Entering 2026, the crypto market is undergoing a profound structural transformation. The long-repeated "four-year bull-bear cycle," which has been repeatedly validated, is losing its explanatory power for the market. It is being replaced by a structural evolution process where multiple asset logics operate in parallel, capital behaviors diverge, and price rhythms slow down. The market no longer rises and falls uniformly around a single narrative; instead, different types of assets are priced independently at their respective stages. The cycle has degenerated from a core variable determining direction to a background factor influencing rhythm.

I. The Cycle Is Failing: Why We No Longer Use "Bull and Bear" to Understand the Crypto Market in 2026

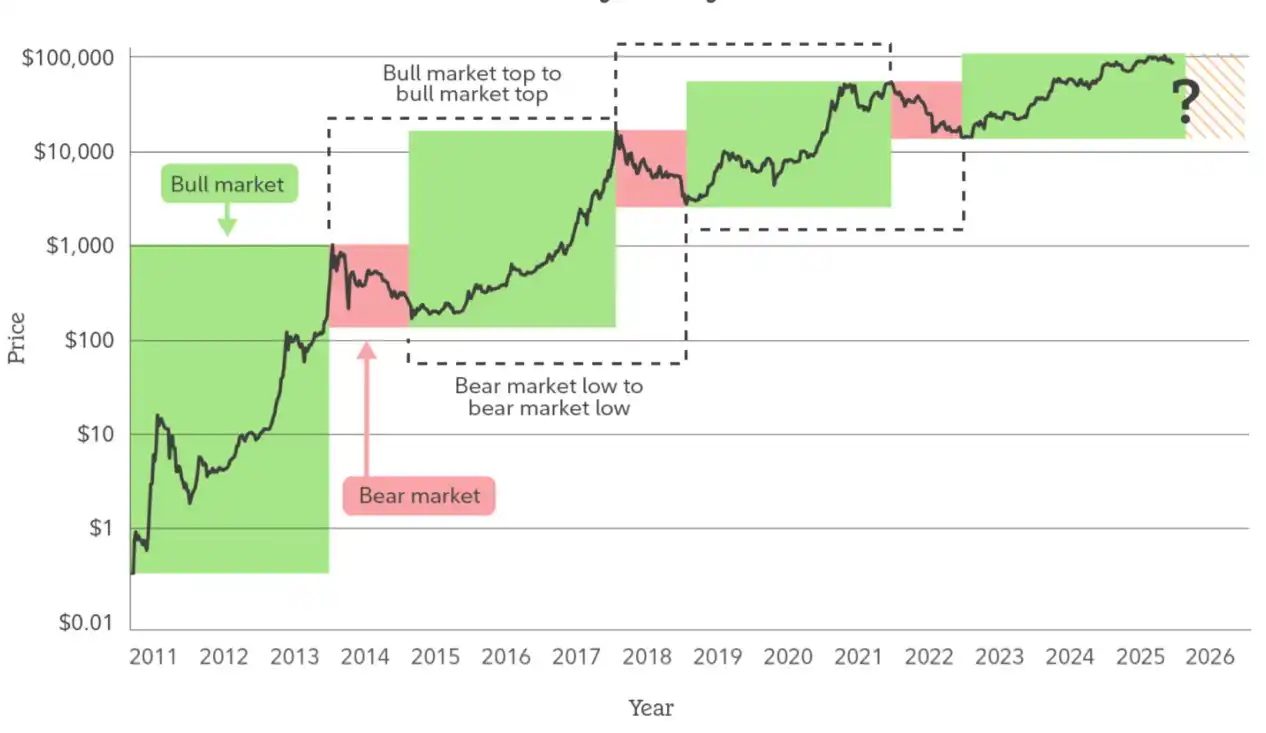

For a long time, the crypto market was almost entirely dominated by the single narrative of the "four-year bull-bear cycle." Halving points, liquidity inflection points, emotional bubbles, and price collapses were repeatedly validated as effective analytical tools, shaping the cognitive habits of a generation of market participants. However, as the market moved into 2025 and beyond, this once highly effective cycle model began to show a systematic decline in explanatory power: market trends did not exhibit extreme polarization at key time nodes, pullbacks were no longer accompanied by comprehensive liquidity stampedes, so-called "bull market start signals" frequently failed, and price movements increasingly showed a state of range-bound fluctuations, structural differentiation, and slow upward movement coexisting. This is not the market "becoming boring" but rather a deep-seated change in its operating mechanism.

The essence of the cycle model relies on highly homogeneous capital behavior: similar risk appetites, comparable holding periods, and high sensitivity to price itself. However, the crypto market around 2026 is gradually moving away from this premise. With the opening of compliant channels, the maturation of institutional-grade custody and audit systems, and the inclusion of crypto assets in broader asset allocation discussions, the marginal pricing power in the market has changed. An increasing amount of capital is entering the market not with "timing trades" as the core objective but rather with long-term allocation, risk hedging, or functional use as the starting point. This type of capital does not chase extreme volatility; instead, it absorbs liquidity during downturns and reduces turnover during uptrends. Its very existence weakens the emotional feedback loop that traditional bull-bear cycles rely on.

More importantly, the increasing complexity of the internal structure of the crypto market is also dismantling the cycle hypothesis of "uniform rise and fall." The logical differences between Bitcoin, stablecoins, RWA, public chain assets, and application tokens are continuously magnified. Their corresponding funding sources, usage scenarios, and value anchoring methods can no longer be covered by the same cycle language. As Bitcoin increasingly resembles a medium- to long-term value reserve tool, stablecoins become the infrastructure for cross-border settlements and on-chain finance, and some application assets begin to be priced based on cash flow and real demand, the terms "bull market" or "bear market" themselves lose their meaning as a unified descriptive framework.

Therefore, a more reasonable way to understand the crypto market in 2026 is not "whether the next bull market has begun" but "whether the structural stages of different assets have changed." The cycle has not disappeared, but it is degenerating from a core variable determining direction to a background factor influencing rhythm. The market no longer resonates rapidly around a central narrative but evolves slowly in a state of multiple parallel logics. This means that future risks are no longer concentrated in a single top collapse but are more reflected in structural mismatches and cognitive lags. Similarly, opportunities no longer come from betting on overall market trends but from early identification of long-term trends and role differentiation.

From this perspective, the "failure" of the cycle is not the price of the crypto market maturing but rather a sign that it is beginning to shed its early speculative attributes and move toward a systematic asset stage. The crypto market in 2026 no longer needs bulls and bears to define its path; instead, it requires structure, function, and time to understand its true operating state.

II. Bitcoin's Role Shift: From High-Volatility Asset to Structural Reserve Tool

If the cycle logic is failing, then Bitcoin's own role shift is the most direct and explanatory manifestation of this change. For a long time, Bitcoin was regarded as the asset with the highest volatility and the most concentrated risk premium in the crypto market. Its price fluctuations were driven more by sentiment, liquidity, and narratives rather than stable usage demand or asset-liability structures. However, entering 2025, this perception is gradually being revised: Bitcoin's price volatility continues to decline, its pullback structure becomes smoother, the stability of key support levels significantly strengthens, and the market's sensitivity to short-term gains and losses is decreasing. This is not a decline in speculative enthusiasm but rather Bitcoin being reincorporated into a pricing framework more inclined toward a "reserve asset."

The core of this shift lies not in whether Bitcoin is "more expensive" but in "who holds it and for what purpose." As Bitcoin is incorporated into the balance sheets of listed companies, long-term capital portfolios, and discussions on asset allocation by some sovereign or quasi-sovereign entities, its holding logic has shifted from seeking price elasticity to hedging against macroeconomic uncertainty, diversifying fiat currency risks, and gaining exposure to non-sovereign assets. Unlike the early retail-dominated market, these holders have higher tolerance for price pullbacks, greater patience with time, and their behavior itself compresses Bitcoin's circulating supply and reduces the overall market's selling pressure elasticity.

At the same time, Bitcoin's financialization path is also undergoing structural changes. Spot ETFs, compliant custody, and mature derivative systems have given Bitcoin the infrastructure conditions to be incorporated into the traditional financial system on a large scale for the first time. This does not mean Bitcoin has been completely "tamed," but its risks are being repriced: price discovery no longer occurs entirely in the most emotionally extreme on-chain or offshore markets but is gradually shifting to trading environments with greater depth and constraints. In this process, Bitcoin's volatility has not disappeared but has transformed from无序剧烈震荡 (disorderly剧烈震荡)剧烈震荡 (violent fluctuations) into structural fluctuations围绕宏观变量与资金节奏 (围绕宏观变量与资金节奏)围绕宏观变量与资金节奏 (revolving around macroeconomic variables and capital rhythms).

More importantly, Bitcoin's "reserve attribute" does not stem from any external credit endorsement but from the result of its supply mechanism, immutability, and decentralized consensus being repeatedly validated through long-term operation. Against the backdrop of expanding global debt规模持续扩张 (scale持续扩张),加剧的地缘政治与金融体系碎片化 (intensifying geopolitical and financial system fragmentation), the demand for "neutral assets" is rising. Bitcoin does not need to assume traditional monetary functions but, at the asset level, is gradually becoming a value carrier that does not require counterparty credit, policy promises, and can be transferred across systems. This attribute positions it in asset allocation closer to a structural reserve tool rather than a单纯的高风险投机标的 (单纯的高风险投机标的)单纯的高风险投机标的 (purely high-risk speculative asset).

Therefore, Bitcoin in 2026 is no longer suitable for measuring its value by "how fast it rises" but should be placed under a longer-cycle配置与博弈视角 (配置与博弈视角)配置与博弈视角 (allocation and gaming perspective). Its core significance lies not in replacing any existing asset but in providing a new, decentralized reserve option for the global asset system. It is in this role shift that Bitcoin's way of influencing the crypto market has also changed: it is no longer just the engine of market trends but is becoming the anchor point for the stability of the entire system. As this transformation deepens, Bitcoin's very existence may be more important for the crypto market in 2026 and beyond than its short-term price performance.

III. Stablecoins and RWA: The Crypto Market's First Real Integration into the Real Financial Structure

If Bitcoin accomplishes the crypto market's "self-affirmation" at the asset level, then the rise of stablecoins and RWA marks the crypto market's first systematic integration into the real world's financial structure. Unlike growth driven by narratives, leverage, or token incentives in the past, the core of this change is not emotional expansion but the continuous entry of real assets, real cash flows, and real settlement demands into the on-chain system. This pushes the crypto market from a relatively closed self-circulating system to an open structure deeply coupled with real finance.

The role played by stablecoins far exceeds that of a "medium of exchange" or "safe-haven tool." As their scale continues to expand and usage scenarios persistently spill over, stablecoins have effectively become a "chain-based mapping" of the global dollar system: with lower settlement costs, higher programmability, and cross-regional accessibility, they undertake functions such as cross-border payments, on-chain清算 (清算)清算 (clearing), fund management, and liquidity allocation. Especially in emerging markets, foreign trade settlements, and high-frequency cross-border capital flows, stablecoins do not replace the existing financial system but rather补足其在效率与可达性上的结构性短板 (补足其在效率与可达性上的结构性短板)补足其在效率与可达性上的结构性短板 (compensate for its structural shortcomings in efficiency and accessibility). This usage demand does not depend on bull-bear cycles but is highly related to global trade, capital flows, and financial infrastructure upgrades. Its stability and stickiness are far higher than traditional crypto trading demand. Building on stablecoins, the emergence of RWA further changes the logic of asset composition in the crypto market. By mapping real-world assets such as U.S. Treasury bonds, money market instruments, accounts receivable, and precious metals into on-chain tokens, RWA actually introduces a long-missing element into the crypto market—a sustainable source of收益 (收益)收益 (income) tied to the real economy. This means that the crypto market no longer relies entirely on "price increases" to support asset value for the first time. Instead, it can construct value anchors closer to traditional finance through interest, rent, or operational cash flow. This change not only enhances asset pricing transparency but also causes on-chain funds to begin reconfiguring around "risk-return" rather than a single narrative.

A deeper change is that stablecoins and RWA are reshaping the financial division of labor within the crypto market. Stablecoins provide the underlying settlement and liquidity foundation, RWA provides exposure to real assets that can be split, combined, and reused, and smart contracts are responsible for automated execution and risk control. Under this framework, the crypto market is no longer just a "shadow market" of traditional finance but begins to possess the ability to independently承载金融活动 (承载金融活动)承载金融活动 (carry out financial activities). The formation of this capability is not achieved overnight but accumulates slowly and steadily through the gradual improvement of compliance, custody, audit, and technical standards. Therefore, stablecoins and RWA in 2026 should not be simply understood as "new tracks" or "thematic investments" but should be regarded as key nodes in the structural upgrade of the crypto market. They enable the crypto system to possess the possibility of long-term coexistence and mutual penetration with real finance for the first time. They also shift the growth logic of the crypto market from cycle-driven to demand-driven, from closed games to open collaboration. In this process, what truly matters is not the short-term performance of individual projects but the crypto market正在形成一种新的金融基础设施形态 (正在形成一种新的金融基础设施形态)正在形成一种新的金融基础设施形态 (is forming a new form of financial infrastructure), whose impact will far exceed the price level and profoundly change the operating methods of global finance in the next decade.

IV. From Narrative-Driven to Efficiency-Driven: The Collective Repricing of the Application Layer

After experiencing multiple cycles of narrative rotation, the application layer of the crypto market is reaching a critical inflection point: the valuation system driven solely by grand visions, technical labels, or emotional consensus is systematically failing. The阶段性退潮 (阶段性退潮)阶段性退潮 (phased ebb) of DeFi, NFTs, GameFi, and even some AI narratives does not mean these directions themselves lack value. Instead, the market's tolerance for "future imagination premium" has significantly decreased. The application layer around 2026 is transitioning from a story-centric pricing system to a new pricing logic centered on efficiency, sustainability, and real usage intensity.

The essence of this shift lies in the changed participant structure of the crypto market. As the proportion of institutional funds, industrial capital, and hedging funds increases, the market no longer focuses only on "whether a big enough story can be told" but cares more about "whether it actually solves a real-world problem, whether it has cost or efficiency advantages, and whether it can operate sustainably without relying on subsidies." Under this scrutiny framework, many applications that were once overvalued are being repriced, while a few protocols with advantages in efficiency, experience, and cost structure are反而获得了更稳定的资本支持 (反而获得了更稳定的资本支持)反而获得了更稳定的资本支持 (instead receiving more stable capital support).

The core manifestation of efficiency-driven competition is that the application layer begins to compete around "output per unit of capital" and "contribution per user." Whether it is decentralized exchanges, lending, payments, or basic middleware, the market's focus is shifting from crude indicators like TVL and registered user numbers to trading depth, retention rates, fee income, and capital turnover efficiency. This means that applications are no longer just "narrative decorations" for the underlying public chain ecosystem but become independent economic entities that need to be self-sustaining and have clear business logic. For applications that cannot generate positive cash flow or highly rely on incentive subsidies, the weight of "future expectations" in their valuation is being rapidly compressed.

At the same time, technological progress is放大效率差异 (放大效率差异)放大效率差异 (amplifying efficiency differences), accelerating the differentiation of the application layer. The maturation of account abstraction, modular architecture, cross-chain communication, and high-performance Layer2 has made user experience and development costs quantifiable and comparable metrics. In this context, the migration cost for users and developers continues to decrease. Applications no longer have "natural moats"; only products that form significant advantages in performance, cost, or experience can retain traffic and capital. This competitive environment is naturally unfavorable for projects that "maintain premium through narratives" but provides long-term生存空间 (生存空间)生存空间 (living space) for truly efficient infrastructure and applications.

More importantly, the repricing of the application layer does not occur in isolation but resonates with the role shifts of stablecoins, RWA, and Bitcoin. When the chain begins to carry more real economic activities, the value of applications no longer comes from "internal循环博弈 (循环博弈)循环博弈 (circular games) within crypto" but from whether they can efficiently undertake real capital flows and real demand. This causes applications serving payments, settlements, asset management, risk hedging, and data coordination to gradually replace purely speculative applications and become the core of market attention. This change does not mean market risk appetite has completely disappeared, but the distribution method of risk premium has shifted, moving from narrative diffusion to efficiency realization.

Therefore, the "collective repricing" of the application layer in 2026 is not a short-term style shift but a structural value reassessment. It marks the crypto market gradually摆脱对情绪与故事的高度依赖 (摆脱对情绪与故事的高度依赖)摆脱对情绪与故事的高度依赖 (shedding its high dependence on sentiment and stories),转而以效率、可持续性和现实适配度作为核心评价标准 (转而以效率、可持续性和现实适配度作为核心评价标准)转而以效率、可持续性和现实适配度作为核心评价标准 (turning instead to efficiency, sustainability, and现实适配度 (现实适配度)现实适配度 (real-world suitability) as core evaluation criteria). In this process, the application layer will no longer be the most volatile part of the cycle but may become a key bridge connecting the crypto market to the real economy. Its long-term value will also depend more on whether it truly integrates into the operating system of the global digital economy.

V. Conclusion: 2026 Is Not the Start of a New Bull Market, But the Start of the Next Decade

If one still tries to understand the crypto market in 2026 by asking "when will the next bull market come," it本身就意味着站在了一个正在失效的分析框架之中 (本身就意味着站在了一个正在失效的分析框架之中)本身就意味着站在了一个正在失效的分析框架之中 (itself means standing within an analytical framework that is becoming obsolete). The greater significance of 2026 lies not in whether prices reach new highs but in the crypto market completing a migration of underlying cognition and structure: it is beginning to transition from a marginal market highly dependent on cycle narratives, emotional diffusion, and liquidity games to a long-term infrastructure system embedded in the real financial system, serving real economic needs, and gradually forming an institutionalized operating logic.

This change is first reflected in the alteration of market goals. Over the past decade, the core question for the crypto market was "how to prove its own reason for existence." After 2026, this question is being replaced by "how to operate more efficiently, how to collaborate with real systems, and how to carry larger scales of capital and users." Bitcoin is no longer just a high-volatility risk asset but is beginning to be纳入结构性储备与宏观配置框架 (纳入结构性储备与宏观配置框架)纳入结构性储备与宏观配置框架 (incorporated into structural reserve and macro allocation frameworks); stablecoins have evolved from a medium of exchange to a key outlet for digital dollars and digital liquidity; RWA, for the first time, truly connects the crypto system to global debt, commodity, and settlement networks. These changes will not bring intense price狂欢 (狂欢)狂欢 (carnivals) in the short term, but they determine the boundaries and上限 (上限)上限 (upper limits) of the crypto market for the next decade.

More importantly, 2026 marks the completion of the "paradigm shift," not its beginning. From cycle games to structural games, from narrative pricing to efficiency pricing, from closed internal crypto cycles to deep coupling with the real economy, the crypto market is forming a new value assessment system. In this system, whether an asset has long-term allocation value, whether a protocol can continuously generate cash flow, and whether an application truly improves financial and collaboration efficiency begin to matter more than "whether the narrative is sexy enough." This means future rises will be more differentiated, slower, and more path-dependent, but it also意味着系统性崩塌的概率在下降 (意味着系统性崩塌的概率在下降)意味着系统性崩塌的概率在下降 (means the probability of systemic collapse is decreasing).

From a historical perspective, what ultimately determines the fate of an asset class is never the height of a particular bull market but whether it successfully completes the transformation from a speculative product to infrastructure. The crypto market in 2026 is at such a critical turning point. Prices will still fluctuate, narratives will still change, but the underlying structure has already altered: crypto is no longer just a "substitute fantasy" for traditional finance but is becoming an extension, supplement, and even a part of its reconstruction. This transformation determines that the crypto market of the next decade will resemble a slow but continuously expanding main thread, rather than pulse-like行情 (行情)行情 (market movements) driven by emotion.

Therefore, rather than asking if 2026 is the start of a new bull market, it is better to admit that it is more like a "coming-of-age ceremony"—the first time the crypto market has重新定义了自身的角色、边界与使命 (重新定义了自身的角色、边界与使命)重新定义了自身的角色、边界与使命 (redefined its own role, boundaries, and mission) in a way closer to the real financial system. The real opportunities may no longer belong to those best at chasing cycles but to those who can understand structural changes, adapt to the new paradigm early, and grow together with this system in the long term.