Author:Zhou, ChainCatcher

The Bank of Japan (BOJ) decided at its monetary policy meeting ending on December 19, 2025, to raise the policy rate by 25 basis points, from 0.5% to 0.75%. This is the BOJ's second rate hike since January this year, bringing the interest rate level to its highest since 1995.

The decision was passed unanimously with a 9:0 vote, fully in line with market expectations. All 50 economists surveyed had predicted this rate hike, marking the first "unanimous" rate hike expectation under Governor Kazuo Ueda's tenure.

At a press conference, BOJ Governor Kazuo Ueda pointed out that short-term interest rates being at a 30-year high holds no special meaning, and the central bank will closely monitor the impact of interest rate changes. He stated that there is still some distance to the lower bound of the neutral interest rate range, and the market should not expect a precise neutral interest rate range to be provided in the short term. The pace of future adjustments to monetary support policies will depend on the economic growth, price performance, and financial market conditions at that time.

Ueda emphasized that the assessment of the economic outlook, price risks, and the likelihood of achieving targets will be updated at each meeting, and decisions will be made accordingly. He acknowledged that the estimated range for Japan's neutral interest rate is wide and difficult to measure precisely, requiring observation of the actual feedback from the economy and prices after each interest rate change. If wage increases continue to be passed through to prices, further rate hikes are indeed possible.

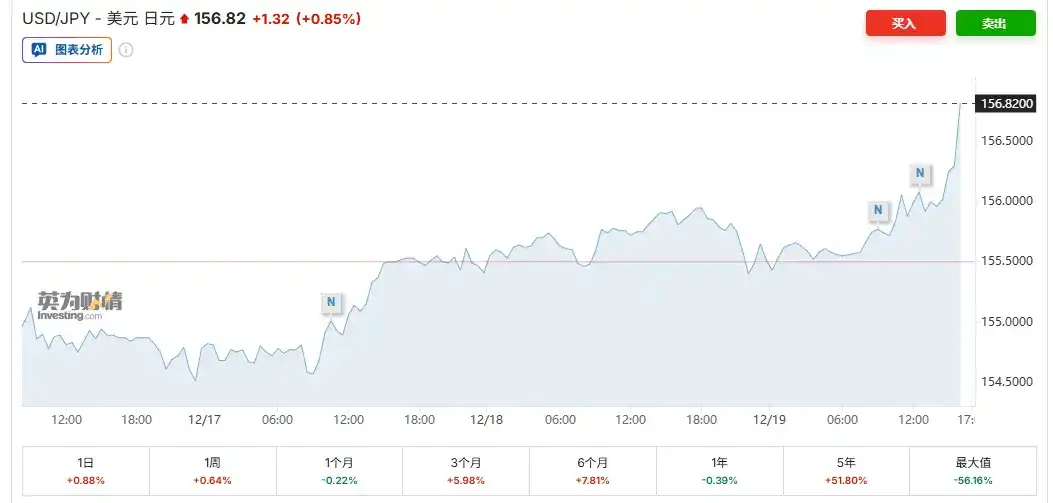

Capital markets reacted relatively calmly: the USD/JPY exchange rate rose slightly by 0.3% to 156.06; Japan's 30-year government bond yield edged up 1 basis point to 3.385%; the Nikkei 225 index rose 1.5% during the session to 49,737.92 points; Bitcoin broke above $87,000, with a daily gain of 1.6%. Risk assets overall did not show significant selling pressure for the time being.

Reviewing the fundamentals, this rate hike by Japan was well-supported by data. Its core CPI grew 3.0% year-on-year in November, meeting expectations, with inflation pressures remaining strong and having been above the 2% policy target for 44 consecutive months. Additionally, wage growth momentum is solid, large manufacturers' confidence hit a four-year high, and even facing U.S. tariff pressures, corporate supply chain adjustments have shown significant strength, with the impact lower than expected.

Furthermore, Japan's major labor unions have set wage hike targets for the upcoming "shunto" (spring wage negotiations) that are on par with last year. Given that last year saw the largest wage increases in decades, this indicates that wage growth momentum is continuing.

Overall, although the rate hike was small, it marks Japan's formal farewell to the long era of ultra-loose monetary policy and could become a significant turning point for global risk asset liquidity at year-end.

Has the Market Fully Priced In Expectations?

Current market pricing suggests the BOJ could raise rates again as early as June or July next year. Yuxuan Tang of J.P. Morgan Private Bank believes that due to full market anticipation, the rate hike's boost to the yen will be limited. One more rate hike to 1% is expected in 2026, with USD/JPY fundamentals remaining high around 150, and 160-162 as a potential defense range; negative interest rate differentials and fiscal risks will continue to limit the yen's appreciation potential.

However, some analysts question this timeline as too aggressive, believing October 2026 is a more realistic window, allowing sufficient time to assess the impact of rising borrowing costs on corporate financing, bank credit, and household consumption. The results of the spring wage negotiations and the yen exchange rate will be the core assessment indicators at that time.

Additionally, Morgan Stanley expects that after a 25bp hike, the BOJ will still emphasize the accommodative nature of the policy environment, and that interest rates remain below neutral levels. The future tightening path will be gradual and highly data-dependent, without a preset aggressive route.

Investinglive analyst Eamonn Sheridan believes that since real interest rates remain negative and policy is still overall accommodative, the next rate hike is expected no earlier than mid-to-late 2026, to allow time to observe the actual penetration of borrowing costs into the economy.

For a long time, Japan's ultra-low interest rate environment provided massive cheap funding for global markets. Through the "yen carry trade," investors borrowed yen at low cost and invested in high-yield assets like U.S. stocks and cryptocurrencies. This mechanism, on a grand scale, has been a key support for the risk asset bull market over many years.

Although the latest TIC data shows Japanese capital has not yet seen large-scale回流 from the U.S. Treasury market (holdings increased to $1.2 trillion in October), as the attractiveness of domestic Japanese government bonds (JGBs) rises, this trend may gradually emerge, pushing U.S. Treasury yields and global dollar funding costs higher, putting pressure on risk assets.

Currently, most major central banks are in a rate-cutting cycle, while the BOJ is hiking rates against the trend, creating policy divergence. This contrast is极易 likely to trigger carry trade unwinding, and crypto markets, with their high leverage and 24-hour trading characteristics, are usually the first to feel the liquidity shock.

Macro analysts had warned that if the BOJ hiked rates on December 19, Bitcoin could face a risk of retesting $70,000. Historical data shows that Bitcoin experienced significant pullbacks after the past three rate hikes, typically falling 20%-30% within 4-6 weeks. For example, it fell 23% in March 2024, 26% in July, and 31% in January 2025. The market was highly concerned that this hike would repeat this historical pattern.

Those warning believe that Japan's rate hike remains one of the biggest variables in current asset pricing, its role in global capital markets is underestimated, and a policy shift could trigger broad deleveraging effects.

A neutral view holds that attributing historical declines solely to Japan's rate hikes is too one-sided, and that this hike was extremely well anticipated (the crypto market had already corrected in advance last week), with most panic情绪 already priced in. Analysts state that the market fears uncertainty more than tightening itself.

It is worth mentioning that, according to Bloomberg, the BOJ could start gradually liquidating its ETF assets as early as January 2026. As of the end of September, its ETF holdings were worth about 83 trillion yen. If accompanied by multiple rate hikes in 2026, bond selling may accelerate, and the ongoing unwinding of the yen carry trade could trigger risk asset sell-offs and yen回流, having a profound impact on stocks and cryptocurrencies.

Click to learn about open positions at ChainCatcher