Bittensor [TAO] continued to trade above the psychological $300 level. While the market leaders Bitcoin [BTC] and Ethereum [ETH] faced strong selling pressure over the past week and were forced to register losses, TAO continued to trend higher.

The $300 was therefore an important support level that swing traders should keep an eye on. Is the sustained uptrend another buying opportunity for TAO traders, or should they take profits and expect a deep retracement next?

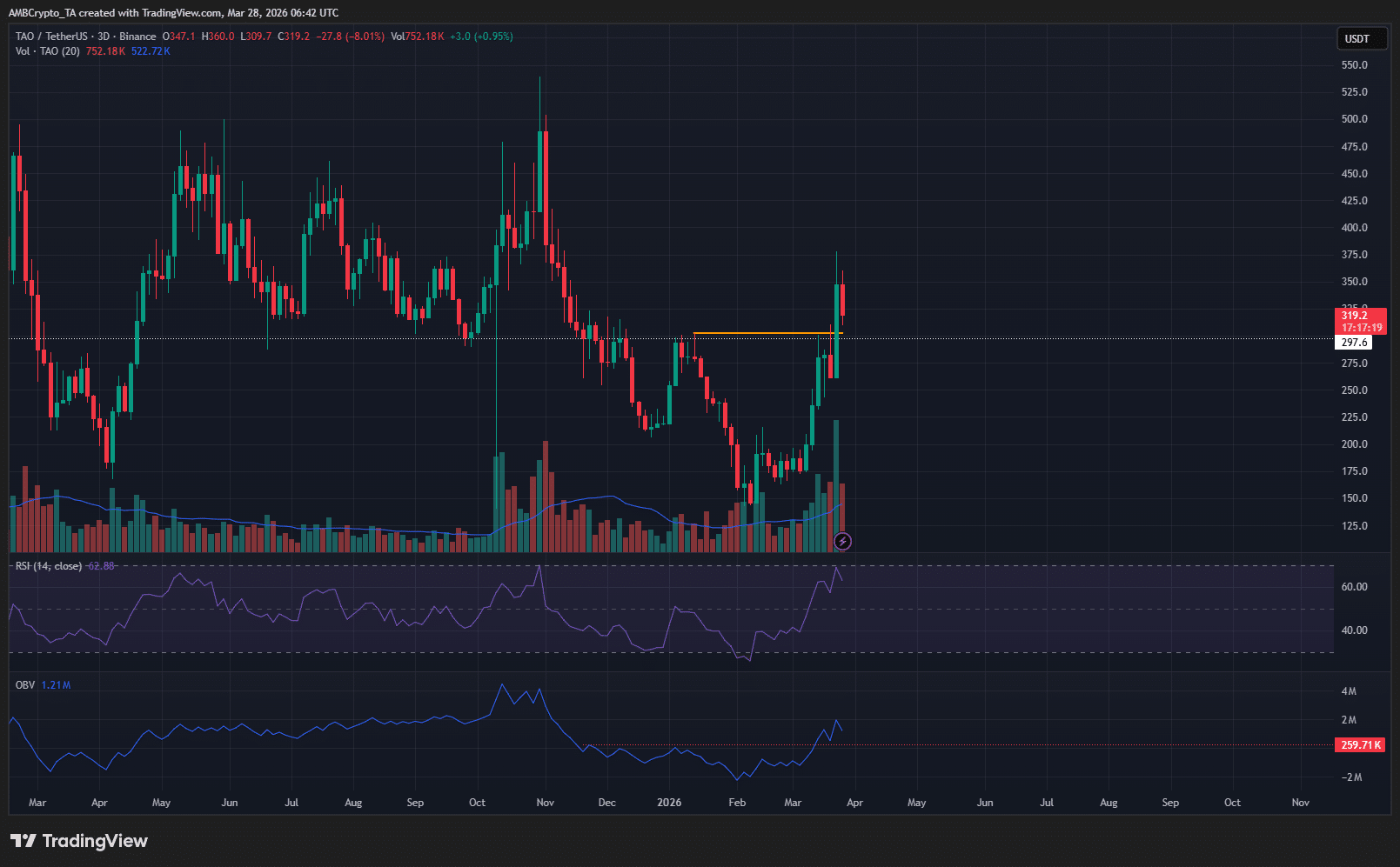

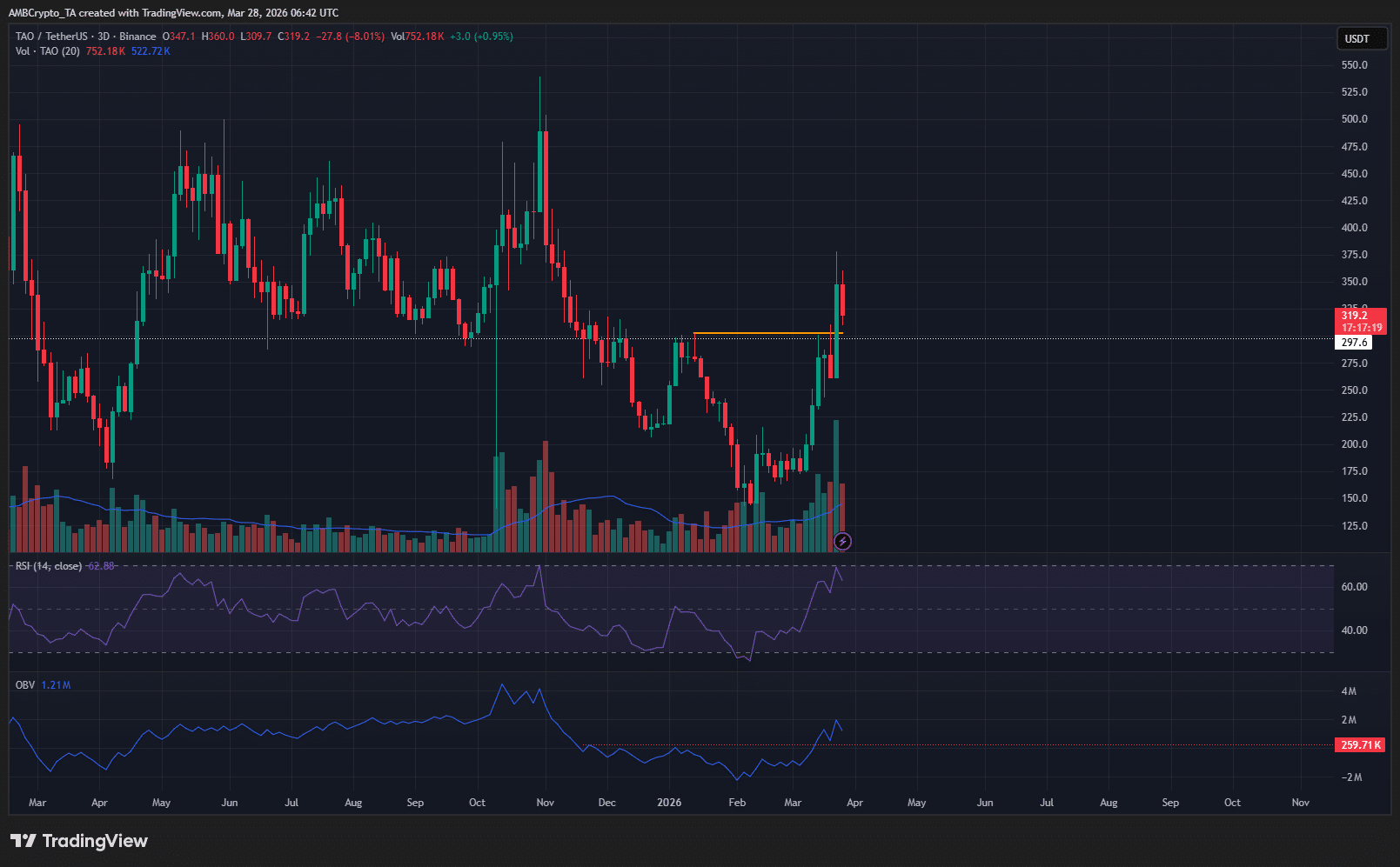

The bullish TAO swing structure confirms the trend direction

The move above $302.4 last week represented a bullish swing structural shift for TAO on the 3-day chart. At the same time, the OBV was making new local highs, and a psychological round number resistance had been overcome.

These developments were remarkable, especially as Bitcoin and many altcoins were forced to go lower or trade sideways. The demand for decentralized AI infrastructure likely explained the AI token’s relative strength.

A pullback toward $300 would be a buying opportunity for Bittensor traders and investors. Their next targets would be $450-$500.

Why traders should buy now

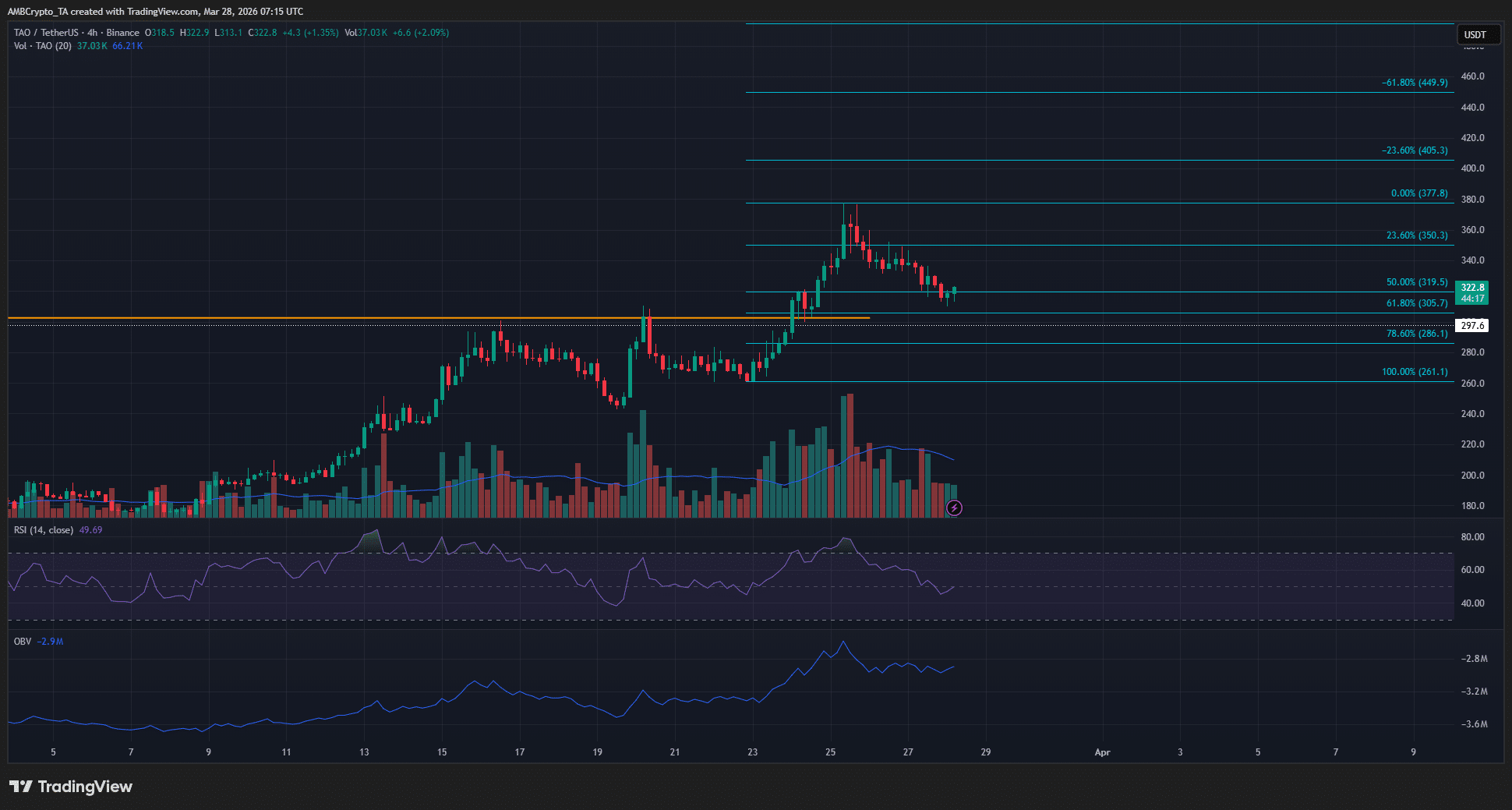

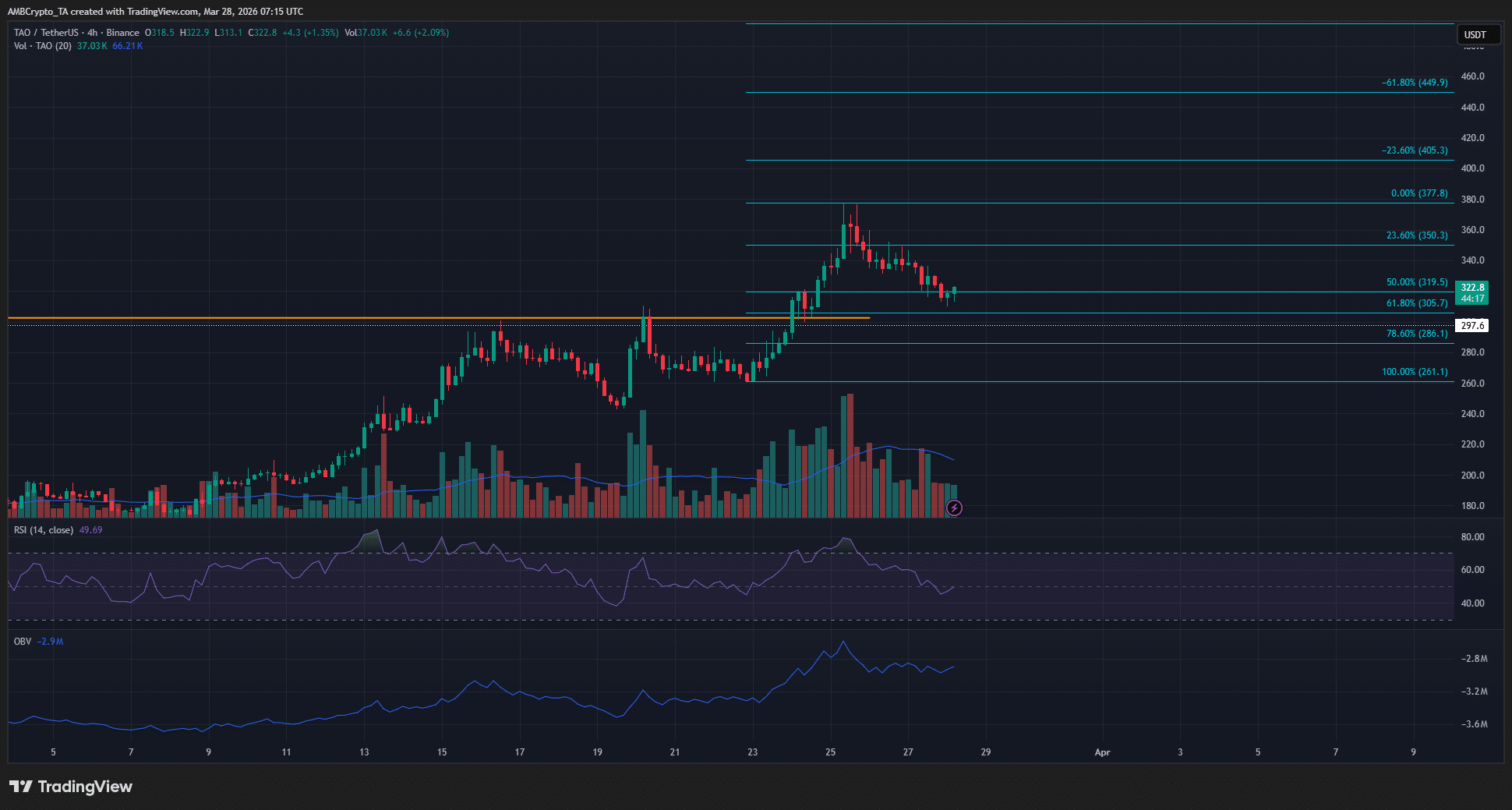

The 4-hour chart was quite encouraging. In this timeframe, the price structure was firmly bullish. The technical indicators also supported the upward momentum and reflected steady buying pressure on the altcoin.

The Fibonacci retracement levels (cyan) showed that a retracement was underway. The $286-$305 pocket would be the ideal buying zone, but it is unclear if we will get this dip.

Traders can look to buy anywhere within the $286-$319 area, as many traders and analysts also consider the 50% retracement as a key support in an uptrend. In either scenario, the $405 and $449 levels would be the next targets.

A drop below the $261.1 mark will shift the H4 structure bearishly and invalidate the bullish setup laid out above.

Final Summary

- Bittensor continued to trade above the $300 level despite the crypto market correction over the past two days.

- This show of relative strength could see another uptrend next week, with $409 and $450 being the next targets.