TAO, the native token to decentralized AI platform Bittensor, has more than doubled from its Q1 2026 low of $145 to over $320, at the time of writing. Some of the major bullish catalysts have been institutional interest via the Spot TAO ETF and the narrative of AI and crypto convergence.

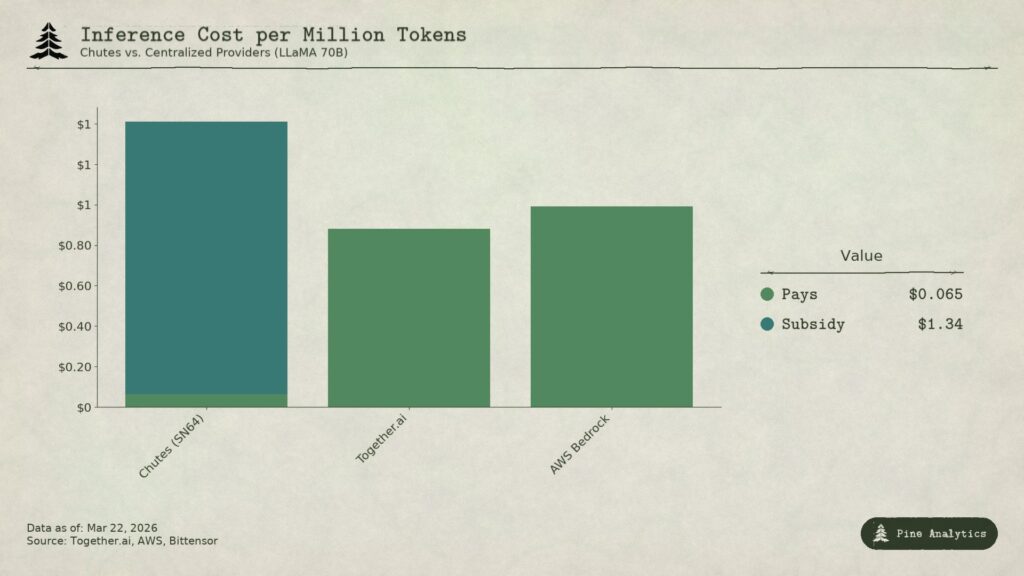

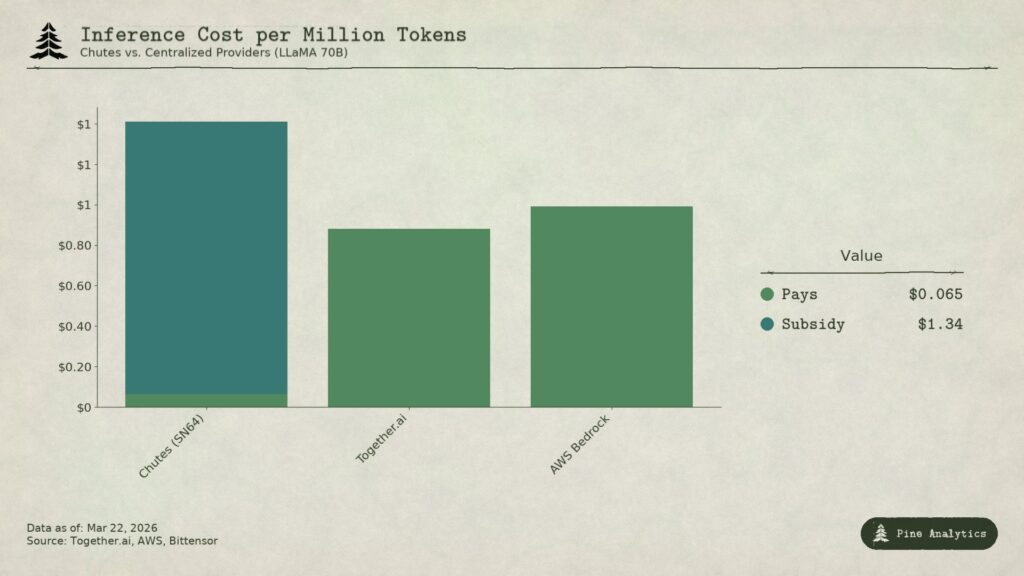

However, the chain’s fundamentals may be staring at a crisis that may force a rerating of the altcoin. According to crypto research firm Pine Analytics, most subnets (AI marketplaces) are heavily subsidized by token emissions, rather than by operational efficiency.

Without the subsidy, some of the top subnets, like Chutes (SN64), would be way more expensive than rival, centralized alternatives like Deepseek and Together AI. According to Pine Analytics,

An unsubsidized Chutes pricing would be 1.6-3.5x more expensive than centralized alternatives. The cost advantage does not narrow. It inverts entirely.

Will Bittensor’s model hold?

For perspective, each subnet serves as a self-contained system for a specific AI service, such as image generation or price prediction.

At the core of this ecosystem are miners and validators. Miners act as producers, aiming to achieve the subnet’s set tasks by running AI models and other activities. The higher the quality of the work, the greater the chance of receiving more TAO rewards.

Likewise, validators are paid through TAO rewards for their quality control or auditing work. They supervise miners’ work and score them accordingly.

Now, back to Bittensor top subnet Chutes. It gets 14.4% of emissions, annualized at $52 million (or 518 TAO per day). This is shared among the subnet creator, miners, and validators. However, there is no publicly available data on demand for these subnets, Pine Analytics noted.

However, the research firm warned that the model could fall apart if the subsidy is cut.

When emissions halve again (projected late 2026 or 2027), either pricing roughly doubles, miners leave the subnet, or the gap between subsidy and revenue widens further.

In other words, most of the Bittensor subnets could become expensive, leading them to hike prices for AI services. This could likely force users to seek cheaper alternatives. Consequently, such a scenario would also trigger miner and validator exits.

With no current verifiable demand for Bittensor, Pine Analytics called this an “income desert” thesis that could force a TAO rerating.

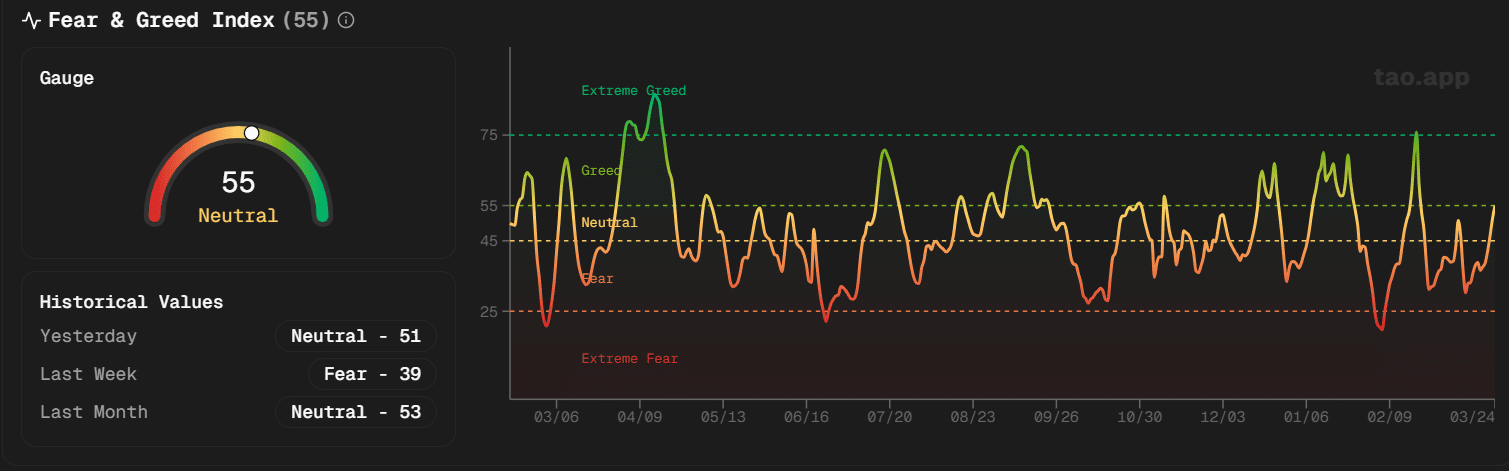

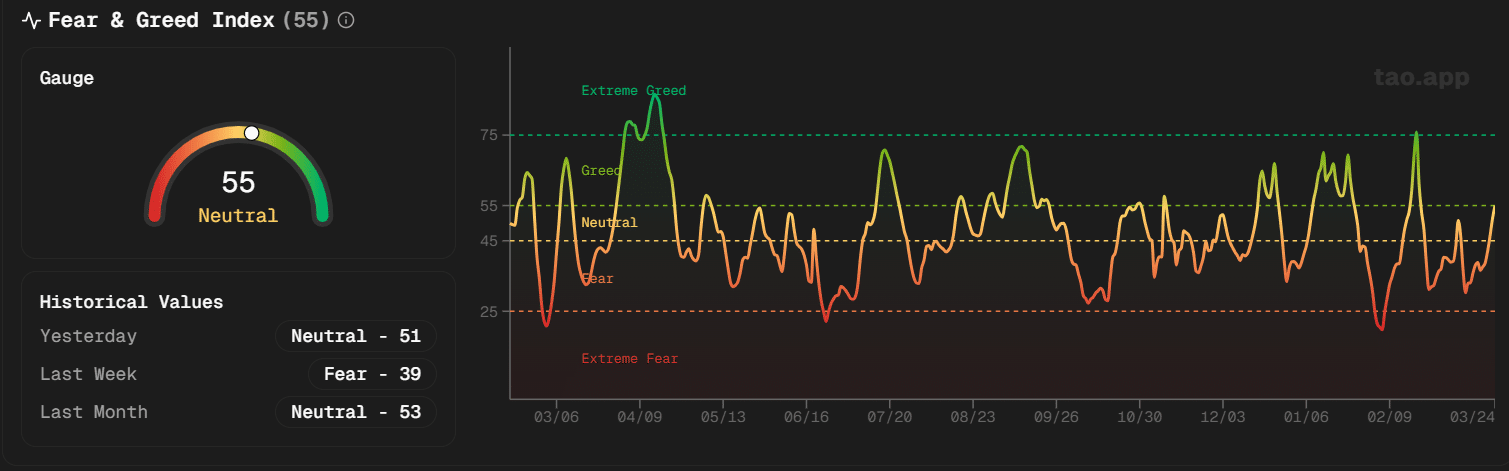

Despite the bearish call though, TAO’s market sentiment recovered to neutral at press time. Especially on the back of the altcoin climbing by 25% in just 24 hours. Overall, TAO was up nearly 130% from its February lows.

Final Summary

- Pine Analytics projected that Bittensor AI services relied more on subsidies than on real demand.

- Should the subsidies be cut in half later in 2026 or early 2027, the Bittensor model could face a massive reckoning.