Author: Lin Wanwan, Dongcha Beating

Original title: Starting with Manus Xiao Hong, Those Crypto Interns Who Made It to the Table

On the last day of 2025, the biggest news in the tech world came from Meta: Mark Zuckerberg spent billions of dollars to acquire Manus, an AI company less than a year old. This is Meta's third-largest acquisition ever, after WhatsApp and Scale AI.

A few days after the news broke, people noticed he had added "BTC Holder" to his bio.

A tweet appeared on Twitter. The poster, using the handle "Shenyu" (real name Mao Shihang), one of China's earliest Bitcoin miners, long since a billionaire:

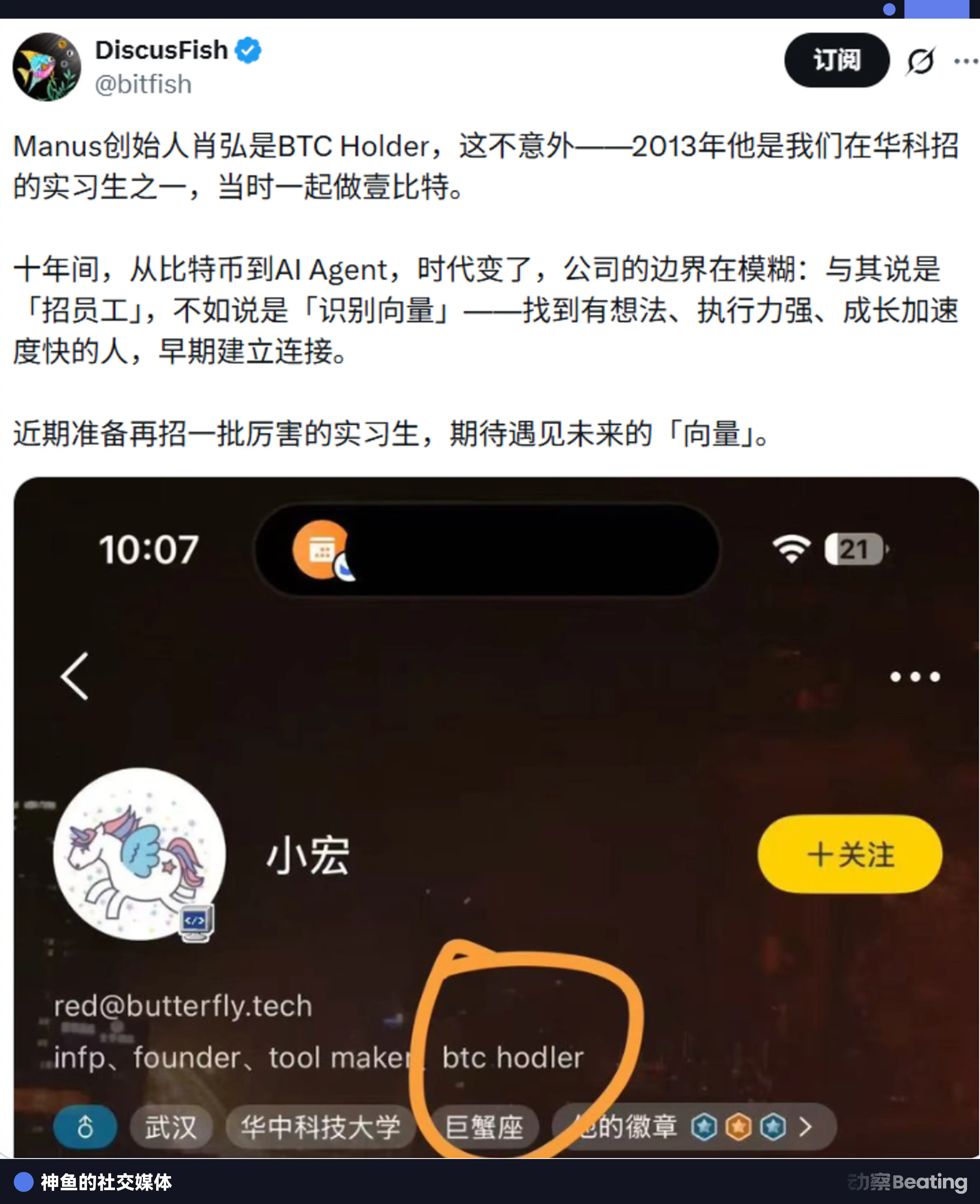

"Manus founder Xiao Hong is a BTC Holder, which is no surprise—back in 2013, he was one of the interns we recruited at Huazhong University of Science and Technology (HUST), working together on YiBit."

2013. YiBit. HUST intern.

Xiao Hong, born in 1993, from a small town in Ji'an, Jiangxi. Before becoming a Meta VP, his most widely known identity was as the founder of the AI products Monica and Manus. But few knew his first proper internship was at a Bitcoin media company called YiBit.

That year, he was just a sophomore at HUST's Qiming College, tinkering with various student projects: WeChat drift bottles, WeChat wall features, campus second-hand trading platforms. Deputy team leader of the联创团队 (Lian Chuang Tuan Dui - Innovation & Entrepreneurship Team), already a somewhat famous tech geek among his peers. But Bitcoin was still a whole new world to him.

YiBit was one of China's earliest vertical Bitcoin news sites, based in Beijing's Galaxy SOHO. The founding team included Shenyu and a few other young idealists. Their work was simple: translate international Bitcoin news, write科普文章 (popular science articles), trying to help more Chinese understand this new thing mainstream media then called a "Ponzi scheme."

What exactly Xiao Hong did at YiBit is hard to verify now. But looking back twelve years later, the significance of that experience far surpassed the internship itself.

The Bitcoin circle in 2013 was a club for early participants in a grand social experiment. No regulation, no pricing anchor, no mature business models—just a group of young people believing in "code is law," huddling for warmth amidst mainstream society's ridicule. Those who entered at that time were either gamblers or those who truly understood something.

Xiao Hong clearly belonged to the latter. Decentralization, permissionless, code-based autonomy. These concepts seemed like geeky self-indulgence back then, but they formed an underlying framework for understanding the world. Twelve years later, as AI began reshaping the boundaries of human-computer interaction, this framework might have become traceable.

From Bitcoin to AI Agent, the technological forms are worlds apart, but the underlying logic is consistent: both are about making machines run autonomously, building collaboration in trustless environments, replacing intermediaries with code. Those who understood Bitcoin in 2013 almost required no additional cognitive purchase to understand AI Agent in 2025.

Shenyu used a term in that tweet: "识别向量" (recognition vector).

"Over the past decade, from Bitcoin to AI Agent, the times have changed, company boundaries have blurred. It's less about hiring employees, more about identifying vectors......"

What is a vector? Direction multiplied by speed. The Xiao Hong of 2013 was a sophomore willing to bet his time on an "unreliable" field. This choice itself was a filter—screening out those who only looked at immediate certainty, leaving those willing to pay for long-term possibility.

12 years later, this vector pointed to the position of Meta VP.

In the cryptocurrency industry, where wealth creation myths coexist with overnight wipeouts, there's a hidden path to success: in your early twenties, follow the right person. Around 2013, a batch of the smartest, boldest young people flooded into this野蛮生长 (wildly growing) world. Some had just dropped out, some hadn't graduated yet, doing the most grassroots work for that era's most疯狂 (crazy) entrepreneurs at exchanges, mining pools, media companies.

They were betting on a certain cognition. This cognition allowed them, a decade later in every technological wave, to identify opportunities faster than their peers.

Warren Buffett once said: "Life is like a snowball. The important thing is finding wet snow and a really long hill."

The cryptocurrency industry in 2013 was that wet, long hill. And those who stepped onto this hill in their early twenties, their snowballs have been rolling for twelve years.

Xiao Hong is one of them. But he is not the only one.

An Intern on a Cap Table

One day in 2013, in an office building in Beijing's Zhongguancun, two young men were discussing something crazy.

Wu Jihan, 27, double degree in Psychology and Economics from Peking University, had just left a venture capital firm. For the past two years, he had been doing Bitcoin investment and evangelism—his Chinese translation of the Satoshi Nakamoto whitepaper remains the most widely circulated version today.

Sitting across from him was Zhan Ketuan, 34, undergraduate from Shandong University, master's from the Chinese Academy of Sciences' Institute of Microelectronics, with over ten years of integrated circuit development experience, recognized in the circle as a master chip designer.

But this story has a third protagonist.

Ge Yuesheng, 21, had graduated from Huzhou University just a year prior. Before joining Bitmain, he and Wu Jihan were colleagues at a Shanghai private equity fund; he was an intern there, both doing investment analysis. Influenced by Wu, Ge started接触 (getting involved with) Bitcoin.

Among these three, Ge Yuesheng was the most inconspicuous. He lacked Wu Jihan's industry insight and Zhan Ketuan's technical background.

But he had one thing: money. More precisely, resources from a family business—capital, mining farms, electricity.

At the time, neither Wu Jihan nor Zhan Ketuan had much money. According to later revelations from former Bitmain executives, Ge Yuesheng's family invested a lot of money early on, with several family members becoming shareholders. Wu Jihan's decision to found Bitmain was很大程度上 (to a large extent) influenced by Ge's investment and help; this intern could be considered Bitmain's earliest angel investor.

The division of labor was clear: Wu Jihan负责 (was responsible for) industry judgment and market, Zhan Ketuan for chip R&D, Ge Yuesheng provided capital and resources.

To get Zhan Ketuan on board, Wu Jihan offered an astonishing condition: Zhan would take no salary, but if he could develop an ASIC chip capable of efficiently running Bitcoin's encryption algorithm in the shortest time, he would get 60% of the shares.

Zhan Ketuan took only six months to develop the 55nm Bitcoin mining chip BM1380 and the first-generation Antminer based on it.

In October 2013, Beijing Bitmain Technology was officially established. Business registration data showed that in the earliest shareholder structure, Zhan Ketuan held 59.2%, Ge Yuesheng held 28%—Wu Jihan's name wasn't even on the list of founding shareholders at the time.

This detail has been反复解读 (repeatedly interpreted) since. Why did the 21-year-old Ge Yuesheng get 28% of the shares?

Bitcoin in 2013 was far from mainstream. In April that year, the Bitcoin price broke $100 for the first time; in November, it surged above $1,000; then in December, it halved, beginning a two-year bear market.

Most people flooded in during the price surge and fled during the crash. Many people have family money, but Ge Yuesheng chose to enter at the industry's earliest, most chaotic stage, and绑定了自己 (bound himself) to that ship.

This required, besides money, a certain intuition for trends, and the courage to place bets amidst uncertainty.

The subsequent story is well-known: these three built Bitmain into the world's largest mining machine company in less than five years, at its peak controlling over 70% of global Bitcoin算力 (hashrate), once valued at $15 billion. On the 2018 Hurun Blockchain Rich List, Wu Jihan became the "85后白手起家新首富" (new self-made richest person of the post-85 generation) with a fortune of 16.5 billion RMB, Ge Yuesheng became the "90后新首富" (new richest person of the post-90 generation) with 3.4 billion RMB.

In 2019, he left Bitmain with Wu Jihan and co-founded Matrixport. Ge Yuesheng became CEO of Matrixport, a role he holds to this day.

A 27-year-old evangelist, a 34-year-old technical genius, and a 21-year-old intern angel investor, bound together at the right time by the same vision.

The First Batch of "OKCoin Whampoa Military Academy"

If Ge Yuesheng's story is a classic case of an intern becoming a co-founder, the next story shows another possibility: from employee number one to being acquired at a high price by a former employer's competitor.

One day in 2013, a young engineer named Wang Hui walked into an office in a Beijing office building.

The office was small, sparsely furnished, looking more like a startup's temporary base. A whiteboard hung on the wall, covered in system architecture diagrams and flowcharts. A few desks pushed together, with less than ten people sitting there.

This was OKCoin's entire operation.

Founder Star Xu was struggling to hire people. Bitcoin in China was still a grey area then, mainstream media coverage either called it a Ponzi scheme or a "money laundering tool." Engineers willing to放弃大厂 offer (give up offers from big tech companies) and join a "crypto trading company" were almost impossible to find.

Wang Hui was the first one willing to take the risk.

As OKCoin's employee number one, he needed to build the entire technical architecture from scratch. No ready-made solutions to copy, no mature open-source projects to use,甚至 (not even) many competitors to reference. Everything was blank.

This meant huge challenges, but also huge opportunity: if he could pull this off, he would become one of the most technically knowledgeable people in the industry.

Within two years, Wang Hui almost single-handedly built OKCoin's core trading system. The performance of that matching engine was碾压级的 (crushing) in the industry at the time. "Many trading platforms' systems couldn't even handle basic concurrency," he later recalled, "they'd freeze up with just a few people trading simultaneously."

More importantly, he cultivated the entire technical team from zero. Many core technical personnel at OKCoin (and later renamed OKEx, OKX) were trained by him.

But by 2016, Wang Hui chose to leave.

Reasons for leaving spawned many rumors in the circle: disagreements with the founder, internal factional struggles, dissatisfaction with the company's direction... Wang Hui himself never publicly responded to these claims.

But one thing is certain: he took with him all the experience and connections accumulated at OKCoin.

His first stop after leaving was a brief collaboration with another former OKCoin executive. That person was Changpeng Zhao (CZ), who later founded Binance, becoming the global crypto richest person.

In early 2018, Wang Hui and two old colleagues founded JEX, focusing on cryptocurrency options trading. The timing was微妙 (very微妙 - delicate/interesting). January 2018, Bitcoin had just started its crash from the all-time high of $20,000, the entire industry was in misery. Most were fleeing, but Wang Hui chose to enter against the trend.

JEX received investment from Huobi and Jinse Finance. Just a year later, in 2019, Binance announced the full acquisition of JEX, reportedly for hundreds of millions of RMB.

This was a rather dramatic结局 (ending): OKCoin's employee number one had his company acquired by Binance.

Going around in circles, these people all came from the same place.

Hence the saying still流传 (circulates) in the crypto circle: OKCoin is the "Whampoa Military Academy of the cryptocurrency industry."

Vectors, Windows, and Survivors

Now, let's return to Xiao Hong.

In 2013, he was just a sophomore interning at YiBit. This internship might occupy only a small part of his life resume—after all, his main path later was WeChat ecosystem entrepreneurship: Yiban, Weiban, Nightingale Tech, eventually sold to Minglue Tech.

But some things leave a mark.

Xiao Hong introduces himself as a "BTC Holder." This means, from 2013 to today, he has maintained at least some关注和参与 (attention and participation) in cryptocurrency. In a market where price fluctuations are measured in multiples of a hundred, holding for twelve years本身就是 (is itself) a skill, or perhaps, a belief.

More importantly, that brief internship in 2013 might have shaped a certain methodology in him: not pursuing technological disruption from zero to one, but being good at finding gaps on existing large platforms, creating value with product capability.

From YiBit to the WeChat ecosystem's Yiban and Weiban, to the AI browser plugin Monica, finally to the general AI Manus, the underlying logic of this path might be consistent: find a large platform that is exploding, build the best tool on that platform.

The stories of these three interns reveal some common patterns:

First, timing is more important than effort. They all entered the cryptocurrency industry between 2013-2017. That was the industry's "chaotic period." Early enough that most people hadn't realized the opportunity existed; but not so early that infrastructure was completely absent. Those who entered during this window gained disproportionate growth space. By 2020 onwards, the industry was relatively mature, making it much harder for newcomers to replicate the same path.

Second, choosing who to follow is more important than choosing what to do. Ge Yuesheng followed Wu Jihan, Wang Hui followed Star Xu, Xiao Hong followed Shenyu. These大佬 (big shots) weren't necessarily the most famous, but they were among the most discerning and execution-oriented people at the time.

The benefit of following the right person isn't just learning, but more importantly, entering a high-quality network. Wang Hui's ability to quickly secure investment and get acquired by Binance after leaving OKCoin was largely due to the reputation and connections he accumulated in the circle.

Third, the ability to place bets in the face of uncertainty is scarce. Joining a Bitcoin company in 2013,坚守 (persisting) in a bear market DEX project in 2018,放弃稳定工作去创业 (giving up a stable job to start a business) in 2020—these choices all seemed full of risk at the time.

But risk and reward are symmetrical. Those willing to承担不确定性 (bear uncertainty) ultimately received returns匹配 (matching) the risks they took.

Of course, these are stories of幸存者偏差 (survivorship bias).

Most of the young people who entered the crypto circle around 2013 did not become billionaires. Many left during bear markets, missed bull runs, got wiped out in the violent fluctuations. But this doesn't prevent us from extracting something valuable from the survivors' stories.

On the last day of 2025, Xiao Hong tweeted: "There are many annoyances in trying to build a good product in a globalized market that don't come from the business itself or user value. All of this is worth it."

From YiBit intern in 2013 to Meta VP in 2025, Xiao Hong took 12 years.

In these 12 years, his former boss Shenyu went from a 23-year-old grad school dropout entrepreneur to a billionaire industry godfather. Shenyu's former partner Wu Jihan went from an evangelist to the builder of a mining empire, left after internal strife, started over, and rose again.

The pace of this industry is too fast. Fast enough that a decade can complete someone's transformation from intern to billionaire, also fast enough that a decade can see a giant fall from peak and rise again.

So, be kind to every intern around you. Because you never know who you'll need to buy dinner for in ten years.

Twitter:https://twitter.com/BitpushNewsCN

Bitpush TG Discussion Group:https://t.me/BitPushCommunity

Bitpush TG Subscription: https://t.me/bitpush