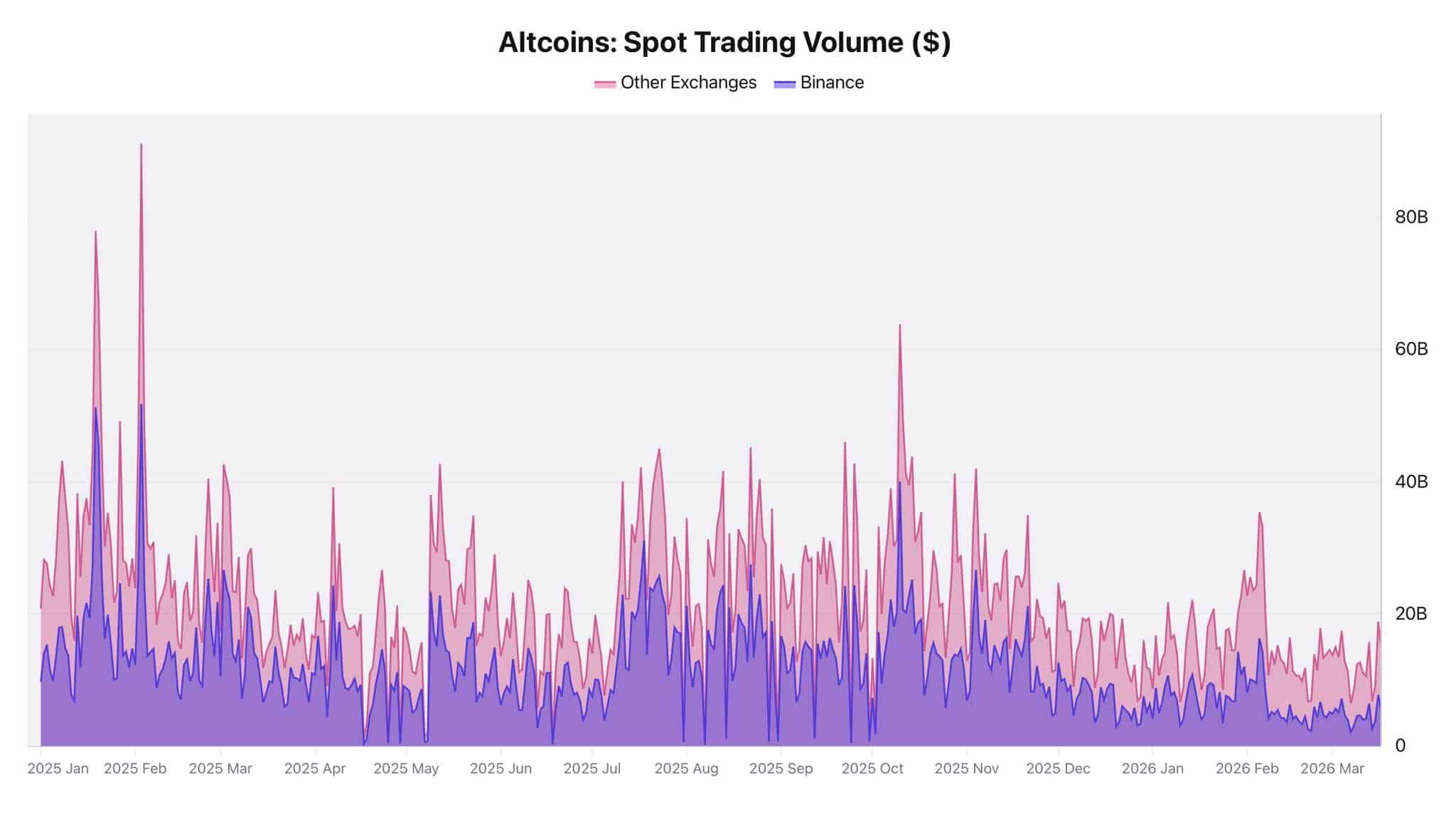

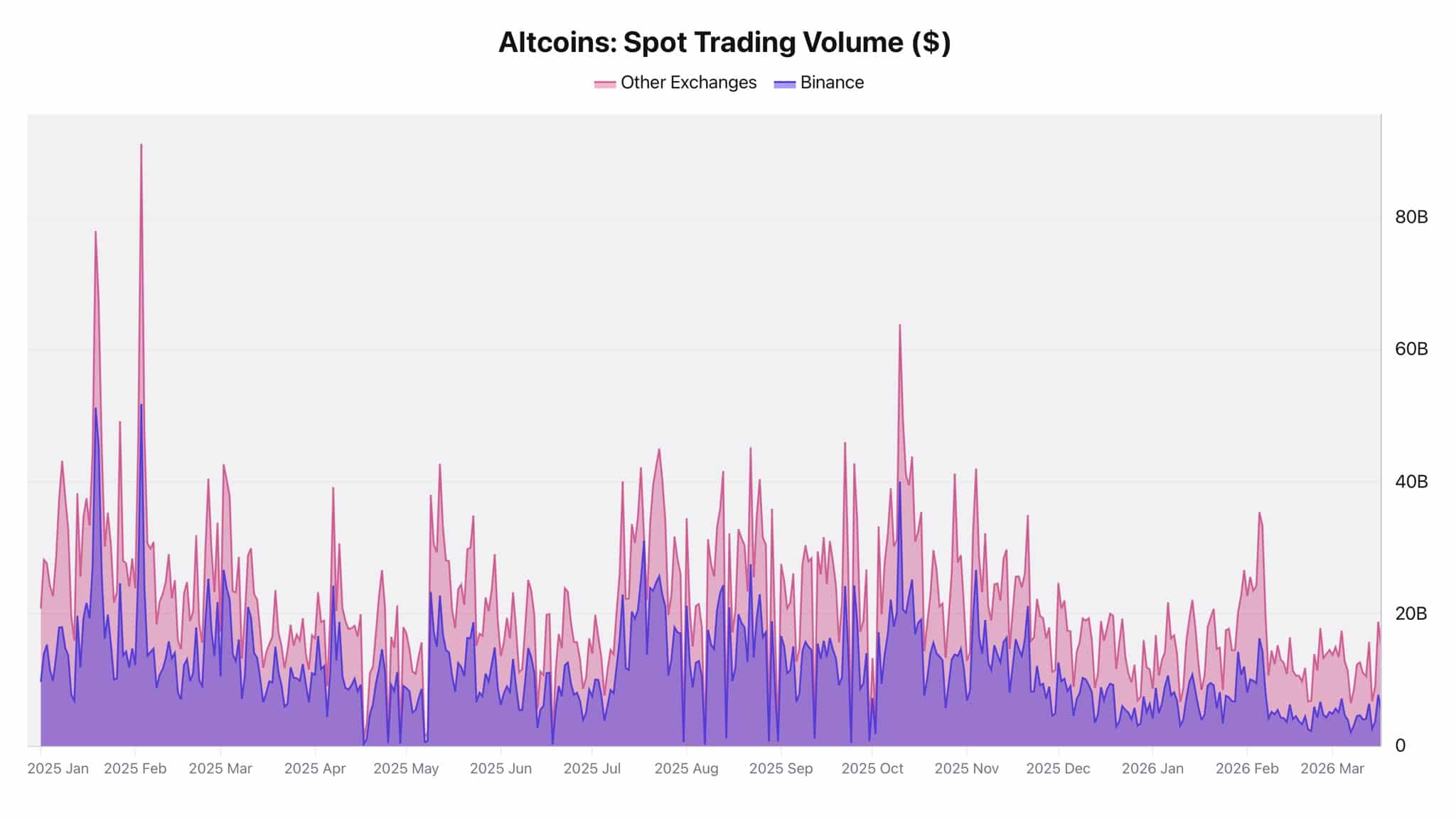

Altcoin trading volume has dropped towards $26.5 billion from peaks above $100 billion, showing a sharp contraction in activity. As this decline unfolded, Binance processed about $7.7 billion. All while other exchanges handled roughly $18.8 billion – Confirming broad-based weakness.

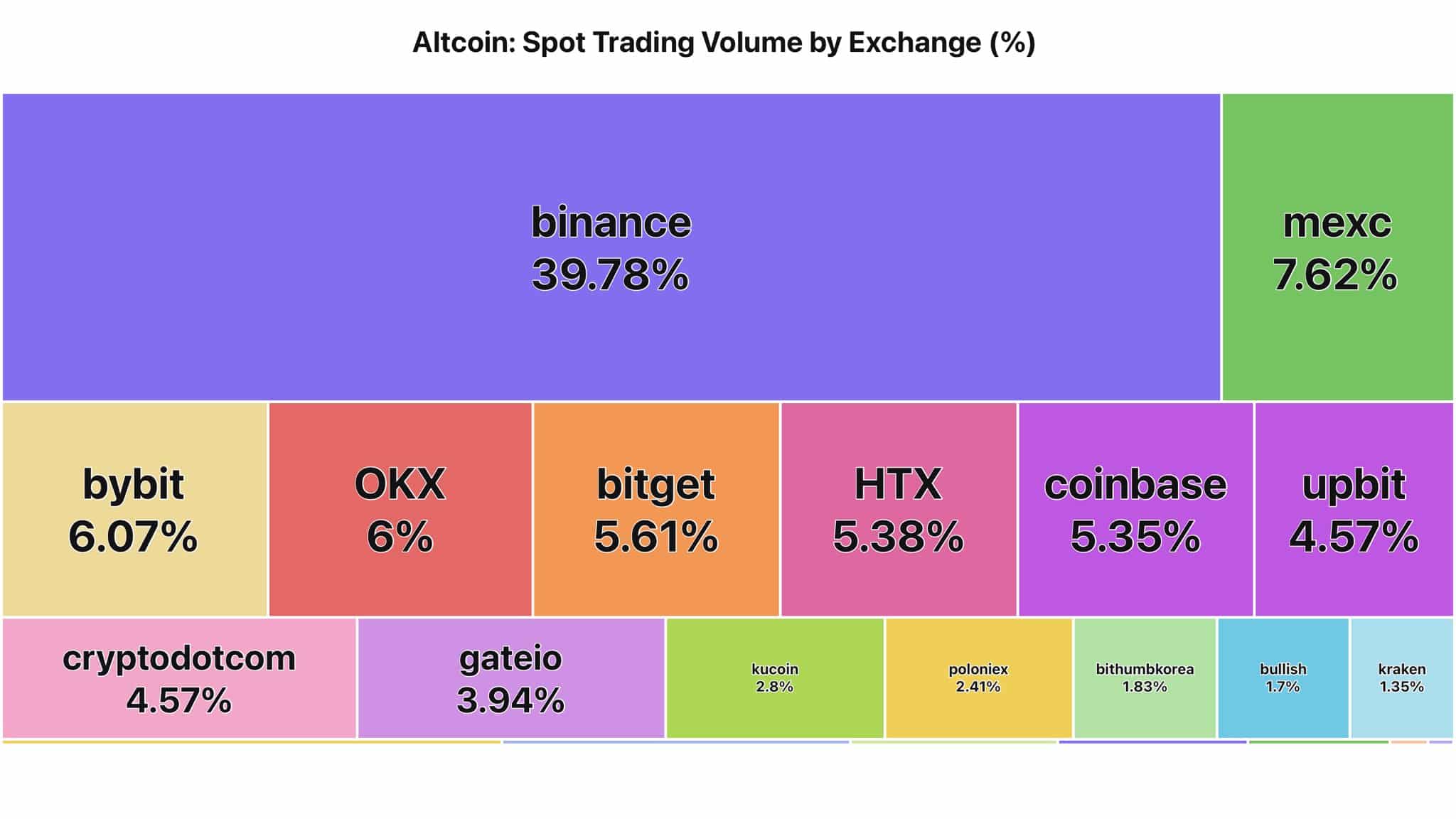

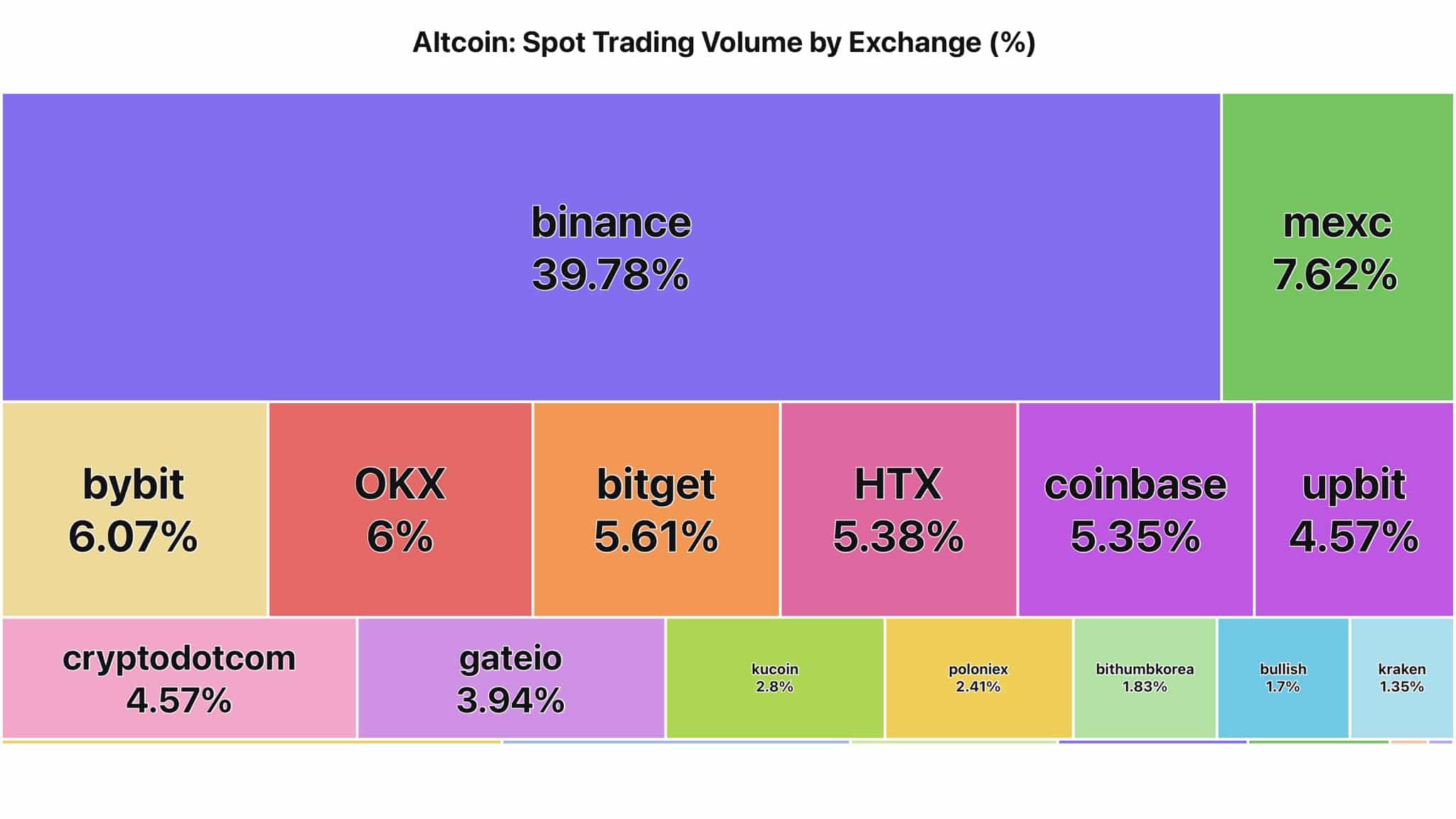

In relative terms, Binance holds nearly a 40% share right now, with the same rising as overall participation shrinks. Earlier peaks in February and October 2025 saw volumes surge to $40–50 billion on Binance and up to $91 billion elsewhere, marking periods of strong demand.

As volumes fall across all venues, participation weakens across pairs and trade sizes, pointing to reduced risk appetite.

However, this also means capital is stepping back rather than exiting entirely. As engagement compresses, volatility often declines, although such phases can precede renewed positioning once sentiment stabilizes and liquidity begins returning.