Author: Chloe, ChainCatcher

In June 2026, over a dozen of America's largest banks jointly announced plans to build a shared tokenized deposit network by 2027, aiming to directly counter the erosion of traditional deposits by stablecoins. This system currently has no official name; within the industry, some call it "the bridge," while others call it "the chain."

This development reflects the quiet resurgence of a concept long neglected by the market: consortium blockchains.

Banks Form an Avengers-Style Alliance

On June 5, 2026, The Wall Street Journal broke the news: a group of US mega-banks led by JPMorgan Chase, Citigroup, and Bank of America planned to construct a shared tokenized deposit network by the first half of 2027.

Later that day, these banks issued a joint press release, expanding the list from the rumored four to over a dozen. Wells Fargo is a founding member, followed by BNY Mellon, BMO, HSBC, PNC, TD Bank, U.S. Bank, Truist, Citizens Bank, Fifth Third Bank, Huntington Bank, KeyBank, Regions Bank, and Santander.

The operator is The Clearing House, a payment company jointly owned by these banks. As reported by The Wall Street Journal, this system still lacks a formal name; within the industry, it's referred to as "the bridge" by some and "the chain" by others.

Over the past two years, the crypto world's focus has largely been on public chains, token issuance, and airdrops. However, the institutional capital and technology moving quietly behind the scenes are heading in a different direction: purpose-built chains, often institution-led, permissioned, and not necessarily involving token issuance. This sounds familiar because it embodies the original spirit of "consortium blockchains," but this time, it might be the real deal.

What Banks Fear Is Stablecoins Siphoning Off Deposits

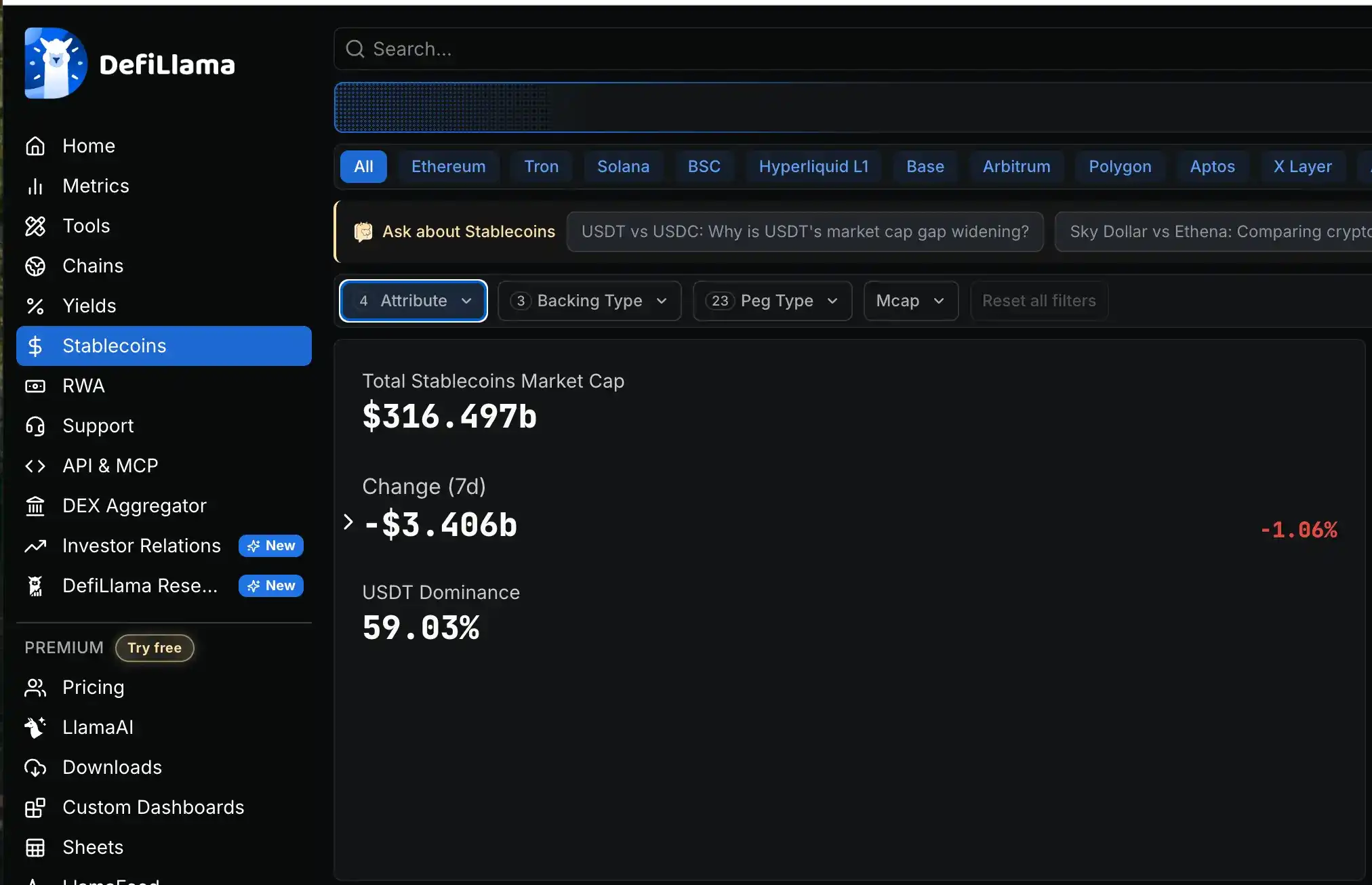

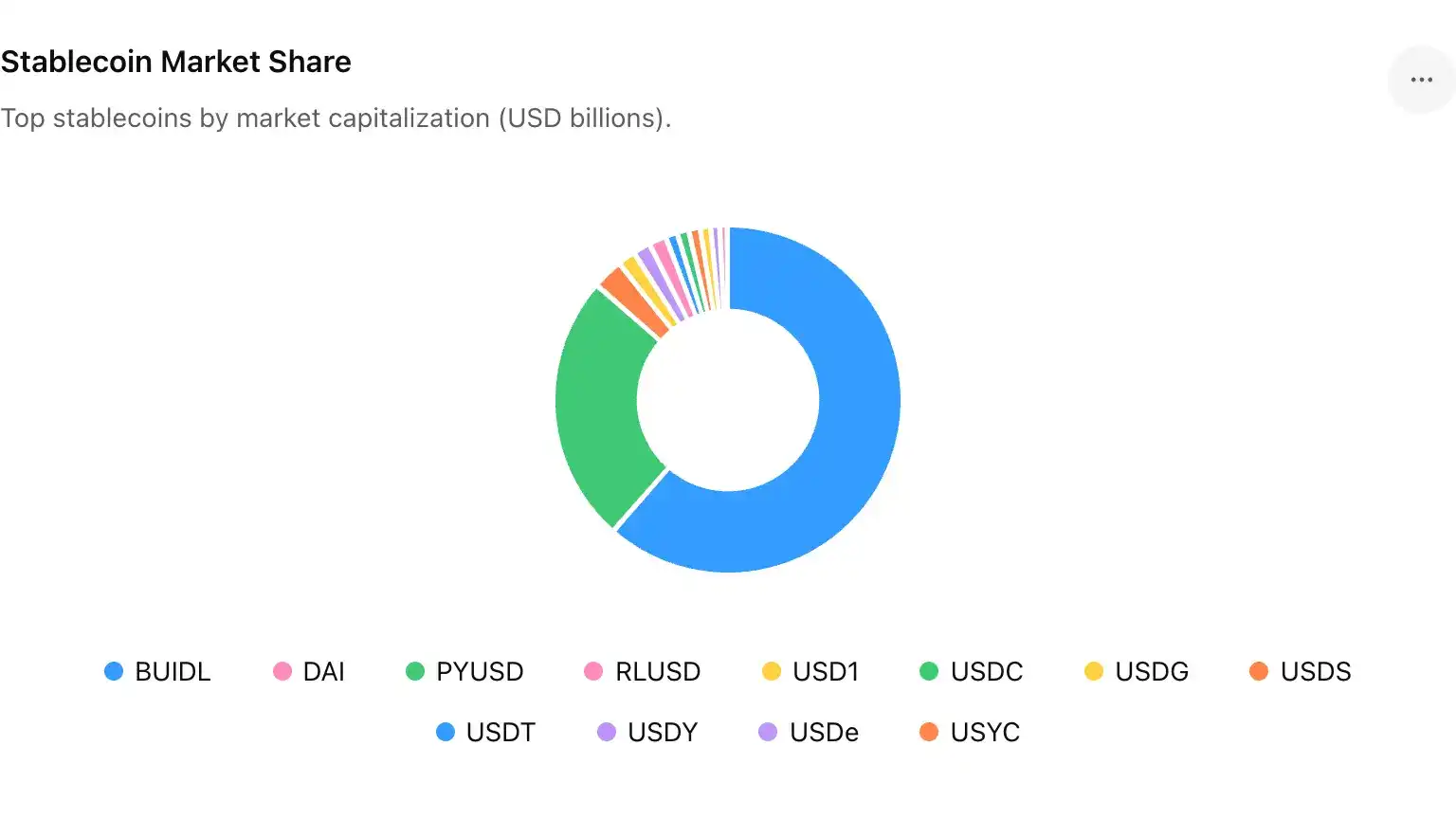

To understand this counterattack, one must first grasp what traditional finance is guarding against: stablecoins. According to DeFiLlama data, in June 2026, the total market capitalization of global stablecoins was approximately $3.16 trillion. USDT alone accounted for about 62%, with a market cap of around $1.86 trillion, while USDC stood at about $750 billion; together, they dominate roughly 80% of the market.

According to Bitrue, stablecoins processed approximately $46 trillion in transaction volume in 2025, over 20 times that of PayPal and approaching three times that of Visa. By Q1 2026, stablecoins accounted for about 75% of total crypto transaction volume. The stablecoin arena has long ceased to be merely a speculative tool; it has become a global payment and settlement pipeline active daily.

For traditional bankers, this pipeline strikes at their core business: deposits. The amount a bank can lend is fundamentally based on the deposits it holds. Once customers get accustomed to moving money from bank accounts into stablecoins in crypto wallets, the foundation for bank lending is hollowed out. Mark Monaco, Global Head of Payments at Bank of America, stated that this system is being prepared in advance for when demand truly takes off.

What is truly compelling banks to act proactively is regulatory easing. The US GENIUS Act has been enacted into law, requiring stablecoins to be fully backed 1:1 with reserves and undergo regular audits, with detailed implementation rules set to take effect on July 18, 2026. The impact of this law lies not in restricting stablecoins but in legitimizing them. When stablecoins transition from a gray area to licensed, audited, and bank-custodied legal instruments, their substitutability for traditional deposits is no longer hypothetical.

Banks have not suddenly fallen in love with blockchain; someone has already laid tracks to their doorstep, forcing them to lay their own.

Bridge or Chain? What Is This Network Exactly?

Returning to that unnamed chain. Its technical designation is a Regulated Settlement Network (RSN). The approach involves converting bank deposits into tokens recorded on a blockchain, enabling round-the-clock, 24/7 real-time settlement, without waiting for the next business day.

"Tokenized deposits" are not a new type of digital asset but the same deposit represented with a different method of record-keeping. They carry the same credit risk, are subject to the same regulations, and remain within the bank system protected by deposit insurance. This is their most fundamental difference from stablecoins: stablecoins move money outside the banking system, while tokenized deposits keep money within the system yet endow it with cryptocurrency-like speed and programmability.

David Watson, CEO of The Clearing House, noted that this is a major move for banks, describing on-chain payments as leading to a completely different future. Max Neukirchen, Co-Head of Global Payments at JPMorgan Chase, offered a more pragmatic perspective, stating that to maintain a stable and resilient payment ecosystem, a regulated market infrastructure is needed to clear these tokenized deposits.

As of the news release, the specific blockchain for this network has not been finalized. The technology is undecided, and its name oscillates between "bridge" and "chain." Yet, over a dozen of America's largest banks have already agreed to put their names on the same press release. At this stage, what has been agreed upon ahead of the technology is governance: who operates it, who can join, and who sets the rules. The answers to these three questions constitute the very essence of what "consortium blockchain" meant in the past.

Revisiting the Last Failure of Consortium Blockchains

From 2016 to 2022, there was a first wave of enterprise blockchain enthusiasm. JPMorgan Chase experimented on Ethereum as early as 2016 and later developed its own private blockchain, Quorum. Hyperledger Fabric by IBM and the Linux Foundation, and Corda led by R3, all saw initial hype followed by a collective fizzle-out.

The reasons, simply put, boiled down to two things. First, there was no compelling pressure for genuine cooperation; each bank built its own closed-off chain, which remained unconnected, resulting in isolated islands. Second, a permissioned ledger in many use cases was essentially just an encrypted database; the technology came first, and problems were sought retroactively. By 2020, as the market narrative shifted entirely toward public chains, DeFi, and liquidity mining, consortium blockchains were labeled as "on-chain, but in the wrong place" and gradually faded from mainstream conversation.

Reflecting on this history provides a contrasting backdrop for today. Consortium blockchains did not fail due to technology; they failed because no one genuinely needed them. What brings them back into view in 2026 precisely fills that critical missing piece: real, urgent, and regulatorily-endorsed demand. Where technology once forced-fit use cases, this time use cases are driving the search for technology.

Data Perspective: Institutional-Grade Consortium Chains Are Already Quietly Operating

The tokenized deposit network is not an isolated event. Over the past eighteen months, multiple institution-led purpose-built chains have accumulated quantifiable scale, with Canton Network having the most comprehensive data.

Developed by Digital Asset, Canton is a public permissioned blockchain, utilizing Daml for smart contracts. Its design goal is to enable competing financial institutions to share a single settlement infrastructure while preserving privacy. Its super validators include Visa, Nasdaq, and BNP Paribas.

In terms of usage, by the end of 2025, over 700 institutions were connected to Canton. The largest application on the network, the Broadridge Distributed Ledger Repo (DLR) platform, processes approximately $4 trillion in monthly tokenized US Treasury repo volume, equating to about $280 billion daily. This figure doubled from $2 trillion per month during 2025.

In December 2025, the US Depository Trust & Clearing Corporation (DTCC) announced a partnership with Digital Asset to tokenize US Treasuries it holds on Canton, with plans to scale up in the second half of 2026. As the core clearing and settlement entity for US equities and fixed income, DTCC's involvement signifies that institutional-grade chains have penetrated the foundational infrastructure of the US market.

Data at the single-bank level is equally concrete. JPMorgan's blockchain unit, Kinexys, has been using JPM Coin on its private blockchain to process institutional payments since 2020, currently handling over $5 billion daily. Citi's Token Services is live, supporting real-time cross-border transfers between New York, London, and Hong Kong. BNY Mellon also launched an institutional tokenized deposit service in January 2026.

Collectively, this data positions the tokenized deposit network as an interoperability layer connecting existing bank projects, rather than another entirely new chain. The driving force is not technology vendors but banks with accumulated real transaction volumes, now seeking a common standard to interconnect.

The Boundary Between Public and Consortium Chains Is Being Blurred by Insiders

A closer look at JPMorgan's strategy reveals it is simultaneously deepening its private blockchain Kinexys, having moved its JPM Coin deposit token (JPMD) onto Coinbase's public chain Base in June 2025. Shortly after, in January 2026, it natively deployed JPMD onto Canton, making it the second chain (after Base) to host this institutional digital cash.

The same bank is betting on three fronts: private chain, public permissioned chain, and public chain.

Earlier, DBS Bank of Singapore and Kinexys agreed in November 2025 to co-develop an interoperability framework enabling tokenized deposits to move between their respective chain ecosystems. What the industry truly cares about is no longer the binary choice of "consortium chain or public chain," but how "permissioned issuance" can interface with "cross-chain settlement."

For banks, public chains are channels to access capital and users, while consortium chains are the settlement backend meeting privacy and compliance needs. The two are not adversaries but sequential segments of the same value chain. What is "reviving" is not the closed, siloed consortium chain of 2018, but its governance soul: purpose-built, institution-led, rules-first. The difference is that this soul now inhabits a new body capable of interfacing with public chains.

Conclusion: The Real Competition Is Over Whose Name the Infrastructure Bears

The dominant narrative of the past few years has been "decentralization will eventually replace traditional finance." However, 2026 is scripting a different version: traditional finance is not being replaced; it is merely extracting blockchain technology from the context of public chains, token issuance, and DeFi, and reconnecting it to its familiar track: a logic of regulation, licensing, and institutional dominance.

This logic differs from the old consortium blockchain approach in that this time it carries the real demand validated by stablecoins, the regulatory runway paved by the GENIUS Act, and the actual transaction volumes demonstrated by Canton and Kinexys. It is no longer just a technological proposition but a functioning reality.

Whether public chains or consortium chains "win" was never the point. When tokenized deposits and stablecoins become functionally indistinguishable, the endgame of competition shifts from products to which infrastructure becomes the default option. Whose name the financial infrastructure of the next decade bears is the real stake on this card table.