Original Title:Prediction Markets: They Grow Up So Fast, Author: Alex Immerman(@aleximm)

Compiled by | Odaily Planet Daily(@OdailyChina); Translator | Asher(@Asher_ 0210)

Editor's Note: At the end of March this year, prediction markets, once considered a niche area, reached a critical moment. Kalshi Research, the research arm of Kalshi, hosted its inaugural research conference in New York, bringing together academics, Wall Street executives, former politicians, and frontline traders. The composition of attendees sent a clear signal—prediction markets are moving from the fringe to the mainstream.

The conference opened with a dialogue between Kalshi co-founders Tarek Mansour and Luana Lopes Lara, moderated by Bloomberg reporter Katherine Doherty. This article excerpts and summarizes key insights from the conference.

Prediction Markets Are More Than Just Elections and Sports

For a long time, prediction markets have been defined by certain "highlight moments"—U.S. elections, the Super Bowl, March Madness. These events dominate news cycles and naturally consume most of the trading volume, leading outsiders to mistakenly believe that the value of prediction markets ends there.

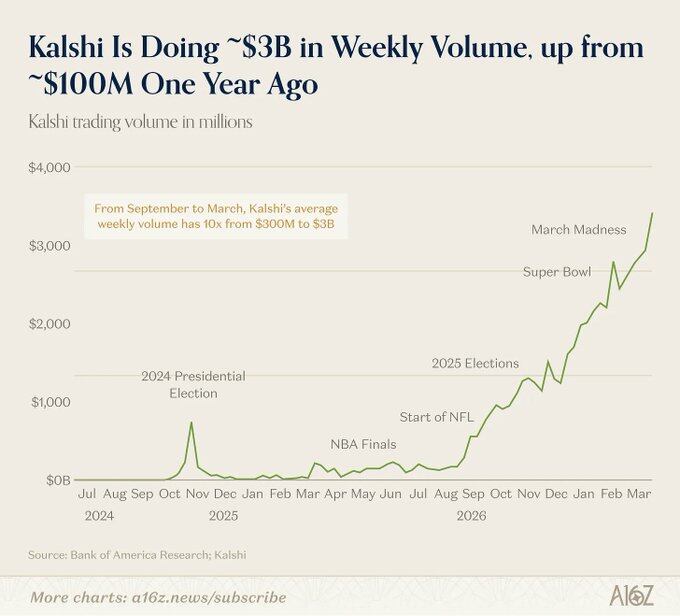

But this impression is being shattered. Just as the conference was held, weekly trading volume for sports predictions had nearly reached $3 billion, accounting for about 80% of Kalshi's total trading volume. While this seems dominant, it hides a more critical trend: sports' share is actually at a historical low.

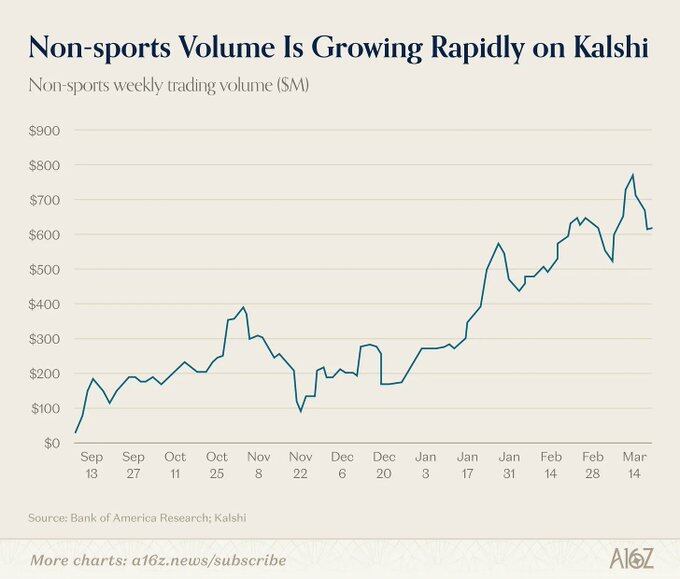

In other words, all other categories are growing faster. Entertainment, crypto, politics, culture, and other areas are driving stronger user growth and more stable retention. Sports act more like an entry product—intuitive, emotionally driven, and rhythmically clear, suitable for attracting mass participation. Meanwhile, long-tail markets, which make up over 20% of total trading volume, are growing rapidly. These markets will play an important role in institutional hedging and information pricing in the future.

This point is also confirmed on the institutional side. Cyril Goddeeris, Global Co-Head of Equity Business at Goldman Sachs, stated that predictions related to macro events and CPI are the categories Wall Street is most focused on currently; Sally Shin, Head of Growth Platforms at CNBC, mentioned that she already uses predictions related to the Fed Chair and non-farm payroll data as narrative tools; Troy Dixon, Global Co-Head of Markets at Tradeweb, envisioned a future where large investment banks will establish dedicated prediction market trading desks, with financial contracts as core products.

Prediction markets are shifting from "recreational trading" to "information and risk tools."

Why Kalshi Has Attracted Wall Street's Attention

Traditional financial markets operate efficiently largely because various assets have recognized benchmarks—the S&P 500 represents the average performance of 500 stocks, and crude oil has the ICE benchmark price. But for political and economic events (such as who will win an election, whether a certain tariff will pass, or the outcome of a Supreme Court case), there was almost no widely recognized and dynamically updated "benchmark" before.

Prediction markets change this. Now, almost any future event can have a real-time, liquid price benchmark. When the market can provide credible pricing for "the probability of a 30% tariff passing," institutions can trade around this price or hedge other risks in their portfolios. This makes the event itself a directly tradable object.

As Tradeweb's Troy Dixon said: "If you go back to when Trump was first elected, many people were hedging in the stock market, such as shorting the S&P, because they thought his election would cause the market to fall. But this was the wrong trade. The question is, how should these events be priced? Where is the benchmark?"

Tarek also mentioned that one motivation for founding Kalshi came from his previous work at Goldman Sachs, where he provided trading advice around the 2024 election and Brexit. Without prediction markets, when institutions hedge political or macro events through related assets, they actually need to make two layers of judgment—they must judge both the outcome of the event itself and the relationship between the event and the traded asset, with the latter carrying a separate risk of failure.

When the event itself has a direct price benchmark, the originally dispersed dual risks are merged into a single judgment. As Tarek said, the market has already begun pricing various events.

The Three Stages Towards Institutional Adoption

It is still too early to say that Wall Street institutions are participating in Kalshi trading on a large scale. Currently, most institutions' usage is still primarily for reference data rather than actual trading.

However, Luana pointed out that the path to institutional adoption is already clear and can be divided into three stages:

- The first stage is data access: Integrating prediction market prices into institutions' daily workflows, such as having Goldman Sachs investment managers view Kalshi odds like they view the VIX index. This stage has already been achieved to some extent. Professor Jonathan Wright from Johns Hopkins University, a former Fed official, stated that for Fed decisions, unemployment rates, and GDP, Kalshi is almost the only reference source;

- The second stage is system integration: Including compliance approval, legal confirmation, technical access, and internal education, i.e., incorporating prediction markets into the usable financial tool system;

- The third stage is actual trading: Institutions begin hedging risks on the platform, trading volume and liquidity gradually accumulate, forming a positive feedback loop. More hedgers attract more speculators, tighter spreads attract more hedgers, and benchmark prices continuously strengthen.

Currently, most institutions are still in the first stage, some have entered the second stage, and only a few have reached the third stage.

A major obstacle preventing institutions from entering the third stage is that current prediction market trading requires full margin—a $100 position requires depositing $100. This is acceptable for retail investors but is a significant limitation for hedge funds or banks that rely on leverage and capital efficiency. As Tarek said, if you want to hedge $100, you must put in $100, which is too costly for institutions; firms like Citadel or Millennium would not adopt this method. Kalshi has already received permission from the National Futures Association and is working with the Commodity Futures Trading Commission to introduce margin trading mechanisms.

What Happens Next?

Michael McDonough, Head of Market Innovation at Bloomberg, gave the most direct judgment: the sign of success is when these things become boring. He compared prediction markets to the options market in the 1970s, which also faced controversies over manipulation and regulatory uncertainty, but these issues were eventually digested and evolved into an almost taken-for-granted infrastructure.

Toby Moskowitz, Partner at AQR, stated that he is willing to bet on the development of prediction markets. Within five years, or even sooner, it will become a viable tool at the institutional level.

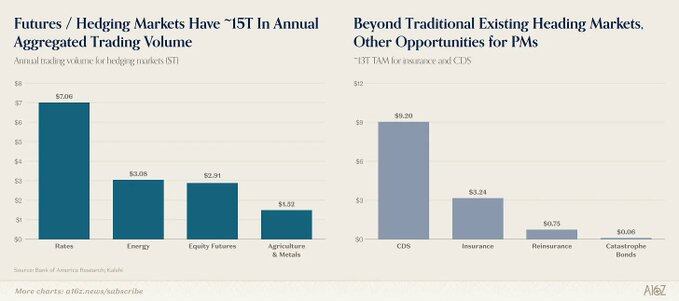

Garrett Herren from Vote Hub described the final form: the question is no longer whether to use prediction markets, but how to use them. Once the discussion shifts to this level, it means they have become indispensable. In fact, although prediction markets are still relatively small, the hedging market itself is extremely large.

The normalization of prediction markets is already happening.

In discussions on political issues, former Congressman Mondaire Jones mentioned that senior figures from both parties, including Trump, House Minority Leader Jeffries, and Senate Minority Leader Schumer, have begun publicly citing Kalshi odds. Scott Tranter from DDHQ also confirmed that prediction market data has now become an important input for intra-party decision-making. Meanwhile, Vote Hub announced that it has directly integrated Kalshi data into its midterm election prediction models.

All of this was almost non-existent two years ago. Back then, the most successful traders on Kalshi were still seen as amateurs. But now, the situation has changed, and it's even hard to define them with that term anymore.

In a roundtable, four traders shared their paths—one spent eleven years studying the Billboard charts, another has been participating in prediction markets since 2006, when it was still a cashless, somewhat geeky interest area. They did not come from the finance industry but from backgrounds in music, politics, and poker. But they unanimously agreed that the platform truly rewards deep domain knowledge, not resumes.

Summary

Prediction markets have come a long way. They were once seen as academic experiments, later became brief highlights during election cycles, and were also viewed as an extension of sports betting.

The message from this conference is clear: prediction markets are gradually evolving into an infrastructure for pricing uncertainty, serving a wide range of participants from retail investors to large institutions and diverse application scenarios.