Author|Azuma(@azuma_eth)

The "de-anchoring" of Strategy's preferred stock STRC continues to intensify.

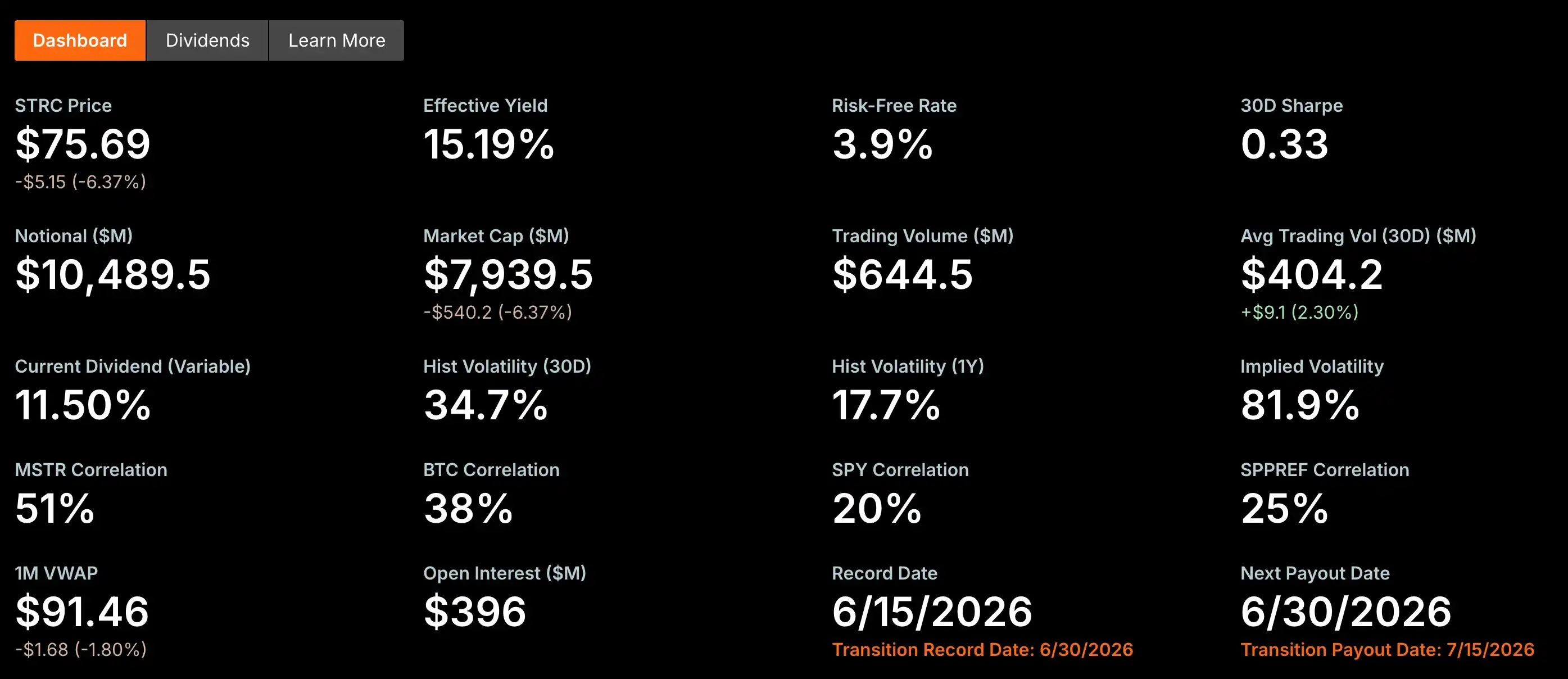

During yesterday's U.S. stock market session, STRC fell below the 80 mark for the first time, touching a low of $73.62 at one point. Although it rebounded slightly by the close, the price remained at only $75.69, nearly 25% "de-anchored" from its target face value of $100.

Last week, we wrote an article titled "STRC De-anchored by 11%, Can Strategy's Perpetual Motion Machine Keep Running?" focusing on the reasons for STRC's de-anchoring and briefly outlining its potential future impacts.

However, judging from community discussions, it seems many readers still do not fully grasp just how dire the consequences of STRC's persistent de-anchoring are, so we decided to write another article to break down this issue.

Strategy's Most Important Fundraising Channel Has Failed

What exactly is STRC? In a nutshell, it is Strategy's cheapest and most efficient fundraising channel.

The essence of Strategy's business model is to continuously raise funds from the market to acquire more BTC, then raise more funds and acquire even more BTC. This is a cycle that must keep turning. Strategy's high valuation is largely based on the market's belief in its ability to persistently raise funds and buy BTC. As long as its fundraising capability remains, it can keep expanding its BTC holdings; and the ever-growing BTC holdings, in turn, further support the market's expectations for its future fundraising ability.

Over the past few years, Strategy has tried almost every fundraising method—issuing common stock, convertible bonds, and various types of preferred stock—and continuously invested the raised funds into BTC. Among all its fundraising tools, STRC was once considered by the market as the one closest to "perfect," and is Michael Saylor's proudest creation. Saylor once boasted, "STRC is a product designed by AI, humans couldn't have designed this."

As a preferred stock, STRC's advantages are very clear. Issuing common stock could dilute existing shareholders' equity; issuing convertible bonds means the company bears future debt repayment pressure; but STRC, as a perpetual preferred stock, has no maturity date, does not dilute common shareholders, and only requires fixed dividend payments. For Strategy and Saylor, this was almost the lowest-cost, highest-efficiency fundraising method.

From its inception, STRC was designed as a product anchored to $100. Strategy envisioned that by dynamically adjusting its dividend yield, STRC would trade long-term around $100 (sound familiar, like algorithmic stablecoins?). As long as the secondary market could maintain this price, the company could continuously issue new STRC at prices close to face value, raise new funds, and continue buying Bitcoin.

In other words, STRC's core value lies in its endless fundraising ability, but this ability is predicated on its price remaining near the target face value. As STRC continues to de-anchor, this fundraising channel is effectively blocked. Because for any investor, if buying the same STRC in the secondary market only costs $75, there is no incentive to participate in the company's new preferred stock issuance at a price close to $100.

For Strategy, the options are either to keep raising the dividend yield to attract funds (which has proven to have limited appeal) or to accept the reduced fundraising efficiency from discounted issuance (which actively breaks the original target face value). Either way, it means this fundraising machine is developing increasingly significant friction.

The Fundraising Tool Has Become a Cash Flow Burden

If it were just a temporary failure of fundraising ability, it might be manageable. The bigger problem is that STRC requires Strategy to make continuous, substantial cash dividend payments.

According to Strategy's latest official disclosure, the current issuance size of STRC is approximately $10.49 billion, with a current dividend yield of 11.5%. This means that for STRC alone, Strategy has an annual cash dividend payment obligation exceeding $1.2 billion. Adding other preferred stocks like STRD, STRK, STRF issued by Strategy, this figure climbs to about $1.7 billion.

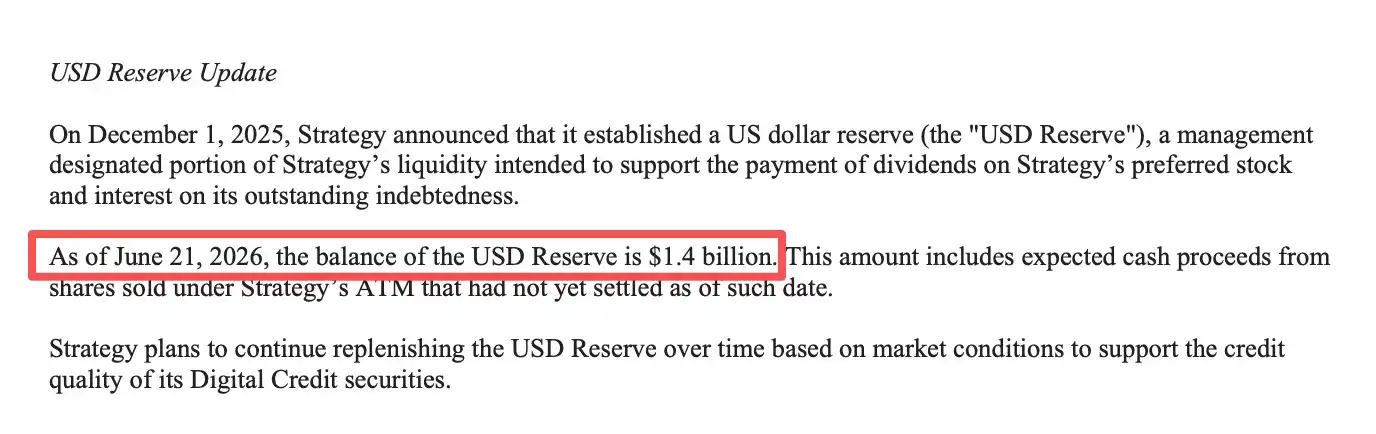

In the common stock issuance filing on June 21st (note: common stock, details below), Strategy disclosed that its cash reserves are approximately $1.4 billion. At this cash reserve level, Strategy's on-book cash can cover less than one year of preferred stock dividend payments.

Resolving the Situation Requires Money, But Where Will It Come From?

Whether to sustain its own business model or to escape its current severe cash flow situation and avoid dividend payment default (the more urgent issue), Strategy needs more money. Theoretically, Strategy now has only three viable paths to "get money."

First, issuing common stock.

This is currently the most direct and mature financing method. Through its ATM (At-the-Market Offering) program, Strategy can continuously sell MSTR common shares to the market to raise funds.

But common stock financing is not without cost. Continuous issuance means the number of outstanding shares keeps increasing. If the growth rate of BTC purchased with newly raised funds cannot outpace the share expansion rate, the BTC per share growth will slow down, and common shareholders will face continuous dilution—note this point, it's important for what follows.

Second, issuing more debt.

Over the past few years, Strategy has repeatedly raised funds through debt instruments like convertible bonds, which were a crucial source of funds for its early large-scale BTC acquisitions.

However, as the scale of preferred stock has continued to expand and fixed cash outflows have persisted, the market has started paying closer attention to Strategy's liquidity and debt repayment capacity. In the current financing environment, if the company issues bonds again, investors are likely to demand higher risk premiums, meaning financing costs will be significantly higher than in the past.

More importantly, bonds differ from preferred or common stock; their interest payments and principal repayments are rigid obligations. Against a backdrop of declining cash reserves and increasing dividend payments, further expanding debt would undoubtedly加重 the company's financial burden and compress its future financing space.

Third, selling BTC.

From a financial perspective, this is the fastest way to replenish cash reserves. Strategy has certainly considered this path. The company stated on its official X account regarding dividend payment pressure: "When considering its massive Bitcoin reserves, they are sufficient to cover 32 years of dividend payments."

But for Strategy, this is also an extremely dangerous choice. Earlier this month, Strategy sold some of its Bitcoin holdings for the first time. Although the sale was only for 32 BTC, and the official presentation framed it as "active market desensitization testing" and mentioned "will buy back more later," it still caused a short-term market dip.

As the largest single holder of Bitcoin in the market, Strategy's actions can easily trigger market chain reactions. If it increases sales volume in the future, it will undoubtedly place huge pressure on the already fragile BTC price. If BTC declines further, Strategy's so-called "reserves" would also quickly shrink.

In summary, in the current situation, every viable fundraising channel for Strategy comes at a higher cost than in the past.

Has Strategy Made Its Choice?

Based on Strategy's latest moves, aside from hinting at possibly selling BTC, the company seems to have already chosen its path.

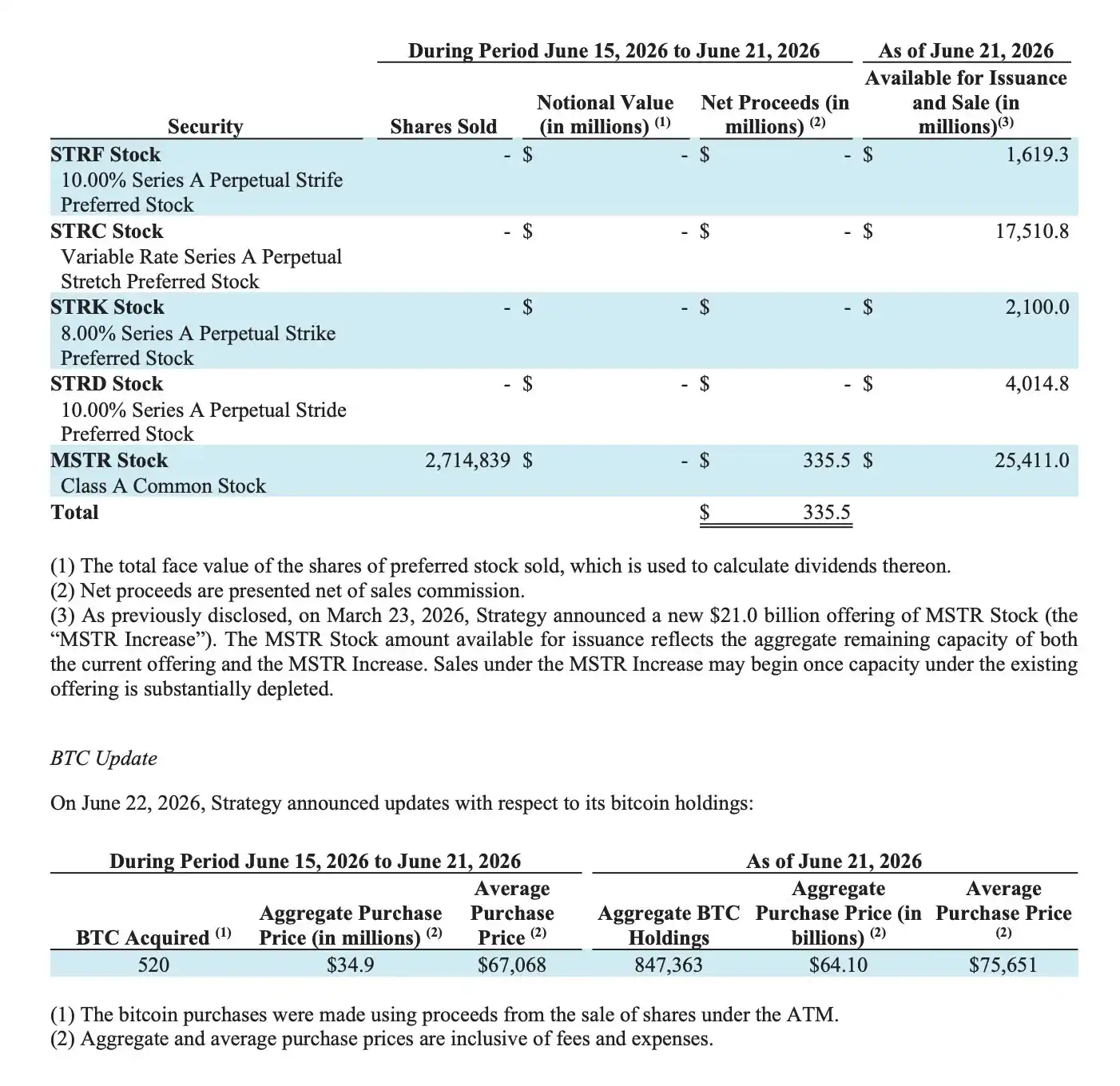

Since June, Strategy has relied on its common stock ATM (At-the-Market Offering) program for fundraising for three consecutive weeks, with the latest round (June 22nd) being particularly typical.

According to Strategy's latest 8-K filing, the company sold a total of 2,714,839 MSTR common shares in one week, raising $335.5 million. However, that same week, Strategy only purchased 520 BTC, spending a total of $34.9 million, with an average purchase price of around $67,068. In other words, of the $335.5 million raised, only about 10% was actually used to continue acquiring BTC. The remaining funds were primarily used to replenish the company's cash flow reserves, increasing cash from about $1.1 billion previously to the current ~$1.4 billion.

This might seem quite effective? But there's another trap here.

For MSTR common shareholders, the most critical information is: for each new common share issued, how much BTC can the raised funds ultimately buy back? Is it enough to cover the BTC equity corresponding to this new share? If the new financing can buy back more BTC than the share originally corresponded to, then common shareholders' equity is actually enhanced. Conversely, if the raised funds buy back insufficient BTC to cover the new share's corresponding BTC equity, then common shareholders suffer dilution.

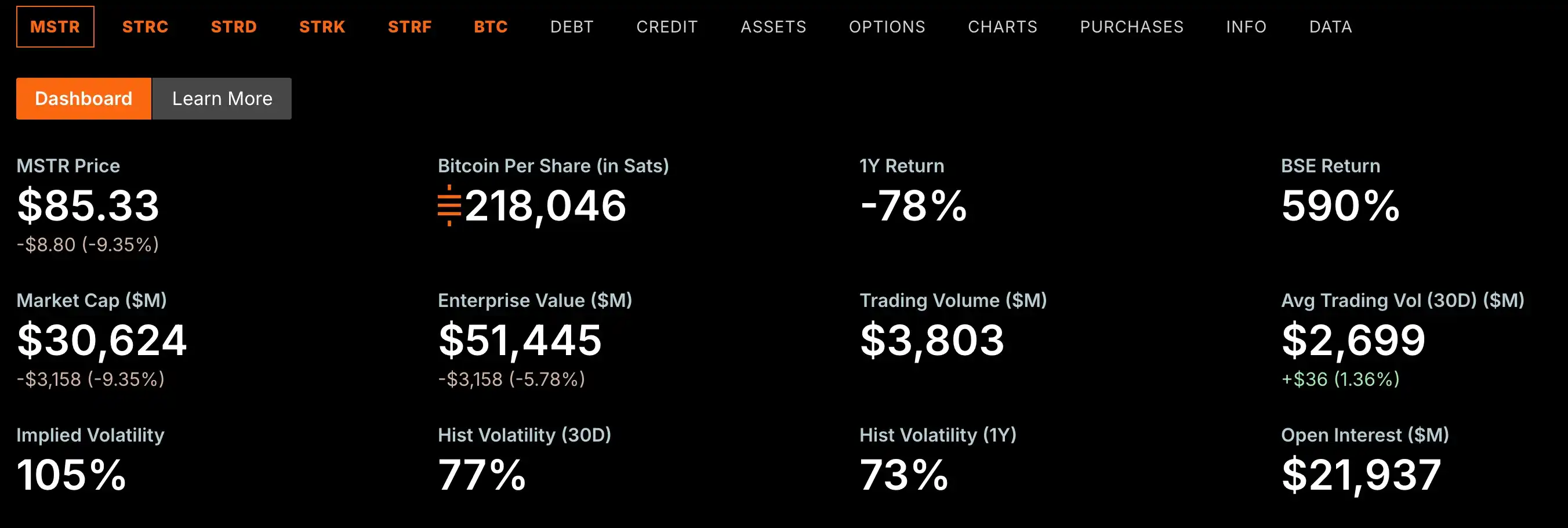

Clearly, Strategy's recent common stock issuance has come at the cost of diluting common shareholder equity. Strategy's official data also shows that MSTR's BTC per share has decreased from a peak of 220,900 Sats to 218,046 Sats.

This is the biggest limitation of common stock financing. For the vast majority of public companies, issuing common stock is just one of many financing methods; but for Strategy, common stock itself is part of its business model.

Over the past few years, Strategy's growth has essentially relied on the continuous operation of the "fundraise ➡️ buy coins ➡️ solidify market expectations ➡️ fundraise again ➡️ buy coins again..." flywheel. The market's core expectation for Strategy lies in its ability to continuously create more BTC equity for common shareholders, not dilute it.

However, when Strategy is forced to rely increasingly on common stock financing to replenish cash reserves rather than continue acquiring BTC, the operating logic of this flywheel changes. While common stock financing can indeed alleviate Strategy's cash pressure in the short term, it is difficult to become a long-term substitute for STRC.

Once common stock financing persistently erodes BTC per share, the foundation upon which MSTR's high premium relies may also be challenged, and this is precisely the core competitive advantage of Strategy's entire business model.

What About BTC?

Over the past few years, Strategy has become the most important marginal buyer in the BTC market (arguably without "one of"). To date, Strategy has accumulated holdings of 847,363 BTC, accounting for about 4% of BTC's current circulating supply, valued at over $50.7 billion. The market has long grown accustomed to Saylor's massive, unwavering weekly purchases.

But now, this situation is changing. Strategy can still raise funds through common stock, but most of the funds are no longer flowing into BTC; they are prioritized for replenishing cash reserves. This means that under the same fundraising scale, the actual new buying power entering the BTC market is diminishing.

More detrimentally, this situation may persist. If STRC fails to re-anchor long-term, and preferred stock financing remains blocked, Strategy will be forced to rely on common stock financing long-term to maintain cash flow, potentially further reducing the proportion of funds used for BTC accumulation. For the BTC market, this means the most stable and certain institutional buying power of the past few years will no longer grow as consistently as before.

But even more concerning is that if excessive common stock issuance overly dilutes MSTR shareholder equity, Strategy may have to consider another financing channel—selling coins.

From weakened new buying power to the emergence of potential selling pressure, today's Strategy is no longer BTC's largest marginal buyer, but a giant sword hanging over BTC.