Author: YQ

Compiled by: Saoirse, Foresight News

Since 2015, I have been deeply involved in scaling technology research, studying all iterative solutions from sharding, Plasma, App Chains to Rollup. I have in-depth collaborations with every mainstream Rollup tech stack and team in the ecosystem. Therefore, I always pay close attention when Vitalik publishes content that can fundamentally reshape our understanding of Layer2 (L2). The post he published on February 3rd is such a key piece of content.

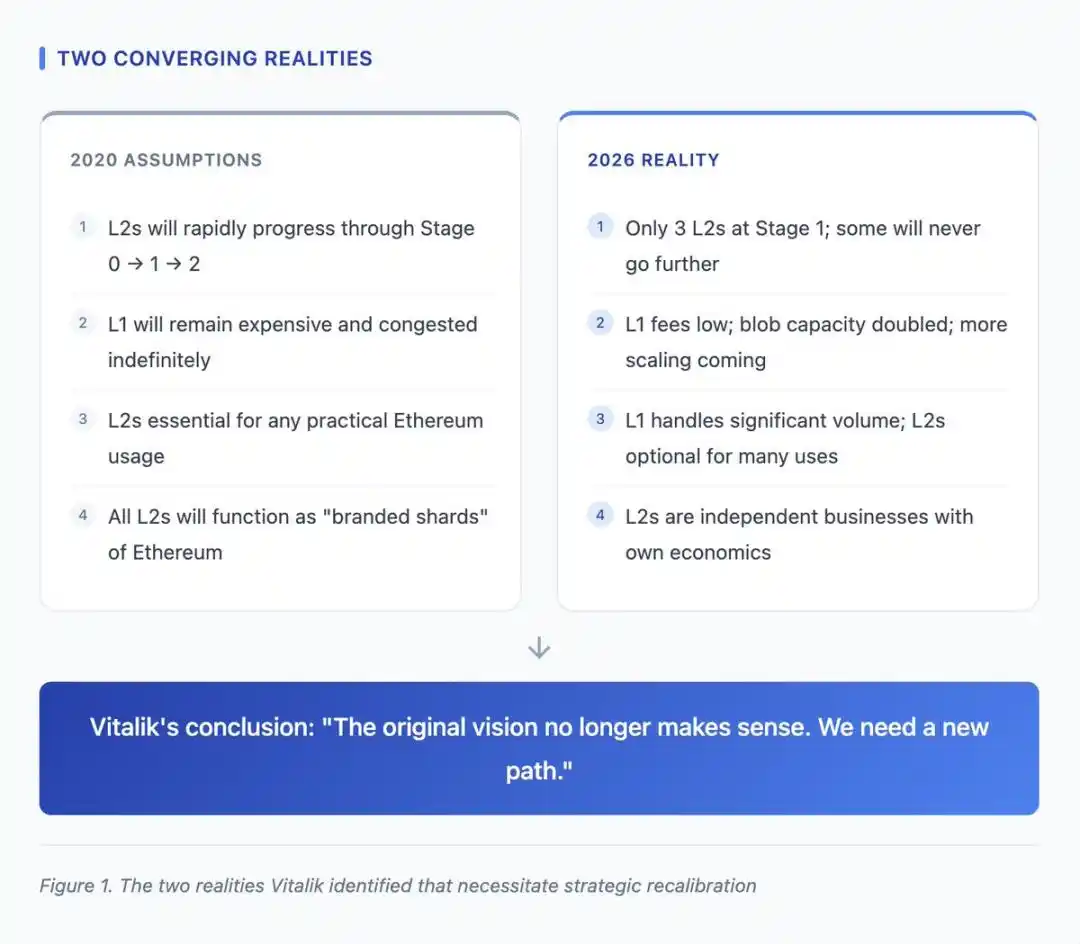

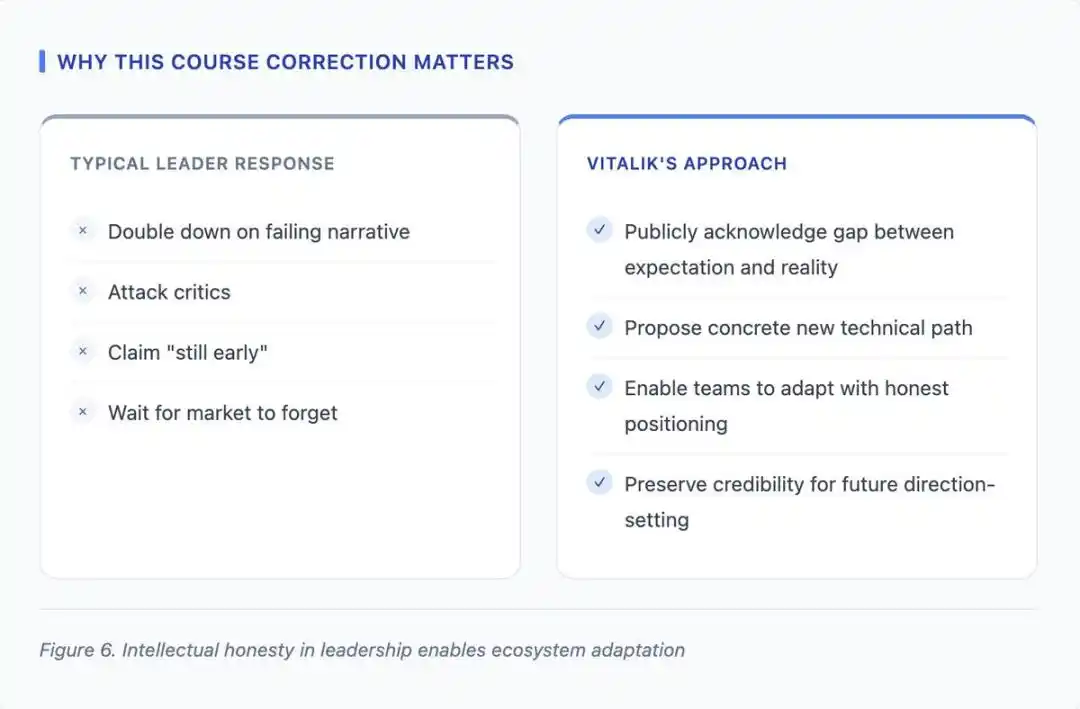

What Vitalik did is not easy — admitting that the core assumptions from 2020 did not materialize as expected. This kind of candor is something most leaders avoid. The "Rollup-centric" roadmap back then was built on the premise that "L2s would act as Ethereum's 'branded shards'." But four years of market data paint a different picture: L2s have evolved into platforms with independent economic incentives, and Ethereum Layer1's scaling speed has far exceeded expectations. The original vision has long been disconnected from reality.

In fact, it would have been easier to continue defending the old narrative — for example, by强行 pushing teams towards a vision the market had already否决. But this is not the mark of good leadership. The truly wise approach is to acknowledge the gap between expectations and reality, propose a new direction, and move towards a brighter future. And this post does exactly that.

The Problems Vitalik Actually Diagnosed

The post points out two core realities requiring strategic adjustment:

First, the decentralization of L2s is much slower than expected. Currently, only 3 mainstream L2s (Arbitrum, OP Mainnet, Base) have reached the first stage of decentralization; some L2 teams have explicitly stated that, due to regulatory requirements or business model limitations, they may never pursue full decentralization. This is not a moral "failure," but a reflection of economic reality — for L2 operators, sequencer revenue is the core business model.

Second, Ethereum L1 has achieved significant scaling. Current L1 fees are low, the Pectra upgrade doubled data blob capacity, and there are plans to continuously increase the Gas limit through 2026. When the Rollup roadmap was designed, "high L1 costs and network congestion" were the basic premises; this premise no longer holds. L1 can now handle a large number of transactions at reasonable costs, which also transforms the value proposition of L2s from "a necessity for ensuring availability" to "an optional solution for specific use cases."

The two realities requiring strategic adjustment as pointed out by Vitalik

Restructuring the Trust Spectrum

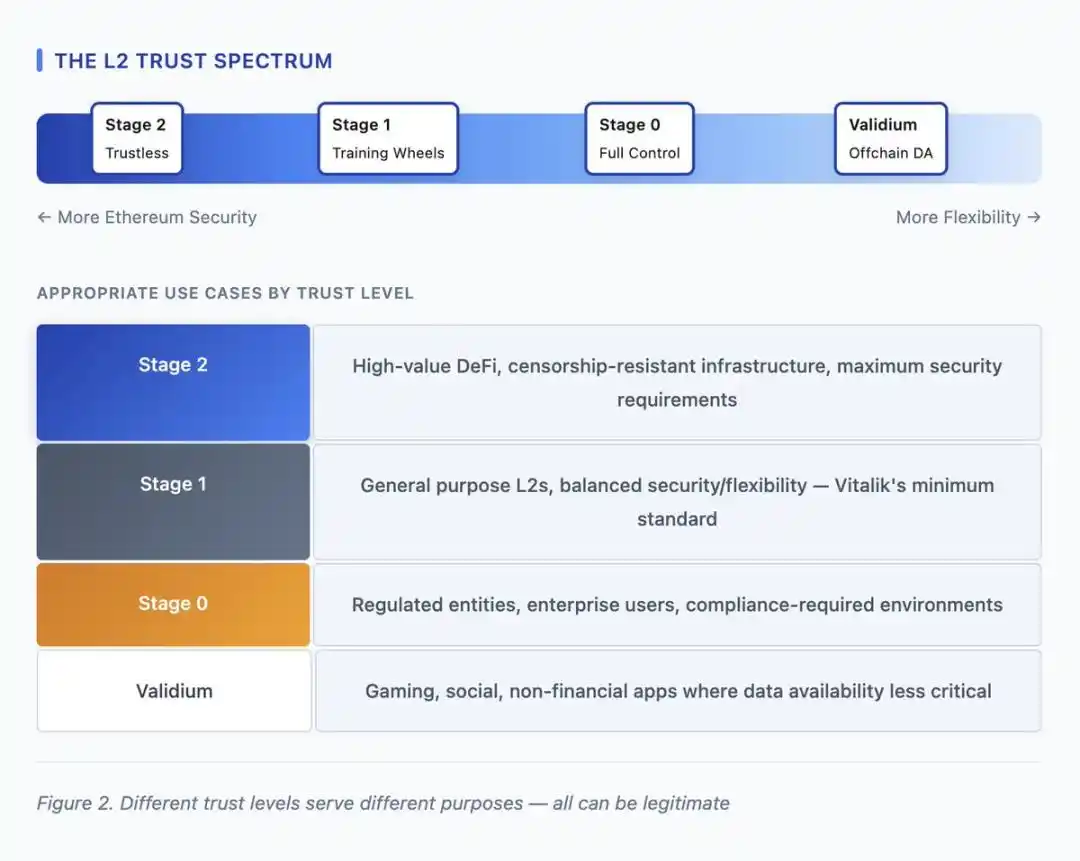

Vitalik's most core conceptual contribution is liberating L2s from the framework of a "single category, uniform obligations" and redefining them as "diverse entities existing on a trust spectrum." The previous metaphor of "branded shards"默认 all L2s needed to pursue Stage 2 decentralization and, as extensions of Ethereum, bear the same value and security commitments as L1. The new framework acknowledges: different L2s have different purposes, and for projects with specific needs, Stage 0 or Stage 1 decentralization can be a perfectly reasonable end goal.

The strategic significance of this reframing is that it breaks the implicit judgment that "an L2 not pursuing full decentralization is a failure." For example, a regulated L2 serving institutional clients that requires asset freezing functionality is not a "flawed Arbitrum," but a "differentiated product for a different market." By endorsing this "trust spectrum," Vitalik allows L2s to be upfront about their positioning, without having to make promises of "decentralization" lacking economic incentive support.

Different trust levels correspond to different uses — all levels can reasonably exist

Classification table of trust levels for Ethereum L2s

Native Rollup Precompile Proposal

The technical core of Vitalik's post is the "Native Rollup Precompile" proposal. Currently, each L2 needs to independently build a system for "proving state transitions to Ethereum": Optimistic Rollups use fraud proofs with a 7-day challenge period, while ZK Rollups use validity proofs based on custom circuits. These implementations not only require independent audits but may also contain vulnerabilities, and need to be updated synchronously when Ethereum hard forks cause changes in EVM (Ethereum Virtual Machine) behavior. This "fragmented" status quo brings security risks and maintenance burdens to the entire ecosystem.

The "Native Rollup Precompile" involves building a function for "verifying EVM execution" directly into Ethereum. Then, each L2 would no longer need to maintain custom provers, but only need to call this shared infrastructure. The advantages are significant: only 1 codebase needs auditing (instead of dozens), automatic compatibility with Ethereum upgrades, and once the precompile functionality is battle-tested, it might even allow for the removal of security councils.

Before and after comparison of Ethereum Native Rollup Precompile architecture

Synchronous Composability Vision

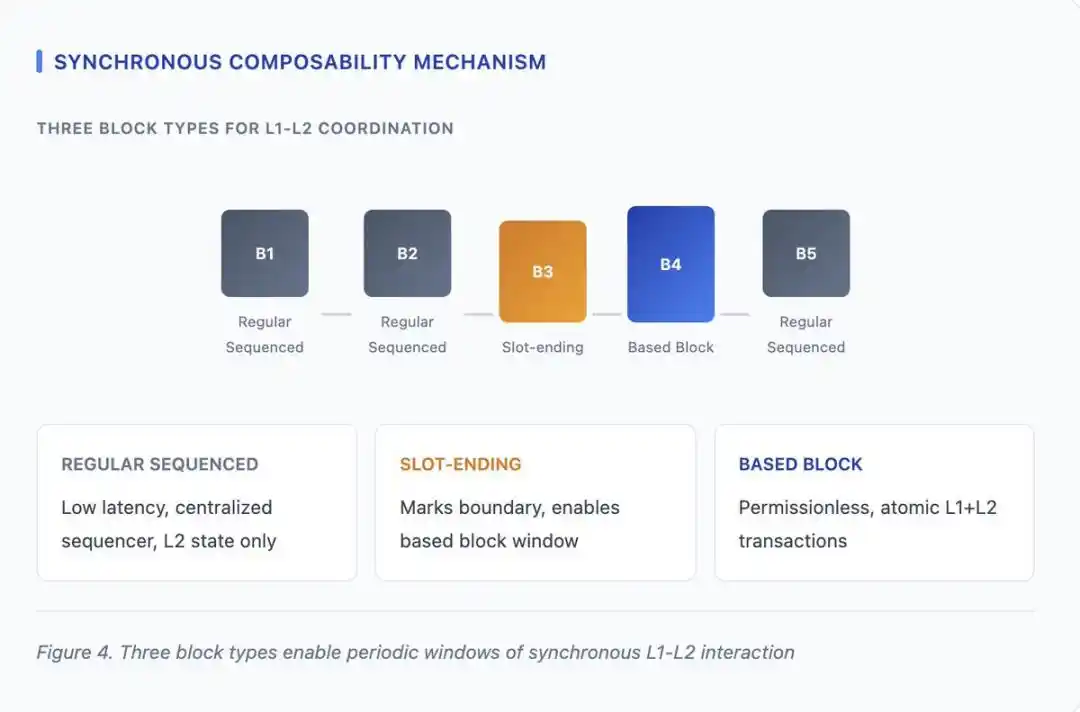

In his post on ethresear.ch, Vitalik detailed a mechanism to achieve "synchronous composability" between L1 and L2. Currently, transferring assets or executing logic across L1 and L2 either requires waiting for final confirmation (7 days for Optimistic Rollups, hours for ZK Rollups) or relies on fast bridges with counterparty risk. "Synchronous composability" would allow transactions to "atomically use L1 and L2 state" — reading and writing data across layers within the same transaction, either completely succeeding or completely rolling back.

The mechanism designs three types of blocks:

- Regular Sequencing Blocks: For processing low-latency L2 transactions;

- Slot End Blocks: Mark the boundary of a time window;

- Base Blocks: Blocks that can be built permissionlessly after the Slot End Block is generated.

During the window for Base Blocks, any block builder can create blocks that interact with both L1 and L2 states simultaneously.

Three types of blocks support periodic synchronous interaction between L1 and L2

Responses from L2 Teams

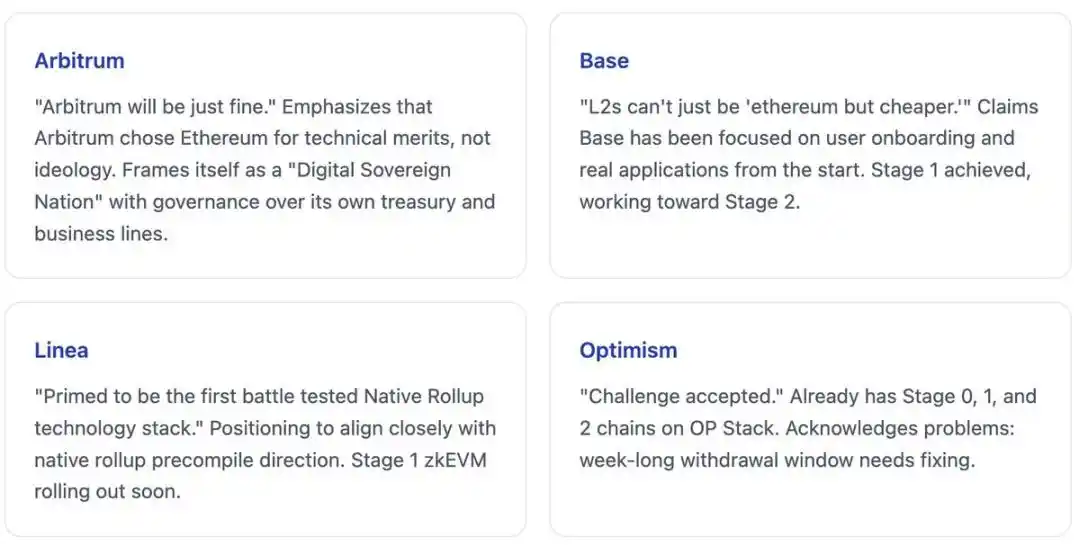

Mainstream L2 teams responded within hours, showing a healthy strategic diversity —这正是 Vitalik's "trust spectrum" framework intended to achieve: different teams can choose different positioning without pretending to march towards the same finish line.

Differentiated responses from four mainstream Ethereum L2 projects to Vitalik's "L2 Reset" proposal

This diversity in response is healthy:

- Arbitrum: Emphasizes independence and self-sufficiency;

- Base: Focuses on applications and users;

- Linea: Closely aligns with the Native Rollup direction proposed by Vitalik;

- Optimism: Acknowledges current challenges while宣称持续推进改进 (claiming continued progress on improvements).

These positions are not right or wrong, just strategic choices for different market segments —这正是 the "trust spectrum" framework recognizes as reasonable.

The L2 Economic Reality Acknowledged by Vitalik

One significant meaning of Vitalik's post is the implicit acknowledgment of L2s' economic attributes. When he mentions that "some L2s may 'never progress beyond Stage 1 decentralization' due to 'regulatory requirements' (need to retain ultimate control),". he is essentially admitting: L2s are not idealized "branded shards," but commercial entities with legitimate economic interests. Sequencer revenue is real, regulatory compliance requirements are real — expecting L2s to abandon these interests to cater to ideology was unrealistic from the start.

L2s retain most fee revenue — this economic reality determines the incentive direction for decentralization

The Future Path Outlined by Vitalik

Vitalik's post is not just about "diagnosing problems" but also focuses on "solving problems." He outlines several concrete directions for those L2s that want to maintain value in the context of continued L1 scaling. These are not mandatory requirements, but suggested paths for L2s to differentiate themselves when "cheaper Ethereum" is no longer the core competitive advantage.

Table of differentiated value directions for Ethereum L2s

Rational candor in leadership enables adaptive development for the ecosystem

Summary

In February 2026, the post published by Vitalik Buterin marked a key calibration of Ethereum's strategy towards L2s. Its core insight is: L2s have evolved into independent platforms with legitimate economic interests, rather than "branded shards" with obligations to Ethereum. Vitalik did not fight this reality but proposed embracing it by: endorsing differentiated paths through the "trust spectrum," strengthening collaboration efficiency for those willing to participate in L1-L2 integration through "native Rollup infrastructure," and enabling cross-layer interaction through "synchronous composability mechanisms."

The response from the L2 ecosystem shows healthy diversity: Arbitrum emphasizes independence, Base focuses on applications, Linea aligns with the Native Rollup direction, Optimism acknowledges challenges and pushes for improvements. This diversity is precisely the expected result of the "trust spectrum" framework: different teams can pursue different strategies without pretending to be on the same path.

For Ethereum, this course correction maintains its credibility by "acknowledging reality" rather than "defending outdated assumptions." Considering the maturity of ZK-EVM technology, the related technical proposals are feasible; and the strategic proposals create space for the ecosystem to evolve efficiently. This is the embodiment of "adaptive leadership" in the technology field: realizing the environment has changed, then proposing a new path, rather than stubbornly sticking to a strategy the market has already否决.

Having been deeply involved in scaling research for a decade and operating a Rollup infrastructure company for four years, I have seen too many leaders refuse to adjust when facts change — often with poor results. Vitalik's choice this time was not easy: publicly admitting that the 2020 vision needed updating. But it was the right choice. Clinging to a narrative the market has abandoned benefits no one. The way forward is now clearer than it was a week ago — that in itself is tremendously valuable.

Criptomoedas em alta

Perguntas relacionadas

QWhat are the two core realities that Vitalik's post identifies as requiring strategic adjustment for Ethereum's Layer2?![]()

AThe two core realities are: 1) The decentralization of L2s is progressing much slower than expected, with only a few major L2s reaching the first stage of decentralization. 2) Ethereum L1 has achieved significant scaling, with lower fees and increased data capacity, which changes the value proposition of L2s from a necessity for availability to an optional solution for specific use cases.

QWhat is the key conceptual contribution of Vitalik's new framework regarding L2s?![]()

AThe key conceptual contribution is reframing L2s from a 'single category with uniform obligations' to a 'diverse existence on a spectrum of trust.' This acknowledges that different L2s have different purposes and that achieving stage 0 or stage 1 decentralization can be a reasonable endpoint for projects with specific needs, rather than a failure.

QWhat is the technical core proposal in Vitalik's post to address the current fragmentation in L2 implementations?![]()

AThe technical core proposal is the 'Native Rollup Precompile.' This involves building a function for 'verifying EVM execution' directly into Ethereum. This shared infrastructure would allow L2s to call this function instead of maintaining their own custom provers, reducing security risks and maintenance burdens.

QHow does the proposed 'synchronous composability' mechanism aim to improve interaction between L1 and L2?![]()

AThe 'synchronous composability' mechanism aims to allow transactions to atomically use both L1 and L2 states within a single transaction, ensuring it either fully succeeds or fully rolls back. It proposes three types of blocks (regular sequencing blocks, slot-end blocks, and base blocks) to enable this cross-layer interaction without the delays or risks associated with current methods like waiting for finality or using fast bridges.

QHow did major L2 teams like Arbitrum, Base, Linea, and Optimism respond to Vitalik's proposal, and what does this indicate?![]()

AThe responses showed healthy strategic diversity: Arbitrum emphasized independence and self-sufficiency, Base focused on applications and users, Linea closely aligned with the native Rollup direction, and Optimism acknowledged current challenges while committing to ongoing improvements. This diversity indicates the success of the 'trust spectrum' framework, allowing different teams to pursue different strategic positions for their respective markets without pretending to move toward the same endpoint.

Leituras Relacionadas

Trading

Artigos em Destaque

O que é $S$

Compreender o SPERO: Uma Visão Abrangente Introdução ao SPERO À medida que o panorama da inovação continua a evoluir, o surgimento de tecnologias web3 e projetos de criptomoeda desempenha um papel fundamental na formação do futuro digital. Um projeto que tem atraído atenção neste campo dinâmico é o SPERO, denotado como SPERO,$$s$. Este artigo tem como objetivo reunir e apresentar informações detalhadas sobre o SPERO, para ajudar entusiastas e investidores a compreender as suas bases, objetivos e inovações nos domínios web3 e cripto. O que é o SPERO,$$s$? O SPERO,$$s$ é um projeto único dentro do espaço cripto que procura aproveitar os princípios da descentralização e da tecnologia blockchain para criar um ecossistema que promove o envolvimento, a utilidade e a inclusão financeira. O projeto é concebido para facilitar interações peer-to-peer de novas maneiras, proporcionando aos utilizadores soluções e serviços financeiros inovadores. No seu núcleo, o SPERO,$$s$ visa capacitar indivíduos ao fornecer ferramentas e plataformas que melhoram a experiência do utilizador no espaço das criptomoedas. Isso inclui a possibilidade de métodos de transação mais flexíveis, a promoção de iniciativas impulsionadas pela comunidade e a criação de caminhos para oportunidades financeiras através de aplicações descentralizadas (dApps). A visão subjacente do SPERO,$$s$ gira em torno da inclusão, visando fechar lacunas dentro das finanças tradicionais enquanto aproveita os benefícios da tecnologia blockchain. Quem é o Criador do SPERO,$$s$? A identidade do criador do SPERO,$$s$ permanece algo obscura, uma vez que existem recursos publicamente disponíveis limitados que fornecem informações detalhadas sobre o(s) seu(s) fundador(es). Esta falta de transparência pode resultar do compromisso do projeto com a descentralização—uma ética que muitos projetos web3 partilham, priorizando contribuições coletivas em vez de reconhecimento individual. Ao centrar as discussões em torno da comunidade e dos seus objetivos coletivos, o SPERO,$$s$ incorpora a essência do empoderamento sem destacar indivíduos específicos. Assim, compreender a ética e a missão do SPERO é mais importante do que identificar um criador singular. Quem são os Investidores do SPERO,$$s$? O SPERO,$$s$ é apoiado por uma diversidade de investidores que vão desde capitalistas de risco a investidores-anjo dedicados a promover a inovação no setor cripto. O foco desses investidores geralmente alinha-se com a missão do SPERO—priorizando projetos que prometem avanço tecnológico social, inclusão financeira e governança descentralizada. Essas fundações de investidores estão tipicamente interessadas em projetos que não apenas oferecem produtos inovadores, mas que também contribuem positivamente para a comunidade blockchain e os seus ecossistemas. O apoio desses investidores reforça o SPERO,$$s$ como um concorrente notável no domínio em rápida evolução dos projetos cripto. Como Funciona o SPERO,$$s$? O SPERO,$$s$ emprega uma estrutura multifacetada que o distingue de projetos de criptomoeda convencionais. Aqui estão algumas das características-chave que sublinham a sua singularidade e inovação: Governança Descentralizada: O SPERO,$$s$ integra modelos de governança descentralizada, capacitando os utilizadores a participar ativamente nos processos de tomada de decisão sobre o futuro do projeto. Esta abordagem promove um sentido de propriedade e responsabilidade entre os membros da comunidade. Utilidade do Token: O SPERO,$$s$ utiliza o seu próprio token de criptomoeda, concebido para servir várias funções dentro do ecossistema. Esses tokens permitem transações, recompensas e a facilitação de serviços oferecidos na plataforma, melhorando o envolvimento e a utilidade gerais. Arquitetura em Camadas: A arquitetura técnica do SPERO,$$s$ suporta modularidade e escalabilidade, permitindo a integração contínua de funcionalidades e aplicações adicionais à medida que o projeto evolui. Esta adaptabilidade é fundamental para manter a relevância no panorama cripto em constante mudança. Envolvimento da Comunidade: O projeto enfatiza iniciativas impulsionadas pela comunidade, empregando mecanismos que incentivam a colaboração e o feedback. Ao nutrir uma comunidade forte, o SPERO,$$s$ pode melhor atender às necessidades dos utilizadores e adaptar-se às tendências do mercado. Foco na Inclusão: Ao oferecer taxas de transação baixas e interfaces amigáveis, o SPERO,$$s$ visa atrair uma base de utilizadores diversificada, incluindo indivíduos que anteriormente podem não ter participado no espaço cripto. Este compromisso com a inclusão alinha-se com a sua missão abrangente de empoderamento através da acessibilidade. Cronologia do SPERO,$$s$ Compreender a história de um projeto fornece insights cruciais sobre a sua trajetória de desenvolvimento e marcos. Abaixo está uma cronologia sugerida que mapeia eventos significativos na evolução do SPERO,$$s$: Fase de Conceituação e Ideação: As ideias iniciais que formam a base do SPERO,$$s$ foram concebidas, alinhando-se de perto com os princípios de descentralização e foco na comunidade dentro da indústria blockchain. Lançamento do Whitepaper do Projeto: Após a fase conceitual, um whitepaper abrangente detalhando a visão, os objetivos e a infraestrutura tecnológica do SPERO,$$s$ foi lançado para atrair o interesse e o feedback da comunidade. Construção da Comunidade e Primeiros Envolvimentos: Esforços ativos de divulgação foram feitos para construir uma comunidade de primeiros adotantes e investidores potenciais, facilitando discussões em torno dos objetivos do projeto e angariando apoio. Evento de Geração de Tokens: O SPERO,$$s$ realizou um evento de geração de tokens (TGE) para distribuir os seus tokens nativos a apoiantes iniciais e estabelecer liquidez inicial dentro do ecossistema. Lançamento da dApp Inicial: A primeira aplicação descentralizada (dApp) associada ao SPERO,$$s$ foi lançada, permitindo que os utilizadores interagissem com as funcionalidades principais da plataforma. Desenvolvimento Contínuo e Parcerias: Atualizações e melhorias contínuas nas ofertas do projeto, incluindo parcerias estratégicas com outros players no espaço blockchain, moldaram o SPERO,$$s$ em um jogador competitivo e em evolução no mercado cripto. Conclusão O SPERO,$$s$ é um testemunho do potencial do web3 e das criptomoedas para revolucionar os sistemas financeiros e capacitar indivíduos. Com um compromisso com a governança descentralizada, o envolvimento da comunidade e funcionalidades inovadoras, abre caminho para um panorama financeiro mais inclusivo. Como em qualquer investimento no espaço cripto em rápida evolução, potenciais investidores e utilizadores são incentivados a pesquisar minuciosamente e a envolver-se de forma ponderada com os desenvolvimentos em curso dentro do SPERO,$$s$. O projeto demonstra o espírito inovador da indústria cripto, convidando a uma exploração mais aprofundada das suas inúmeras possibilidades. Embora a jornada do SPERO,$$s$ ainda esteja a desenrolar-se, os seus princípios fundamentais podem, de facto, influenciar o futuro de como interagimos com a tecnologia, as finanças e uns com os outros em ecossistemas digitais interconectados.

124 Visualizações TotaisPublicado em {updateTime}Atualizado em 2024.12.17

O que é AGENT S

Agent S: O Futuro da Interação Autónoma no Web3 Introdução No panorama em constante evolução do Web3 e das criptomoedas, as inovações estão constantemente a redefinir a forma como os indivíduos interagem com plataformas digitais. Um projeto pioneiro, o Agent S, promete revolucionar a interação humano-computador através do seu framework aberto e agente. Ao abrir caminho para interações autónomas, o Agent S visa simplificar tarefas complexas, oferecendo aplicações transformadoras em inteligência artificial (IA). Esta exploração detalhada irá aprofundar-se nas complexidades do projeto, nas suas características únicas e nas implicações para o domínio das criptomoedas. O que é o Agent S? O Agent S é um framework aberto e agente, especificamente concebido para abordar três desafios fundamentais na automação de tarefas computacionais: Aquisição de Conhecimento Específico de Domínio: O framework aprende inteligentemente a partir de várias fontes de conhecimento externas e experiências internas. Esta abordagem dupla capacita-o a construir um rico repositório de conhecimento específico de domínio, melhorando o seu desempenho na execução de tarefas. Planeamento ao Longo de Longos Horizontes de Tarefas: O Agent S emprega planeamento hierárquico aumentado por experiência, uma abordagem estratégica que facilita a decomposição e execução eficientes de tarefas intrincadas. Esta característica melhora significativamente a sua capacidade de gerir múltiplas subtarefas de forma eficiente e eficaz. Gestão de Interfaces Dinâmicas e Não Uniformes: O projeto introduz a Interface Agente-Computador (ACI), uma solução inovadora que melhora a interação entre agentes e utilizadores. Utilizando Modelos de Linguagem Multimodais de Grande Escala (MLLMs), o Agent S pode navegar e manipular diversas interfaces gráficas de utilizador de forma fluida. Através destas características pioneiras, o Agent S fornece um framework robusto que aborda as complexidades envolvidas na automação da interação humana com máquinas, preparando o terreno para uma infinidade de aplicações em IA e além. Quem é o Criador do Agent S? Embora o conceito de Agent S seja fundamentalmente inovador, informações específicas sobre o seu criador permanecem elusivas. O criador é atualmente desconhecido, o que destaca ou o estágio nascente do projeto ou a escolha estratégica de manter os membros fundadores em anonimato. Independentemente da anonimidade, o foco permanece nas capacidades e no potencial do framework. Quem são os Investidores do Agent S? Como o Agent S é relativamente novo no ecossistema criptográfico, informações detalhadas sobre os seus investidores e financiadores não estão explicitamente documentadas. A falta de informações disponíveis publicamente sobre as fundações de investimento ou organizações que apoiam o projeto levanta questões sobre a sua estrutura de financiamento e roteiro de desenvolvimento. Compreender o apoio é crucial para avaliar a sustentabilidade do projeto e o seu impacto potencial no mercado. Como Funciona o Agent S? No núcleo do Agent S reside uma tecnologia de ponta que lhe permite funcionar eficazmente em diversos ambientes. O seu modelo operacional é construído em torno de várias características-chave: Interação Humano-Computador Semelhante: O framework oferece planeamento avançado em IA, esforçando-se para tornar as interações com computadores mais intuitivas. Ao imitar o comportamento humano na execução de tarefas, promete elevar as experiências dos utilizadores. Memória Narrativa: Utilizada para aproveitar experiências de alto nível, o Agent S utiliza memória narrativa para acompanhar os históricos de tarefas, melhorando assim os seus processos de tomada de decisão. Memória Episódica: Esta característica fornece aos utilizadores orientações passo a passo, permitindo que o framework ofereça suporte contextual à medida que as tarefas se desenrolam. Suporte para OpenACI: Com a capacidade de funcionar localmente, o Agent S permite que os utilizadores mantenham o controlo sobre as suas interações e fluxos de trabalho, alinhando-se com a ética descentralizada do Web3. Fácil Integração com APIs Externas: A sua versatilidade e compatibilidade com várias plataformas de IA garantem que o Agent S possa integrar-se perfeitamente em ecossistemas tecnológicos existentes, tornando-o uma escolha apelativa para desenvolvedores e organizações. Estas funcionalidades contribuem coletivamente para a posição única do Agent S no espaço cripto, à medida que automatiza tarefas complexas e em múltiplos passos com mínima intervenção humana. À medida que o projeto evolui, as suas potenciais aplicações no Web3 podem redefinir a forma como as interações digitais se desenrolam. Cronologia do Agent S O desenvolvimento e os marcos do Agent S podem ser encapsulados numa cronologia que destaca os seus eventos significativos: 27 de Setembro de 2024: O conceito de Agent S foi lançado num artigo de pesquisa abrangente intitulado “Um Framework Agente Aberto que Usa Computadores como um Humano”, mostrando a base para o projeto. 10 de Outubro de 2024: O artigo de pesquisa foi disponibilizado publicamente no arXiv, oferecendo uma exploração aprofundada do framework e da sua avaliação de desempenho com base no benchmark OSWorld. 12 de Outubro de 2024: Uma apresentação em vídeo foi lançada, proporcionando uma visão visual das capacidades e características do Agent S, envolvendo ainda mais potenciais utilizadores e investidores. Estes marcos na cronologia não apenas ilustram o progresso do Agent S, mas também indicam o seu compromisso com a transparência e o envolvimento da comunidade. Pontos-Chave Sobre o Agent S À medida que o framework Agent S continua a evoluir, várias características-chave destacam-se, sublinhando a sua natureza inovadora e potencial: Framework Inovador: Concebido para proporcionar um uso intuitivo de computadores semelhante à interação humana, o Agent S traz uma abordagem nova à automação de tarefas. Interação Autónoma: A capacidade de interagir autonomamente com computadores através de GUI significa um avanço em direção a soluções computacionais mais inteligentes e eficientes. Automação de Tarefas Complexas: Com a sua metodologia robusta, pode automatizar tarefas complexas e em múltiplos passos, tornando os processos mais rápidos e menos propensos a erros. Melhoria Contínua: Os mecanismos de aprendizagem permitem que o Agent S melhore a partir de experiências passadas, aprimorando continuamente o seu desempenho e eficácia. Versatilidade: A sua adaptabilidade em diferentes ambientes operacionais, como OSWorld e WindowsAgentArena, garante que pode servir uma ampla gama de aplicações. À medida que o Agent S se posiciona no panorama do Web3 e das criptomoedas, o seu potencial para melhorar as capacidades de interação e automatizar processos significa um avanço significativo nas tecnologias de IA. Através do seu framework inovador, o Agent S exemplifica o futuro das interações digitais, prometendo uma experiência mais fluida e eficiente para os utilizadores em diversas indústrias. Conclusão O Agent S representa um ousado avanço na união da IA e do Web3, com a capacidade de redefinir a forma como interagimos com a tecnologia. Embora ainda esteja nas suas fases iniciais, as possibilidades para a sua aplicação são vastas e cativantes. Através do seu framework abrangente que aborda desafios críticos, o Agent S visa trazer interações autónomas para o primeiro plano da experiência digital. À medida que avançamos mais profundamente nos domínios das criptomoedas e da descentralização, projetos como o Agent S desempenharão, sem dúvida, um papel crucial na formação do futuro da tecnologia e da colaboração humano-computador.

741 Visualizações TotaisPublicado em {updateTime}Atualizado em 2025.01.14

Como comprar S

Bem-vindo à HTX.com!Tornámos a compra de Sonic (S) simples e conveniente.Segue o nosso guia passo a passo para iniciar a tua jornada no mundo das criptos.Passo 1: cria a tua conta HTXUtiliza o teu e-mail ou número de telefone para te inscreveres numa conta gratuita na HTX.Desfruta de um processo de inscrição sem complicações e desbloqueia todas as funcionalidades.Obter a minha contaPasso 2: vai para Comprar Cripto e escolhe o teu método de pagamentoCartão de crédito/débito: usa o teu visa ou mastercard para comprar Sonic (S) instantaneamente.Saldo: usa os fundos da tua conta HTX para transacionar sem problemas.Terceiros: adicionamos métodos de pagamento populares, como Google Pay e Apple Pay, para aumentar a conveniência.P2P: transaciona diretamente com outros utilizadores na HTX.Mercado de balcão (OTC): oferecemos serviços personalizados e taxas de câmbio competitivas para os traders.Passo 3: armazena teu Sonic (S)Depois de comprar o teu Sonic (S), armazena-o na tua conta HTX.Alternativamente, podes enviá-lo para outro lugar através de transferência blockchain ou usá-lo para transacionar outras criptomoedas.Passo 4: transaciona Sonic (S)Transaciona facilmente Sonic (S) no mercado à vista da HTX.Acede simplesmente à tua conta, seleciona o teu par de trading, executa as tuas transações e monitoriza em tempo real.Oferecemos uma experiência de fácil utilização tanto para principiantes como para traders experientes.

1.3k Visualizações TotaisPublicado em {updateTime}Atualizado em 2026.06.02