Bài gốc | Odaily Planet Daily(@OdailyChina)

Tác giả | Azuma(@azuma_eth)

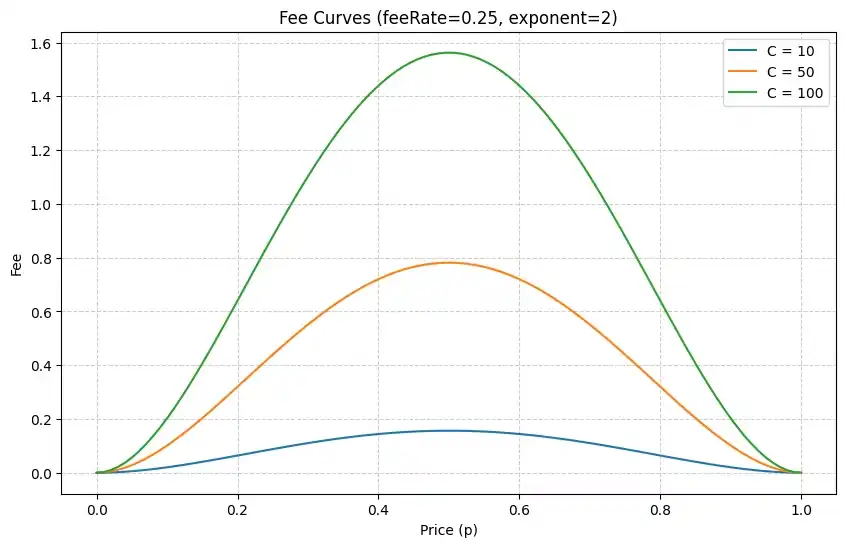

Vào ngày 6 tháng 1 năm nay, Polymarket chính thức bắt đầu thu phí giao dịch đối với các thị trường liên quan đến "biến động giá tiền điện tử 15 phút", với tỷ lệ phí cụ thể thay đổi theo tỷ lệ cược thời gian thực — tỷ lệ cược càng gần 0% hoặc 100%, phí càng thấp; ngược lại, tỷ lệ cược càng gần 50%, phí càng cao, tối đa lên đến 1.56%.

Đây là lần đầu tiên Polymarket ngừng mô hình hoàn toàn miễn phí và bắt đầu thu phí giao dịch cho một loại thị trường cụ thể, ngoại trừ thị trường Hoa Kỳ (Polymarket thu phí 0.01% đối với thị trường Hoa Kỳ). Sau ba tuần, đã có một mẫu dữ liệu quan sát được, đã đến lúc ước tính sơ bộ khả năng doanh thu của Polymarket.

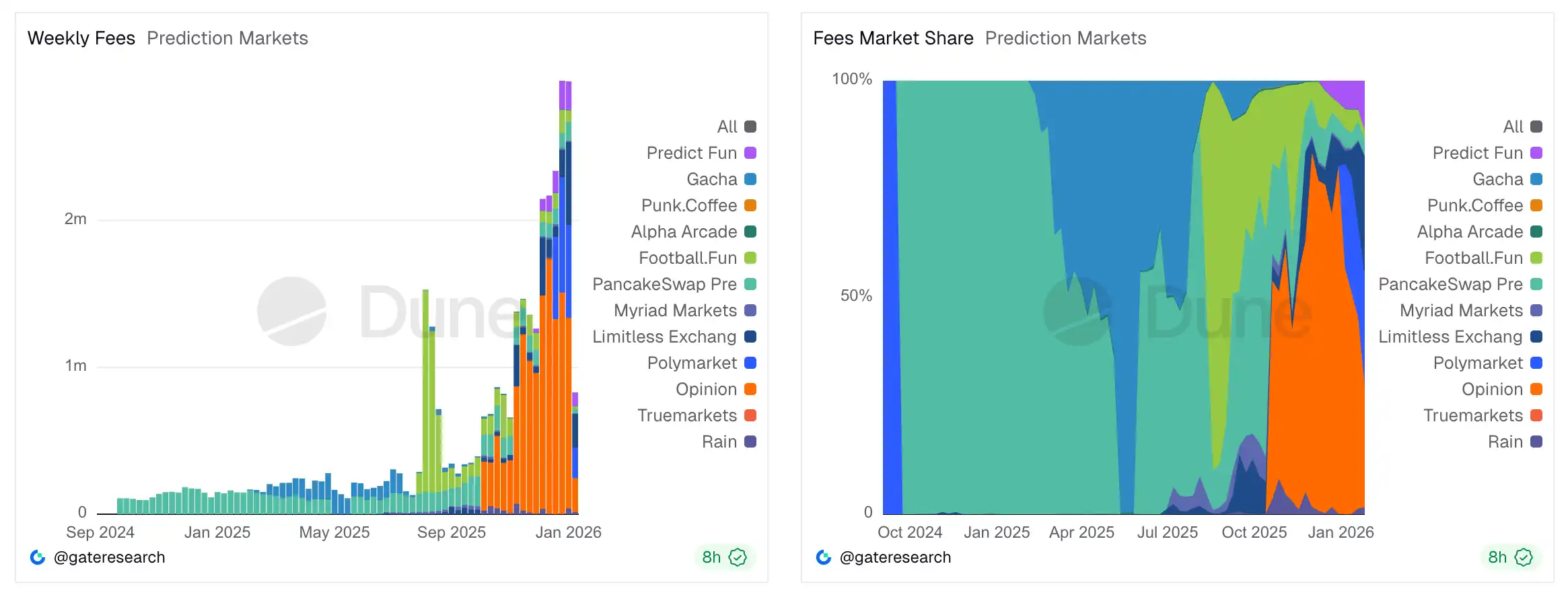

Đầu tiên, hãy xem quy mô doanh thu phí trực quan nhất. Theo dữ liệu được biên soạn bởi Gate Research trên Duna, kể từ khi bắt đầu thu phí này, Polymarket đã tích lũy thu được khoảng 2.19 triệu USD doanh thu phí, trung bình mỗi tuần thu được khoảng 730,000 USD — dựa trên dữ liệu này để suy tính tĩnh, trong điều kiện khối lượng giao dịch và cấu trúc hoạt động giao dịch của thị trường liên quan không thay đổi, dự kiến mỗi năm có thể mang lại cho Polymarket khoảng 38 triệu USD doanh thu.

Có thể dự đoán rằng, phạm vi thu phí của Polymarket chắc chắn sẽ không chỉ giới hạn ở danh mục "biến động giá tiền điện tử 15 phút". Kể từ khi chính thức thu phí đối với danh mục thị trường này, Polymarket đã duy trì lâu dài mô hình hoàn toàn miễn phí, đồng thời tự bỏ tiền trợ cấp thanh khoản thị trường, cuối năm ngoái Coplan đã thừa nhận rằng Polymarket đang hoạt động thua lỗ... nhưng chúng ta đã thấy quá nhiều câu chuyện "đốt tiền" tương tự trong thị trường internet, khi thói quen người dùng và vị thế thị trường của Polymarket dần ổn định, việc thu phí nhiều thị trường hơn trong tương lai không có gì lạ.

- Odaily chú thích: Về vấn đề doanh thu của Polymarket, có thể tham khảo mục Trà thoại của Odaily số mấy ngày trước《Odaily编辑部茶话会(1月7日)》.

Giả sử Polymarket tiếp tục áp dụng tiêu chuẩn phí hiện tại cho các thị trường khác trong tương lai, chúng ta có thể so sánh khối lượng giao dịch thị trường "biến động giá tiền điện tử 15 phút" với tổng khối lượng giao dịch toàn nền tảng Polymarket, để dò xem giới hạn doanh thu lý thuyết của Polymarket ở cấp độ khối lượng giao dịch hiện tại — càng nhiều thị trường thu phí, doanh thu tự nhiên càng cao.

Dữ liệu Odaily thu thập được cho thấy, tuần qua tổng khối lượng giao dịch thị trường "biến động giá tiền điện tử 15 phút" trên Polymarket là khoảng 159 triệu USD(trong bốn loại tiền chính, BTC là 114 triệu USD, ETH là 30.29 triệu USD, SOL là 8.93 triệu USD, XRP là 5.73 triệu USD), chiếm khoảng 9.1% so với tổng khối lượng giao dịch khoảng 1.75 tỷ USD của Polymarket tuần qua — Dựa trên tỷ lệ này suy tính tĩnh, ở mức khối lượng giao dịch và cấu trúc giao dịch hiện tại, nếu Polymarket áp dụng mô hình phí tương tự trong tất cả các thị trường, dự kiến có thể mang lại doanh thu hàng năm 418 triệu USD cho nền tảng.

Cần phải nói rõ, tất cả những điều trên đều là tính toán của Odaily dựa trên dữ liệu lịch sử, tình hình doanh thu thực tế của Polymarket chắc chắn sẽ có sai số do nhiều biến — một là Polymarket thu phí mới chỉ ba tuần, quy mô mẫu vẫn còn nhỏ; hai là Polymarket không chắc sẽ áp dụng cơ chế tỷ lệ phí tương tự ở các thị trường khác, và sự khác biệt thói quen giao dịch người dùng ở các thị trường khác nhau cũng sẽ dẫn đến kết quả phí cuối cùng khác nhau dưới cơ chế phí động; ba là điểm then chốt nhất, Polymarket vẫn đang trong đà tăng trưởng mạnh mẽ, dự kiến khi khái niệm thị trường dự đoán được phổ biến hơn, cộng với điểm nóng tiềm năng World Cup 2026 và bầu cử giữa kỳ, khối lượng giao dịch nền tảng trong tương lai sẽ tiếp tục tăng.

Nhưng ngay cả khi xem xét những bất định trên, một xu hướng đã khá rõ ràng — Polymarket đang chứng minh tiềm năng doanh thu của hình thái thị trường dự đoán hoàn toàn mới này, đây không còn là khái niệm sáng tạo mới lạ nữa, mà là một mô hình kinh doanh thực sự bền vững tạo máu, và không gian lợi nhuận cực kỳ giàu trí tưởng tượng.