Author: Wall Street Insights

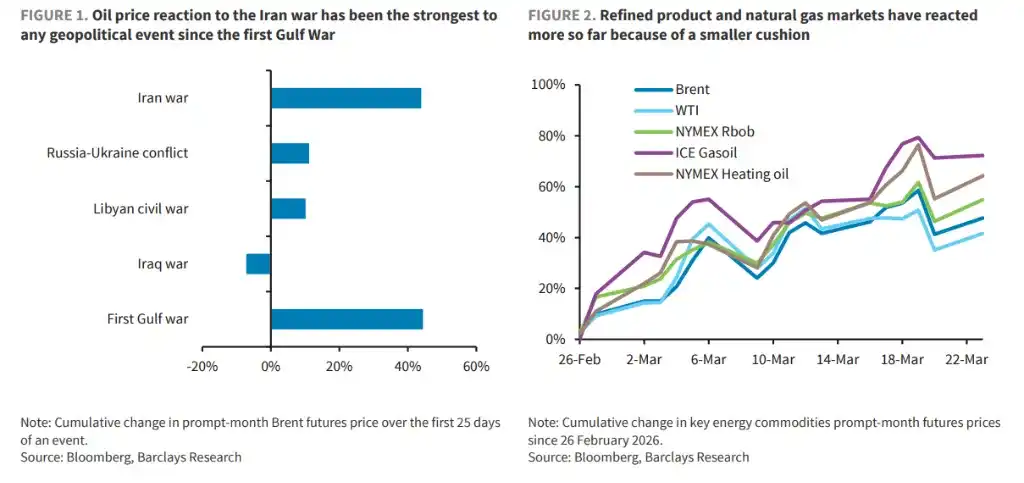

The Iran War has become the strongest geopolitical shock to the global energy market since the 1990 Gulf War.

Since the outbreak of the Iran War on February 26, 2026, Brent crude has surged 44% in just 25 days, U.S. gasoline wholesale prices (Rbob) have risen 48%, U.S. diesel prices have increased 51%, and European diesel prices have jumped 58%.

Barclays Capital's latest research report warns: When the war ends will directly determine whether oil prices return to the baseline scenario of $85 per barrel or break through $110 per barrel. For investors, five key catalytic factors—military objective progress, congressional funding battles, U.S. military casualty numbers, retail gasoline prices, and Trump's personal judgment—are the critical variables for current energy market pricing.

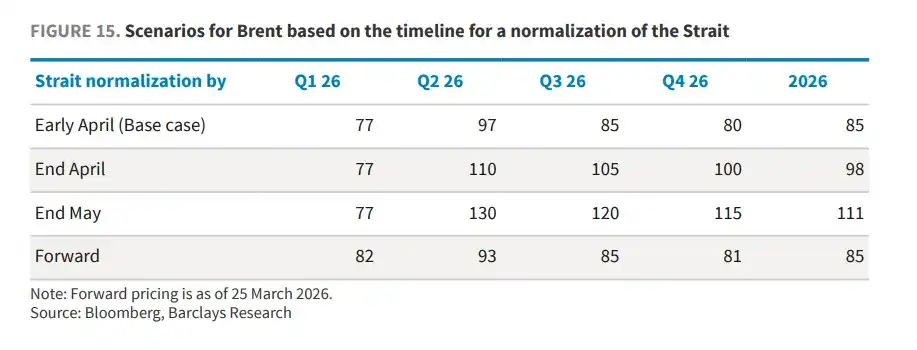

Barclays believes that oil price trends will diverge at three key time nodes: If the Strait of Hormuz returns to normal passage by early April, Barclays maintains its baseline forecast of an average Brent crude price of $85 per barrel for 2026; if delayed until late April, the average price may be repriced to around $98 per barrel; if prolonged until the end of May, the average price could reach $111 per barrel. Each day of delay causes the accumulated inventory shortfall to snowball, pushing the price center higher.

Five Key Factors: Core Variables Determining the War's Endgame

Barclays public policy analyst Michael McLean identifies five potential catalysts that could end the Iran War:

Key Point One: Achievement of Military Objectives

According to CCTV News, the U.S. previously defined three objectives for Iran: destroy Iran's ballistic missile and drone capabilities; strike the Iranian navy to maintain passage through the Strait of Hormuz; and destroy Iran's military and industrial base, rendering it incapable of external attacks for years. Notably, the objectives do not include regime change or Iran's nuclear program.

President Trump initially estimated the operation would last "four to five weeks." The war is now in its third week, and according to the White House's stance, it may be at the midpoint.

However, judging by the number of targets struck, the U.S. Central Command has not yet shown a clear inflection point of action contraction, with additional forces continuing to be deployed. Although the frequency of Iranian ballistic missile and drone attacks on the UAE, Kuwait, Saudi Arabia, and Bahrain has significantly decreased, they have not completely ceased, indicating Iran still retains some offensive capability. Barclays believes that until these indicators decrease further, it cannot be determined that the objectives have been achieved.

Key Point Two: Congressional Constraints—The War Powers Act Sets a Hard Deadline of May 31

The War Powers Act stipulates that within 60 days of deploying armed forces and submitting a report to Congress, the President must obtain congressional authorization (AUMF). The President can extend this by an additional 30 days. After 90 days, military operations must be terminated. Trump submitted the report on March 2, making the 90-day hard deadline May 31.

An AUMF requires 60 votes to pass in the Senate, and Republicans currently hold only 53 seats. Democrats have already expressed their stance through two opposing resolution votes—therefore, an AUMF is highly unlikely to pass. May 31 is the institutional hard boundary for the war's end.

The economic cost of the war is also accumulating rapidly: the first week cost approximately $11 to $12 billion, the current daily operational cost has dropped to about $500 million, and the total cumulative expenditure to date is estimated at around $21 billion.

For comparison, the nominal cost of the 13-year Iraq War was $815 billion; the total discretionary defense expenditure for fiscal year 2026 is $839 billion. Additionally, the "One Big Beautiful Bill" has pre-allocated $150 billion to the Department of Defense, providing some temporary financial buffer.

Key Point Three: Rising U.S. Military Casualties Will Further Erode Public Support

Barclays states that domestic support for this war in the U.S. is fragile and shows clear partisan division.

As of March 22, the RealClearPolitics poll average shows: support rate is only 41%, opposition rate is 49%. President Trump's overall approval rating has slightly decreased from 43% to 42%, the lowest record of his second term (the lowest of his first term was 37% in December 2017).

Thirteen U.S. military personnel have been killed so far.

Historical experience shows that wars usually bring a "rally-around-the-flag" effect, giving the president a short-term boost in support, but Trump has not gained this effect. The general rule is: the longer the war, the higher the casualties, and the more pessimistic the public is about the prospect of victory, the stronger the anti-war sentiment becomes.

Key Point Four: Gasoline Prices Hitting the "Political Red Line"—$5/Gallon is the Key Threshold

In July 2022, during the Biden administration, the national average gasoline price peaked at $5.01 per gallon.

For Republicans, not exceeding this "Biden peak" is a psychological political defense line, corresponding to a WTI oil price of about $120 per barrel, more than 20% above the current oil price.

Currently, Republican officials remain relatively optimistic, believing that even if oil prices are under short-term pressure, there is enough time for them to fall back by Labor Day (before investors truly start paying attention to the midterm elections) as the war ends. The administration has also taken a series of measures to try to alleviate oil price pressures, including releasing strategic reserves and exempting related sanctions.

Key Point Five: Trump "Declaring Victory" and Proactively Shifting Course

Barclays believes that, regardless of the actual progress on the battlefield, there is always the possibility that Trump may proactively declare victory and end the war at some point. Previously, when asked how he would judge when the war should end, Trump's answer was intriguing—"when I feel it in my bones".

Barclays clearly states that the timing of this catalytic factor is almost completely unpredictable.

In communications with clients, a mainstream analogy suggests: Trump's previous policy U-turn after "Liberation Day" (the tariff announcement on April 2, 2025) has conditioned investors to reflexively believe that a market plunge can drive Trump to shift course.

However, Barclays believes the market's reaction so far is not "panicked" enough: the S&P 500 fell about 12% after Liberation Day, while it has only fallen about 5% since this war began; the 10-year Treasury yield jumped 60 basis points after Liberation Day, but has only risen about 40 basis points this time; investment-grade credit spreads widened 26 basis points after Liberation Day, with a peak widening of only 9 basis points this time. More importantly, pausing a tariff executive order is far easier than ending a real war.

Significant Upside Risk Skew in Oil Prices

Barclays' core judgment is: the current oil price increase is not a speculative bubble, but a reflection of real supply-demand imbalance.

Before the war, Brent crude was undervalued by about 19% relative to the historical fair value implied by OECD inventory levels, and undervalued by about 15% relative to the replacement cost model; the net speculative long positions for Brent and WTI were at the 2nd percentile of historical extremes since 2014 at the end of 2025.

The dynamic evolution of the five catalytic factors—military objective progress, congressional funding battles, U.S. military casualty numbers, retail gasoline prices, and Trump's personal judgment—will be the most important high-frequency tracking dimensions for judging the direction of the energy market going forward. Barclays clearly states that, given the uncertainties, the risk to its 2026 Brent crude forecast of $85 per barrel is skewed to the upside.