Author: Shower Thoughts

Compilation: Deep Chao TechFlow

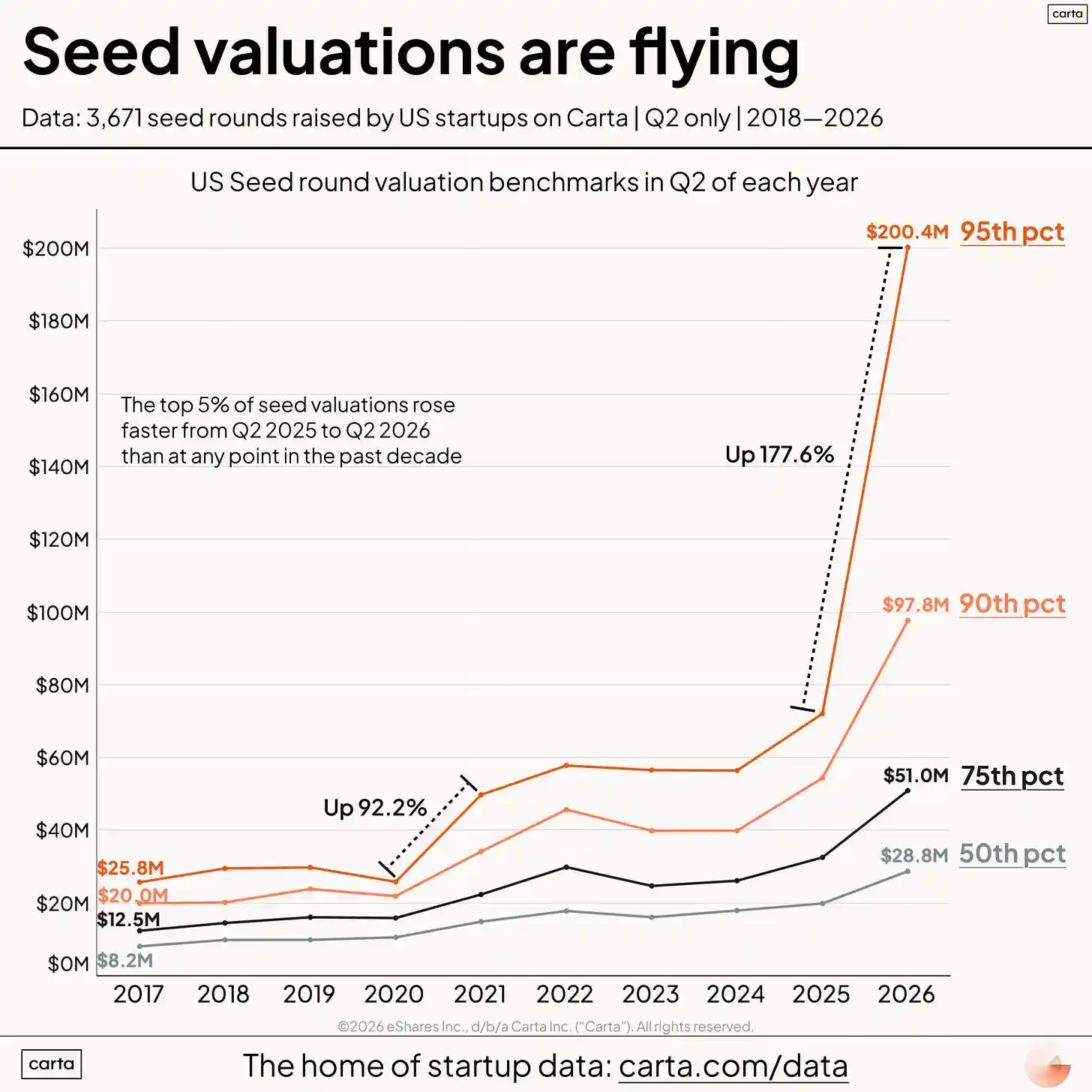

Deep Chao Guide: Silicon Valley is shifting from meritocracy to connections-based favoritism. Founders with Stanford backgrounds raise funds effortlessly, VCs preemptively invest $50 million in 'centrally cast' teams to create hype, while truly capable outsiders struggle to raise capital. This approach may work short-term, but ultimately, it will lose to the underestimated outliers—those who follow the herd are waiting to be slaughtered.

Peter Thiel often asks variations of this question: "In a given environment, what is it that you cannot say?" In the evangelical-dominated South, it's dangerous to be gay or liberal. On university campuses, it's dangerous to be conservative.

In Silicon Valley, the unassailable dogma is meritocracy.

Silicon Valley has long prided itself on meritocracy. Outsiders with no background or connections could emerge, build generational companies, and be rewarded for it. The industry has always been proud of being 2,851 miles away from Washington D.C.—a place notorious for getting things done through lobbying and insider connections.

Today, success in Silicon Valley depends on who you know and how willing they are to prop you up.

This is no different from how any other old-money industry operates. In East Coast high finance, you need the right elite school. In British politics, you need the right family surname.

How did Silicon Valley go from meritocracy to king-making?

Consensus Groupthink

It's no secret that Silicon Valley thinking has become extremely consensus-driven in recent years. This is mainly due to 1) AI distorting growth expectations, 2) LP capital concentration, and 3) the professionalization of the venture capital industry.

First, AI has completely distorted expectations for revenue growth. For the first time in history, we're seeing startups go from $0 to $100 million ARR in one to two years. Compared to the SaaS era, sustained three-year growth would get your company to an IPO. Even more extreme is growth on the scale of Anthropic—from $9 billion ARR in December 2025 to $47 billion ARR by May 2026 (adding up the annual revenues of Palantir, Snowflake, and CoreWeave along the way), which is unprecedented.

Well-known VCs now say never invest in diamonds in the rough. Either wait for an inflection point and try to get into the hottest companies, or try to pattern-match past successes and back a new company early. The former is the right strategy for growth-stage investing; the latter is a mistake. I'll explain why later and how this affects founders.

Second, LP capital has concentrated into the hands of a few established multi-stage franchise funds. In the first half of last year, 12 VCs took 50% of all LP capital. This is largely a reaction to over-allocation to the venture asset class in 2021-2022 and a flight to "quality" brand names that institutional allocators don't have to risk their careers defending in IC meetings. Family office LPs, in particular, are especially keen on getting into hot Silicon Valley companies, regardless of valuation. If a VC fund must pay a high price for a tiny stake in a hot company to secure LP capital, then so be it.

Third, the culture of the VC industry has shifted from a boutique craft to a mature career path. Over a decade ago, venture capital was a craft. Like a medieval guild, VCs followed an apprenticeship model, where seasoned GPs trained young junior VCs to develop the taste for judging founder quality and the feel for market timing.

Over time, the VC industry has professionalized into another standard career path. Previously, it was 2 years of investment banking → 2 years of business school → private equity. Now it's 2 years at a big tech company → 2 years at a high-growth startup → venture capital. Once there's a standard career path, it attracts excellent sheep NPCs who follow the herd, rather than the intensely independent thinkers the industry relies on to make contrarian bets.

Given that IPO timelines are longer than ever, thus extending feedback cycles, getting into hot companies (not necessarily the best companies!) is a better strategy for promotion within a VC firm. Mid-level VCs would rather quickly and easily get markups from safe consensus bets than risk betting on a potential fund returner. Large VC firms also have higher turnover than ever, so they might not even be at the firm in a few years to get carry on that fund-returning deal.

Consensus Money Attracts Consensus Founders

One would think the typical startup founder is an intensely non-conformist rebel, carving their own path in the world, who doesn't care at all what the establishment thinks. These founders are often polarizing to their peers, ignore their boss's instructions, and would be fired from structured corporate jobs. But that's less the case now.

Starting a company is becoming a more standard career option, no different from big tech or consulting. A contributing factor is the high unemployment rate for new college graduates looking for entry-level white-collar jobs, which are shrinking due to AI. Instead of struggling in the job search, apply to a startup accelerator, treat it like an internship program, burn through $500k, have fun, and figure out adult life.

The Stanford Review once wrote that YC is for cowards. With YC increasing from 2 batches a year to 4 (about 800 startups per year!), plus the explosion in the number of other accelerator programs, it's no surprise that the typical startup founder has become more uniform and less an unorthodox outlier.

Accelerators pressure startups to be legible to VCs by demo day, so startups naturally wandering through the idea maze trying to find product-market fit tend to build in the most obvious, crowded categories that already work. 81% of the current YC batch are doing AI for XYZ. Crypto startups are building new banks for stablecoins in XYZ region or prediction markets for XYZ niche. Consensus VCs fund these consensus ideas because they feel safe and familiar, easily pattern-matching to what already works. But the truth is the best companies define new categories and start years before that category is obvious or even has a name.

For founders not going through accelerators, a good background is more important than ever. Anyone who went to Stanford can raise money. Anyone spinning out of OpenAI can raise money. Check size and valuation are a function of how good the pedigree is and how well-connected the founder is within VC circles.

Beyond that, large multi-stage funds are giving a set of centrally cast characters (i.e., those with the best pedigrees) war chests of $10 million to $50 million to crown a category before their company has traction, making it hard for others who aren't centrally cast to win those markets.

So now it's not "Can you build a great business?" but "Can you fit the mold that large VC firms want to fund?"

An insular inner circle of soul-less individuals—those with background and connections getting preferential treatment—goes against the meritocratic idea that any skilled, hardworking entrepreneur can win. Meritocracy historically gave Silicon Valley its halo, the only place in America where the American Dream still exists and works. Today, Silicon Valley is becoming more like Wall Street or K Street.

Founders outside the network now feel they have to play "the game" to become one of the centrally cast. This means schmoozing with VC associates at happy hours and dinners, acting slightly autistic to create FOMO and fundraising momentum. Normally, founders networking with VCs is a waste of time; they should be focused on building the company and talking to customers. Now it's all part of the game, an extra skill founders must cultivate.

Downstream Effects of King-Making

To be fair, king-making does work to some extent. Raising massive capital gives you a huge war chest to acquire customers at a loss (i.e., unprofitably until your competitors go bankrupt or pivot). It scares other teams away from entering your market.

However, king-making also creates moral hazard for bad behavior. Companies get ~creative~ in reporting revenue, and founders sell secondary shares early.

King-making pressures companies to show revenue growth at all costs to be legible to VCs. This leads some companies to outright fabricate revenue (securities fraud) or get creative with methodologies. One example is taking a one-off contract and annualizing it into ARR. These contracts are often just pilot pricing with exit clauses, so they are ironically neither "annual," "recurring," nor even "revenue." Another example is rebranding ARR from "annual recurring revenue" to "annual run rate" and calculating ARR as last week's revenue × 52 or even last day's revenue × 365. This isn't exactly securities fraud, but it doesn't look good to anyone doing diligence.

VCs trying to king-make a competitive round often allow founders to sell secondary shares to win the deal. Apparently, 10% of a hot company's round going to founder secondary shares is now common practice. The downstream effect of founder secondary shares is that it attracts scammers. Those who can play the "game" described earlier well to create VC FOMO for a Series A and use it to sell millions in founder secondary shares (often more than the company's lifetime revenue) and then slowly rug.

Mean Reversion

The pendulum has swung too far toward consensus today, and I bet there will be a mean reversion toward contrarian thinking.

History repeatedly shows that the hottest theme in any given year is not the category of the most valuable company founded that year. I have no reason to believe this time will be different.

I'd rather back outsiders with chips on their shoulders 24/7 than insiders prematurely crowned by VCs. I believe there's a huge blind spot outside the Silicon Valley groupthink bubble—great founders without backgrounds, outside the distribution, illegible to most VCs.

I'm optimistic that meritocracy will ultimately win, and those chasing momentum playing the king-making game will be left licking their wounds.

Those who follow the herd are waiting to be slaughtered.