1. BTC rebound pressure is high

The short-term trend of BTC price is very weak, and the rebound strength is not high during the relative contraction of trading volume. Judging from this, the selling pressure generated during the rapid price drop on November 8 and 9 in the previous period was relatively large, which still limited the price increase. In addition, the volume effect of these two trading days is the highest in history. The 24-hour peak volume on November 8 and 9 reached more than twice the average volume in the recent three months. As a result, more investors' cost of holding coins fell within the range of 15588 to 20600 dollars. It is necessary to break through this price range. At present, the trading volume is shrinking and the rebound is more difficult.

2. Increase in turnover of BTC long-term investors

From the performance of the number of destroyed currency days, the number of destroyed currency days on November 16 rebounded again, reaching a high of 35.27 million. According to this judgment, there is still room for a rebound in the turnover rate of long-term investors in the near future, and the cumulative BTC turnover rate is rising. Long term investors change hands with BTC, which means that their currency holdings are still in an obvious loose state, which is unfavorable for BTC's short-term stability. At present, BTC is at the bottom of the horizontal market. Although it has the cost advantage of low absorption, it is unlikely to make profits after buying in the near future.

3. ETH price performance is low

After the fall of ETH's early classification, the recent trading volume is still in a shrinking state, and the volume and price performance are sluggish, which means that there is little room for ETH to achieve growth in the near future. On November 10, the ETH price reached a minimum of $1073. Therefore, after the technical rebound, ETH may retest the support effect of this point. US $1106 is also the support level for 78.6% of Fibonacci, so investors should pay special attention to trading signals.

4. AXS rebounds strongly

Recently, the price shock of AXS has increased significantly. On November 13, the price fluctuation amplitude of AXS reached 232%, and the highest price hit $19.12. If we calculate from the closing price of $6.52 on November 12, AXS's short-term increase is as high as 293%. Judging from this, AXS's market performance is exceptionally strong, but the profitability of short-term trading is unlikely. As AXS's short-term rise was completed during the period of rising and falling, the main rise and fall process lasted only one hour. From the perspective of the main force holding money, it may be a means for the main force to save itself.

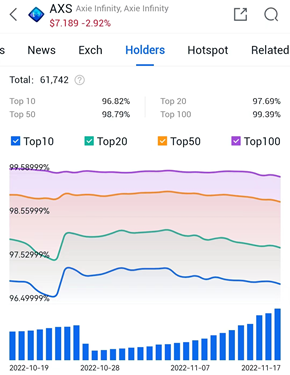

5. AXS's main currency holding rebounded and fell back

From the perspective of the number of coins held by AXS, the top 10 coins held have a large fluctuation space. As early as October 23 to October 25, the proportion of AXS held by the top 10 major holders of coins rose from 96.5% to 97.24%, and the number of coins held could be 0.74 percentage points higher. Next, AXS's currency holding has little room for fluctuation. On November 12, 96.91% of AXS held by the top 10 players of AXS was higher than that on October 23. According to this judgment, 232% of the AXS strong earthquake on November 13 may be caused by the main trading. After all, AXS's closing price on November 12 contracted by more than 40% from the previous high.

Similar short-term self-help actions of the main players will occur, but in the process of confirming the bottom of the mainstream currency recently, the rebound expectation is not high, so pay attention to the risk of catching up.