Written by: Zhao Ying

Source: Wall Street News

Two major catalysts for disinflation are simultaneously unfolding, providing ample justification for Fed Chair Wash to adopt a more dovish stance at this week's Federal Open Market Committee (FOMC) meeting.

According to a report from Citi Research released on June 15th via Wind Trading Desk, the planned reopening of the Strait of Hormuz is expected to push oil prices lower, eliminating the upside risk to inflation from energy prices. Meanwhile, last week's core CPI data came in surprisingly cool, with a month-on-month increase of only 0.21%.

The combination of these two developments further weakens the rationale for the Fed to maintain a hawkish stance, bringing the path to eventual rate cuts back onto the table.

For the markets, this assessment has direct pricing implications. The two-year Treasury yield has fallen by about 13 basis points compared to a week ago, but remains more than 60 basis points higher than its February level. There is still room for market pricing of rate hikes to be compressed, and for pricing of rate cuts to be further increased.

Energy Price Pressures Ease, Upside Inflation Risks Blunt

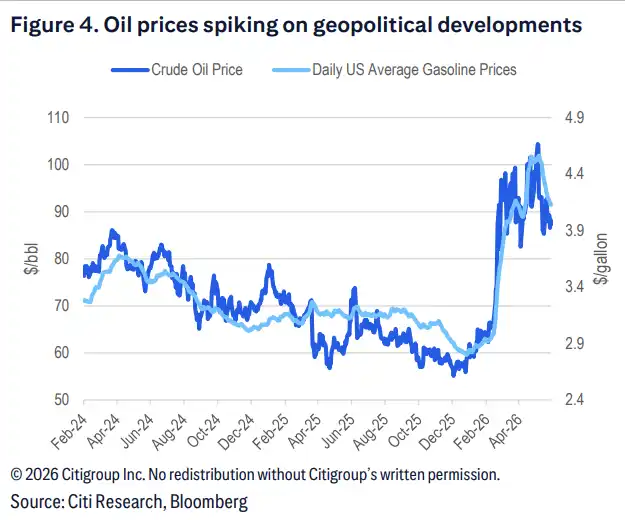

Expectations for the reopening of the Strait of Hormuz are a core driver of the current dovish narrative. Once the strait resumes passage, increased crude oil supply will lead to lower oil and other energy prices.

Gasoline prices have been declining for a full month, with the national average dropping from around $4.50 per gallon to $4.00. Citi expects further declines following other energy commodities. This trend is likely to produce at least several months of negative overall inflation readings in the coming months, prompting Fed officials to shift their characterization of energy prices from an "inflation risk" to a "neutral or even disinflationary factor."

Core CPI Cools, Divergence Among Inflation Metrics Intensifies

On the core inflation front, although May's core PCE is still expected to remain strong, core CPI has shown clear signs of cooling, with a month-on-month increase of only 0.21%.

Core PCE is increasingly becoming an "outlier" among current inflation metrics—both trimmed-mean PCE and core CPI are closer to target levels and show a clearer downward trend. This divergence is being increasingly recognized by both markets and Fed officials, also providing data support for a dovish stance.

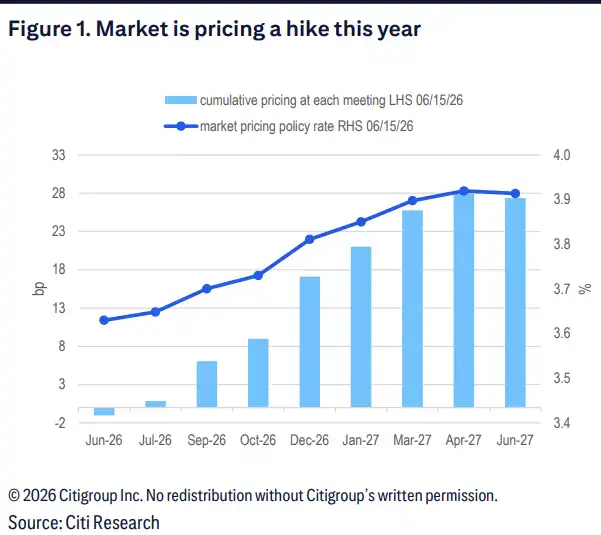

FOMC Hawkish Adjustments Fully Priced In, Dovish Signals Have Upside Potential

The report expects this week's FOMC statement to remove the "easing bias" wording, and the median dot in the interest rate projections (dot plot) will indicate rates held steady this year. However, these hawkish adjustments are already fully anticipated by the market and do not constitute new information.

The real variable lies in Chair Wash's wording. Considering the latest developments regarding the Strait of Hormuz reopening and the cooling trend in core inflation, the risk of Wash delivering more dovish signals at this meeting is tilting to the upside. If his wording proves more accommodative than expected, the market's repricing of the rate cut path could accelerate.

Room for Treasury Yields to Fall Further, Market Pricing Has Adjustment Room

From a market pricing perspective, the report believes implied probabilities of rate hikes in interest rate futures remain elevated. Although the two-year Treasury yield has fallen about 13 basis points from a week ago, it is still over 60 basis points higher than its February level, indicating the market has not fully priced in the impact of receding inflation risks.

As the previously supporting upside inflation risks to the hawkish outlook gradually dissipate, the market is expected to further compress pricing for rate hikes while simultaneously increasing pricing for rate cuts, leaving further room for Treasury yields to decline.