Author: Chloe, ChainCatcher

According to a Bloomberg report, digital bank Erebor, initiated by Anduril founder Palmer Luckey and backed by billionaire investor Peter Thiel, is in talks with investors for a new round of financing, targeting a valuation of at least $8 billion, roughly double its December 2025 round ($350 million raised, $4.35 billion valuation). The financing is still in early stages, with the valuation not yet finalized. An Erebor spokesperson declined to comment on the negotiations.

A bank that has only been operating for a few months, doubling its valuation, stands as one of the highest valuation increases among newly licensed U.S. banks in recent years. What likely makes investors willing to reprice it is the expansion speed revealed in its financial reports.

What Potential Do Investors See in the Financials?

According to sources familiar with the matter, Erebor's deposit base surged from $1.1 billion disclosed to regulators at the end of March to approximately $4.05 billion within three months, nearly quadrupling in a single quarter. It also added nearly 400 new clients, with the bank expecting to become profitable by the end of 2026.

This growth rate has also sparked external skepticism—whether Erebor's ties to Silicon Valley tech circles and government/defense circles are too close, raising suspicions of a "friends and family" game.

Luckey responded directly, emphasizing that none of the quarterly growth came from his own companies, and new clients independently chose Erebor. He added that a significant portion of the recent expansion focused on companies rebuilding U.S. manufacturing capacity, and the bank has correspondingly expanded equipment financing, venture debt, and credit businesses supporting industrial and defense enterprises.

Looking back at the Q1 financials, Erebor's total assets were $1.703 billion, deposits $1.098 billion, and bank equity $600.6 million. There were no loans, leases, or borrowings other than deposits (items like federal funds purchased, repurchase agreements, other borrowed money, subordinated debt were all zero). The asset structure was extremely liquid: approximately $1.411 billion in cash and due from banks, and about $275 million in available-for-sale debt and equity securities (of which bonds $116 million, equity securities $159 million).

Additionally, quarterly net interest income was only $3.36 million, non-interest expenses were $10.56 million, resulting in a net loss of $6.01 million. However, for a newly launched bank still amortizing technology, compliance, and operational costs, such losses are considered necessary expenditures.

In other words, investors are willing to pay an $8 billion valuation not for Erebor's current monetization potential, but for its growth speed—deposits surging from $1.1 billion to $4.05 billion—and the expectation that it will eventually lend out these deposits and develop stablecoin business.

Founder Unfamiliar with Wall Street, Yet Comes with Considerable Pedigree

To understand Erebor, one must first understand the recurring product-building pattern behind it.

Founder Palmer Luckey's trajectory spans Oculus VR and Anduril, consistently focusing on capital-intensive industries at the intersection of hardware, regulatory moats, and government-adjacent ecosystems. In 2012, he entered the not-yet-formed VR market, solving long-standing industry issues like latency and spatial tracking, selling Oculus to Facebook for $2 billion in 2014. His second venture, Anduril, applied the same playbook to the defense industry: using private venture capital to build defense systems first, then selling them to the government as "products" rather than through traditional "cost-plus" contracts, thereby building deep relationships with the Department of Defense and intelligence agencies. Luckey explicitly stated that Erebor would "work with the intelligence community from day one" to prevent fraud, adopting a proactive compliance posture.

However, Luckey himself is an outsider to banking. Erebor's brand partly relies on his and Thiel's reputations, but prestige ultimately cannot replace regulatory and operational track records. Once entering Wall Street, the bank will ultimately be judged by the standards of a regulated institution.

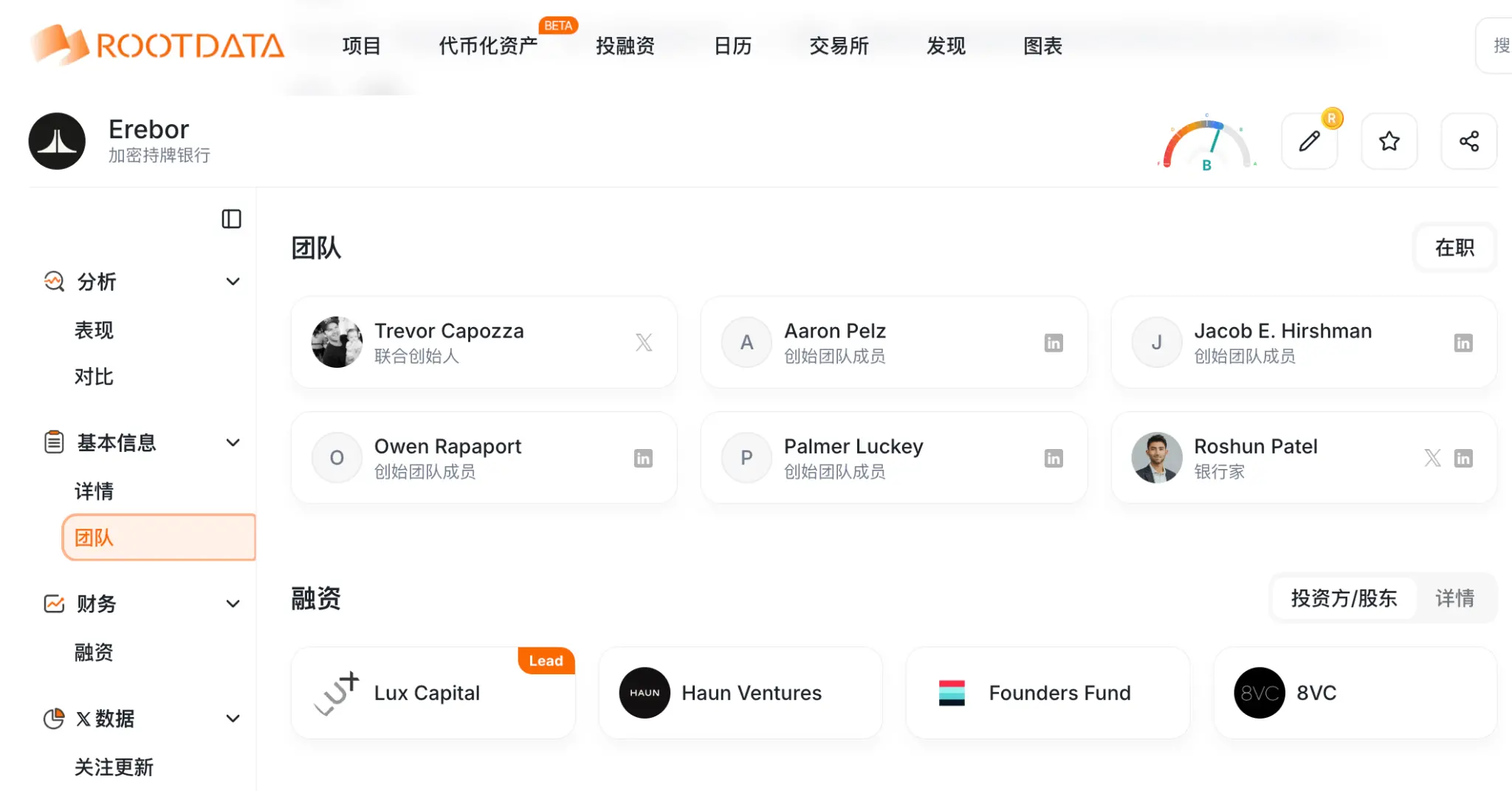

Therefore, the real operators are a team with deep financial backgrounds: President Michael Hagedorn from Wells Fargo's regional banking; CEO Owen Rapaport with crypto compliance experience through Aer Compliance; Chief Strategy Officer Jacob Hirshman, who worked on Circle's stablecoin business and practiced at Sullivan & Cromwell; Growth VP Noah Pompan with a background at MoonPay. The investor lineup includes Joe Lonsdale's 8VC, Thiel's Founders Fund, Lux Capital, and a fund associated with a16z.

Image Source:RootData

Furthermore, a key strategic choice for Erebor is: insisting on obtaining its own license and being responsible for its financials, unlike Mercury or Brex which rely on partner banks. Luckey's argument is that relying on third-party infrastructure exposes one to risks of "de-platforming," policy pressure, and product limitations; only by holding the license and ledger can it fulfill promises of on-chain settlement, stablecoin minting, and redemption.

Looking back at Erebor's origin, it is almost entirely tied to the collapse of Silicon Valley Bank (SVB) in 2023. That failure left a large number of startups and venture capitalists suddenly without banking partners and deposit protection. Luckey and investors believed this left a "structural vacuum"—the disappearance of banks specializing in serving startups, while traditional banks were too conservative or slow for startups holding non-standard assets (defense contracts, AI hardware, digital tokens).

Erebor claims to address roughly four pain points: First, providing credit for physical assets—traditional banks are good at lending against real estate or receivables but not at valuing "GPUs" or "aerospace research." Second, bridging the on-chain/off-chain divide, bringing fiat banking and stablecoin settlement onto the same regulated balance sheet. Third, meeting 24/7 settlement needs, replacing SWIFT and ACH still operating on decades-old schedules. Fourth, providing USD access for high-growth international companies, combating the "de-banking" friction they often face.

Of course, how much of this operational potential is real versus marketing remains debatable. Venture-backed companies now have alternatives like non-bank lenders and DeFi lending, and some incumbent banks had already started targeting tech niches before SVB's collapse. Erebor's founders clearly believe existing institutions are insufficient, and the fact that it obtained a full banking license suggests regulators might also see some merit in this assessment?

Additionally, digital assets are core to Erebor's long-term strategy. It plans to handle deposits and payments for dollar stablecoins, provide instant fiat/stablecoin conversion, 24/7 settlement rails, and gradually support stablecoin minting and redemption within a regulated framework. Its OCC license even explicitly allows it to hold small amounts of crypto assets on its own books to pay for on-chain transaction fees, with supervisory letters defining such holdings as "incidental" to banking business—a noteworthy precedent in compliance.

On April 2nd, the Sui Foundation announced that Erebor now supports the Sui network, allowing clients to deposit and withdraw stablecoins. This is one of the first public pieces of evidence of it connecting regulated bank infrastructure to on-chain payments.

However, reality also presents gaps. Sources indicate demand for crypto-collateralized loans has been lower than the bank initially expected. This aligns with the earlier financials: the recent growth has actually been driven by companies rebuilding U.S. manufacturing capacity and their equipment financing and venture debt needs. In other words, Erebor currently resembles more of a "defense + advanced manufacturing + crypto" hybrid than a purely native crypto bank.

Perfect Timing—Even Its License Application Timing Was Fortuitous?

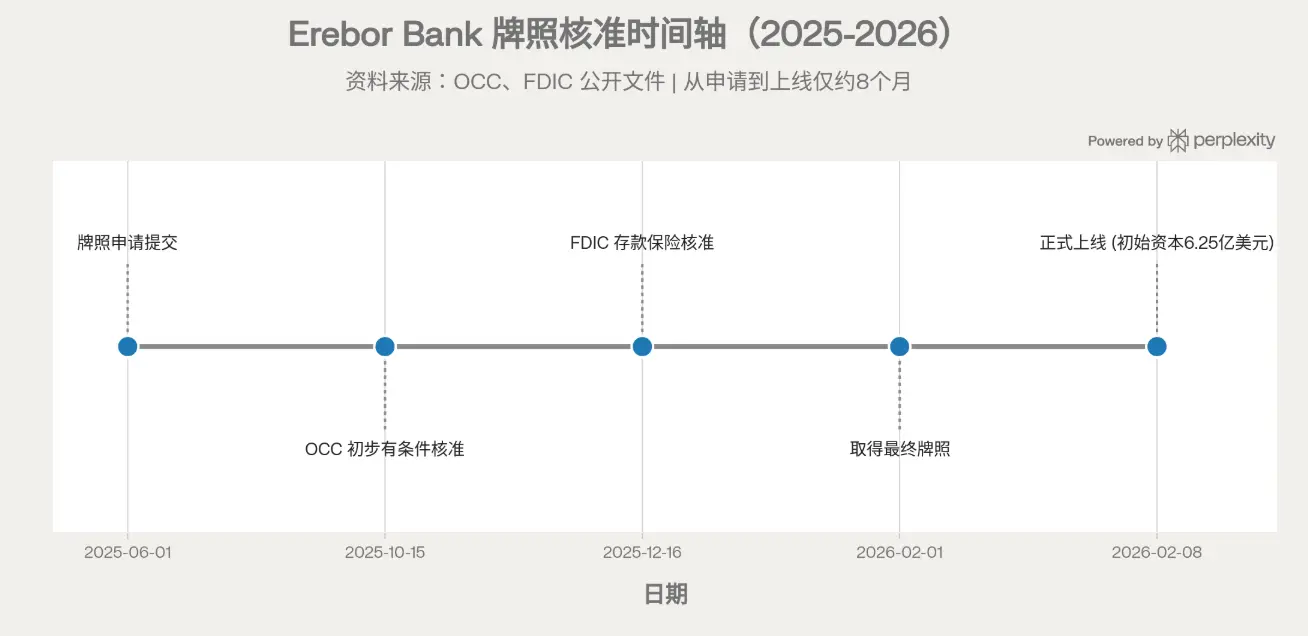

Breaking down the licensing: Erebor received preliminary conditional approval from the OCC on October 15, 2025, FDIC deposit insurance approval on December 16, final license in early February 2026, and officially launched on February 8 with approximately $625 million in initial capital (significantly increased from about $275 million during the preliminary approval phase). It is the first newly issued (de novo) national bank charter under the current U.S. administration.

All this occurred against the backdrop of a clear shift in U.S. banking policy: Under the leadership of Acting Comptroller Jonathan Gould, the OCC has adopted an explicitly open regulatory stance toward digital asset banks, with Gould himself hailing this license as an example of a "dynamic and diverse financial system"; coupled with the advancement of federal-level stablecoin framework (GENIUS Act), once-fuzzy legal territories have been clarified considerably.

Notably, regulators did not grant approval without conditions. In exchange for approval, the OCC and FDIC imposed strict requirements: maintaining a Tier 1 leverage ratio of at least 12% for the first three years (roughly double the "well-capitalized" threshold) and a capital maintenance commitment. It could be said that Erebor's feasibility is partly tied to the current political cycle. If future regulatory stances shift, or stablecoin and anti-money laundering rules tighten, its entire narrative built on "token-friendly rules" could face headwinds.

Finally, synthesizing external media judgments, Erebor's model replicates almost every risk that contributed to SVB's downfall.

It serves early-stage, tech-heavy companies with non-traditional collateral. It caters to a small number of large accounts (startups, founders, investment funds) rather than thousands of retail customers; any single client's failure or withdrawal (crypto market volatility, venture capital pullback) could significantly impact liquidity. Regulators have long pointed out that SVB's "monoculture" client structure was a key driver of its run.

Crypto correlation makes the issue more tricky. If a supported stablecoin de-pegs or crypto prices crash, the deposit base and loan collateral could shrink simultaneously. Further down are policy reversal risks (its entire narrative bets on lenient token rules), execution risks of building core systems and on-chain settlement from scratch, and the unverified premise of "whether stablecoins will be widely adopted by clients." Finally, reputational and political risks—Luckey's highly controversial political affiliations plus the novelty of a "crypto bank" itself could amplify market confidence loss if the bank ever faces trouble.

It could be said Erebor is a high-profile experiment happening at the intersection of banking, crypto, and industrial policy.

The market need it advocates emerged from the financing gap left by SVB's collapse and friction in crypto payments. Now, regulators have given paper endorsement, the team combines tech prestige with Wall Street backgrounds. The execution of this new model, the continuity of regulatory stances, and the genuine market demand for its integrated services are precisely the points under rigorous market scrutiny.