Written by: Gino Matos

Compiled by: Luffy, Foresight News

Since January 2024, the performance comparison between cryptocurrencies and stocks indicates that the so-called new "altcoin trading" is essentially just a substitute for stock trading.

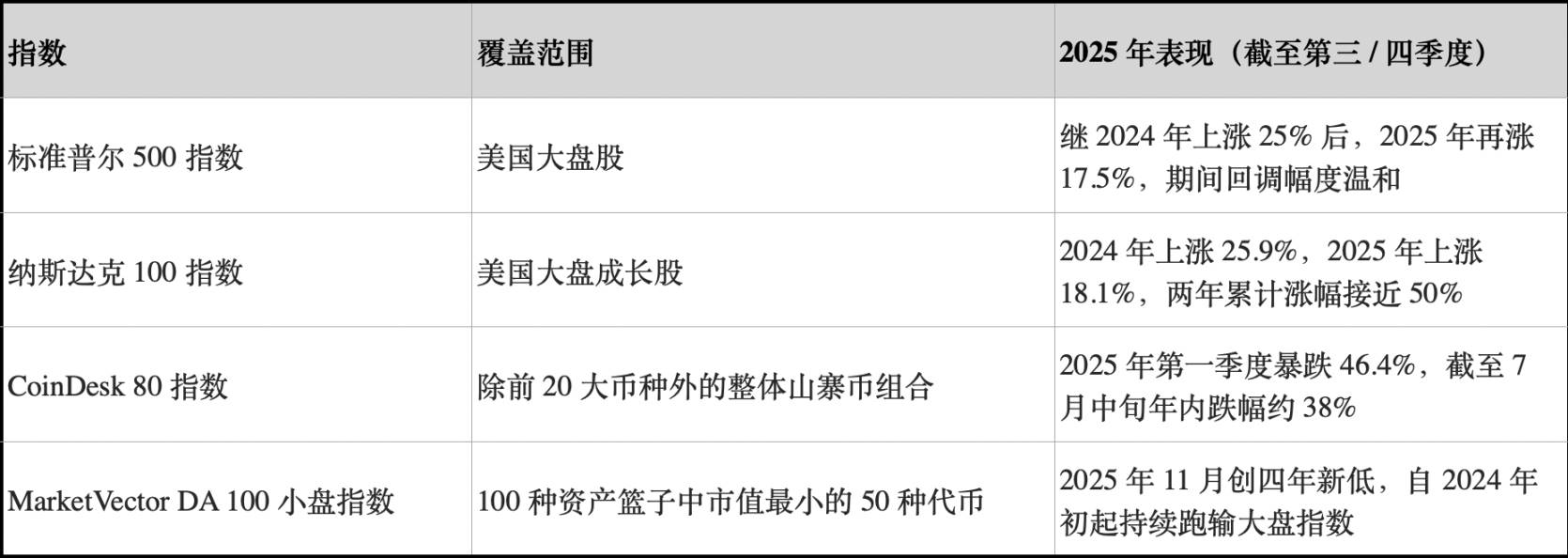

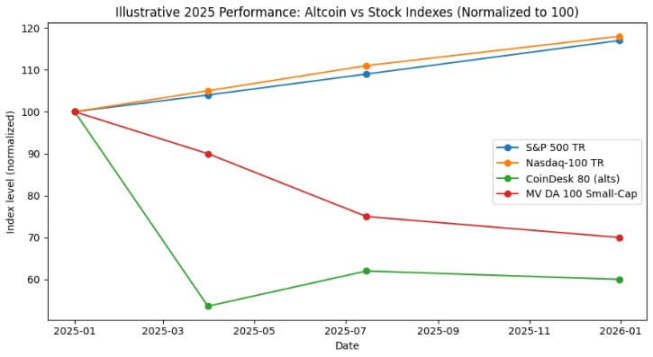

In 2024, the S&P 500 index had a return of approximately 25%, reaching about 17.5% in 2025, with a cumulative two-year increase of nearly 47%. During the same period, the Nasdaq 100 index rose by 25.9% and 18.1% respectively, with a cumulative increase close to 49%.

The CoinDesk 80 Index, which tracks 80 assets outside the top 20 cryptocurrencies by market cap, plummeted 46.4% in the first quarter of 2025 alone, and by mid-July, it was down about 38% year-to-date.

By the end of 2025, the MarketVector Digital Assets 100 Small-Cap Index fell to its lowest level since November 2020, wiping out over $1 trillion from the total cryptocurrency market capitalization.

This divergence in performance is by no means a statistical error. Not only did a portfolio of overall altcoins have a negative return, but its volatility was also comparable to or even higher than that of stocks; in contrast, major U.S. stock indices achieved double-digit growth with manageable drawdowns.

For Bitcoin investors, the core question is: Can allocating to small-cap tokens provide risk-adjusted returns? Or is such an allocation merely taking on additional exposure to negative Sharpe ratio risk while maintaining similar correlation to stocks? (Note: The Sharpe ratio is a core metric for measuring the risk-adjusted return of an investment portfolio, calculated as: Annualized portfolio return - Annualized risk-free rate / Annualized portfolio standard deviation.)

Choosing a Reliable Altcoin Index

For analysis, CryptoSlate tracked three altcoin indices.

The first is the CoinDesk 80 Index, launched in January 2025. This index covers 80 assets outside the CoinDesk 20 Index, providing a diversified portfolio of标的 beyond Bitcoin, Ethereum, and other top tokens.

The second is the MarketVector Digital Assets 100 Small-Cap Index. This index selects the 50 smallest tokens by market cap from a basket of 100 assets, serving as a barometer for the market's "junk assets."

The third is the small-cap index launched by Kaiko. This is a research product, not a tradable benchmark, offering a clear sell-side quantitative perspective for analyzing the small-cap asset group.

These three depict the market landscape from different dimensions: the overall altcoin portfolio, high-beta small-cap tokens, and a quantitative research perspective. Yet, the conclusions they point to are highly consistent.

In contrast, the benchmark performance of the stock market shows a completely opposite trend.

In 2024, major U.S. indices achieved gains of around 25%, with double-digit growth also in 2025, accompanied by relatively limited drawdowns. During this period, the maximum intra-year drawdown for the S&P 500 index was only in the mid-to-high single digits, while the Nasdaq 100 index maintained a strong upward trend throughout.

Both major stock indices achieved compounded annual growth without significant givebacks of gains.

The trend of the overall altcoin indices, however, was vastly different. Reports from CoinDesk Indices show that the CoinDesk 80 Index plummeted 46.4% in the first quarter alone, while the large-cap tracking CoinDesk 20 Index fell 23.2%.

By mid-July 2025, the CoinDesk 80 Index was down 38% year-to-date, whereas the CoinDesk 5 Index, which tracks Bitcoin, Ethereum, and three other major tokens, gained between 12% and 13% over the same period.

Andrew Baehr of CoinDesk Indices, in an interview with ETF.com, described this phenomenon as "identical correlation, vastly different profit and loss performance."

The correlation between the CoinDesk 5 Index and the CoinDesk 80 Index was as high as 0.9, meaning their price movements were completely aligned in direction, but the former achieved modest double-digit growth while the latter crashed nearly 40%.

It turns out that the diversification benefits from holding small-cap altcoins were minimal, while the performance cost was severe.

The performance of the small-cap asset sector was even worse. According to Bloomberg, by November 2025, the MarketVector Digital Assets 100 Small-Cap Index had fallen to its lowest level since November 2020.

Over the past five years, this small-cap index had a return of approximately -8%, while the corresponding large-cap index surged about 380%. Institutional capital clearly favored large-cap assets, avoiding tail risks.

Looking at the performance of altcoins in 2024, the Kaiko small-cap index fell over 30% for the year, and mid-cap tokens also struggled to keep up with Bitcoin's gains.

Market winners were highly concentrated in a few top tokens, such as SOL and Ripple (XRP). Although the share of altcoin trading volume once rebounded to 2021 highs in 2024, 64% of the trading volume was concentrated in the top ten altcoins.

Liquidity in the cryptocurrency market did not disappear; it migrated towards higher-value assets.

Sharpe Ratio and Drawdown Magnitude

If compared from a risk-adjusted return perspective, the gap widens further. The CoinDesk 80 Index and various small-cap altcoin indices not only had deeply negative returns but also exhibited volatility comparable to or higher than stocks.

The CoinDesk 80 Index crashed 46.4% in a single quarter; the MarketVector small-cap index, after another round of declines, fell to pandemic-era lows in November.

The overall altcoin indices experienced multiple index-level halving drawdowns: the Kaiko small-cap index fell over 30% in 2024, the CoinDesk 80 Index plummeted 46% in Q1 2025, and the small-cap index fell again to 2020 lows by the end of 2025.

In contrast, the S&P 500 and Nasdaq 100 indices achieved cumulative returns of 25% and 17% over the two years, with maximum drawdowns only in the mid-to-high single digits. The U.S. stock market had fluctuations, but they were overall manageable; the volatility of cryptocurrency indices, however, was highly destructive.

Even considering the high volatility of altcoins as a structural feature, their unit risk return from 2024 to 2025 was still far lower than that of holding major U.S. stock indices.

From 2024 to 2025, the overall altcoin index had a negative Sharpe ratio; the S&P and Nasdaq indices, even without volatility adjustment, showed strong Sharpe ratios. After volatility adjustment, the gap between them further widened.

Bitcoin Investors and Cryptocurrency Liquidity

The first insight from this data is the trend of liquidity concentration and migration towards high-value assets. Reports from Bloomberg and Whalebook on the MarketVector Small-Cap Index both pointed out that since early 2024, small-cap altcoins have consistently underperformed, while institutional funds flowed into Bitcoin and Ethereum ETFs.

Combined with Kaiko's observations, although the share of altcoin trading volume rebounded to 2021 levels, funds were concentrated in the top ten altcoins. The market trend is clear: liquidity did not completely leave the cryptocurrency market; it migrated towards high-value assets.

The previous altcoin bull market was essentially just a basis trade strategy, not a structural outperformance of assets. In December 2024, the CryptoRank Altcoin Season Index once soared to 88 points, only to crash to 16 points in April 2025, completely erasing all gains.

The 2024 altcoin bull market ultimately turned into a typical bubble burst; by mid-2025, the overall altcoin portfolio had given back almost all its gains, while the S&P and Nasdaq indices continued to compound growth.

For wealth advisors and asset allocators considering diversification beyond Bitcoin and Ethereum, the data from CoinDesk provides a clear case reference.

As of mid-July 2025, the large-cap tracking CoinDesk 5 Index achieved modest double-digit growth year-to-date, while the diversified altcoin index CoinDesk 80 plummeted nearly 40%, yet their correlation was as high as 0.9.

Investors allocating to small-cap altcoins did not gain substantial diversification benefits; instead, they suffered far higher return losses and drawdown risks compared to Bitcoin, Ethereum, and U.S. stocks, while still being exposed to the same macro drivers.

Current capital views most altcoins as tactical trading instruments, not strategic allocation assets. From 2024 to 2025, Bitcoin and Ethereum spot ETFs had significantly better risk-adjusted returns, and U.S. stocks also performed brilliantly.

Liquidity in the altcoin market is increasingly concentrating towards a few "institutional-grade coins," such as SOL, Ripple (XRP), and other tokens with independent positive catalysts or clear regulatory prospects. Asset diversity at the index level is being squeezed by the market.

In 2025, the S&P 500 and Nasdaq 100 indices rose about 17%, while the CoinDesk 80 cryptocurrency index fell 40%, and small-cap cryptocurrencies fell 30%

What Does This Mean for Liquidity in the Next Market Cycle?

The market performance from 2024 to 2025 tested whether altcoins could achieve diversification value or outperform in an environment of rising macro risk appetite. During this period, U.S. stocks achieved double-digit growth for two consecutive years with manageable drawdowns.

Bitcoin and Ethereum gained institutional recognition through spot ETFs and benefited from a moderating regulatory environment.

In contrast, the overall altcoin indices not only had negative returns and larger drawdowns but also maintained high correlation with major crypto tokens and stocks, yet failed to provide adequate compensation for the additional risk investors undertook.

Institutional capital always chases performance. The five-year return of the MarketVector Small-Cap Index was -8%, while the corresponding large-cap index surged 380%. This gap reflects capital's continuous shift towards assets with clear regulation, sufficient derivatives market liquidity, and well-developed custody infrastructure.

The CoinDesk 80 Index's 46% crash in the first quarter and its 38% year-to-date decline by mid-July indicate that the trend of capital migration towards high-value assets is not reversing but accelerating.

For Bitcoin and Ethereum investors evaluating whether to allocate to small-cap crypto tokens, the data from 2024 to 2025 provides a clear answer: the absolute returns of overall altcoin portfolios underperformed U.S. stocks, their risk-adjusted returns were inferior to Bitcoin and Ethereum; despite a high correlation of 0.9 with major crypto tokens, they provided no diversification value.