On February 10, 2026, Alphabet, Google's parent company, issued a bond in London with a maturity date a hundred years in the future.

A hundred years.

Anyone buying this bond is betting that by the time their grandchildren retire, this company will still be alive and have the money to pay it back.

Historically, century bonds are extremely rare. Disney issued one in 1993, Coca-Cola did, and further back, Norfolk Southern Railway did. In fact, this term length was standard for 19th-century railroad companies because laying tracks, digging tunnels, and building bridges had investment payback periods so long they had to be calculated in 'centuries'.

But now, an internet company is borrowing money like a railroad company. Why?

Over the past eighteen months, the answer has gradually emerged. It's not in the PPT of any AI launch event, not on the benchmark leaderboards, and not in the debates about 'when AGI will arrive'. It's hidden in the capital expenditure line of financial reports, in the spread changes of bond issuances, in the cliff-like plunge of free cash flow.

To understand this answer, you first need to see what has disappeared.

The Money-Printing Machine Smashed by Its Own Hand

First, we need to understand that over the past two decades, what Wall Street believed in most was not a particular tech company itself, but a financial structure adopted by this cohort of companies.

These tech companies' revenue came from advertising, cloud services, platform commissions—all delivered digitally, with marginal costs approaching zero. No factories needed, no inventory, no mines or oil wells. The more users, the thinner the cost spread, the higher the profit margin.

The direct product of this structure is free cash flow. Unlike net profit, which on the income statement can be polished by accounting rules, free cash flow is the real money flowing into bank accounts, money that can be used for stock buybacks, dividends, and investing in the future. This is why US tech stocks get premium valuations.

There was an old joke about Apple sitting on over $200 billion in cash not knowing how to spend it; Google generating tens of billions in free cash flow year after year, as if the search box was directly connected to a gold mine; Amazon, under the guise of a low-margin e-commerce business, having a cloud computing money printer underneath; Meta making heaps of money from over two billion people seeing ads every day.

Investors weren't just buying growth; they were buying the 'light-asset, high-cash-flow' narrative because it promised these companies would never be dragged down by factories like General Motors, crushed by infrastructure debt like AT&T, or tortured by the capital expenditure cycles of oil companies. They could directly ignore the gravity of industrial capitalism.

Then AI arrived. And AI brought a surprisingly counterintuitive result.

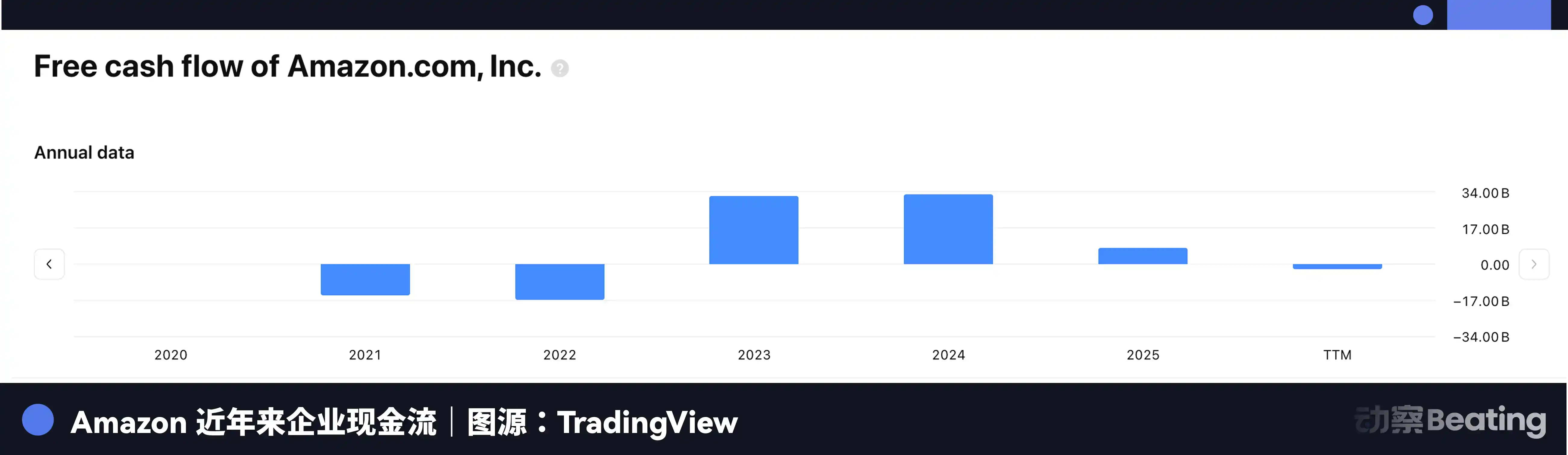

At the end of April this year, Amazon released its Q1 earnings. Revenue, profit, AWS growth were all decent. Over the past twelve months, Amazon's operating cash flow was $148.5 billion, up 30% year-over-year, looking good. But during the same period, free cash flow dropped from $25.9 billion to $1.2 billion, evaporating by 95%.

Where did the money go? Amazon's Q1 capital expenditure alone was $44.2 billion, up 76.7% year-over-year, with full-year guidance around $200 billion. Almost all of this money is being thrown into AI infrastructure—data centers, GPUs, networking equipment, power contracts.

Amazon isn't making less money; on the contrary, they're making more than before. It's just that they're throwing almost every penny of it into the bottomless pit of AI. Operating cash flow is the Yangtze River, capital expenditure is the Three Gorges Dam, and free cash flow has become a trickle downstream.

The others aren't much better.

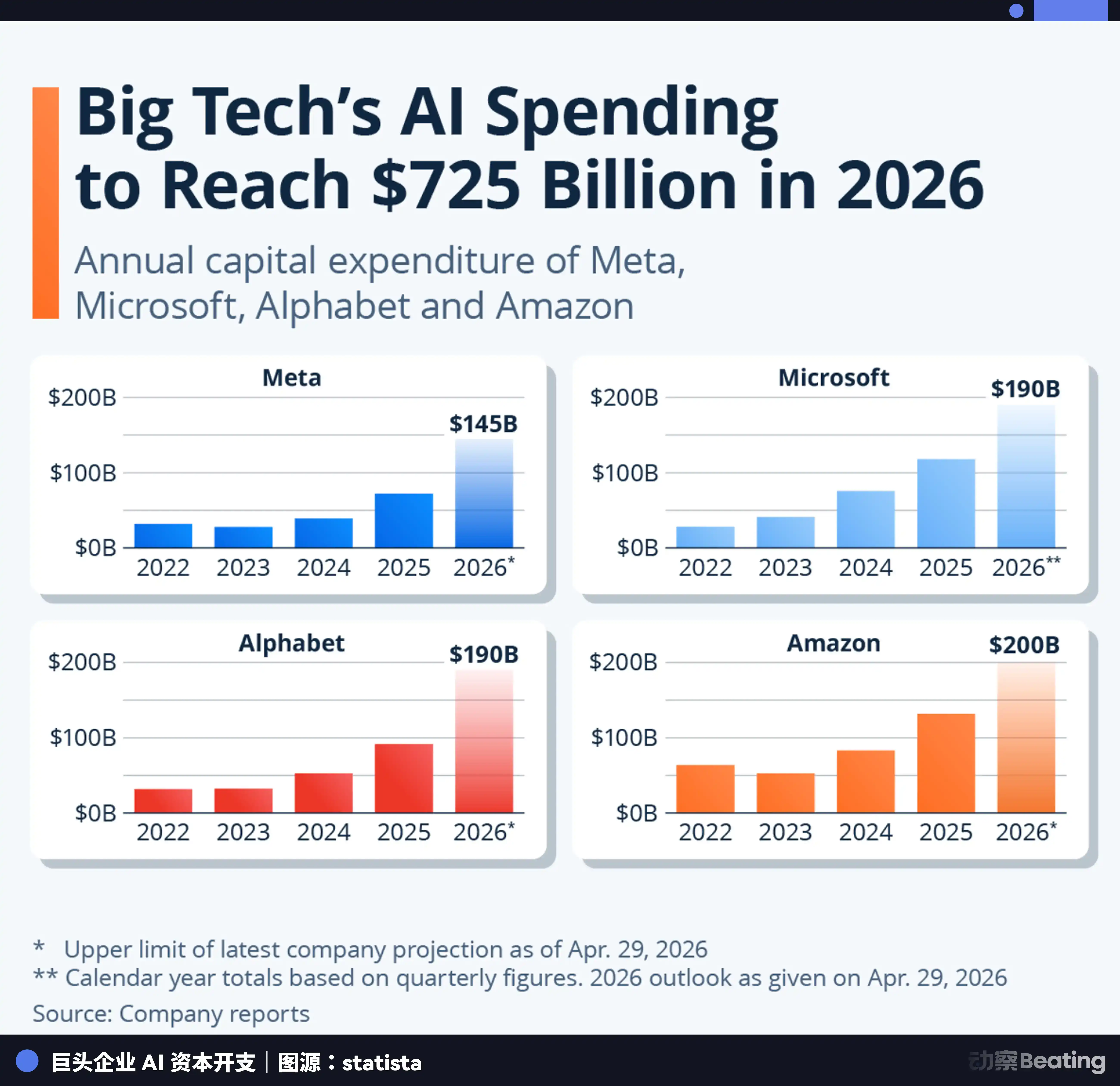

In 2026, the combined capital expenditure guidance for the four giants is $700 to $725 billion: Amazon ~$200B, Microsoft ~$190B, Alphabet ~$185B, Meta $125-145B. In 2022, the four combined spent $162 billion, a 4.5x increase in four years. Just in Q1 2026 alone, the four spent over $130 billion combined, more than the annual GDP of many countries.

On the surface, these companies still look shiny. Revenue is growing, profit margins are holding up well, and the AI launch events are still lively. But 'Free Cash Flow' doesn't agree.

'Profit' is, ultimately, an opinion. How depreciation periods are set, how R&D is capitalized, how revenue is recognized—all have room for creative accounting. But 'Cash Flow' is a fact. Money in, money out, clear as day. Profit tells a story; cash flow tells the truth.

So the truth is that the core financial advantage of being 'light-asset, high-cash-return' that these companies built over two decades is being eaten away, bite by bite, by AI capital expenditures.

The immediate question follows: Free cash flow is at rock bottom, yet their investments are ramping up. So where is this money coming from?

Borrowing. And the way they're borrowing now is unprecedented.

In Three Months, Borrowing Half the World's Money

Alphabet borrowed $32 billion in February.

One month later, in March, Amazon completed a $36.9 billion bond issuance, with 11 tranches ranging from two-year to fifty-year maturities. Investor orders totaled $126 billion, 3.4 times oversubscribed. After this bond, Amazon's total debt nearly doubled in a year. Another month later. On April 30, Meta issued $25 billion in bonds.

Another month later, on May 11, Alphabet announced it was preparing its first yen-denominated bond. This is interesting; Alphabet's February bond issuance wasn't just in dollars, it also included 3.1 billion Swiss francs.

This is a company based in California, USA, with revenue almost entirely in US dollars, yet it went to Switzerland to borrow money. And in May, it set its sights on the yen. Amazon's March deal also included euro tranches.

This isn't currency diversification by the giants' finance departments for appearances; this is forced.

Look at Meta. Its April $25 billion bond, the longest 2066 maturity tranche was priced at a spread of 1.47 percentage points—the risk premium investors demanded over US Treasuries. Six months earlier, in October 2025, when Meta issued a similar forty-year tranche, the spread was only 1.10. It widened by 37 basis points in six months, and not just for the longest tranche; the premium for almost all six tranches it issued was higher than the last round.

So, these giants need to find places with lower interest rates. The Swiss National Bank's policy rate is the lowest among major economies, and Swiss franc bond yields are far lower than dollar ones. Japan, while having ended the negative interest rate era, still offers a huge advantage in yen financing costs. More critically, investors in Zurich and Tokyo aren't yet flooded with Silicon Valley tech debt; their appetite is fresh, not as picky as New York's. For a top-tier borrower like Alphabet, borrowing elsewhere is both cheaper and avoids the queue.

AI's capital expenditures land in the US (data centers) and Taiwan, China (chips), but the money to pay for it is pulled from Switzerland, from Japan, from Europe. Silicon Valley globalized technologically for two decades; now it's globalizing in debt.

And the buyers of these bonds aren't hedge funds or venture capital. Those who can digest century, fifty-year bonds are pension funds, insurance companies, sovereign wealth funds—the most risk-averse money in the global financial system. Their mission is capital preservation, stability, beating inflation, not taking risks.

But now, the pension fund of a retired teacher in Zurich, the reserves a Tokyo insurance company sets aside for life insurance policies, are flowing through the transmission chain of the bond market into a data center in Oregon or Virginia, turning into GPUs on racks and cooling towers on roofs. Most of these holders don't know the underlying assets of their bonds. Their fund managers buy 'Alphabet Aa2 credit', 'Amazon A1 credit'; the rating agencies' letters give a sense of security. As for what buildings this money ultimately builds, what equipment it installs, what models it runs, whether those models can earn enough to repay the debt—there are too many intermediate layers; it's impossible to see clearly from Zurich and Tokyo.

The world's most conservative money is now funding the world's most radical technology bet.

When Internet Companies Grow Smokestacks

But this money hasn't become ad spending, user subsidies, or stock buybacks. None of the usual ways tech companies spent money over the past two decades have been followed this time.

This money has turned into concrete, steel, copper wire, transformers, and cooling pipes.

Amazon's $200 billion 2026 capital expenditure guidance means it spends $550 million per day, $23 million per hour, $380,000 per minute. Microsoft announced plans to invest $10 billion in AI infrastructure in Japan alone from 2026 to 2029.

This isn't a software company's expansion pace; this is infrastructure.

And the essence of infrastructure is making a company heavy.

The construction cycle, investment scale, and operational complexity of a large data center are on the same order of magnitude as an auto assembly plant or a semiconductor fab. Site selection, environmental impact assessment, power connection agreements, water source guarantees, physical security—the whole process has to be run through.

GPUs in AI play a role similar to high-end machine tools in manufacturing: expensive, capacity-constrained, rapidly depreciating. The chips bought with heavy money today may be obsolete in two or three years, but you can't wait, because your competitors won't.

Electricity has become a strategic resource. A large AI data center's power consumption is equivalent to a mid-sized city. Giants are signing long-term power purchase agreements, investing in nuclear power, negotiating dedicated power lines with utility companies.

Cooling water is starting to compete with residents for water rights; many communities in arid regions find an unwelcome guest on their water usage rankings.

These scenes were impossible for tech companies twenty years ago. Site negotiations, grid access, water rights disputes, local tax incentives—these are things railroad companies, power companies, and refineries do. And century bonds, fifty-year bonds, cross-currency issuances—the last time these financial instruments were used intensively was also during the great era of railroad and telecom construction.

Opening the 2026 balance sheets and cash flow statements, these companies' numbers now look closer to TSMC, Duke Energy, or Union Pacific Railroad than they do to their own ten years ago.

This touches on valuation. The core assumption of the past investor pricing logic for tech giants was marginal cost decrease—one more user, one more ad, incremental cost near zero, so profit margins would keep expanding. But the AI infrastructure layer isn't like that. Every additional model trained, every inference cluster deployed, every data center built requires real money invested. Whether the investment pays off depends on whether customers will pay, how model efficiency evolves, and how the competitive landscape changes.

And all of this is uncertain.

This is more like semiconductors: each new process node requires a bigger fab, and returns depend on yield and the market. It's also like power: generation capacity is built first, and returns depend on electricity prices and demand. And it's like railroads: tracks are laid first, and returns depend on whether the economy along the line develops.

So, since tech giants' financial structures are becoming more like heavy-asset companies, the valuation multiples the market gives them will eventually converge toward those of heavy-asset companies.

Some might say once the infrastructure is built, they'll return to a light-asset model. Too naive. Railroads have been built for over a hundred years and are still being built; power grids have been built for a century without stopping; semiconductor fabs need upgrades every few years. The infrastructure of a general-purpose technology has never been 'finished.'

AI may not be a continuation of the internet; it might be a resurgence of industrial capitalism, wearing a cloak of code and standing on a concrete foundation. The internet spent twenty years letting tech companies escape gravity; AI is pulling them back in two years.

Every General-Purpose Technology Revolution

In 1840s Britain, railroads were the AI of that era. Freight speed jumped from a few miles per hour with horse-drawn carriages to tens of miles per hour with trains—an order-of-magnitude efficiency leap, also quite exaggerated.

Capital flooded in. In 1846, the total railway investment authorized by the British Parliament was about £600 million, while Britain's annual GDP was only around £500 million. A nation bet more than a full year's national income on a new technology. Today, that's like the US throwing over $25 trillion into AI.

Early railroads mainly relied on selling stock for financing. Buyers were filled with imagination about the future. Later, as construction scale snowballed and returns were delayed, with later projects deteriorating in quality, equity financing wasn't enough; debt financing stepped into the spotlight. Railway companies began issuing bonds, mortgaging future revenues from uncompleted lines. Financing became increasingly aggressive, from domestic to international borrowing.

What killed the boom wasn't a problem with railway technology; it was interest rates. In 1846, the Bank of England tightened monetary policy, triggered by grain imports and gold outflows due to the Irish famine, which had nothing to do with railways. But interest rates don't care about the reason; they just kill the borrowers with the weakest cash flow. Railway stocks crashed, and many railway companies went bankrupt.

But fortunately, the railways themselves remained. Tracks, stations, tunnels, bridges didn't disappear because investors lost money. They were taken over at a discount by later players, integrated, and operated, eventually becoming the arteries of the British Industrial Revolution. The rise and fall of cities, industrial layouts, and population flows were rearranged along the tracks.

Twenty years later, the same play repeated across the Atlantic. After the US Civil War, the federal government encouraged western railroad construction with land grants and loan guarantees. Over 35,000 miles of new track were laid during the boom. Railway bond yields of 6.4% to 6.7% were the most attractive fixed-income product at the time. Money poured in from the East Coast, from Europe, into the wilderness of the American West.

In 1873, Jay Cooke & Company, the main financier of the Northern Pacific Railway and one of the largest investment banks in the US at the time, declared bankruptcy. The chain reaction ultimately led to 18,000 businesses failing within two years, with 89 railroads going bankrupt over six years.

But America's railway network was ultimately built. It became the physical foundation for the US becoming a 20th-century super industrial power. However, the people who built the railroads and the people who ultimately made money from them were not the same people.

Fiber optics were similar.

In the late 1990s, the rise of the internet fueled huge imaginations about bandwidth. Telecom companies began laying fiber optics frantically, not just connecting cities but also linking continents and crossing oceans. Between 1996 and 2001, US telecom companies issued over $500 billion in new bonds to finance this construction, burying tens of millions of miles of fiber optic cable underground and on seabeds.

But the laying speed far outpaced demand. When the bubble burst, only about 5% of the fiber laid across the US was connected to equipment and carrying data. The remaining 95% was 'dark fiber,' lying underground, waiting for an unknown future.

WorldCom, the second-largest US long-distance operator, with $107 billion in assets, filed for bankruptcy in 2002—the largest bankruptcy in US history at the time. Global Crossing, which built one of the world's largest fiber networks, also fell that year. Winstar, 360networks, McLeodUSA—a string of names fell on the excess of dark fiber.

But fiber optics also ultimately remained. Those undersea cables and metropolitan networks ridiculed as overbuilt in the 1990s became the backbone of the entire internet economy over the next two decades. Netflix streaming, Google search, Amazon's cloud all ran on that fiber, or on its upgraded versions.

The same logical chain appears repeatedly in these three historical episodes.

First, the technology itself is real. Railroads were indeed faster than carriages, fiber optics were indeed faster than copper wires, and AI indeed can do things previously impossible. No one denies the value of the technology itself in hindsight.

But the construction speed far exceeded short-term demand because competition among peers didn't allow anyone to stop and wait for demand to catch up. You believed it was a winner-take-all game where the first to build locked in customers and ecosystems, so you had to keep running.

Everyone was running, leading to collective overbuilding. To sustain the overbuilding speed, financing became increasingly aggressive: equity wasn't enough, so debt was used; short-term wasn't enough, so long-term was used; domestic currency wasn't enough, so foreign currency was used. Railroads were like this, fiber optics were like this, and Swiss franc bonds, yen bonds, century bonds are also like this.

What ultimately triggered the correction was often not a problem with the technology, but a change in financial conditions. In 1846, it was rising interest rates; in 1873, it was an investment bank's bankruptcy triggering a credit chain break; in 2001, it was the dot-com bubble combined with recession. The technology kept advancing, but companies couldn't hold on.

In the end, the infrastructure remained, but a significant portion of the builders did not. The beneficiaries of the railroads were the cities and factories along the lines, not necessarily the original shareholders of the railroad companies. The beneficiaries of the fiber optics were Google, Netflix, Amazon, not WorldCom's bondholders.

Of course, we can't directly equate today's tech giants with 19th-century railroad tycoons or 1990s telecom adventurers. The difference is that today's companies have massive, still-growing core business cash flows. Amazon has AWS and e-commerce; Alphabet has Search and YouTube; Meta has the world's largest social advertising network; Microsoft has Office and Azure.

They aren't startups building data centers by burning investor money; they are giants with real profits mortgaging their own futures.

So the question is whether the payback period for capital expenditure can outrun the repayment period of the debt. Railroads were good, but borrowing money for six years to build lines that take twenty years to pay back can kill you just the same. Fiber optics were good, but borrowing for five years to lay cables only 5% of which are used can't save a balance sheet either.

AI data centers are certainly good. But what scale of AI revenue is needed to break even on $200 billion in annual capital expenditure? How many years are needed to recoup $700 billion in combined investment? If model efficiency advances faster than expected—say, a new architecture makes the same task require one-tenth the computing power—could the computing power built at great cost today become the new generation of dark fiber?

All Bonds Issued Are Buying the Same Thing

Back to that century bond at the beginning.

The institutional investor who bought it—maybe a Swiss pension fund, maybe a British insurance company—made a decision that day: lend money to Alphabet, to be repaid in a hundred years.

Behind this decision is a chain of beliefs: believing AI will be widely adopted, Alphabet will survive this race, its Search and advertising businesses will continue to generate cash, the data centers it builds will be fully utilized, and no disaster will destroy this company over the next century in the global economy.

The holders of Amazon's fifty-year bonds have a similar, though perhaps slightly shorter, chain of beliefs in their minds. Meta's bondholders accepted record-high CDS premiums, but the chain is shorter because the market is clearly giving Meta a narrower credit window than the others.

The chains vary in length, but they are buying the same thing. Not GPUs, not data centers, not fiber optics and transformers—those are intermediates. What they are truly buying is time.

AI models are trending towards homogenization. Open source is catching up with closed source; small models are approaching large models; the capability gap is narrowing. Before this window closes, before everyone can run similar models, whoever can first scale up computing power and lock enterprise customers onto their cloud can turn temporary technological leadership into a lasting commercial moat.

So the giants aren't betting on 'whose model is smartest,' but on a more fundamental proposition: before AI capabilities fully diffuse, can I build infrastructure and customer relationships to a scale others can't catch up with?

This is time arbitrage—using today's low-cost money to buy tomorrow's market position.

Time arbitrage has a cruel prerequisite: the future must arrive on time.

The four companies face different time pressures.

Amazon is the most urgent. Free cash flow has been swallowed by capital expenditure to a mere $1.2 billion. AWS's AI service revenue must reach scale within two or three years; otherwise, debt pressure will seep from the balance sheet into the income statement.

Meta is the most fragile. Social advertising profits are rich, but there's a missing bridge between them and the commercialization of AI infrastructure. Azure and AWS can directly sell computing power to enterprise clients. After Meta spends over a hundred billion building infrastructure, what it turns into, who it sells to, and how it charges—the story isn't fully fleshed out yet. The market's impatience is already written in its stock price and CDS.

Alphabet is the most composed. Search and YouTube require little maintenance to keep generating cash. Even if AI yields no short-term returns, the core business can provide a safety net. The market gave it century-long credit—the longest time window among the four. But $185 billion in capital expenditure is 2.5 times last year's; the acceleration itself consumes patience. Composure doesn't equal safety.

Microsoft is the clearest. Its deep tie-up with OpenAI has made Azure a direct beneficiary of AI commercialization. Copilot is already charging; GitHub Copilot is one of the highest-paid-for AI products among programmers. The path from infrastructure to revenue is the shortest. But $190 billion in capital expenditure means that even with a clear path, the bet's size is so large that everything must go according to script to break even.

All four are betting on the same thing, which in a nutshell is: borrowing money from the future to build something not fully understood today, betting that use cases explode before the debt comes due.

This road has been traveled by railroads, by fiber optics. Each time, the technology ultimately proved its worth, and the infrastructure remained. But each time, there were also a group—sometimes a large group—of people who paid for the construction and didn't live to see it pay off. The technology was right, the timing was wrong, and financial markets don't give wrong timing a second chance.

No one knows if AI's 'future' will arrive on time. The only certainty is this: the world's most conservative pool of money has already, by buying these century, fifty-year, forty-year bonds, signed a contract with Silicon Valley.

The contract's terms are simple: We lend you time, you give us the future.

As for whether the future will keep its promise, no one can say for sure now.