Author: Changan, Biteye Content Team

A few days ago, many KOLs on X suddenly discovered that the badges symbolizing their partnership with Kalshi had disappeared from their accounts.

Prediction News reported on this incident, and soon after, a screenshot that was hard not to laugh at surfaced: Polymarket's official account had quietly liked this report.

The business war between Polymarket and Kalshi has been going on for a long time, and the prediction market is truly entering an era of duopoly.

On one side is the crypto-native Polymarket, on the other is Kalshi from the compliant financial system.

The essence of this competition is not about which company is stronger, but rather: who will own the pricing power of future information, Crypto or Wall Street.

Therefore, this analysis is worth doing.👇

I. Business War Chronicles: From Regulatory Games to Offline Showdowns

Over the past year, the competition between the two has escalated from product-level to a multi-front war involving channels, regulation, and public opinion.

1. Valuation Race: A 41-Day Capital Counterattack

On October 7, 2025, Polymarket announced a $2 billion strategic investment from ICE, valuing the company at $9 billion.

Three days later, Kalshi announced the completion of a $300 million Series D funding round, with a valuation of $5 billion. The timing was so precise it was hard to believe it was just a coincidence.

But Polymarket clearly wasn't ready to stop. On October 23, Bloomberg reported that Polymarket was in talks with investors to prepare for a new funding round, targeting a valuation of $15 billion.

On November 20, Kalshi's response arrived: it completed a $1 billion funding round, with its valuation jumping directly to $11 billion, led by Paradigm. This not only surpassed Polymarket's previous $9 billion valuation but also rapidly approached that $15 billion funding target. Only 41 days had passed since its last Series D announcement.

2. Cultural Breakthrough: The Traffic Battle

On September 24, 2025, the trailer for Season 27, Episode 5 of "South Park," titled "Conflict of Interest," was released, indicating the episode would feature content related to prediction markets.

As soon as the news broke, both platforms simultaneously recognized the opportunity—this was the first time prediction markets entered the视野 (vision/field of view) of mainstream culture. Whoever could first convert this attention into trading volume would get a larger piece of the breakout红利 (dividend/benefit).

Kalshi and Polymarket quickly launched a batch of markets highly relevant to the plot, allowing users to bet on the storyline's direction on their respective platforms immediately.

On the day the episode aired, the Kalshi team collectively changed their X profile pictures to South Park cartoon avatars, flooding X and embedding their brand firmly into the day's hot discussions. These two platforms don't miss any marketing opportunity to convert热点 (hot topics/trends) into transactions.

3. Affiliate Accounts and Badge Wars

As platform user numbers膨胀 (swelled/expanded) rapidly, Polymarket and Kalshi almost simultaneously launched their respective affiliate account programs in the latter half of last year,开始 (beginning) to award badges to KOLs, traders, and ecosystem projects on X.

Polymarket moved faster: The Trader badge was used to certify active traders, encouraging them to share strategies and持仓 (position/holding) views on X,引流 (diverting traffic/leading users) to the platform. The Builder badge was aimed at ecosystem project teams, attracting developers to build applications on the platform, gaining more exposure with official endorsement.

At the same time, Polymarket also配套推出 (rolled out a配套/supporting) $1 million Builders incentive program, directly using real money to pull developers into the ecosystem.

Kalshi quickly followed suit, launching a broader badge system covering sports, culture, trader certification, and other sectors, replicating this model in the sports and mass market areas where it held more advantage.

Now, prediction market traders on Twitter either sport a Polymarket badge or a Kalshi badge.

4. Physical Marketing Duel: Manhattan Free Goods War

On February 2, 2026, Kalshi announced on X that it would provide free food at Westside Market grocery store the next day from noon to 3 PM, with a limit of $50 per person. As soon as the news broke, long lines formed quickly, with students and low-income人群 (crowds/people) swarming in, creating a quite火爆 (booming/lively) scene.

nThe next day, February 3rd, Polymarket quickly responded, announcing it would open its first free food pop-up store in New York, open to the public for 5 consecutive days. The rules were simple: customers could fill and take away one handbag, no strings attached. At the same time, Polymarket also announced a $1 million donation to Food Bank for New York City to help address food security issues citywide.

The two events happened back-to-back, full of火药味 (gunpowder smell/strong competitive spirit).

5. Regulatory and Political Resource Arms Race

The lobbying machines of both sides in Washington have never stopped, both coincidentally bringing in Donald Trump Jr. for endorsement, aiming both to leverage Republican-aligned regulatory resources and to place political chips in the court of public opinion.

But beneath the surface, the real battlefield lies in two dimensions: the regulatory gaps at the CFTC and the offensive and defensive battles against injunctions in various state courts.

Polymarket,凭借 (relying on) its offshore structure to avoid direct regulatory火力 (firepower), quietly paved its way into the US market by acquiring QCEX; Kalshi chose to confront head-on, holding the CFTC's first prediction market license, but也因此 (thus also) becoming a live target for state attorneys general - at least 4 states have currently filed lawsuits against it, accusing it of illegally accepting bets from local users.

This场 (measure/instance of)朴实无华 (unadorned/unpretentious) business war is早已 (long since) no longer about product competition, but a full-scale war of political capital and traffic monopoly.

II. Hardcore Comparison: Deconstructing the Two Titans Across Five Dimensions

2.1 Trading Data Comparison: Misaligned Growth of Political Cycles and Sports Calendars

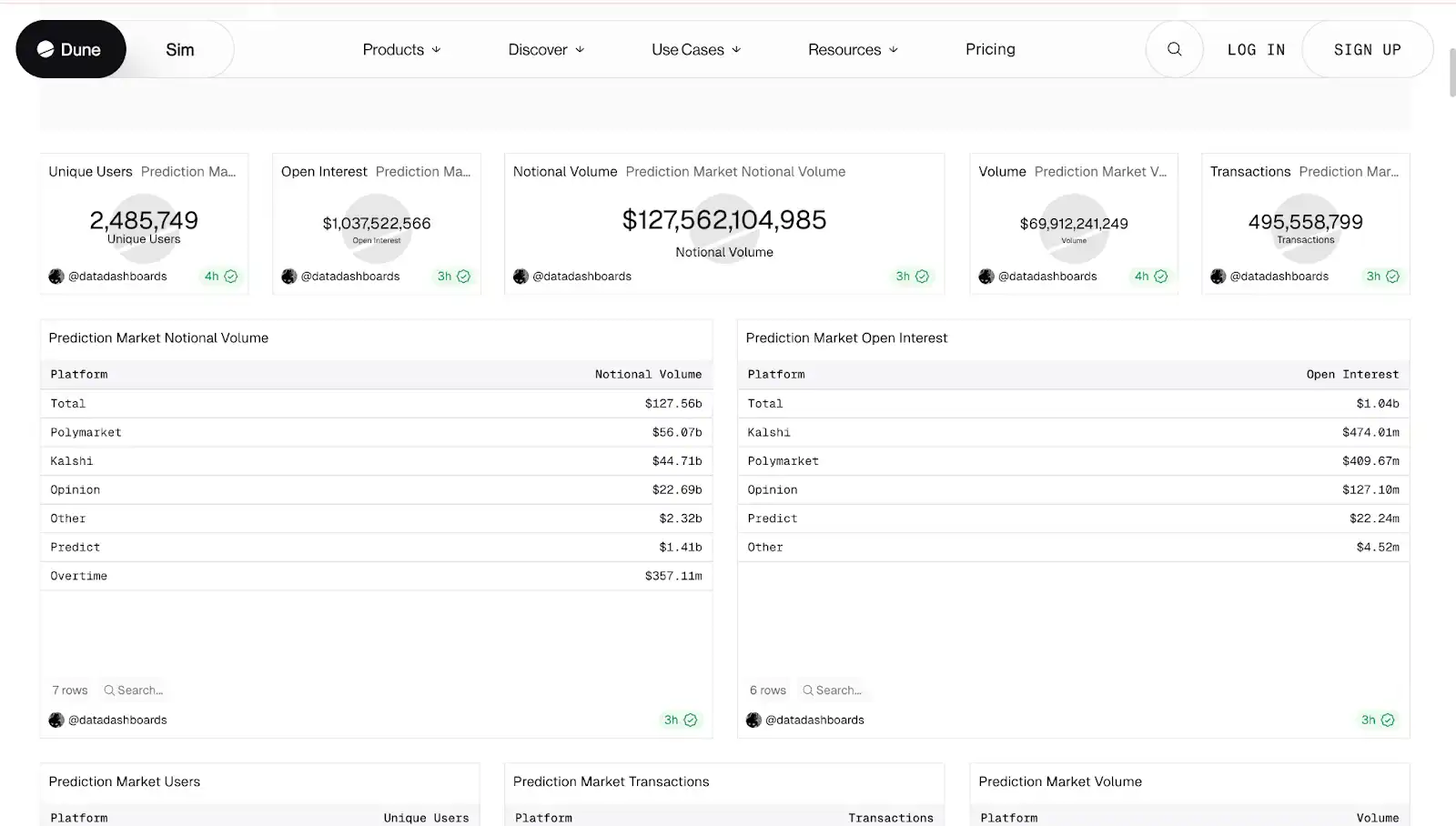

As of February 2026, the total Notional Volume for the prediction market industry was $127.5 billion, actual Volume was $69.9 billion, with 2.49 million unique users, and open interest突破 (breaking through) $1 billion.

Polymarket and Kalshi together account for approximately 79% of the market share. Polymarket ranks first with $56.07b Notional Volume, followed closely by Kalshi with $44.71b. In terms of Open Interest, Kalshi's $474.01m slightly leads Polymarket's $409.67m, with the two combined accounting for over 85% of the total market OI.

Trend-wise, the growth of both is highly event-driven. Polymarket's OI peaked around $500m during the October 2024 election before receding; Kalshi's OI saw rapid growth starting with the 2025 NFL season, reaching a historical high by the end of 2025.

Both platforms are growing in volume, but driven by different factors. One relies on political cycles, the other on sports calendars.

(Data source: Dune, cutoff time Feb 26, 11:00)

2.2 Revenue Comparison: Validated Dynamic Fees vs Nascent Taker Fee

The fee logic of the two platforms is fundamentally different.

Kalshi

Uses probability-weighted dynamic fees: Charges a trading fee based on the contract price, with the fee rate varying with the contract price, peaking at 50 (i.e., 50/50 probability), and decreasing towards 0 or 99. For a $100 trade, the maximum fee is about $1.74, with an effective fee rate of about 1.2%.

2024 revenue was $24 million, 2025 revenue was $260 million, a year-on-year increase of 994%. But revenue is highly concentrated in the sports season: the NFL season (Sept-Nov) alone contributed $138 million, with December's single-month revenue of $63.5 million setting a historical record. Revenue significantly drops during the off-season, showing clear seasonal characteristics.

Polymarket

Looking back at Polymarket, they took the completely opposite path. Until the end of 2025, Polymarket was operating at a loss, offering zero fees throughout, trading free access for users. It wasn't until this February that they officially implemented a Taker Fee dynamic fee structure in sports markets. In the first week after introducing fees, Polymarket's fee revenue exceeded $1 million. Data from DefiLlama shows Polymarket's revenue over the last 30 days is $3.18 million, with the revenue curve only starting to rise significantly from January this year.

It is worth noting that daily settlement markets might become a future revenue source for Polymarket. High-frequency, short-cycle markets generate more transactions. Similar to Meme stocks, users of this type of market are less sensitive to fees.

Comparison: Kalshi's fee model is validated but relies on the sports season. Polymarket's fee structure is just starting; its annual revenue, though not even a fraction of Kalshi's, signifies that Polymarket's phase of using zero fees to exchange for liquidity is over. Next, they are going to start doing business seriously.

2.3 User Profile: Licensed Elites vs Global Retail

The user structure of the two platforms is largely shaped by the regulatory environment.

Kalshi holds a CFTC license and can legally serve US users, with its business primarily concentrated in the US domestic market.

Polymarket returned to the US market at the end of 2025 by acquiring QCEX. In the years before that, it was primarily active overseas. This "exile period"反而 (instead) helped it accumulate a broader international user base.

The difference in users can also be seen from the revenue structure.

89% of Kalshi's revenue comes from sports markets. User behavior is closer to traditional sports betting: high trading frequency, relatively small single bet amounts, activity fluctuating with the season. Users grow rapidly when the NFL season starts, and trading volume noticeably decreases after the season ends, showing clear seasonal characteristics.

Polymarket's structure is completely different. Politics and macro markets occupy the core position, attracting many institutional-level traders to hedge macro risks here. Single bet amounts are significantly higher. During the 2024 US election, a French trader placed a single bet exceeding $50 million, ultimately profiting $85 million. Such volume is almost unheard of in sports betting markets.

2.4 Channel Moat: Distribution Agents vs Developer Ecosystem

At the end of 2025, both Robinhood and Coinbase launched prediction market features on their platforms, both partnering with Kalshi. It's not just brokerages integrating; sports platforms like PrizePicks and Underdog also directly channel their existing sports betting users to Kalshi. In December, Kalshi also joined forces with Coinbase, Robinhood, and Crypto.com to form the Prediction Market Alliance.

The logic is quite straightforward. Kalshi holds the Designated Contract Market (DCM) license issued by the CFTC. For licensed financial institutions, integrating its system is like connecting to a traditional futures exchange—clear processes, low compliance costs, and controllable risks.

Polymarket took a completely different direction. They didn't focus on channel distribution but rather on building a set of underlying infrastructure, hoping others would develop products around it.

The most obvious step in this strategy was the acquisition five days ago: Polymarket bought Dome, a project from Y Combinator's Fall 2025 batch. Dome provides a prediction market API; developers write code once and can simultaneously access data and liquidity from multiple platforms like Polymarket and Kalshi.

Now with Vibe Coding being hot, developers can directly call Dome's interface to build trading bots, data dashboards, and embedded market components. AI Agents can also use this API to automatically execute prediction trading strategies.

Putting the two paths side by side makes it clear. Kalshi is expanding channels, relying on partners to bring users and trading volume. Polymarket is building the foundation, hoping developers will spontaneously grow applications on top of it. One path leans more towards commercial network expansion, the other bets on the spontaneous formation of an ecosystem. Once the underlying layer truly achieves network effects, it will be very difficult for latecomers to replicate.

2.5 Marketing Strategy: Brand Exposure vs Community Virality

The marketing approaches of the two are highly consistent with their respective user structures.

Kalshi focuses on brand exposure, with a very traditional, direct approach. During the New York mayoral election, they plastered real-time odds advertisements in Times Square, Penn Station, and on subway trains, putting prediction probabilities directly on street screens. By the NBA Finals, Kalshi used AI tools to produce a $2000 TV commercial in two days, airing it during prime time, garnering over 3 million views on X.

Coupled with partnerships with CNN and CNBC, Kalshi's data can appear directly in live news broadcast graphics. For average viewers, this equates to official endorsement, naturally increasing trust.

Polymarket's approach is completely different, more偏向 (leaning towards) community self-propagation.

They designed the promotion mechanism in great detail. Users share their专属 (exclusive) link; the promoter gets $0.01 for each click. If the referred person deposits over $20, it triggers a $10 CPA (Cost Per Acquisition) reward.

When clicks and trading volume reach a certain scale, additional distribution rewards are available. The entire structure gives promoters持续 (sustained) motivation to attract new users, similar to the rebate link玩法 (play/mechanism) in meme trading platforms.

Additionally, Polymarket is also deliberately cultivating its own content ecosystem, such as supporting accounts like @BrosOnPM. These KOLs primarily serve prediction market builders and traders, outputting content daily, helping developers connect with traffic, and allowing the community to form its own internal circulation of传播 (propagation).

III. So, Who is the Ultimate King?

The previous section described what the two companies look like now, but the current landscape is not the future landscape. Prediction markets are still in their early stages, with too many variables - regulation is undecided, competitors are涌入 (pouring in), business models are not yet validated. Rather than giving a definitive conclusion, it's better to梳理 (tease out/sort out) the key issues that will truly determine the outcome.

Both are expanding into each other's core territories

Judging from the actions of both platforms, both have recognized their shortcomings and are starting to补课 (make up for lessons/catch up).

When Polymarket returned to the US market, the first batch of contracts launched were all sports-related. They later signed official partnerships with MLS, NHL, and the New York Rangers, using these league brands to endorse their sports markets. A platform that started with politics is now desperately trying to挤 (squeeze into) the sports circle.

The editor analyzes there might be two main reasons:

-

Political markets might暂时 (temporarily) be less favored by US regulators, sports markets are more easily accepted.

-

To capture Kalshi's market share in the US.

Kalshi那边也没闲着 (isn't idle either). They signed deals with CNN and CNBC, getting their odds data to appear in the on-screen graphics of live news broadcasts. A platform that started with sports is now trying to扎 (thrust/push) into the political track, attempting to establish media-level credibility.

But the risks for the two are not on the same scale. Polymarket has real trading volume in both politics and sports, while almost all of Kalshi's trading volume is concentrated on sports. This structural difference will become a very troublesome issue when discussing regulatory risks later.

The Biggest Channel Partner, or the Most Dangerous Competitor?

Robinhood is one of Kalshi's most important retail distribution channels, contributing over half of its trading volume in 2025. Coinbase has also launched prediction markets in all 50 US states, also clearing through Kalshi.

But both almost simultaneously made the same move:

-

Robinhood formed a joint venture with Susquehanna to acquire MIAXdx

-

Coinbase acquired The Clearing Company

Both companies are building their own CFTC-qualified exchange infrastructure, expected to be operational in 2026. After building their own, they can choose to continue cooperating with Kalshi and sharing revenue, or choose to keep this profit for themselves. By then, they will already have user data, trading habits, and liquidity积累 (accumulation).

For Kalshi, this is not just the risk of channel partners potentially leaving one day, but a specific threat with a timeline. Kalshi's channel moat is essentially a first-mover advantage with an expiration date.

Polymarket Fees: A Key Step in Validating the Business Model

Polymarket's trading volume exceeded $33.8 billion in 2025, yet its revenue was close to zero. But a $9B valuation ultimately needs revenue to support it; 2026 is the time to deliver.

Fee collection started with a pilot in cryptocurrency markets, then expanded to sports events on February 18, 2026. The logic behind this choice is clear: these are both daily settlement markets, with high trading frequency, relatively small single amounts, fast user turnover, and lower sensitivity to fees compared to long-cycle political macro contracts. Starting fees here has the least impact on core liquidity.

But the risks are also evident. Prediction market liquidity is entirely provided by users; there are no market makers to backstop. Once professional traders feel fees are eating into arbitrage opportunities, withdrawing is a matter of seconds.

Historically, many exchanges have seen liquidity rapidly deteriorate due to poorly timed or sized fee introductions,陷入 (falling into) a death spiral of declining liquidity → users leaving → even worse liquidity.

Polymarket is currently using maker rebates to hedge this risk, returning part of the fees collected from takers to those providing liquidity (makers), trying to maintain order book depth.

Whether it can establish stable revenue without driving away liquidity is the prerequisite for Polymarket's valuation logic to hold. The fee experiment has just begun; the answer will only become clear by the end of 2026.

Conclusion: A War Without a King, Only Winners of the Era

The prediction market industry is still very young; it's indeed too early to conclude who wins or loses now. But the outlines of the two companies are gradually becoming clear.

Kalshi's strengths are clear: it holds the first-mover advantage in compliance, has mature retail channels, and its revenue model is already proven. However, the pressures it faces are not small. Sports revenue占比 (proportion) is偏高 (on the high side), state-level regulatory uncertainty persists, and the timeline for Robinhood and Coinbase to build their own exchanges is approaching.

Polymarket's advantages are equally distinct: it has the deepest global liquidity,几乎没有对手 (almost no rivals) in the political and macro tracks, and a developer ecosystem is taking shape. But its business model is still being validated; whether the fee mechanism can truly work won't be known until the end of 2026.

The interesting part of this competition is that the current positions of the two companies do not completely overlap. Kalshi is expanding its retail scale, while Polymarket is more focused on information density and market depth. The real head-to-head confrontation will likely occur after Polymarket's US sports market matures and after Kalshi enhances its capabilities in political markets.

Until then, the industry space is still broad enough to accommodate the parallel development of both paths.