Author: FIP Crypto

Compiled by: Deep Tide TechFlow

Deep Tide Intro: In the current landscape of airdrop frenzy and rampant points systems, many investors are experiencing "grinding fatigue." This article proposes a counterintuitive airdrop strategy: the best airdrops aren't "grinded" for; they are encountered unexpectedly through genuine on-chain interactions.

By analyzing cases like Monad, ZKsync, and Base, the author reveals the core logic behind retrospective airdrops—project teams value on-chain footprints that generate real value more than mechanical Sybil behavior. If you feel your airdrop returns are being diluted, this article will teach you how to build a genuine on-chain reputation for efficient, low-pressure earning.

Main Text:

Not all airdrops require endless "grinding," and the ones that don't are often the highest quality.

I've tried various types of airdrops, and many left me utterly exhausted.

But I realized the smartest way to get airdrops is actually not to deliberately "farm" them.

Here is the strategy I currently employ, aimed at "accidentally" getting the highest rewards with minimal effort:

We Get Rewarded for Being Active On-Chain

Not every project does this, but some projects distribute airdrops to active on-chain users.

Here are some examples of past retrospective airdrops:

- TIA and DYM: Rewarded stakers in the Cosmos ecosystem and active L2 users.

- AVAIL: Rewarded active L2 users, including Starknet users.

- PENGU: Rewarded wallets with strong activity records on Ethereum and Solana.

- MegaETH: SBT eligibility was based on our on-chain contributions.

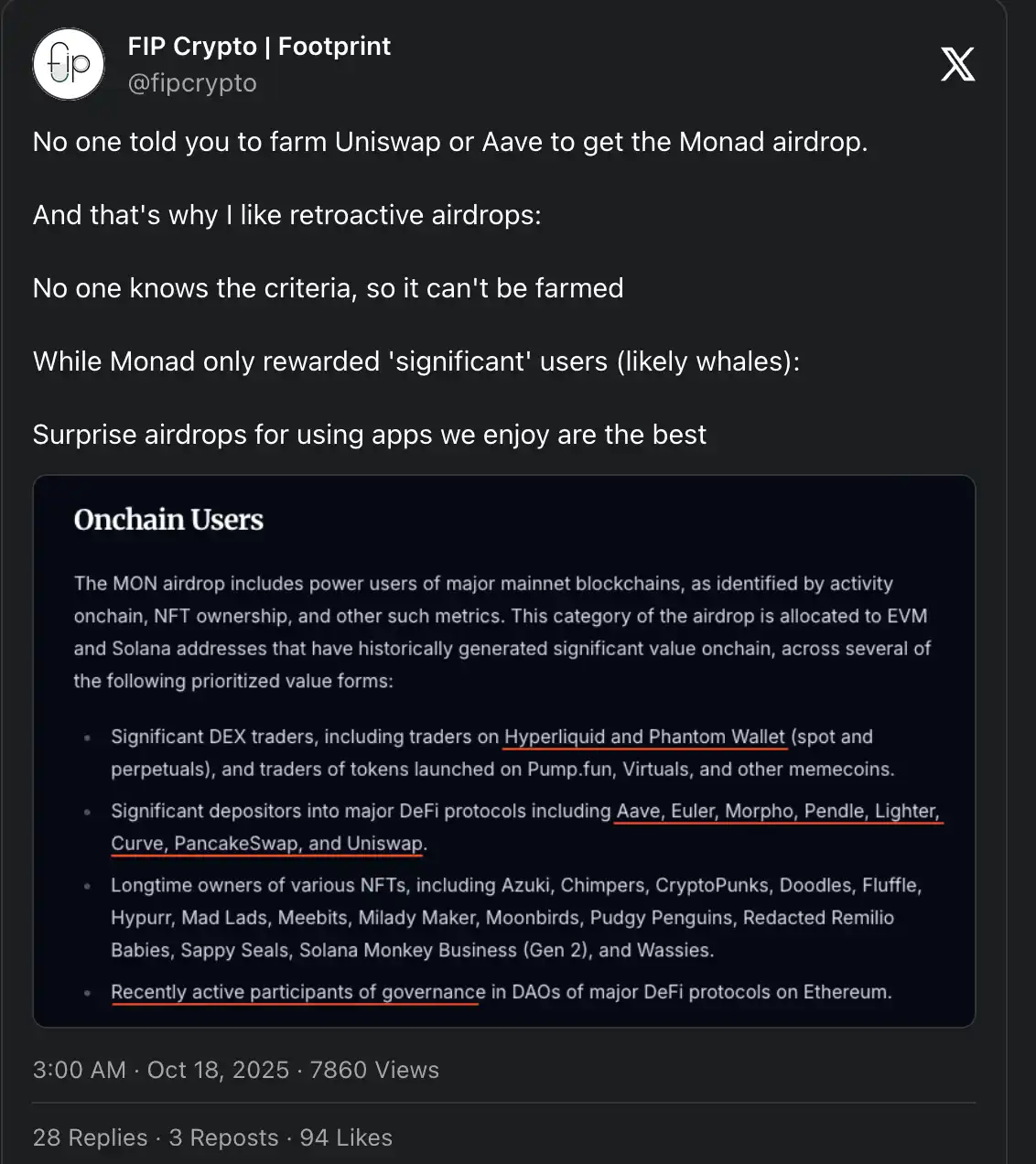

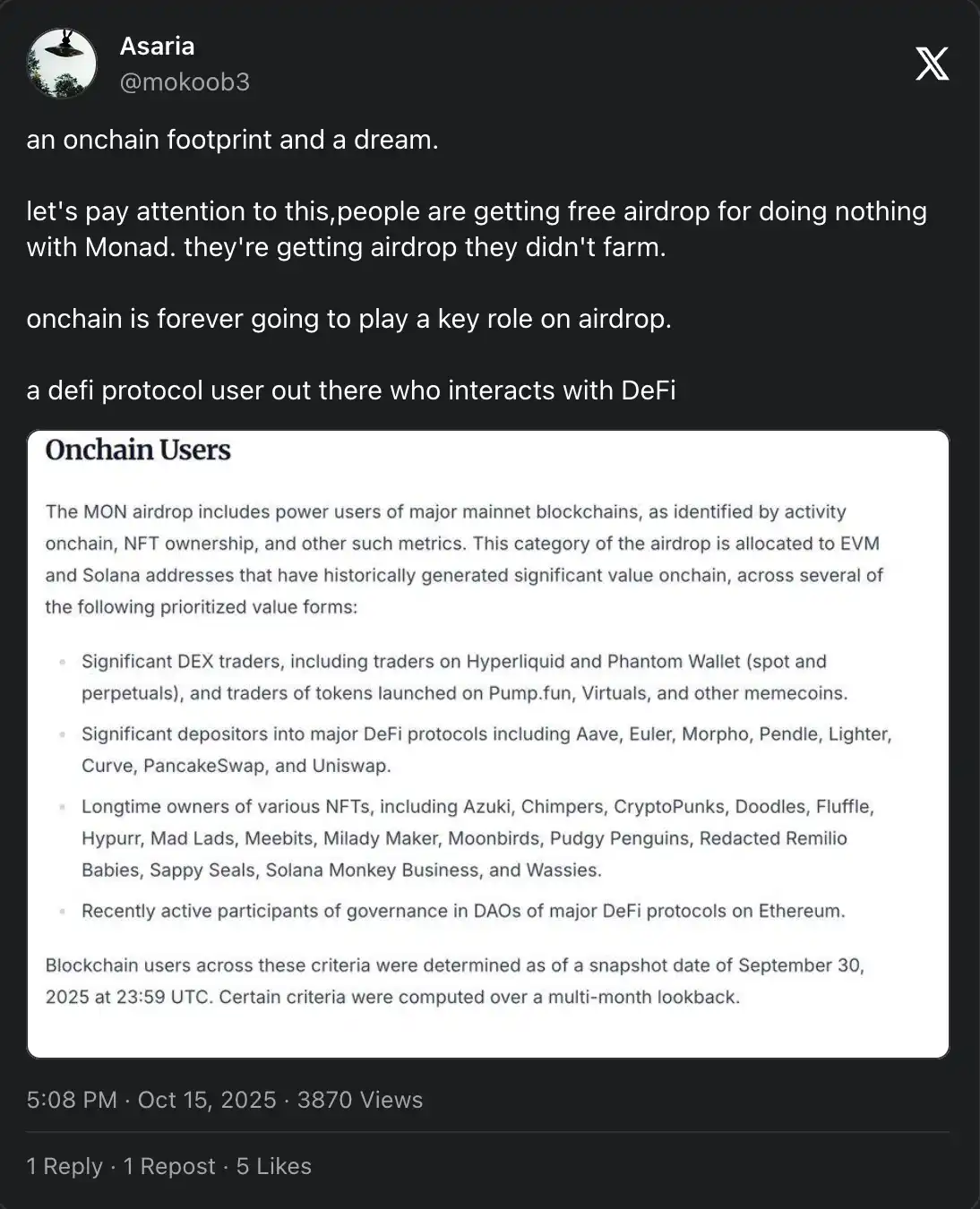

- Monad: Rewarded significant traders and depositors in top Ethereum and Solana protocols (they defined this as users who provided substantial value on-chain).

Following @Zeneca's airdrop philosophy, as long as we keep an open mind and explore new things on-chain, airdrops will come naturally.

Our footprint makes us eligible for various airdrops simply by interacting with protocols we like.

No One Knows the Criteria

Points programs with clear criteria are boring because the project team directly tells you how to grind them.

One of the most "notorious" projects is MarginFi, which ran a points program for months (or even years?) without ever revealing any token details.

But this is the trap of any points program:

No one promises you anything, and the activity can go on forever.

They can change the rules at any time; that's the game we're playing.

If the sole purpose is to hard-grind a project for an airdrop, many people get frustrated.

When our expectations for airdrop returns are too high:

We are setting ourselves up for massive disappointment.

These programs are also heavily manipulated by Sybils, which further dilutes the allocation.

Meanwhile, retrospective airdrops do not publicly share their criteria.

We can compare the criteria used by two different L2s:

- ZKsync used Time-Weighted Average Balance (TWAB), but only announced it after the snapshot.

- Scroll used Marks points across multiple campaigns.

Both used similar factors (liquidity) to determine eligibility.

But Scroll didn't perform well except for favoring whales, while ZKsync was quite lucrative if you had the right strategy.

Many are still angry about missing ZKsync eligibility, but in reality, we could have qualified even with a small amount of capital.

We Have Less Competition

When there's so much uncertainty, no one likes to farm airdrops.

The ideal scenario is like Base or Arbitrum:

Actively denying they will issue a token, until they change their minds and decide to issue one.

Therefore, fewer wallets actively participate because those solely chasing incentives won't join.

Or they might drop out halfway, as it doesn't make sense from a Return on Investment (ROI) perspective to farm this project.

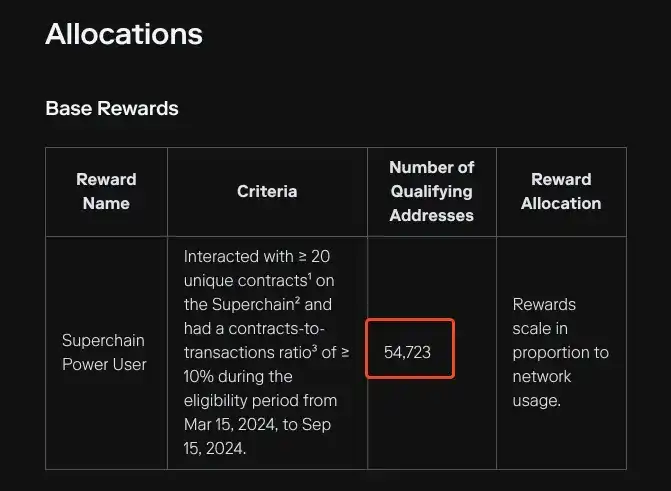

Optimism's 5th airdrop was a huge surprise for me; it turned out only 54,723 wallets were eligible.

Many will adopt a wait-and-see attitude, questioning if it's worth interacting without guarantees.

But the real reward comes from uncertainty:

We risk our time and capital based on our convictions, which could be a failure or a highly rewarding investment.

Even if we fail, it helps us further optimize our strategy and understand what to avoid in the future.

We Don't Get Burned Out

I've been asked countless times which are the best projects to farm.

We are always looking for the next farm, and after the token dump, the next one.

But sometimes, the best way to play airdrops is to use products you enjoy.

Who would have thought that staying active on Aave or Uniswap would make us eligible for a Monad airdrop?

I've been burned out multiple times from constantly searching for the next Alpha.

But if we can get rewarded based on our on-chain footprint:

The real Alpha is interacting with protocols we enjoy using and profiting from in the process.

Focusing too much on the end result leads to disappointment.

Receiving surprise airdrops keeps us motivated to continue exploring on-chain.

Sybil Attacks Can't Game the System

Sybil farms mimic real users by performing the most basic operations to gain eligibility.

There will always be Sybils trying to extract value from projects.

But projects using retrospective criteria can adjust rules to filter out Sybils.

Of course, these are never perfect:

- Real users get falsely filtered out.

- Some Sybils get allocations.

It's hard to balance between the two; someone always gets left out.

On our end, we can try our best not to be filtered out as Sybils.

It all starts with this principle:

Value is the Primary Criterion

Retrospective airdrops are distributed based on the value your wallet provides.

Monad described it as "addresses that have historically generated significant value on-chain across different forms of value."

If we do the same low-value tasks as Sybils:

We get flagged and lose eligibility.

Project teams don't want to reward farmers who repeatedly make the same low-value swaps.

Instead, they reward high-value contributions.

But there are no strict rules for this; project teams decide which behaviors they want to reward.

So, to be eligible, we just need to find applications we like and use them consistently.

Our footprint will be recognized by other projects, and we'll get rewarded for using applications we enjoy.

Building a Strong On-Chain Social Footprint

The on-chain footprint has been declared dead by many, but I still believe it plays a key role in future airdrops.

Even though airdrops now heavily lean towards social distributions:

The on-chain footprint still forms the foundation of trust for your social reputation.

Others can easily tell if you're faking it or genuinely participating, so there's no point in trying to lie.

You just need to talk about what you've done on-chain to increase your "surface area for luck."