This article does not constitute investment advice. Readers must strictly comply with local laws and regulations.

CoinShares has released its annual Digital Asset Outlook Report. Below are several key points worth noting from the "Conclusion: Emerging Trends and New Frontiers" section:

1. Strong recovery in crypto VC funding: Crypto VC funding in 2025 has already surpassed last year's total, confirming that crypto investment is a "high beta" expression of macro liquidity. In an expected宽松 (accommodative) macro environment, capital inflows will continue, supporting growth in 2026.

2. VC investment focuses on "big tickets" and utility: Investment style is shifting from diversification to "big ticket concentration," with capital倾斜 (tilting) towards a few leading projects and placing greater emphasis on practical utility and cash flow rather than vague concept炒作 (hype) or meme coins.

3. Four major investment tracks for 2026: Looking ahead to next year, VCs are focusing on RWA (with stablecoins as the core), consumer applications combining AI and crypto, on-chain investment platforms for retail investors, and infrastructure enhancing Bitcoin's utility.

4. Prediction markets elevated to information tools: Prediction markets, represented by Polymarket, have moved beyond a niche stage to become mainstream information infrastructure. Their trading activity remains high even after the election, and their market odds have proven to be highly accurate.

5. Institutionalization of prediction markets: Prediction markets are accelerating their institutionalization, with the strategic investment by ICE, the parent company of the NYSE, being a key signal. This indicates recognition from traditional financial institutions, and prediction markets are expected to continue increasing their influence through competition and consolidation, creating new trading records.

6. Accelerated transition of mining companies to HPC (High-Performance Computing): Bitcoin mining companies are undergoing a fundamental shift in their business models towards higher-margin HPC/AI data centers. It is expected that by the end of 2026, the proportion of revenue from mining for transitioning companies will drop below 20%, driven by HPC profit margins being approximately 3 times those of mining.

7. Short-term hash rate growth lag: Despite the strategic shift to HPC, due to large 2024 orders being集中交付 (delivered集中ly) in 2025, the network's total hash rate is still in a period of strong growth. This is a short-term phenomenon, with companies like Bitdeer and IREN being the main growth points.

8. Future divergence in mining models: Traditional industrial-scale mining will be replaced. Future mining will diverge into four models: ASIC manufacturer self-mining, modular (temporary) mining, intermittent (grid-balancing) mining, and sovereign nation mining. In the long run, hash rate will be dominated by sovereign nations and ASIC manufacturers.

Crypto VC Funding: Where is the Money Flowing?

Jérémy Le Bescont—Chief Content Manager

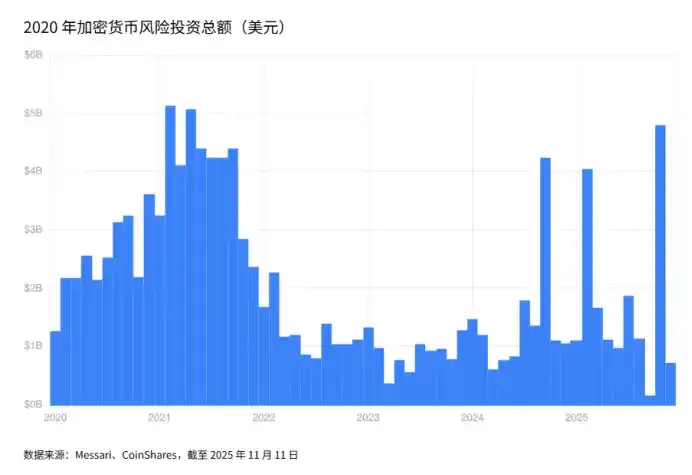

Overall, 2025 marks the return of crypto assets to VC investment logic, ending a period of near stagnation, or even可以说 (one could say) downturn, that lasted nearly two years.

In 2023, total funding in the crypto space was $11.53 billion, a significant drop from $34.9 billion the previous year; in 2024, the digital asset industry saw a recovery, but the funding scale was still only $16.54 billion. As of November 11, 2025, the annual funding total has reached $18.8 billion, exceeding 2024's figure.

"This is the year with the highest number of deals in the past three years," Marguerite de Tavernost, a VC investor at Ledger Cathay, told us.

This growth also confirms the overall recovery in the deal environment—by Q3 2025, the global deal volume had reached $250.2 billion, surpassing the levels of 2022 to 2024.

Concentration Towards Ultra-Large Deals

The most notable feature this year is the concentration of funds into ultra-large single deals. Prediction market Polymarket secured a $2 billion strategic investment deal with ICE, followed by Stripe's $500 million investment in Layer-1 project Tempo, and a $300 million investment in prediction market Kalshi.

These landmark funding rounds reflect a high concentration of capital in single projects. Similar trends are seen in other areas, especially AI.

"We used to enter with smaller amounts and then gradually increase our position in subsequent rounds," continued Marguerite de Tavernost—the €100 million fund has invested in Flowdesk, Ether.fi, Crypto, and Midas, among others. "Now, we are putting in larger sums of money at an earlier stage."

The main capital providers are still familiar names: Coinbase Ventures, Pantera, and Paradigm were particularly active in strategic rounds related to stablecoins, prediction markets, network layers, and DeFi applications.

In contrast, meme coins (excluding the standout Pump.fun) and NFTs have almost disappeared this year, showing market fatigue with these themes and the overall maturation of the industry.

Another noteworthy trend is the privacy track: Canton Network completed a $135 million Series E round, followed by Mesh ($92 million) and Zama ($57 million Series B), becoming the most prominent cases in this investment thesis.

If the US government continues to promote pro-crypto innovation policies, this theme is expected to continue, especially after Zcash (one of the earliest privacy coins) gained a publicly listed treasury company controlled by the Winklevoss brothers.

Macro Context: The Liquidity Link

Before discussing 2026, understanding the macro context that shaped the 2025 recovery is crucial. Crypto VC funding is highly correlated with changes in the global liquidity environment, which are primarily driven by central banks.

Although not always a one-to-one correspondence, our data consistently shows that crypto VC is a "High Beta" manifestation of the macro liquidity cycle.

During the tightening phase, especially in 2022-2023, higher policy rates, rising real yields, and quantitative tightening significantly suppressed market risk appetite. Venture capital, which relies on long-term capital and often lacks short-term cash flow, was hit first.

Crypto VC activity fell from highs of over $5 billion per month in 2021-2022 to well below $1 billion for the entirety of 2023.

As financial conditions began to ease in late 2023, risk sentiment gradually improved. The Fed paused rate hikes, inflation fell, and the market began pricing in rate cuts. These changes drove a gradual recovery in global liquidity, which echoed the复苏 (recovery) in crypto VC funding in 2024-2025.

Although liquidity remains the core driver, Bitcoin price movements, regulatory progress, and new themes like RWA, Lightning Network-based infrastructure, and stablecoin settlement layers also influence short-term dynamics. However, the overall pattern is very clear:

When liquidity expands, crypto VC funding accelerates; when liquidity tightens, funding retreats. This highlights the characteristic of crypto VC as one of the purest expressions of the global monetary environment.

Therefore, liquidity is unlikely to be a bottleneck in 2026, and the favorable macro conditions supporting the 2025 recovery seem set to continue.

Furthermore, unlike traditional funds, crypto funds can often provide DPI to LPs earlier, thanks to the high liquidity and rapid realization ability of tokens. If the Fed maintains its accommodative stance and the global liquidity environment remains friendly, 2026 could see even more impressive fundraising performance on top of 2025's.

"Overall, US market sentiment is very positive against the backdrop of the Trump administration's pro-crypto policies," confirmed the Ledger Cathay investor.

Even if liquidity tightens again, investment strategies may not necessarily be affected. Jonathan King, Senior Manager at Coinbase Ventures, added: "We invest in all market cycles. When market sentiment is more optimistic, the number of projects increases significantly; but some of our best investments were actually made when the market slowed down and became quiet. Depending on the cycle, funding rounds may take longer to finalize, but overall, our door is always open."

Four Key Trends to Watch in 2026

With the above macro context established, four areas are particularly值得持续观察 (worth持续ly observing) in 2026: the integration of AI and crypto, RWA (Real World Assets), Bitcoin infrastructure, and investment platforms for retail investors.

RWA (Real World Assets)

First, the tokenization track will undoubtedly continue to expand next year. Republic's investment in Centrifuge, the Series A funding of stablecoin startup Agora (led by Paradigm and Dragonfly, $50 million规模), and particularly the announcement related to Securitize's SPAC上市 (SPAC listing), have attracted market attention and confirmed the strong interest from well-funded investors (including banking institutions like JPMorgan, Clearstream, UBS, Société Générale) in digitized real-world assets.

Within this vertical, stablecoins are once again the most dominant segment:

"If you look at stablecoins, their market cap has grown 50% year-over-year. Predictions suggest it will become a $2 trillion asset in the coming years.

We've done a lot of work at the infrastructure level, from B2B cross-border payments, localized stablecoins (e.g., p2p.me in India), to stablecoin networks like Sphere (Editor's note: on/off-ramp channels for cross-border payments).

"This further extends to on-chain credit and new forms of financing. Stablecoins will continue to be a flagship focus for Coinbase Ventures and Coinbase's overall strategy," explained Jonathan King.

Notably, this field may intensify competition between different jurisdictions. MiCAR gives Europe a first-mover advantage in tokenization落地 (landing), with relevant rules formally生效 (effective) throughout the European Economic Area (EEA); while the US GENIUS Act has recently passed, it is still in the specific implementation stage.

AI Connected with Crypto

Over the past two years, public chains and applications connecting crypto and AI have continuously emerged, covering areas like resource consumption pricing and monetization, payment automation, user identity verification, and autonomous operation of AI agents. According to VCs, this trend is明显加速 (明显 accelerating).

"Previously, we mainly focused on the underlying infrastructure of crypto and AI. Next year, we hope to see more consumer-grade AI applications built on crypto rails. For example, new DeFi interfaces integrating natural language trading and operations, and智能体 (agents) gradually possessing asset management capabilities,类似 (similar to) wealth management advisors," explained Jonathan King.

Marguerite de Tavernost added: "This is an area we hadn't planned to focus on heavily, but we ended up making two investments related to AI and blockchain."

Investment Platforms for Retail Investors

A factor that may impact VC activity next year is the rise of native crypto consumer investment applications, most notably Echo and Legion.

Echo, founded by well-known crypto figure Jordan "Cobie" Fish, was acquired by Coinbase for $375 million in October 2025, attracting widespread attention. The platform's core is decentralized angel investing: through a whitelist curator mechanism, it opens equity financing and ICOs to users, essentially an "on-chain native VC fund."

In prominent cases, Layer-2 projects MegaEth and Plasma raised $10 million and $50 million respectively last year.

Its competitor, Legion, partnered with crypto exchange Kraken to launch a new platform for public offerings. Meanwhile, MetaDAO (backed by 6MV, Paradigm, and Variant) launched a fundraising platform on Solana with on-chain governance mechanisms to prevent default issues, having completed 8 oversubscribed ICOs so far.

After years of liquidity drought, such platforms are naturally welcomed as new financing channels and are beginning to compete directly with early-stage VCs.

Bitcoin Infrastructure

Finally, VC interest in Bitcoin-related areas is heating up. This is somewhat ironic, as Bitcoin, the most important digital asset, has long been overlooked.

Due to the inability to issue tokens "out of thin air," the Bitcoin ecosystem, apart from the mining industry, has historically not been the preferred direction for LPs, although mining continues to attract significant capital (e.g., Auradine's $153 million Series C round completed in April 2025).

With the early funding success of Bitcoin Layer-2 projects, including Arch Labs ($13 million led by Pantera), BoB (Build on Bitcoin, a co-investment by Coinbase Ventures and Ledger Cathay), and BitcoinOS ($10 million funding completed in October 2025), the market focus seems to be shifting towards a more substantive investment thesis that directly enhances Bitcoin's utility, rather than issuing new tokens on top of it.

This point is quite similar to the Lightspark case:

"Two years ago, market attention on Bitcoin L2 was very high. Now, we are seeing a renewed focus on expanding Bitcoin's utility, especially its security attributes, and building new markets on top of it," noted Jonathan King.

Shift in Investment Thesis from High Speculation to High Utility

The changes over the past few months and the outlook for next year indicate that capital is increasingly seeking projects that can impact existing financial infrastructure and provide "building blocks" for a new system, gradually moving away from tokens and public chains that are all concept and lack practical value.

Ethereum Layer-2 is no longer the market's追逐的焦点 (chased focus), general-purpose Layer-1 has also cooled down, and the frequency of mentions of terms like "Web3" and "NFT" continues to decline.

Of course, every cycle comes with some micro-bubbles, and the number of stablecoin companies that will ultimately survive this round remains to be seen. But overall, an era that prioritizes cash flow and/or real utility is clearly more值得期待 (worth期待ing).

The Rise of Polymarket

Luke Nolan—Senior Research Associate

Although the concept of prediction markets has been around for nearly five years, their actual adoption and popularity have mainly occurred in the past two years, with the 2024 US election being the strongest catalyst.

Platforms represented by Polymarket have grown from niche products within the crypto领域 (crypto realm) to mainstream sources of real-time sentiment and even "facts," attracting a large number of users who don't care about crypto itself but want cleaner signals than news media or social platforms.

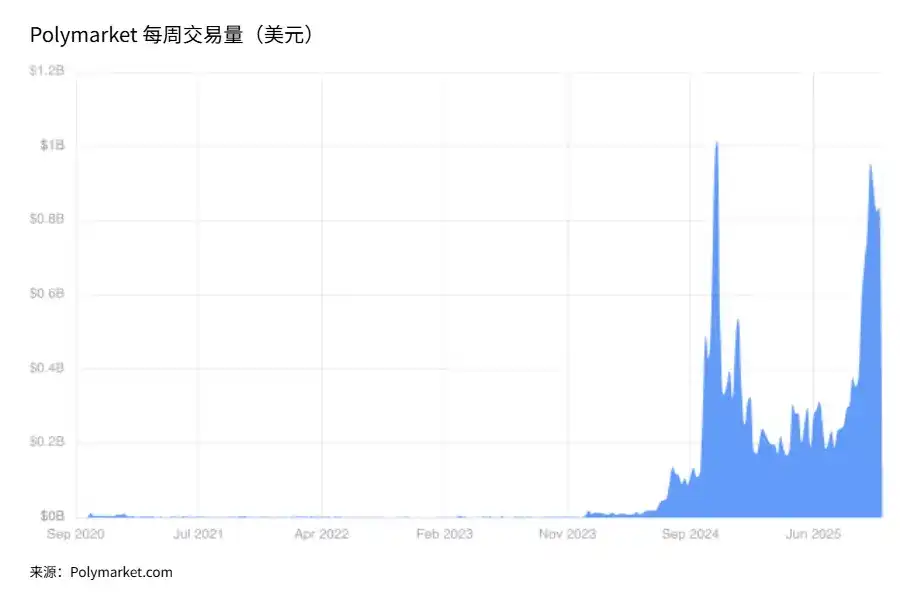

About 18 months ago, we wrote about Polymarket. At that time, we judged that it might remain at the enthusiast product level, with stable but limited usage. This prediction proved too conservative. Since then, Polymarket's liquidity and cultural influence have reached heights almost no one anticipated.

During the 2024 US election cycle, markets related to the presidential and congressional elections often saw weekly trading volumes exceeding $800 million, consistently stable, often surpassing traditional betting platforms and even exceeding some poll aggregators in public attention.

Sustained Activity Post-US Election

Some observers believed that after the election, as public attention shifted, the activity of prediction markets might quickly decline. But this was not the case.

Trading volume remains strong, and open interest is maintained at levels far higher than before the election, suggesting that prediction markets may have crossed a certain "tipping point," no longer just a one-time爆发 (outburst), but entering a stage of long-term existence.

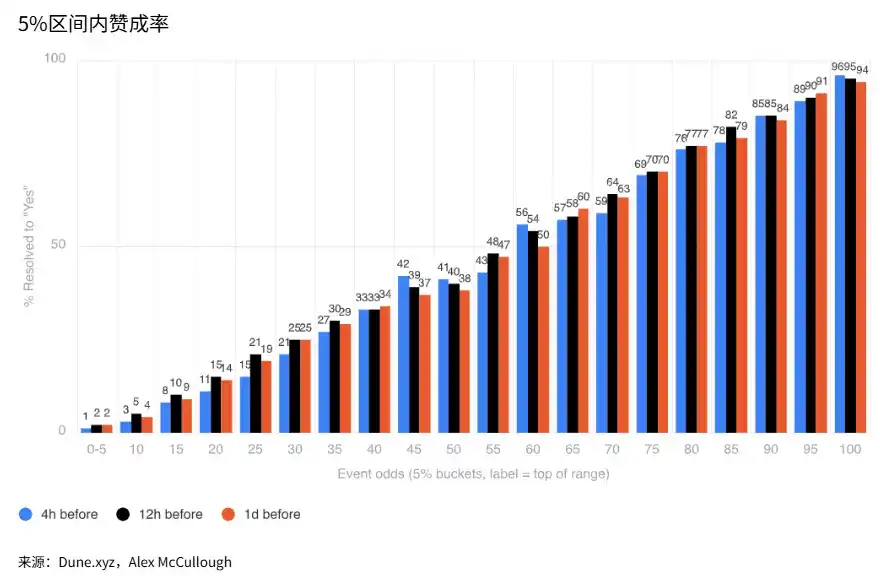

A more important question than activity is accuracy. The essence of prediction markets is to aggregate分散的信息 (dispersed information) into a single probability, and financial incentives force participants to get as close as possible to the true outcome. The chart in the article compares Polymarket's odds at different points in time with the actual results.

The interpretation is not complicated. For example, events priced in the 60% range ended with "Yes" about 60% of the time; events priced in the 80% range, depending on the number of hours remaining before the cutoff, were realized about 77%–82% of the time.

In other words, Polymarket performs like a well-calibrated prediction system; when the market gives an 80% probability of occurrence, it usually does happen. This is exactly how a system where "making a mistake costs money" should perform.

Prediction Markets Begin Institutional Adoption

This accuracy and liquidity have not gone unnoticed. In October 2025, Intercontinental Exchange (ICE), the parent company of the New York Stock Exchange, made a strategic investment in Polymarket (up to $2 billion), which is equivalent to one of the most traditional, core institutions of the global financial system casting a vote of confidence in prediction markets.

Meanwhile, Polymarket's compliant US competitor, Kalshi, is also expanding its influence through integration with brokerage platforms, media partners, and data providers, creating a competitive landscape that pushes the entire track forward.

These integrations reveal a very important fact—prediction markets are not just trading venues for speculators to earn pocket money; they are being integrated into broader information infrastructure. Many people who never place a trade still check Polymarket because the probabilities it gives are "cleaner" than news headlines.

For traders, the appeal is equally obvious. There is no house advantage here; the platform only charges a small fee on profitable trades, meaning long-term profitability is possible in principle. In traditional bookmakers, the odds are designed to ensure the house必然获利 (inevitably profits).

All these factors point to a simple conclusion—prediction markets are likely to continue growing because they simultaneously solve the needs of multiple groups:

Traders get efficient markets, observers get "true signals," institutions get almost free sociological or economic research data (in the form of probabilities), and the platforms themselves become more powerful as they grow—the deeper the liquidity, the more accurate the predictions.

The trajectory of the past two years suggests that Polymarket is gradually becoming a way for people to understand the world. With the launch of builder code, we expect Polymarket's weekly trading volume有望 (有望) to hit new highs in 2026, even突破 (breaking through) $2 billion in a single week.

Mining After HPC: What's Next?

Alexandre Schmidt—Index Fund Manager

For a long time, Bitcoin mining companies have been a core channel for gaining exposure to blockchain and crypto assets through publicly listed stocks. After a period of investment and expansion, reaching industrial-scale mining, this market is shifting again.

In 2024, several mining companies announced plans to transition into the AI and HPC (High-Performance Computing) fields; by 2025, most mining companies were already fully advancing the construction of their HPC data centers.

This article attempts to answer two questions: Why did this transition occur? And, in the context of no longer building new large-scale industrial mining facilities, where is the mining industry headed next?

2025: Industry-Wide Expansion

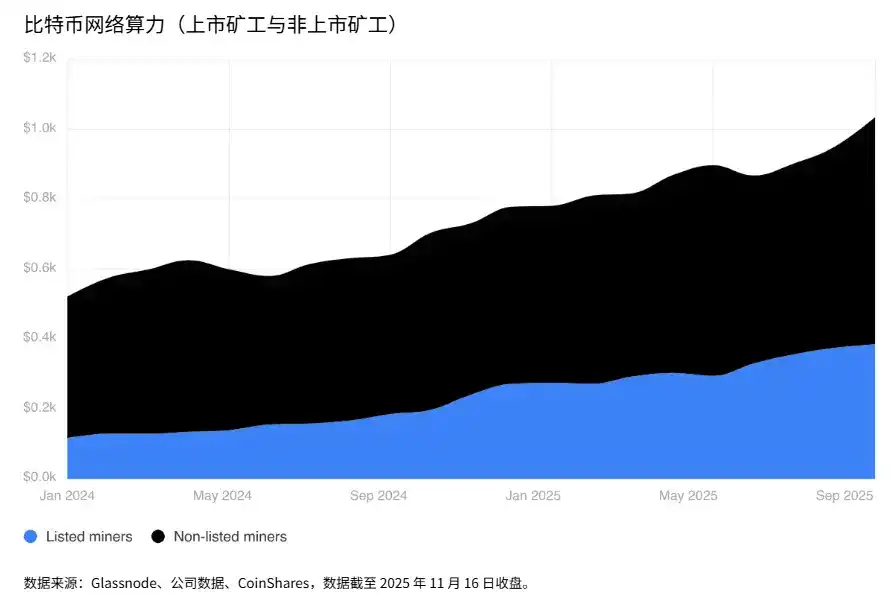

In 2025, Bitcoin mining companies showed strong growth momentum. In the first nine months up to September, the total hash rate growth of listed mining companies was approximately 110 EH/s, compared to only about 70 EH/s in the same period of 2024.

Although these data seem to contradict the statements of mining companies "downgrading mining and转而 (turning to) building HPC facilities," the reason is that these companies actually placed several large orders with ASIC manufacturers in 2024, and the related equipment was陆续交付 (delivered陆续ly) in 2025.

Half of this year's hash rate growth came from three companies: Bitdeer (+26.3 EH/s), HIVE Digital (+16 EH/s), and Iris Energy (IREN) (+15 EH/s).

HPC Transition Begins to Materialize

Besides considerable hash rate growth, the transition to HPC finally materialized this year in the form of actual contracts and revenue.

For Bitcoin mining companies, building and retrofitting facilities to carry HPC loads is highly attractive: it not only diversifies the business, obtaining more stable, predictable, and per-megawatt (MW) profit margins about 3 times higher but also allows mining companies to participate in the tens of billions of dollars in transactions announced by hyperscalers and semiconductor companies.

As of the end of October 2025, mining companies have announced contracts totaling approximately $65 billion with hyperscalers and neoclouds.

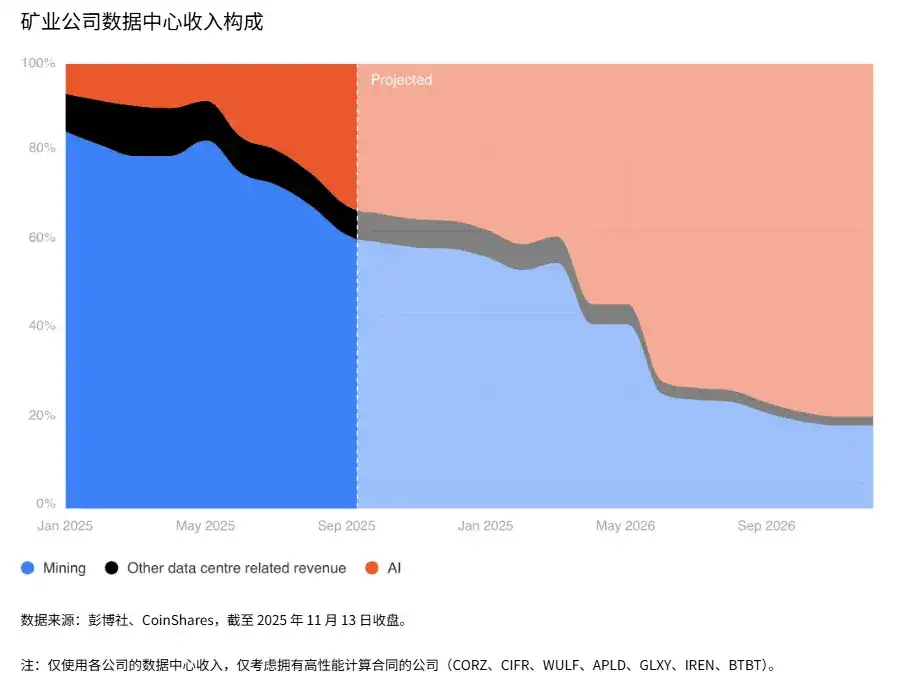

These announcements significantly boosted the stock prices of the related companies. These contracts will fundamentally change these companies' business structures: on one hand, alleviating the pressure from the continuous growth of the Bitcoin network's total hash rate, and on the other hand, significantly improving corporate profit margins (most companies expect these contracts to bring 80%–90% operating margins).

Therefore, among the six companies that have announced HPC contracts so far, we expect the proportion of Bitcoin mining revenue in total revenue to drop from about 85% at the beginning of 2025 to below 20% by the end of next year.

Outlook for 2026

First, it needs to be clear—mining companies are still mining companies.

Most companies that have shifted to HPC currently still derive the vast majority of their revenue and cash flow from Bitcoin mining operations.

In the foreseeable stage, HPC is more of an incremental supplement to the existing business rather than a direct replacement for Bitcoin mining capacity, although with the signing of new contracts and increasing power capacity demands, we do expect these companies to gradually and slowly phase out部分 (part of) their mining operations.

By 2026, a few mining companies may still continue to increase their mining hash rate. Based on discussions with management, CleanSpark stated that its mining business still has the option to add approximately 10 EH/s; and Canaan recently announced a deal for 50,000 mining machines, suggesting that other mining companies may also be significantly expanding their mining scale.

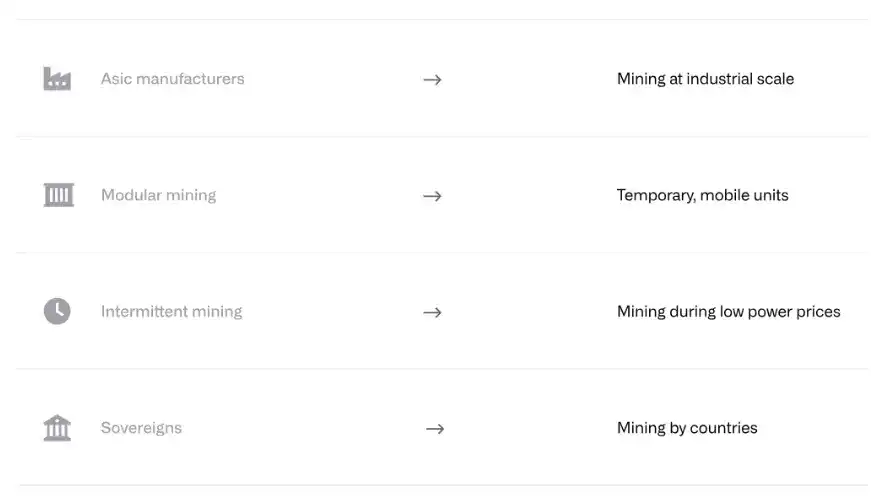

From a longer-cycle perspective, the form of Bitcoin mining will likely be very different from the current operational model and may include the following forms:

ASIC Manufacturers: ASIC manufacturers are most likely to continue maintaining mining接近或达到 (接近 or reaching) industrial scale. To retain their wafer fab capacity quotas (especially at TSMC), manufacturers must place minimum orders. If these miners are not sold, they are likely to be deployed in the ASIC manufacturers' own mining farms.

Furthermore, ASIC manufacturers can also design and produce specifically for their own use at significantly lower costs, thus supporting larger-scale mining operations.

Modular Mining: Some companies are proposing a model that introduces temporary, mobile mining modules into sites being developed for other uses. Once the power infrastructure is in place, these modules can be connected and begin mining, operating until the power shell construction is completed and the site is officially leased out.

Intermittent Mining: This is an alternative model that can coexist with HPC: mining facilities are built并行 (parallel) to HPC but operate only when electricity prices are接近零 (接近 zero), thereby helping to balance grid load. In this case, mining companies are more likely to use fully depreciated older equipment, as the load factor is usually very low.

Sovereign Entities (Nations): We believe sovereign nations already occupy a large amount of non-public mining hash rate. The motivations for state participation in mining are varied, including acquiring foreign exchange, monetizing power resources, and directly accessing the Bitcoin network. Given the financial strength and resource access advantages of sovereign nations, we believe that state-level mining will maintain an industrial scale for the foreseeable future.

Which of the above models ultimately dominates will depend on the Bitcoin network's own incentive mechanisms and the sensitivity of various participants to mining economics.

Our judgment is that, in the medium term, sovereign nations and ASIC manufacturers will dominate the hash rate distribution;而从更长期的视角 (from a longer-term perspective), mining may return to a smaller-scale, more decentralized form, relying on cheap "stranded power," and likely primarily from renewable energy sources.