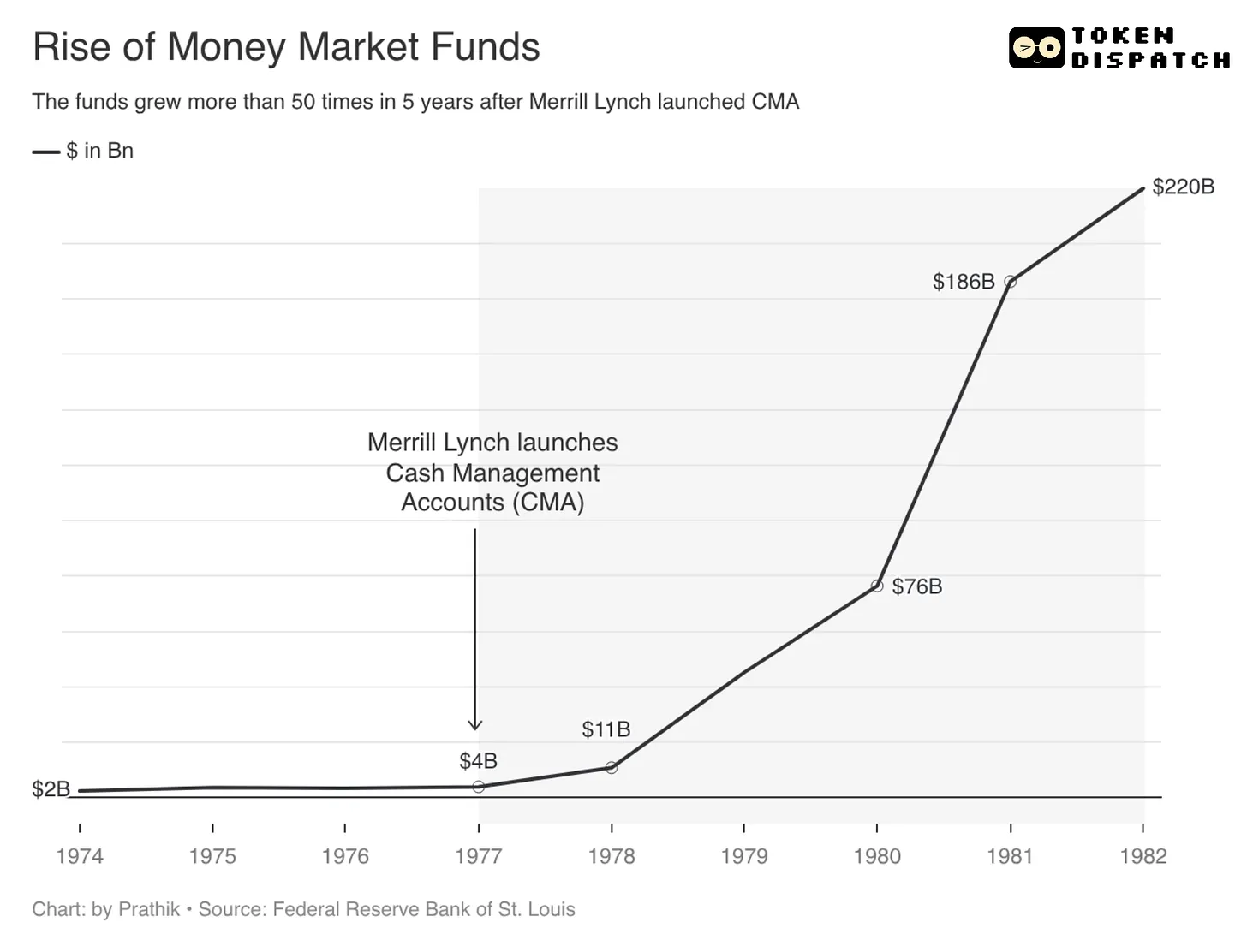

In 1977, wealth management and investment firm Merrill Lynch introduced the Cash Management Account (CMA). At the time, U.S. Regulation Q capped deposit interest rates at no more than 5.25%, while U.S. Treasury yields exceeded 7%. Merrill Lynch identified a regulatory loophole and leveraged the CMA's functionality to automatically sweep clients' idle cash from their securities accounts into money market funds daily. Simultaneously, Merrill Lynch provided clients with checking account and debit card services.

The combination of these features allowed clients to enjoy high market-level yields while accessing their funds as easily as from a checking account. This led to explosive growth in money market funds, soaring from about $4 billion in 1977 to $220 billion in 1982—a 55-fold increase—fueled largely by massive outflows from bank deposits.

The banking industry immediately protested. Ultimately, the U.S. Congress repealed the interest rate caps under Regulation Q, and major banks顺势推出货币市场存款账户,凭借更高的收益率重新吸纳存款. From the inception of the Cash Management Account to the removal of deposit rate restrictions, the entire process took nine years.

Today, technological innovations have reduced fund transfer times to minutes or even less, and depositors are no longer willing to wait for extended periods.

During the Silicon Valley Bank crisis on March 8, 2023, depositors requested withdrawals totaling $42 billion in less than eight hours, averaging about $1.5 million per second. Over 85% of the bank's deposits were uninsured, which was the core reason for the concentrated bank run.

Prudent depositors will always move their funds to safer places where the capital can at least preserve its value, if not appreciate.

Two Digital Dollars

In response to this issue, two competing forms of digital dollars have emerged in the market, each heading in distinctly different directions: one moves funds outside the banking system, while the other keeps them within, albeit in a transformed format.

The First: Stablecoins

Taking USDC, issued by Circle, as an example: when users convert dollars to USDC, the corresponding fiat funds are used to purchase U.S. Treasury bonds, thereby exiting the bank's balance sheet. This reduces the principal banks have available for lending and earning interest spreads. Simultaneously, these funds also lose the protection of FDIC insurance. If the stablecoin issuer ceases operations, holders may find it difficult to recover their principal.

The GENIUS Act, which officially took effect in July 2025, specifically establishes regulatory rules for the issuance and use of stablecoins. The Act explicitly prohibits stablecoin issuers from paying interest to users—a control measure reminiscent of Regulation Q's deposit rate limits. However, just as Merrill Lynch circumvented Regulation Q by using money market funds to achieve higher yields, stablecoin issuers now provide returns through reward distribution, a practice currently under debate within the legislative discussions of the CLARITY Act. Alternatively, users can independently deposit stablecoins into various lending protocols to earn yields.

For the banking industry, this is undoubtedly an existential threat. During the Silicon Valley Bank collapse, massive deposits flowed out of the banking system within hours. Standard Chartered predicts that by 2028, up to $500 billion in bank deposits could gradually shift to stablecoins, with U.S. regional banks being the most severely impacted, as their revenue heavily relies on net interest margin operations.

Even if these predictions do not fully materialize, the trend of deposit outflow is clear. This is precisely why, for the first time in decades, America's four largest banks have joined forces to explore new countermeasures.

The Second: Tokenized Deposits

The core advantages of stablecoins are low transfer costs and sub-second settlement. Addressing this pain point, the banking industry has introduced tokenized deposits.

Banks can convert users' deposits into on-chain token forms, which can circulate on blockchain networks with low cost and high efficiency. Simultaneously, the original dollar deposits remain on the bank's balance sheet, allowing banks to continue normal lending operations and earn interest. Moreover, tokenized deposits are still insured by the FDIC.

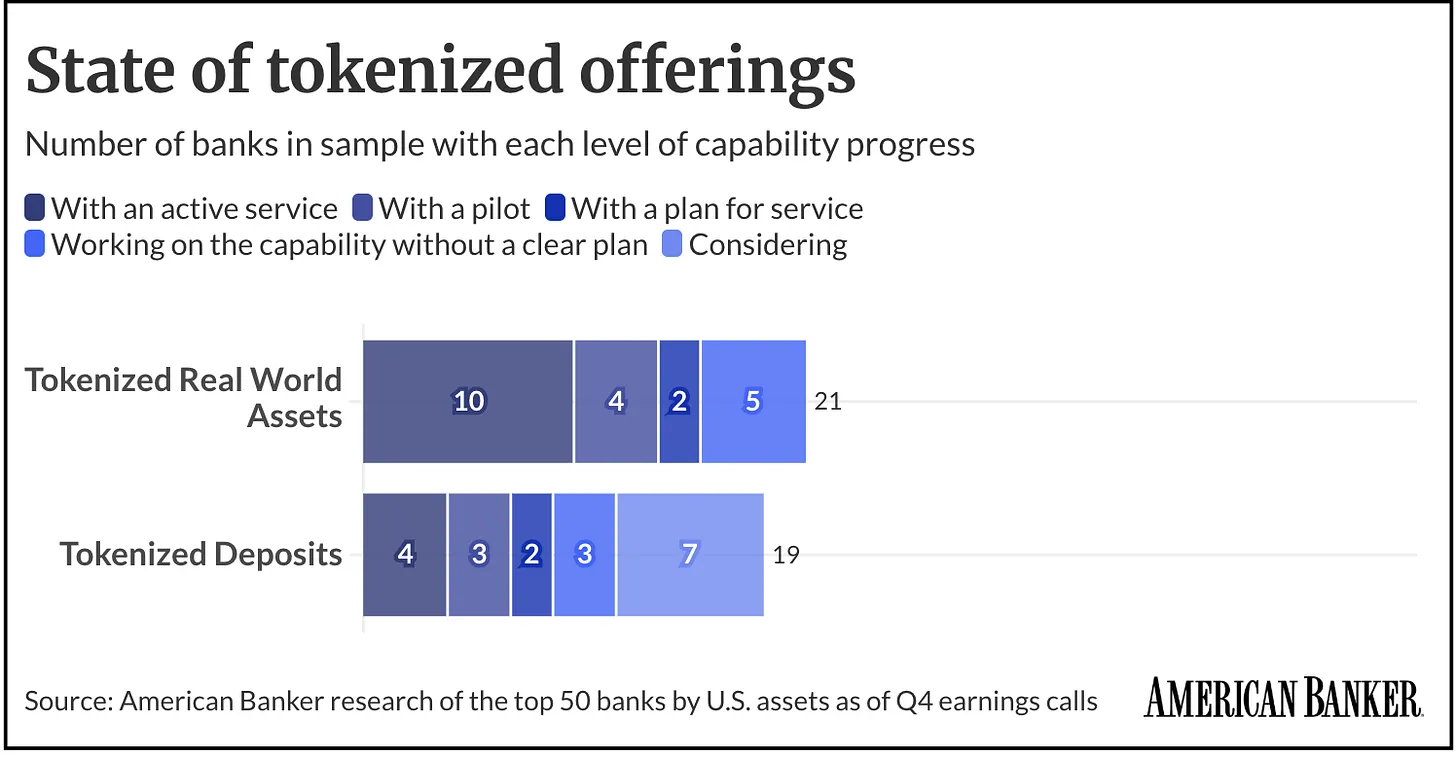

Currently, two major banking consortia have formed in the market to jointly promote the implementation of tokenized deposits.

The first is The Clearing House network, where over ten institutions including JPMorgan Chase, Citibank, Bank of America, and Wells Fargo are collectively building a unified tokenized deposit platform, scheduled for official launch in the first half of 2027. This platform primarily targets institutional clients, offering 24/7 settlement, programmable fund clearing, and cross-border payment functions, directly competing with stablecoins.

The second is Cari Network, composed of five regional banks including Huntington, M&T, KeyCorp, First Horizon, and Old National, with combined assets under management of approximately $780 billion. This network leverages the Prividium technology stack of the zero-knowledge proof public chain ZKsync to build a tokenized deposit platform for retail users, expected to launch in Q4 2026. That regional banks are taking the lead also highlights the severity of deposit outflow risks triggered by stablecoins, as the survival of these banks highly depends on net interest margin income.

So, which product will depositors ultimately favor?

Historical experience shows that when choosing products, depositors often do not simply judge the product's merits in isolation. Instead, they prioritize the option that most easily alleviates their current pain points regarding fund usage.

In the late 1970s, depositors' core demand was to increase returns. Constrained by Regulation Q, bank deposits, while safe, lost their competitive edge when market interest rates rose. Merrill Lynch's innovation was to deconstruct the bank account into two core needs: market-level yields and daily liquidity. Once regulations lifted interest rate restrictions, major banks also推出货币市场存款账户, integrating similar functions.

Today, stablecoins possess advantages similar to Merrill Lynch's product back then: they operate independently of the traditional deposit system, support global circulation, can connect to various crypto platforms, and enable programmable use of idle funds. However, they also share the same shortcomings as the money market funds of that era: they are not insured bank liabilities. Asset safety depends entirely on the issuer, reserve asset structure, redemption channels, and the overall regulatory environment.

Tokenized deposits, on the other hand, replicate the advantages of traditional banks from the 1980s: funds remain within the regulated banking system, preserving banks' lending profit model while continuing the familiar deposit insurance mechanism. But precisely because they follow the banking system's regulatory rules, tokenized deposits lack the openness, circulation capability, and composability of stablecoins. Bank deposits can be sped up and made programmable, but if they were to fully possess the open attributes of stablecoins, banks would lose their core control over deposits.

Thus, the core of the competition between the two sides is gradually evolving into a battle over control of fund convertibility.

Against this backdrop, a third development path has emerged, offering a glimpse into the future form of banking and currency.

The Bridge of Convergence

On May 27 of this year, SoFi Bank officially launched SoFiUSD, the first stablecoin issued by a U.S. national bank. The token is already live on the Ethereum and Solana public chains, and the platform's 15 million users can exchange and use it via the mobile app. SoFiUSD possesses all the characteristics of a stablecoin: 24/7 circulation, cross-border transfers settled in seconds, with transfer fees of just a few cents per transaction.

Simultaneously, users can convert SoFiUSD into tokenized deposits within the same app. These deposits can generate interest and are covered by FDIC insurance. Users gain the flexibility to switch forms: using the stablecoin when they want convenient fund circulation, and switching to tokenized deposits when they seek interest earnings and security guarantees. If dissatisfied with the bank's offered yield, they can switch back to the stablecoin and deposit it into various lending protocols to pursue higher returns.

SoFi may never become more decentralized than Circle, nor grow larger in scale than JPMorgan Chase, but it has created a unique advantage: integrating bank accounts, stablecoin wallets, and tokenized deposits all within a single application interface.

This model is closer to Merrill Lynch's innovative approach back then, distinct from pure stablecoin issuers or traditional banking consortia. SoFi attempts to eliminate the user's dilemma of choosing between the convenience of blockchain technology and the earning power of bank deposits.

The evolution trajectories of various products confirm one truth: in the context of fund storage and circulation, the form of the product itself is not the key; the ability to freely convert between forms is the core.

Faced with the impact of stablecoins, the banking industry's initial response was to lobby regulators to prohibit stablecoins from distributing yields and rewards. However, relying solely on regulatory pressure is unlikely to win this competition. The only way for banks to break through is to proactively evolve, matching or even surpassing the capabilities of crypto products: adding interest earnings and deposit insurance on top of having second-level transfers and programmable features. Interestingly, the vehicle enabling this upgrade is precisely blockchain technology.

This is the charm of the market: it forces traditional industries to continuously evolve until the entire ecosystem maximizes service for participants. Back then, Merrill Lynch's Cash Management Account forced the U.S. to repeal Regulation Q and prompted banks to introduce money market deposit accounts. Today, the rise of stablecoins is pushing banks to develop tokenized deposits and build 24/7 settlement systems. In both transformations, traditional industries were not completely eliminated. Instead, they absorbed the advantages of innovative products and completed self-iteration to maintain their position.

This round of transformation impacts regional banks most severely. These banks rely more heavily on net interest margins and have far less room to withstand deposit outflows compared to large banks. If they only optimize traditional bank accounts, they lose users seeking high fund liquidity. If they blindly match the transfer speed of crypto products, they sacrifice their core advantages of deposit insurance and lending profitability. The Cari Network is a self-rescue attempt by regional banks; The Clearing House consortium represents the defensive strategy of large banks; while SoFi has chosen a more radical path: actively building a bridge of converged services to avoid being preempted by external players.

Reviewing past financial development patterns, emerging formats often break through by exploiting inefficient aspects of the traditional system. Once these pain points become impossible to ignore, traditional giants absorb new functionalities to complete upgrades and stabilize their market position. Back then, Merrill Lynch pointed out the disconnect between deposit rate caps and market yields; banks later filled the gap with money market deposit accounts. Today, stablecoins have exposed the drawbacks of traditional banks operating only on weekdays with restricted fund circulation; banks are now using tokenized deposits and 24/7 settlement functions to fill the gap.

The ownership of industry advantages has also gradually shifted from the innovative products that initially identified the problems to the institutions capable of integrating functionalities, operating compliantly, and scaling the implementation of solutions.

We have recently been discussing a viewpoint: the crypto industry, or more precisely, blockchain technology, is becoming the underlying infrastructure for fintech.

This judgment holds true in this transformation as well. Blockchain is not intended to completely replace bank deposits but to force the industry to deconstruct the value dimensions of various services: yield is one layer of value, settlement efficiency is another, deposit insurance is another, and the ability to freely convert between forms might be the highest-value layer among them.

Regardless of the industry's direction, bank deposits will not disappear entirely; they will only be deconstructed and reconstituted. The ultimate winners will inevitably be the institutions that enable frictionless switching for funds between security, yield, and high liquidity.