Original | Odaily Planet Daily(@OdailyChina)

Author | Azuma(@Azuma_eth)

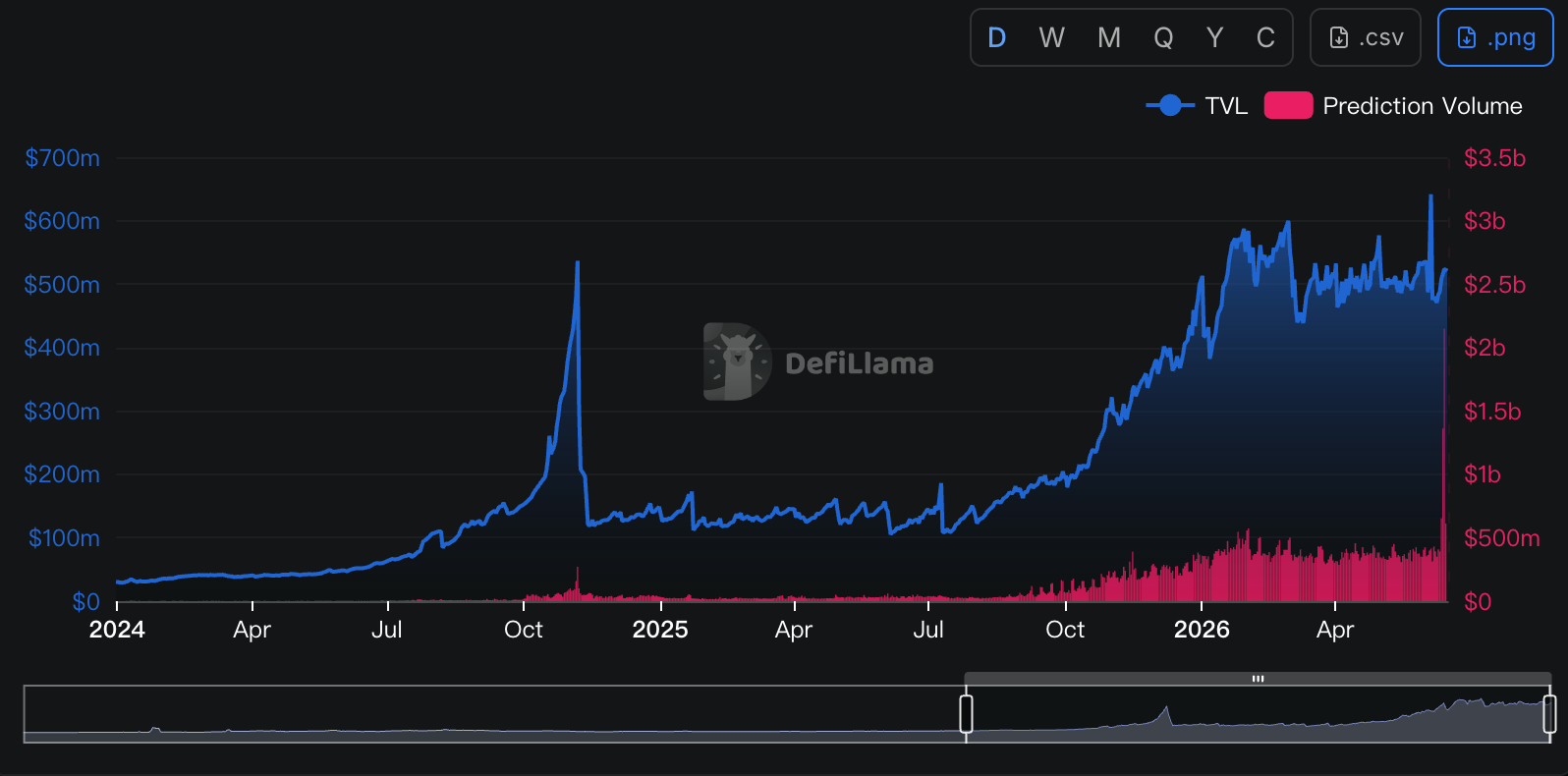

The fires of the World Cup have been lit, and the total trading volume across prediction markets continues to hit new highs. However, as the industry leader, Kalshi might not be in the best mood right now.

The reason isn't due to fluctuations in Kalshi's own business data, but because a formidable new rival has "suddenly" appeared in front of Kalshi, following Polymarket. This opponent was once Kalshi's most important ally.

- Odaily Note: Data sourced from Defillama.

Kalshi's Most Crucial Traffic Channel — Robinhood

Let's turn the clock back to March 2025. At that time, Kalshi announced a partnership with the U.S. online brokerage Robinhood. The latter would leverage Kalshi to offer its users prediction market trading services, allowing users to place bets on events like politics, economics, and sports.

From a business model perspective, this was a typical case of "mutual benefit" — Robinhood, responsible for user access and trade distribution, could directly use Kalshi's mature product. Kalshi, responsible for the underlying market, matching, clearing, and regulatory compliance system, could access Robinhood's massive pool of retail user traffic.

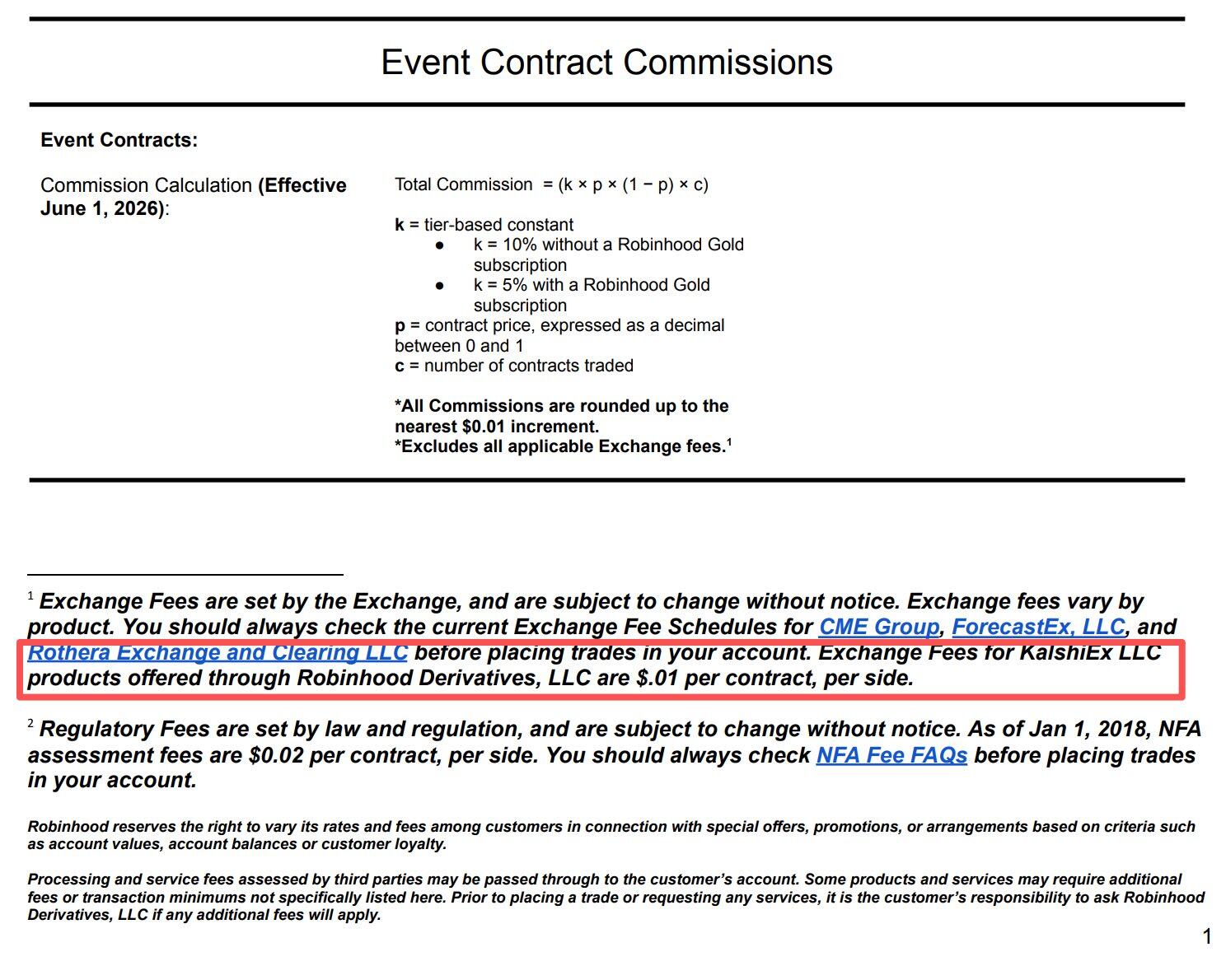

The subsequent story proved the "win-win" outcome of this collaboration. Through Robinhood's distribution channel, Kalshi indirectly gained vast amounts of users and trading volume. Piper Sandler analysts estimated that "trading volume completed through the Robinhood channel accounted for about 25%-35% of Kalshi's total trading volume." These orders ultimately translated into revenue on both parties' ledgers — Robinhood independently charged for all Kalshi event contracts traded through its channel, $0.01 per contract per side, before sharing profits with Kalshi (the specific split was not disclosed).

The Q1 financial report disclosed at the end of April this year showed that Robinhood transacted 8.8 billion event contracts in Q1, driving "other transaction revenue" to increase 320% year-over-year, reaching $147 million. Prediction markets had become the brightest growth engine in Robinhood's product line.

But recently, this relationship has undergone some subtle changes.

Robinhood's Ambition: Reclaiming the Cake Shared with Kalshi

As internet history has proven countless times, when a distribution channel gains enough clout, it is no longer satisfied with being just a channel. Robinhood is no exception.

Although the partnership with Kalshi also brought Robinhood considerable revenue, as prediction markets became one of the fastest-growing new businesses on the platform, Robinhood was no longer content with the current profit-sharing arrangement.

In the partnership model, Kalshi provided the market and infrastructure, while Robinhood provided the users and order flow. However, as the collaboration deepened, Robinhood gradually realized that what might truly be scarce was not the market itself, but the user entry point it firmly controlled. After all, for most Robinhood users, they don't care whether orders are ultimately filled on Kalshi or another platform — users only see a trading entry point within the Robinhood app, not the underlying infrastructure provider.

In other words, Robinhood always controlled one of the most important resources for a prediction market — distribution capability. If the users belonged to itself, then why should the order flow go to someone else?

In fact, while Robinhood was rapidly validating the demand for prediction markets through Kalshi, another Plan B was quietly launched shortly after.

In November 2025, Robinhood announced the formation of a joint venture with Wall Street quantitative trading giant Susquehanna and planned to acquire the CFTC-regulated derivatives exchange MIAXdx. According to the official statement, the joint venture would operate an independent futures and derivatives exchange and clearinghouse in the future, with prediction markets being one of its key focuses. At the time, the outside world mostly viewed it as an infrastructure investment. However, as more information was disclosed later, people gradually realized that Robinhood's ambition far exceeded merely finding a new partner for prediction markets.

In January 2026, the deal was officially completed. Robinhood and Susquehanna gained 90% control of MIAXdx, along with a complete CFTC regulatory framework, including Designated Contract Market (DCM) and Derivatives Clearing Organization (DCO) licenses. Subsequently, MIAXdx was renamed Rothera Exchange, and its clearinghouse was renamed Rothera Clearing.

At this point, Robinhood already possessed the core elements required to independently operate a prediction market. What was missing was only a mature product comparable to Kalshi's, but for Robinhood with its rich internet product development experience, this was clearly not a challenge.

Rothera's Opportunity: The World Cup

In June 2026, after about half a year of accelerated development, the Rothera product began to take shape. Robinhood finally made the move that seemed almost inevitable — gradually shifting the order flow that originally went to Kalshi into its own controlled system.

Robinhood specifically chose an excellent debut battlefield for Rothera — the World Cup. For prediction markets, the World Cup is undoubtedly one of the most traffic-generating trading themes. Whether it's match outcomes, advancement results, or the final champion, related markets can attract a large number of new users to trade in a short time. For the new Rothera platform just starting up, there's no better scenario than the World Cup for a cold launch.

According to Robinhood's official disclosure, during this World Cup, which consists of 104 matches, some event contracts would be directed to Rothera for matching and clearing. These include markets for individual World Cup match results, the ultimate World Cup champion, and total goals in single matches. Compared to the previous model that relied entirely on Kalshi, this marked the first time Robinhood would import prediction market orders into its own trading system on a large scale.

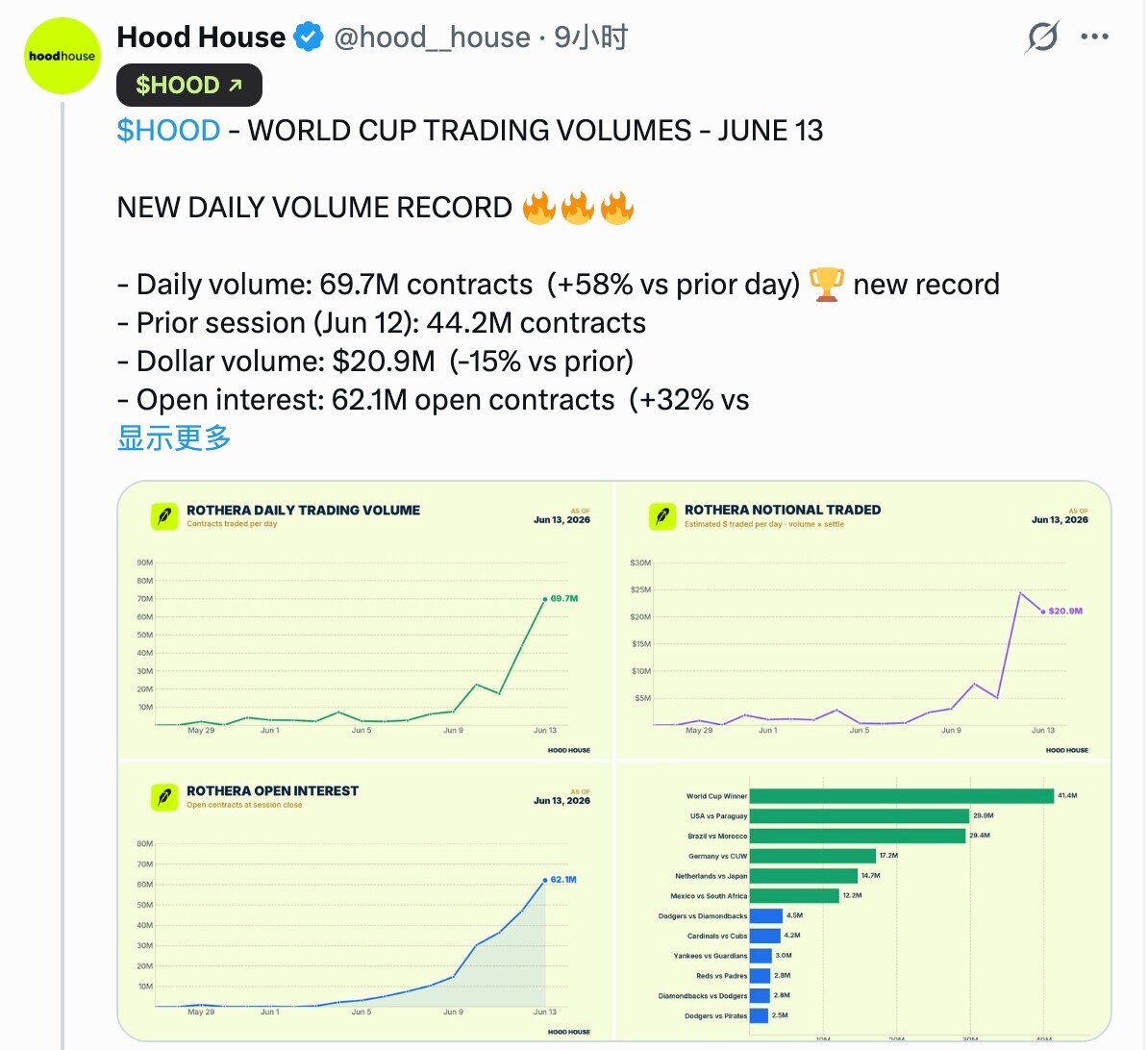

Judging by the results, Rothera clearly seized this opportunity. According to data disclosed by Hood House, a research-focused media outlet tracking Robinhood dynamics, on June 12, Rothera transacted 44.2 million contracts, corresponding to a dollar trading volume of approximately $24.4 million. On June 13, Rothera transacted 69.7 million contracts, corresponding to a dollar trading volume of approximately $20.9 million... Although these figures still have a gap compared to Kalshi's hot markets with billions of dollars in trading volume, considering that Rothera had literally just launched a few days prior, this performance data is already sufficiently successful.

For both Robinhood and Kalshi, this indicates that the balance in their collaboration has begun to tilt. From Robinhood's perspective, the commission revenue that previously needed to be shared with Kalshi can now be retained within its own ecosystem. From Kalshi's perspective, this means that one of its most important growth engines is starting to show signs of weakening.

And the World Cup is clearly just the beginning of Rothera's encroachment on Kalshi. Looking further into the future, Robinhood is bound to expand Rothera's coverage to more sports events as well as economic and political themes. Those orders that originally flowed to Kalshi will be successively intercepted by Rothera.

Since Robinhood and Kalshi have never disclosed their profit-sharing ratio, we cannot know the exact value of this interception. However, considering that Robinhood alone generated $147 million in prediction market-related revenue in Q1, and the Q2 World Cup and the more distant midterm elections will likely bring larger-scale trading activity, the value of this interception could reach billions of dollars on an annual basis.

Who Controls Distribution, Controls Everything

The drama of Robinhood and Kalshi moving from allies to opponents once again illustrates a logic repeatedly proven in the internet market — products are easy to build, but traffic is hard to find; whoever controls distribution controls everything.

Over the past few years, the market generally believed that Kalshi's core moat came from regulatory licenses, exchange qualifications, and clearing capabilities. Therefore, whether it's brokerages like Robinhood or various media, communities, and traffic platforms, they were essentially just Kalshi's distribution channels and traffic inlets. However, the emergence of Rothera proves one thing: in an era of severe product homogenization, the product itself might not be the most important element. What remains truly scarce is always the user.

Where the users are, the liquidity is; where the liquidity is, the market will be. When Robinhood controls the entry point for tens of millions of retail users, it has full capability to direct these users to any trading venue. For users, they don't care whether orders are ultimately filled on Kalshi or Rothera. As long as the experience isn't significantly different, who handles the matching and clearing behind the scenes doesn't matter.

If the theme of the prediction market industry in the past few years was the market battle between Polymarket and Kalshi, then the theme for the coming years might become a channel war. Robinhood incubating Rothera is essentially a reverse integration initiated by the distribution side towards the market layer. As more and more platforms with traffic inlets begin to realize the strategic value of prediction markets, similar stories are highly likely to continue. Whether it's exchanges, brokerages, social platforms, or media platforms, any could become a new entry point for prediction markets.

And when inlets start to control the market, and channels begin to possess pricing power, the ultimate winner in the prediction market industry might no longer be the platform responsible for matching orders, but the one closest to the user, the one who can best control distribution.

This was true in the internet era, and also true in the mobile internet era. This time, it's no exception.