Original | Odaily Planet Daily (@OdailyChina)

Author | Asher (@Asher_0210)

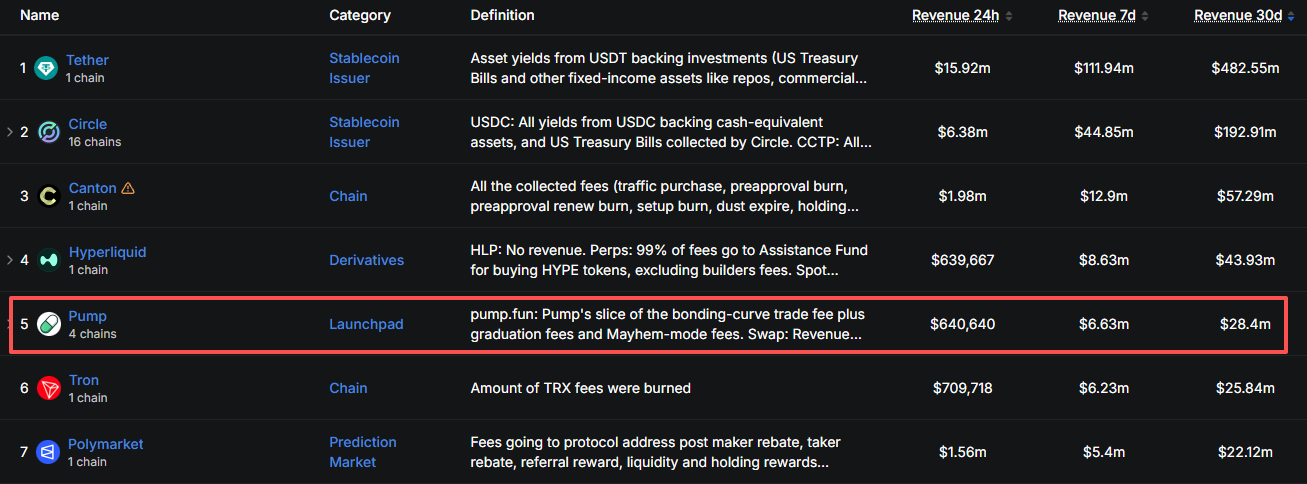

Even though the Meme market has cooled down significantly from its peak, Pump.fun remains one of the most profitable protocols in Web3. According to DefiLlama data, over the past 30 days, Pump.fun protocol revenue reached $28.4 million, higher than Polymarket ($22.12 million monthly revenue), and only lower than Hyperliquid ($43.93 million monthly revenue).

Web3 Protocol Monthly Revenue Rankings

Someone issues a token, it takes a cut; someone trades, it takes a cut; a Meme coin from birth to death, it can extract fees from every buy and sell. Since its launch over two years ago, Pump.fun has issued over 12 million tokens, with cumulative platform revenue reaching approximately $1.05 billion, once becoming the first application on Solana to surpass $1 billion in revenue.

Pump.fun uses a portion of its revenue to repurchase and burn PUMP, converting the money the platform earns into buy-side pressure for the token. But at 10 PM last night, this value cycle faced its biggest test yet. PUMP saw its first unlock of team and investor tokens, totaling 82.5 billion tokens, accounting for 8.25% of the total supply, equivalent to 20.23% of the circulating supply before the unlock, valued at approximately $125 million.

In comparison, PUMP's trading volume in the past 24 hours was only $28 million. So, will this potential sell pressure of $125 million cause PUMP's price to plummet? How much can the platform's repurchase buy-side absorb? Is PUMP still worth buying?

Just Burned 129 Billion PUMP in April, Why Can't It Stop the Unlock Pressure?

On April 29 this year, Pump.fun executed a one-time burn of 129 billion PUMP, accounting for 12.9% of the max supply, the largest burn in PUMP's history.

In terms of quantity, the 129 billion burned is even more than the 82.5 billion unlocked this time. However, they cannot directly offset each other. Most of the burned PUMP had already been repurchased by the platform and stored in specific wallets; they were not freely circulating on the market in the first place. The concentrated burn merely removed these tokens permanently and did not create an extra 129 billion token buy-side on that day in April.

This unlock is the complete opposite. Starting last night, 82.5 billion previously non-tradable team and investor holdings gained the possibility to enter the market. April reduced the total theoretical supply, July increased the potentially sellable holdings.

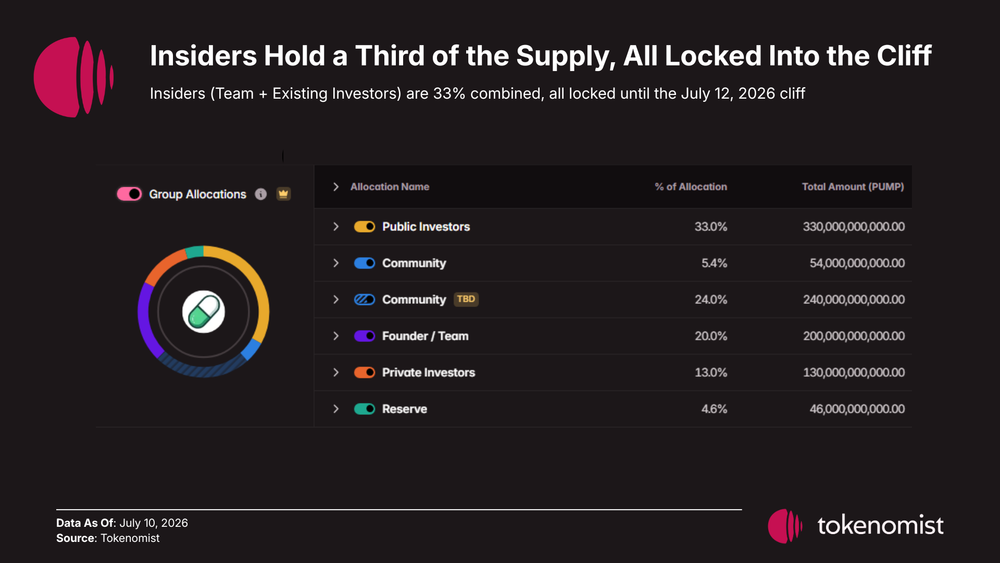

Furthermore, the 82.5 billion is just the first batch. The team and investors collectively hold 330 billion PUMP; this unlock represents only a quarter of that, with 247.5 billion still locked. It's worth noting that there are also 240 billion community tokens without a clear release schedule.

PUMP Token Distribution Chart

The two parts combined total 487.5 billion, equivalent to 1.2 times the circulating supply before the unlock. The market not only needs to digest the immediate 82.5 billion but also faces long-term uncertainty from the subsequent supply.

Unlock Gates Open, While Repurchases Are Ebbing

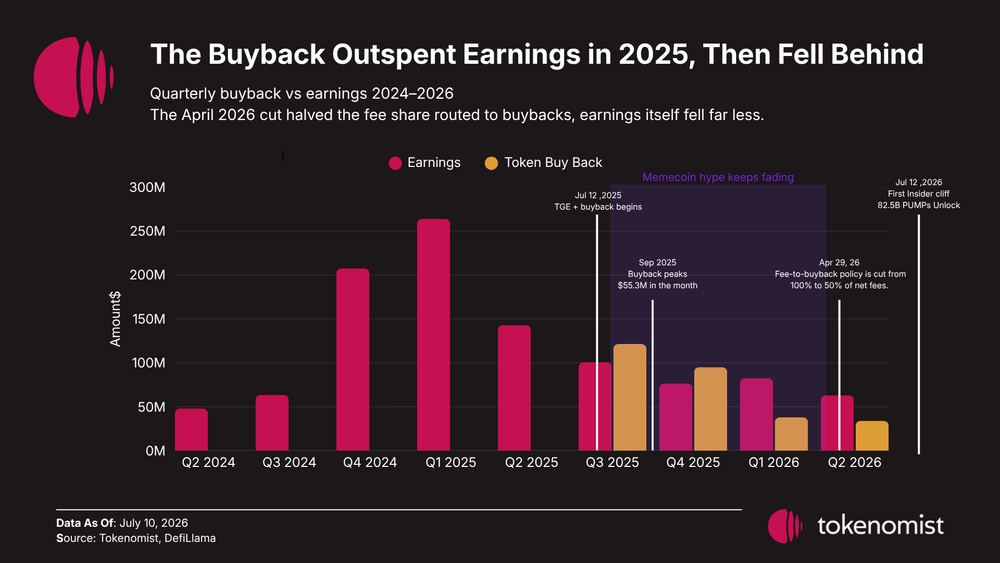

In the past, the most stable buy-side pressure for Pump.fun came from the platform's token repurchases.

After the repurchase program launched in July 2025, Pump.fun once used 100% of net protocol fees to buy PUMP. In September of last year, the monthly repurchase amount surged to $55.3 million, even higher than the $42.8 million protocol revenue for that month.

However, this April, Pump.fun announced it would reduce the repurchase ratio from 100% to 50%, reserving the other half for the company for hiring, marketing, and acquisitions. In June this year, the monthly repurchase amount for PUMP dropped to just $9.2 million, shrinking over 80% from its peak.

PUMP Revenue vs. Token Repurchase Comparison Chart

Looking at a six-month period, the difference is even more pronounced. In the second half of 2025, Pump.fun invested about $217 million in repurchasing PUMP; in the first half of 2026, it invested only $72.2 million, a 67% decrease, while protocol revenue during the same period decreased by only 18%.

Pump.fun is still highly profitable, but the funds actually flowing into PUMP have significantly diminished. Based on June's repurchase scale of $9.2 million, selling just about 7% of this unlocked batch would be enough to offset one month of the platform's repurchases.

Picking the Best of a Bunch, PUMP Remains a Scarce Asset in a Bear Market

Sell pressure is evident, but looking across the entire market, there aren't many platforms that can consistently generate high revenue.

Hyperliquid, with higher revenue than Pump.fun, had protocol revenue of approximately $43.93 million in the past 30 days. However, HYPE's current market cap is nearly $15 billion, over 20 times that of PUMP. Polymarket had revenue of about $22.12 million in the past 30 days and has not yet issued a token. The company's previously rumored financing valuation was already $15 billion. Even if it issues a token in the future, the valuation will likely not be cheap.

In comparison, Pump.fun's revenue over the past 30 days reached $28.4 million, while PUMP's market cap is only about $610 million. It faces unlock pressure, and repurchases are shrinking, but at least the platform's revenue is real, its business model is stable, and the token has already fallen to a relatively low valuation.

More importantly, Pump.fun doesn't rely on any single hit Meme coin. As long as the market continues to issue and trade tokens, the platform can continuously collect fees. Betting on PUMP is essentially not betting on the next big Meme, but betting that whether in a bear or bull market, the Meme market will continue to repeatedly generate hype, and that Pump.fun can continue to guard this traffic gateway.

Choosing assets for accumulation in a bear market is not about finding projects with no issues; it's about prioritizing protocols that still have users, are still profitable, and still have the ability to repurchase from a pile of risks. From this perspective, PUMP is not perfect, but it remains one of the few high-revenue platform tokens whose valuation hasn't yet been pushed to astronomical levels.

The 82.5 billion token unlock tests short-term absorption capacity, but Pump.fun's revenue determines how far PUMP can go. As long as this Meme machine continues to make money, PUMP may not necessarily follow the "unlock means rug pull" script. The current situation might instead be a good time for long-term accumulation.