Editor's Note: Why has this cycle not seen an "altseason"? The author argues that the old market paradigm, driven by high leverage and speculation, has completely ended, replaced by a new regime dominated by compliance thresholds and institutional capital. In this new landscape, the investment logic will shift from capturing liquidity spillovers to selecting long-term value assets with genuine utility and regulatory adaptability.

Original content below:

The widespread underperformance of altcoins since 2022 reflects a shift in the underlying structure, not a typical market cycle.

The liquidity architecture that once broadly transmitted capital to all ends of the risk curve has collapsed and has never been rebuilt.

In its place is a new market landscape that has changed how opportunities are generated and captured.

The collapse of Luna in 2022 dismantled the liquidity architecture that once transmitted capital down the cryptocurrency risk curve. The market didn't suddenly break on that October 10th; it fractured years prior, and everything since has been an aftershock.

The post-Luna era encountered the most favorable macro, regulatory, and fundamental backdrop in crypto history. Traditional risk assets and gold surged significantly, but the long tail of the crypto market did not. The reason is structural: the liquidity system that once drove broad asset rotation no longer exists.

This isn't the loss of a healthy growth engine. It's the collapse of a market structure fundamentally mismatched with durable value creation.

2017-2019:

2020-2022:

May 2022 - Present:

(Note: "OTHERS" = Total crypto market cap excluding the top 10 tokens)

Despite the Most Favorable Macro Backdrop, Altcoins Stagnate

In the years following Luna's collapse, particularly 2024-2025, the crypto industry encountered an unprecedented combination of the strongest macro, regulatory, and fundamental tailwinds. Under the pre-Luna market structure, these forces would have reliably triggered a deep rotation down the risk curve. Yet, to the confusion of crypto investors, this did not happen over the past two years.

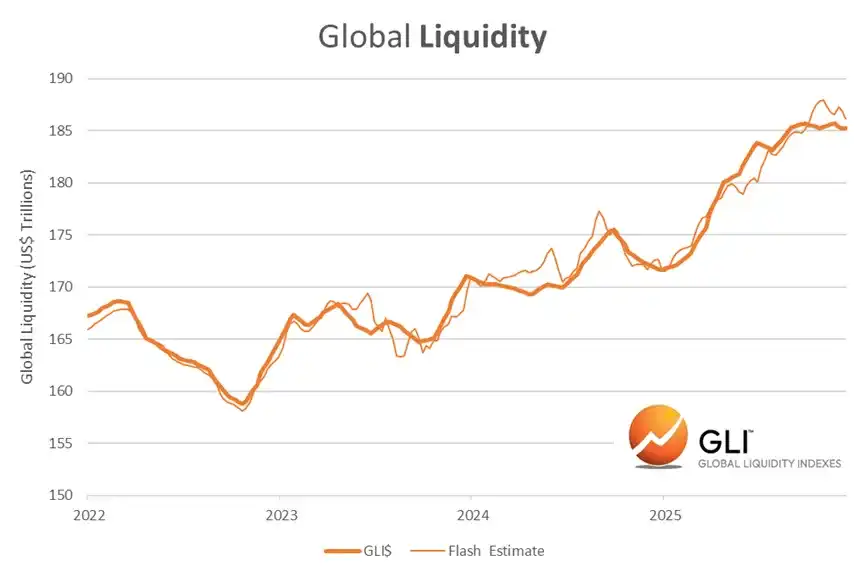

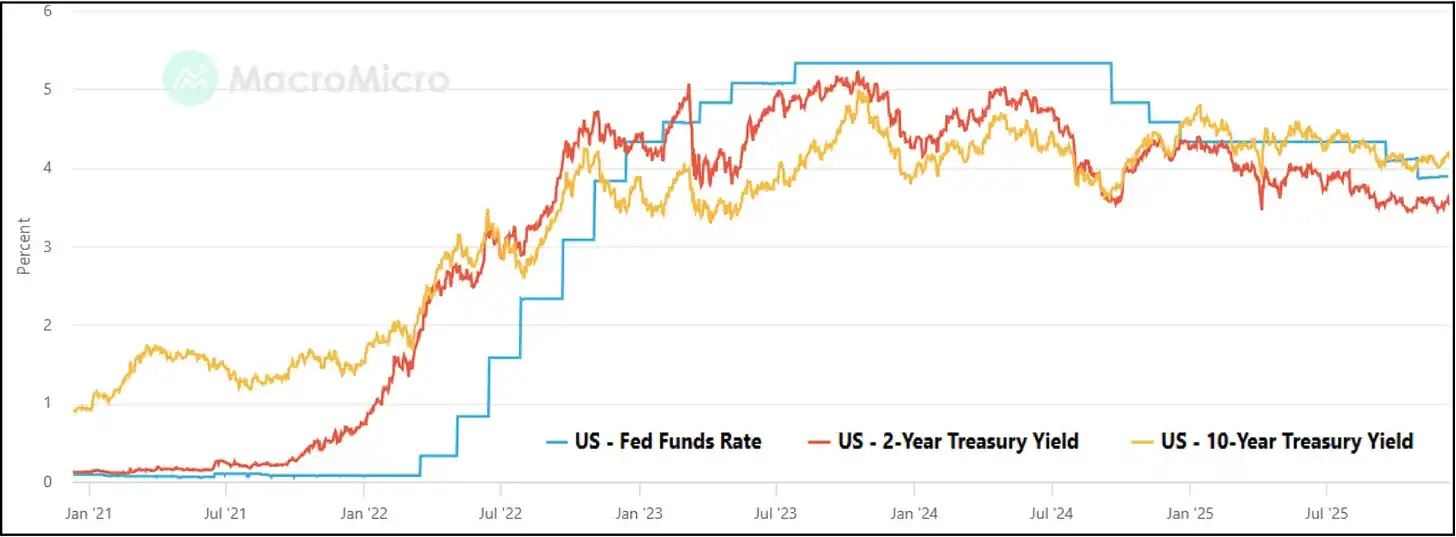

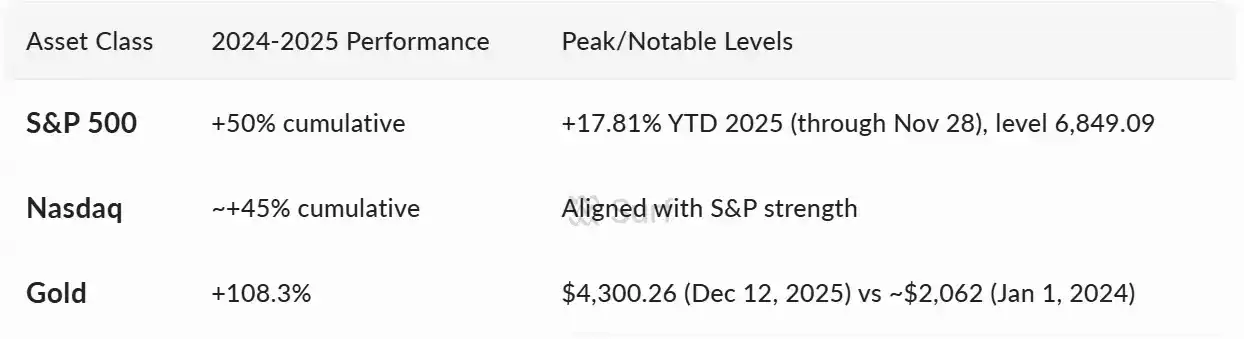

Ideal Liquidity Conditions

Global liquidity expansion, falling real rates, central banks shifting to risk-on mode, traditional risk assets hitting new all-time highs.

Strong Regulatory Momentum

· Accelerated regulatory clarity, long a barrier for large allocators:

· The US welcomed its first pro-crypto administration.

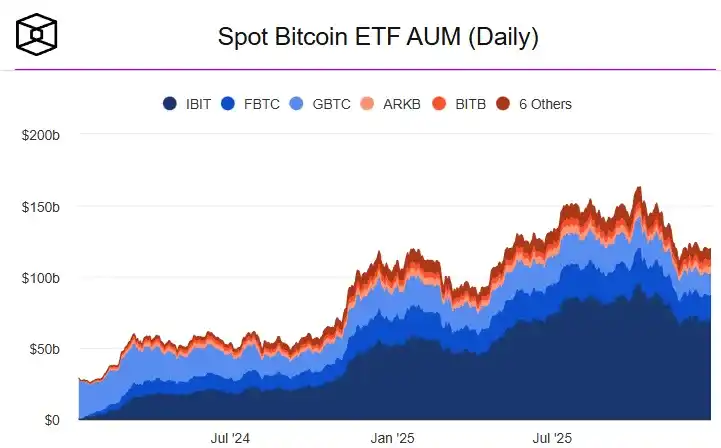

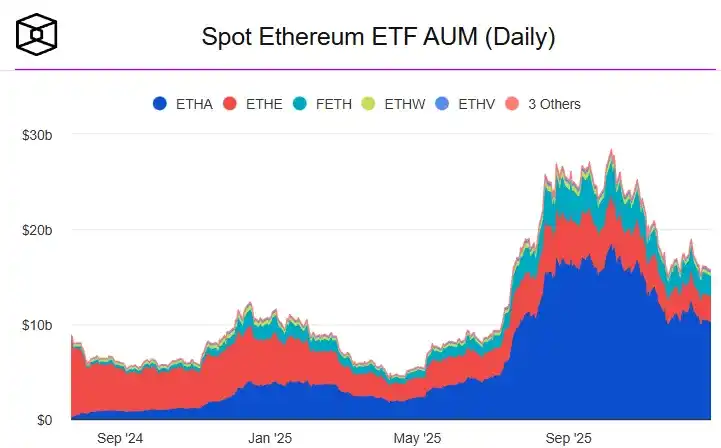

· Bitcoin and Ethereum spot ETFs launched.

· ETP framework standardized (arguably paving the way for the DAT boom mentioned later).

· MiCA established a clear, unified treatment.

· US passed a stablecoin bill (GENIUS Act).

· Clarity Act failed passage by a single vote.

On-Chain Fundamentals Hit All-Time Highs

Activity, demand, and economic relevance all surged significantly:

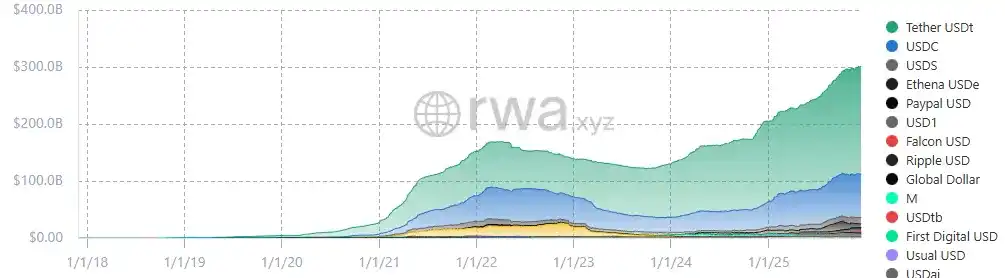

· Stablecoin market cap surpassed $300 billion.

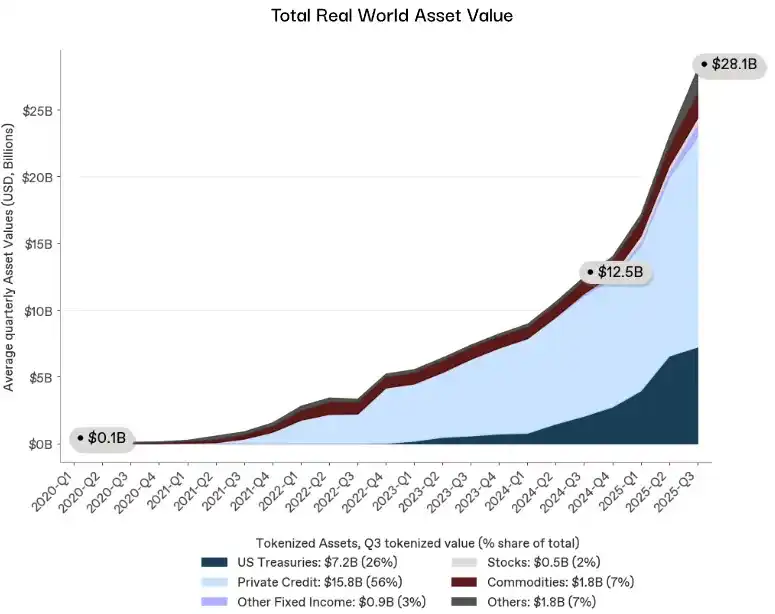

· RWA (Real World Assets) surpassed $28 billion.

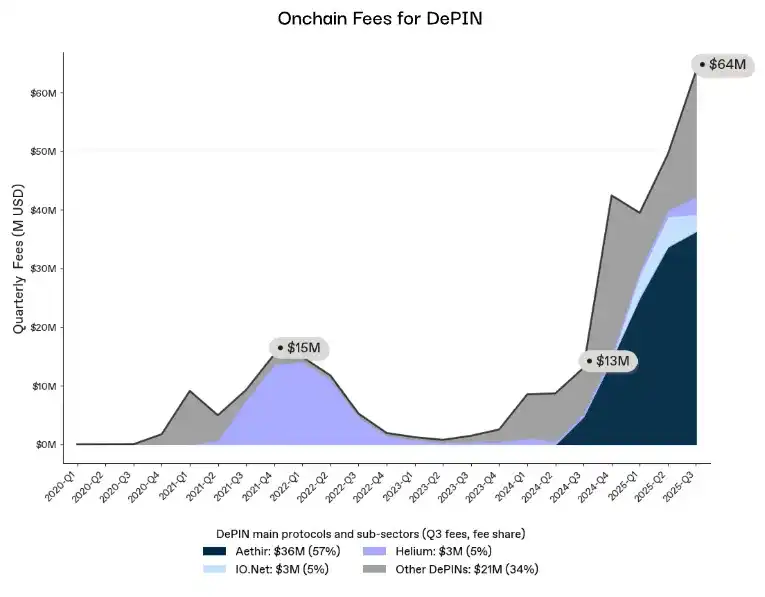

· DePIN revenues rebounded.

· On-chain fees approaching new highs.

This is Clearly a Structural Problem

This is not a failure of demand, narrative, regulation, or macro conditions. It is the consequence of a broken liquidity transmission system. The market structure that dominated 2017-2021 is gone, and no amount of macro, regulatory, or fundamental force can resurrect it.

This does not mean an absence of opportunity, but a shift in how opportunity is generated and captured; a shift that will prove decisively bullish over time.

The previous market did produce larger nominal "pumps," but it was structurally unsound. It rewarded reflexivity over fundamentals, leverage over utility, and fostered manipulation, insider advantage, and extractive behavior incompatible with institutional capital or mainstream adoption.

What Exactly Broke?

Market liquidity consists of three layers: capital suppliers, distribution channels, and leverage amplifiers. Luna's collapse dealt a crushing blow to all three.

Liquidity Engine Shut Down

From 2017 to 2021, altseasons were driven by a concentrated group of balance sheet providers willing to deploy capital across thousands of illiquid assets:

· Market makers operating across venues.

· Offshore lenders providing uncollateralized credit.

· Exchanges subsidizing long-tail markets.

· Prop trading firms warehousing risk.

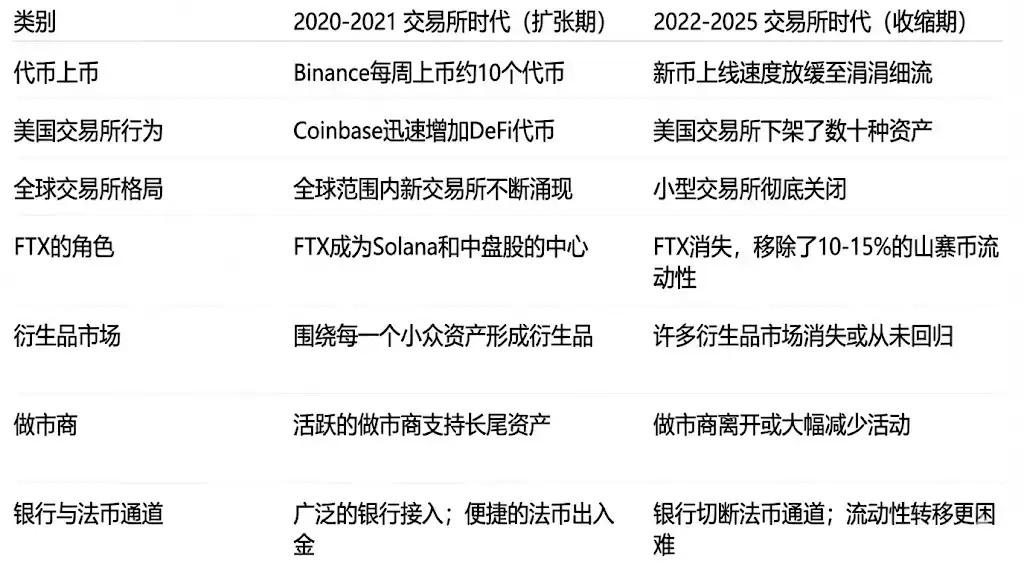

Then Luna collapsed. Three Arrows Capital (3AC) failed. Alameda's risk exposure was revealed. Genesis, BlockFi, Celsius, and Voyager imploded one after another. Offshore market makers retreated en masse. The capital suppliers vanished, and no new entrants with comparable balance sheet size, risk appetite, or willingness to介入 long-tail markets emerged.

Distribution Pipelines Broken

More important than capital itself were the mechanisms for distributing it. Pre-2022, liquidity naturally flowed down the risk curve because a handful of intermediaries were constantly moving it:

· Alameda smoothed prices across trading venues.

· Offshore market makers quoted thousands of trading pairs.

· FTX provided highly capital-efficient execution.

· Internal credit lines moved liquidity between assets.

When Luna's contagion spread to 3AC and FTX, this routing layer disappeared. Capital could still enter crypto, but the pipes that once channeled it to the long tail were severed.

Liquidity Amplifiers Deactivated

Finally, liquidity wasn't just supplied and routed; it was amplified. Small inflows could move markets because collateral was aggressively reused:

· Long-tail tokens used as collateral.

· BTC and ETH leveraged into altcoin baskets.

· Recursive on-chain yield loops.

· Re-hypothecation across venues.

Post-Luna, this system rapidly unwound, and regulators froze the remnants:

· SEC enforcement limited institutional exposure.

· SAB-121 barred banks from custody.

· MiCA imposed strict collateral rules.

· Institutional compliance departments restricted activity to BTC and ETH.

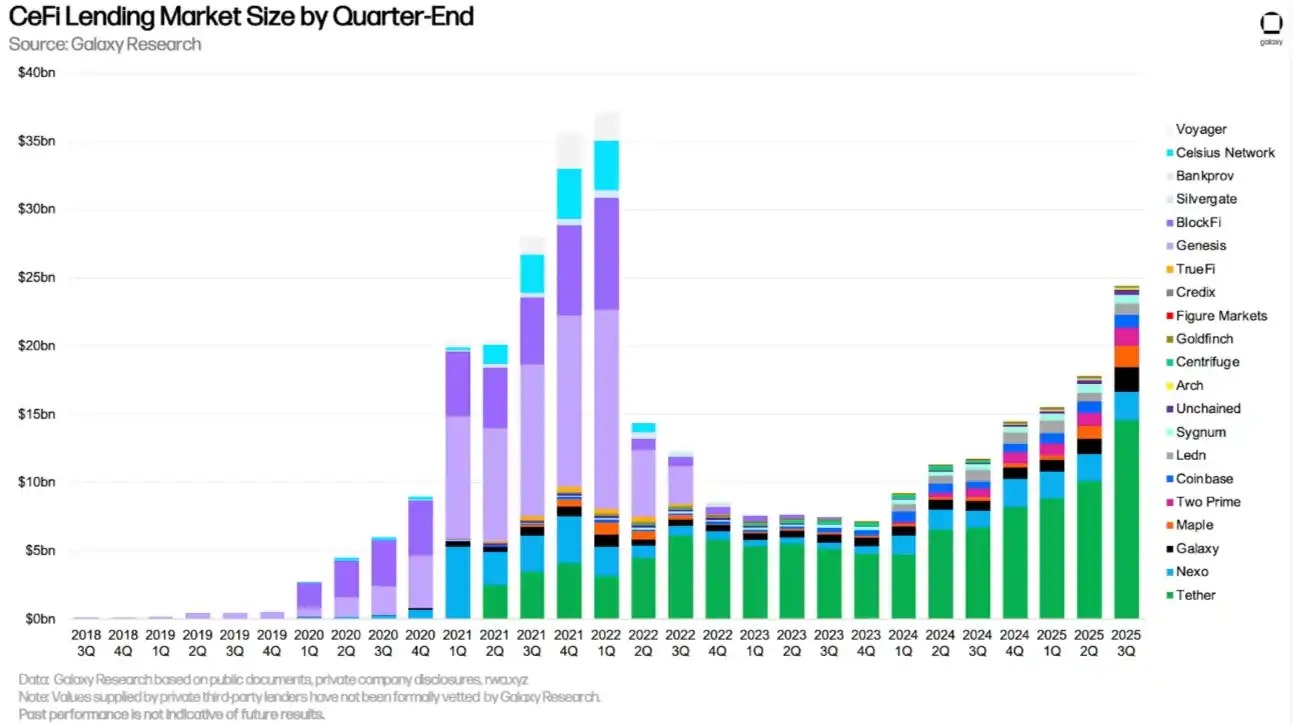

While lending volume at top CeFi (Centralized Finance) has recovered, the underlying market has not. The lenders that defined the previous regime are gone, replaced by a more risk-averse system almost entirely concentrated in top assets. What re-emerged is lending without long-tail credit transmission.

This system only works if leverage grows faster than risk exposure; a dynamic that guaranteed eventual failure.

Structural Altcoin Liquidity Recession

Once the engine shut down, the pipes broke, and the collateral amplifiers turned off, the market entered an unprecedented state: a multi-year structural liquidity recession. A completely different market followed.

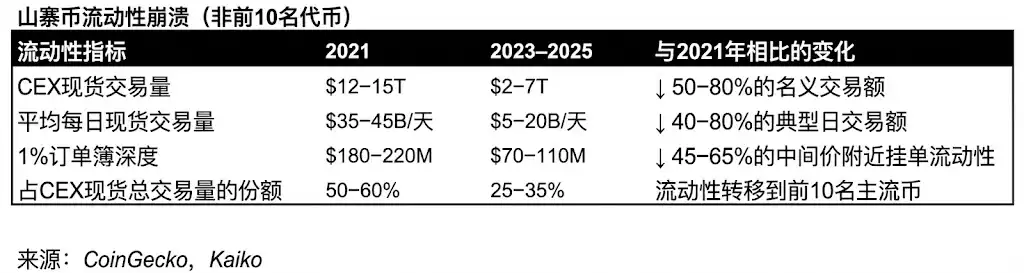

Market Depth Collapsed

Historically, depth always recovered because the same players rebuilt it. Without them, altcoin depth never returned.

· Long-tail asset depth down 50-70%.

· Spreads widened.

· Many order books effectively abandoned.

· Cross-venue price smoothing vanished.

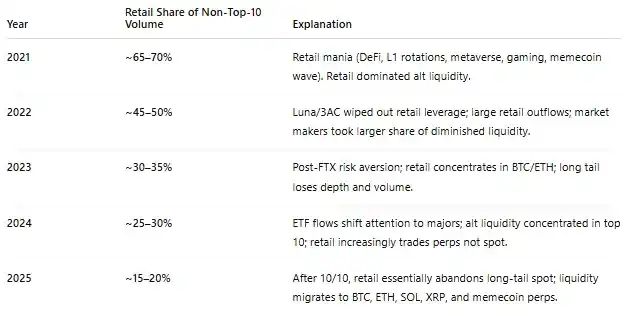

Demand Shifted Upstream

Liquidity migrated upstream and never flowed back down.

· Institutional compliance banned long-tail exposure, sticking to blue chips like BTC and ETH.

· Retail exited.

· ETFs and DATs focused only on blue-chip tokens with sufficient existing liquidity.

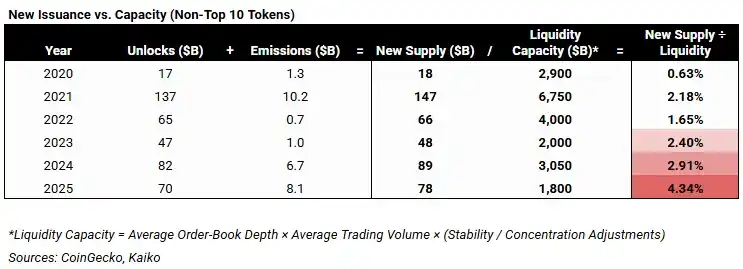

Frenzied Token Issuance Met a Market With No Buyers

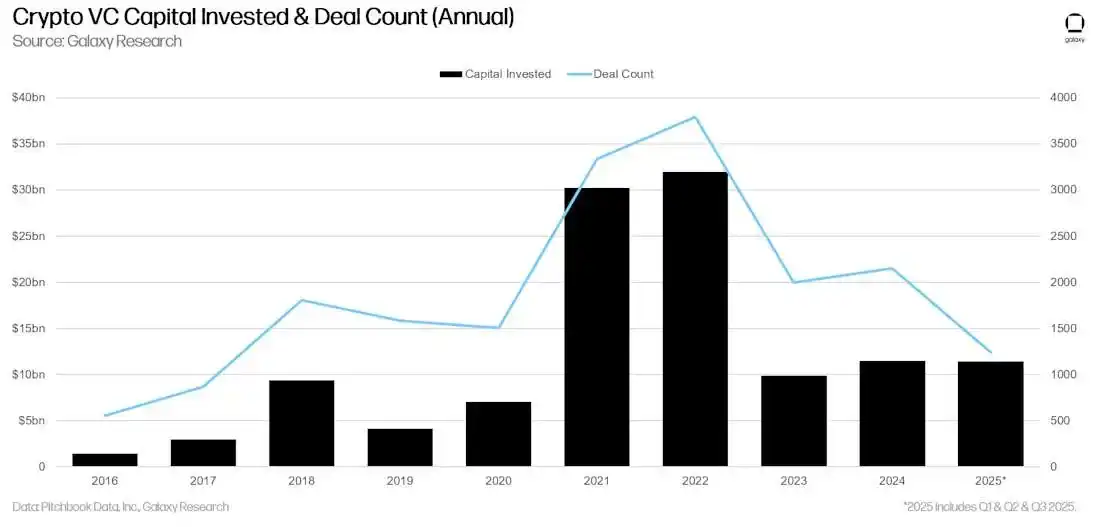

The peak of VC activity in 2021/2022 created a massive wave of future supply.

When these projects issued tokens in 2024-2025, they hit a market missing all absorption mechanisms. The damaged system couldn't handle the constant sell pressure.

(Token unlocks are expected to normalize in 2026 as the 2021-2022 VC issuance cycle clears, easing a key structural headwind for long-tail liquidity)

The conditions that once propelled altseasons have been systematically dismantled. So where does that leave us today?

Investing in the New Landscape

The post-2022 period has been painful for altcoins, but it represents a decisive break from a market structure fundamentally unsuited for scale. What followed wasn't a normal market pullback, but a regime defined by the absence of reflexivity and leverage-driven liquidity. This absence still defines the market today.

In the current structure, even assets with strong fundamentals trade under persistently illiquid conditions. Price action is dominated by thin order books, limited credit, and broken routing, not fundamental performance. Many assets will stagnate for extended periods. Some will fail to survive. This is the inevitable cost of operating without artificial liquidity or balance sheet amplification.

This won't change substantively until regulation changes.

The impending passage of the Clarity Act is a key inflection point for altcoin market structure. It unlocks access to vast capital pools: regulated asset managers, banks, and wealth platforms managing tens of trillions, whose mandates prohibit holding exposure without clear legal classification, custody rules, and compliance certainty.

Until this capital can participate, the altcoin market will remain trapped in an illiquid regime. Once it can, the market structure will彻底改变.

Major financial institutions are already positioning for this shift:

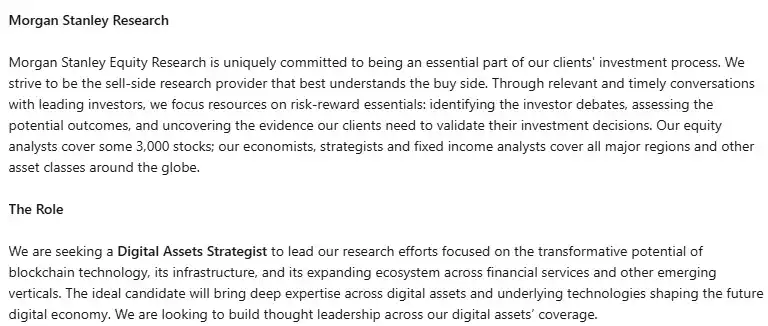

· BlackRock is building out a dedicated digital assets research function, covering tokens like stocks.

· So is Morgan Stanley.

· So is Bloomberg.

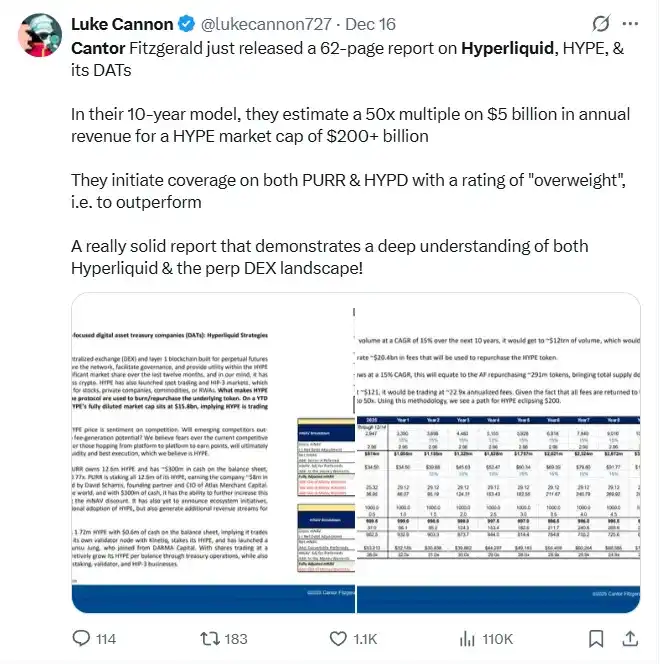

· Cantor Fitzgerald has begun publishing equity-research-style reports on individual tokens.

This institutional build-out marks the beginning of a全新的 market regime. The capital unlocked by regulatory clarity will not flow in through offshore leverage, reflexive rotation, or retail momentum. It will enter slowly, selectively, through familiar institutional channels. Allocation decisions will be driven by eligibility, durability, and scale potential—not narrative velocity or leverage amplification.

The implications are clear: the old altcoin playbook is obsolete. Opportunity will no longer come from regime-wide liquidity waves. It will come from specific assets that can endure prolonged illiquidity on fundamentals and justify institutional allocation once compliant capital is permitted to participate.

These filters were optional in the past. In the new regime, they are mandatory.

· Durable Demand: Does the asset capture recurring, non-discretionary demand, or is activity only present when incentives, narratives, or speculation are?

· Institutional Eligibility: Can regulated capital own, trade, and underwrite the asset without legal or custody risk? Assets outside the scope of institutional mandates will remain liquidity-constrained regardless of technical merit.

· Rigorous Economic Model: Supply, emissions, and unlocks must be predictable and constrained. Value capture must be clear. Reflexive inflation is no longer tolerated.

· Proven Utility: Is the product used because it provides differentiated and valuable functionality, or does it survive on subsidies while awaiting relevance?

Beyond stablecoins and tokenized assets (which continue to capture focus), blockchain-based systems are also being integrated into healthcare, digital marketing, and consumer AI, operating quietly beneath the surface.

These applications are rarely reflected in token prices and remain largely overlooked, not just by mainstream society but even by many Web3 practitioners themselves. They are not designed to be flashy or viral; their appeal is subtle, embedded, and easy to miss.

Yet, the shift from speculation to reality has begun: infrastructure is live, applications are real, and novel differentiation is validated. As market participants increasingly turn to institutional allocators and regulated capital, the gap between quiet adoption and valuation will become increasingly difficult to ignore.

Eventually, this gap will close.

Stepping Back, We Did It

I first fell down the crypto rabbit hole in 2014, and it was immediately clear that blockchain was more than digital currency; it was disruptive technology for data networks.

A decade later, ideas that once felt abstract are operating in the real world.

Software can finally be both secure and useful: your data under your control, kept private and protected, while still being usable to deliver genuinely better experiences.

This is no longer experimental. It's becoming part of everyday infrastructure.

We succeeded: not in achieving a "crypto supercycle," but in achieving the actual goal.

Now comes the execution phase.

Perguntas relacionadas

QAccording to the article, what is the fundamental reason for the underperformance of altcoins since 2022?![]()

AThe fundamental reason is a structural shift in the market's underlying architecture, not a typical market cycle. The old system, which relied on high leverage, reflexivity, and a specific liquidity transmission mechanism, has collapsed and was never rebuilt.

QWhat three components of market liquidity were destroyed by the Luna crash, as outlined in the article?![]()

AThe three components were: 1) The capital providers (e.g., market makers, offshore lenders), 2) The distribution channels (e.g., routing layers that moved liquidity down the risk curve), and 3) The leverage amplifiers (e.g., systems for rehypothecating collateral).

QWhat does the article identify as the key regulatory turning point that could unlock institutional capital for the altcoin market?![]()

AThe key regulatory turning point is the passing of the Clarity Act, which would provide the legal classification, custody rules, and compliance certainty needed for regulated asset managers, banks, and wealth platforms to gain exposure.

QIn the new market regime, what four criteria will be mandatory for an asset to attract institutional capital, as opposed to the old 'altcoin playbook'?![]()

AThe four mandatory criteria are: 1) Persistent demand (non-discretionary, recurring usage), 2) Institutional eligibility (can be owned/traded/underwritten by regulated capital), 3) Rigorous economic models (predictable, limited supply), and 4) Proven utility (provides differentiated, valuable functions without subsidies).

QThe article states that the market is shifting from speculation to reality. What examples of real-world, non-speculative applications does it mention?![]()

AThe article mentions that blockchain-based systems are being integrated into real-world sectors such as healthcare, digital marketing, and consumer AI, often operating quietly in the background, in addition to the continued focus on stablecoins and tokenized real-world assets (RWA).