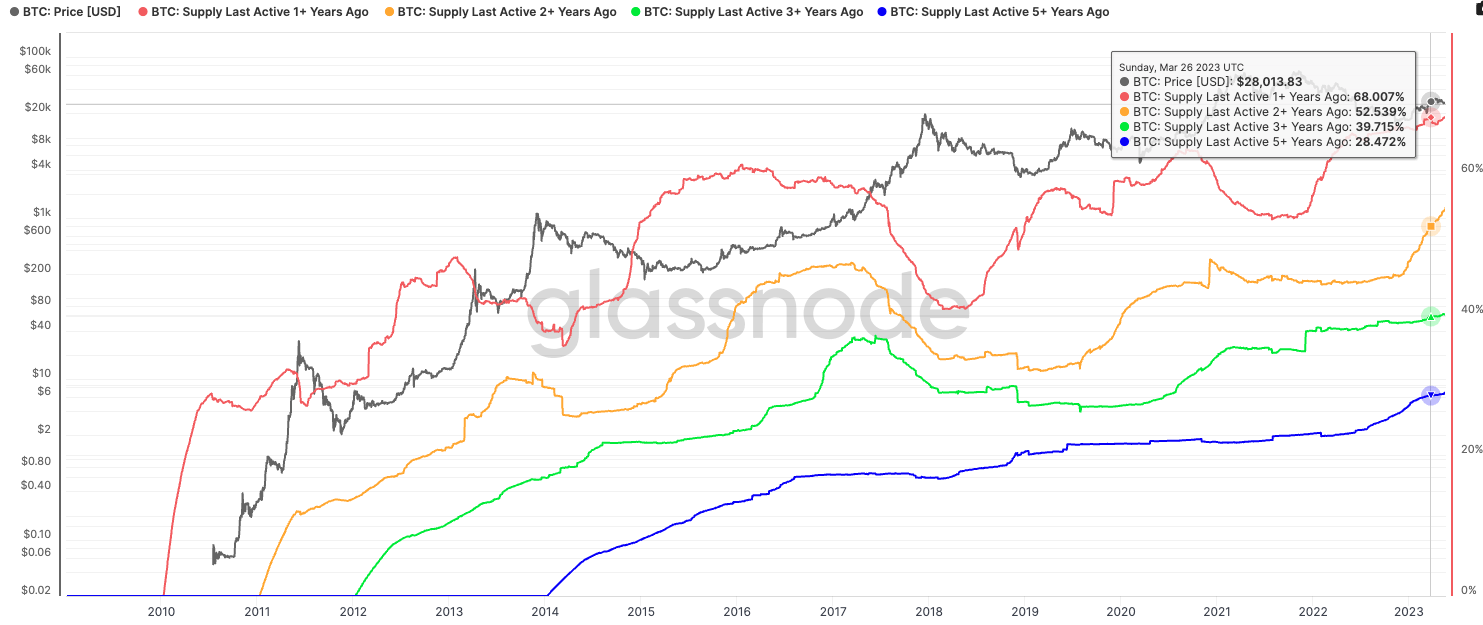

Investors are hanging onto their bitcoin (BTC) longer than ever – HODLing in industry parlance – according to data from Glassnode.

The proportion of BTC that’s been held for at least a year has climbed to a record 68%, Glassnode data shows, while 55% of bitcoin has been held for at least two years and 40% for three years.

Many analysts consider it bullish when BTC sits dormant on grounds that investors are choosing to hold on rather than sell. The prevalence of buy-and-hold in crypto contrasts with the long-term shift in U.S. stocks, a market where investors now hold assets for dramatically less time than they used to.

BTC: supply last active 1yr + age bands (Glassnode)

Sean Farrell, head of digital assets research at FundStrat, said that being a long-term holder has tended to get more popular over time. The exception is when markets get frothy and investors who bought dips sell their older coins to eager buyers.

“The trend is bullish insofar it means that higher prices are ahead in this cycle and any reticence to sell from current HODLers could result in a mini-supply squeeze,” said Farrell.

He added that looking at long-term holder supply metrics is not necessarily useful for short-term price signals.

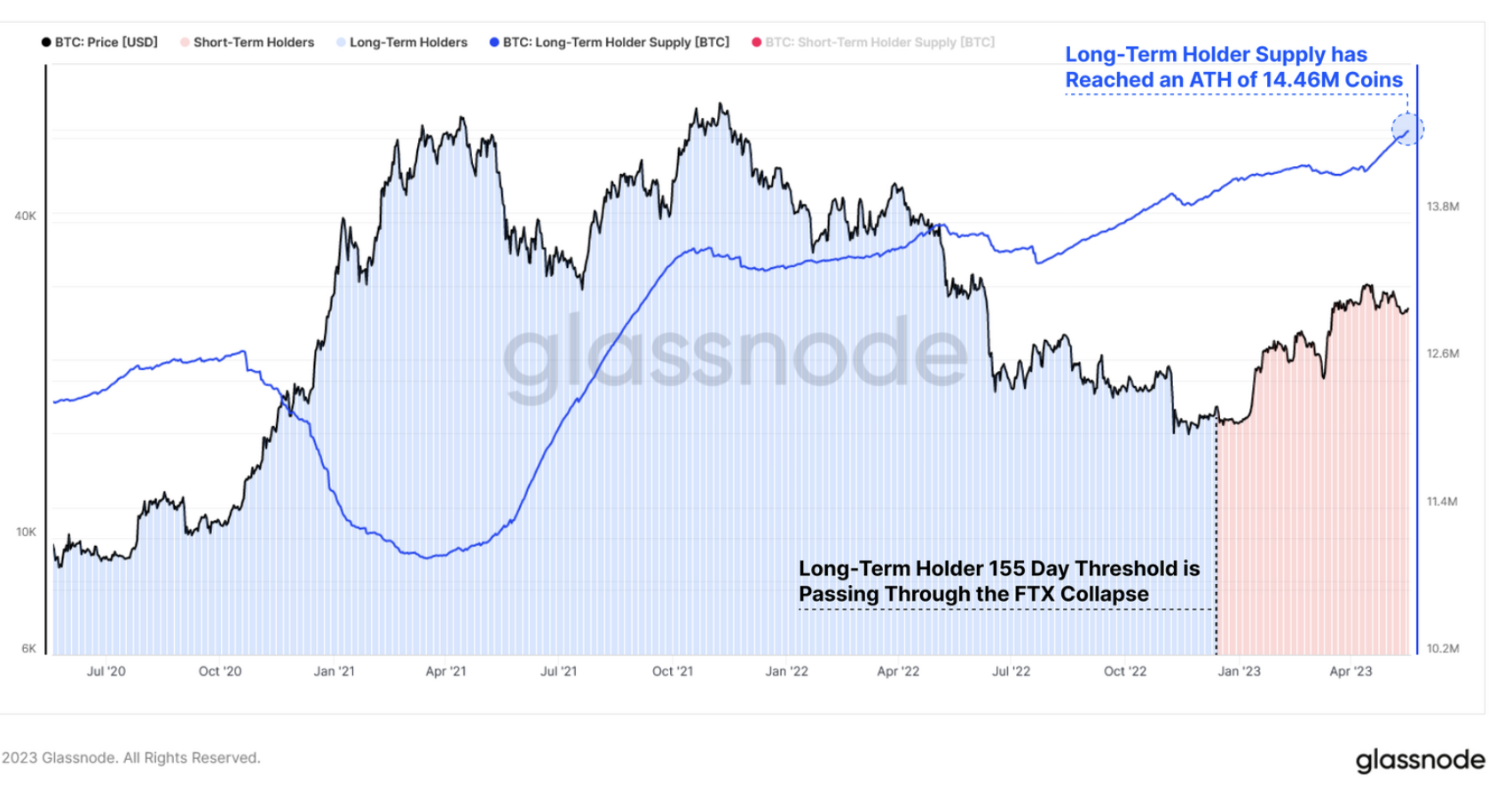

Long-Term-Holder Supply, which Glassnode deems as coins held for longer than 155 days, has also seen a new all-time high — reaching 14.46 million bitcoin. “This reflects coins acquired immediately after the FTX failure maturing into long term holder status,” said the report.

Bitcoin long term/short term holder threshold (Glassnode)

Glassnode’s Liveliness metric – which compares the relative balance between HODLing and spending behavior – also shows investors are hanging on. It has fallen to the lowest level since December 2020.