Compiled by: Macro_Lin

Recently, I read a special report released by the Bank of Korea (BoK) titled "Examination of the Sustainability of the Global Semiconductor Boom." This report is quite unique.

South Korea is a major global exporter of memory chips. The financial reports of Samsung and SK Hynix are, to some extent, the national economic reports for the BoK. When this central bank itself steps in to seriously discuss how far this AI-driven semiconductor super cycle can actually go, the attitude itself is noteworthy. Sell-side research reports have their biases, bearish reports carry emotion; BoK's document is permeated with the restrained tone characteristic of a central bank, with a much higher density of argumentation than emotional charge.

Core View

The Bank of Korea judges that the amplitude and duration of the supply-demand imbalance in this memory cycle significantly exceed those of the past three cycles, and expansion is certain to continue at least until the first half of 2026. However, starting in 2027, five variables will jointly determine the timing of the reversal, with two of the most concerning signals already emerging.

I. How This Round Differs from the Past Three

BoK divides the semiconductor cycles since 2010 into four rounds: smartphone普及 (2013-2015), cloud expansion (2017-2018), pandemic non-contact demand (2020-2021), and the current round of AI diffusion (2024-present).

The script for the past three rounds was the same. New technology pulls up demand, supply lags behind to catch up, concentrated release of expanded production leads supply to surpass demand, inventory accumulates, prices fall, and the cycle reverses. Post-2017, this reversal point highly coincided with the inflection point in CAPEX of large US tech companies.

This round differs in three aspects.

First, demand growth is the fastest in history. HBM is exploding with the loading volume of AI accelerators, and general-purpose DRAM is also being driven up by inference needs. It's a synchronous expansion across all categories.

Second, supply elasticity is the worst in history. HBM processes are difficult with long expansion cycles. Memory manufacturers, having experienced the bloodbath of 2022-2023, are conservative in expansion. General-purpose DRAM production lines are being switched to HBM, further exacerbating the tightness of general-purpose products.

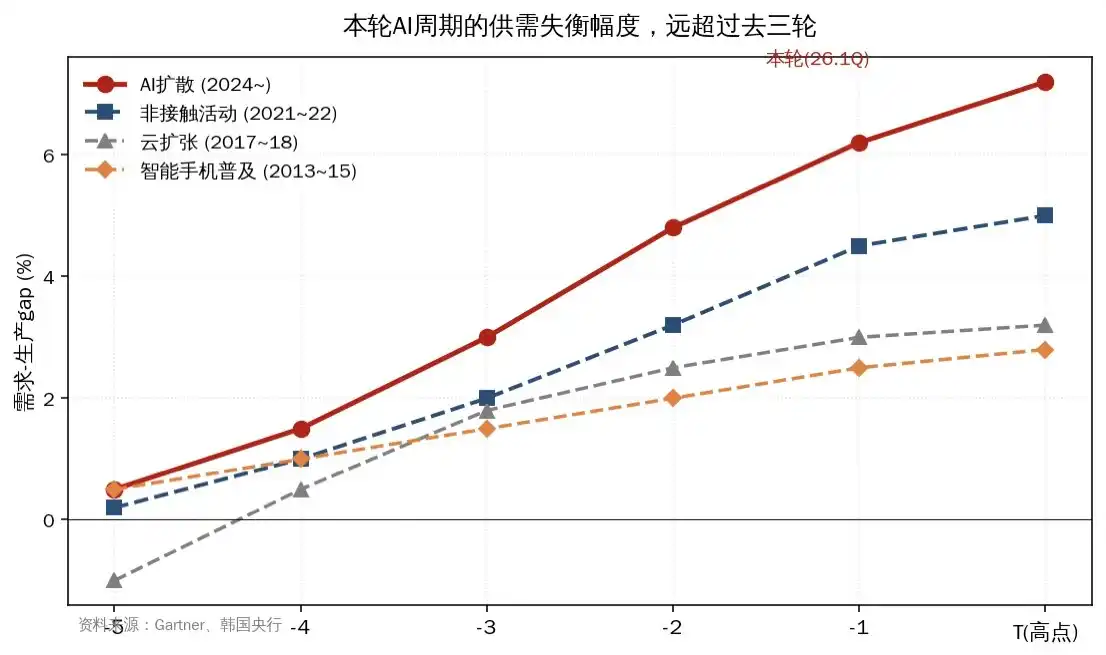

Third is the result. BoK created a crucial chart plotting the demand-production gap of the four cycles on the same coordinates. The imbalance amplitude and duration of this round significantly exceed those of the past three. Inventory levels at both the DRAM manufacturing and demand ends are declining, with no signs of accumulation.

Figure 1: Comparison of Demand-Production Gaps in Past Semiconductor Cycles, Current AI Cycle Amplitude Significantly Exceeds History

II. The Five Variables Determining How Far the Cycle Can Go

BoK provides a clear five-factor framework: three on the demand side, two on the supply side. I'll explain them in order of importance.

1. Timing of Profitability Verification for AI Investments. Currently, OpenAI, Anthropic, etc., are operating at a loss. What supports their valuations and investments is the market's expectation of future dominance. BoK's judgment is subtle: starting next year, the market's focus will shift from grabbing territory to whether it can make money. Coupled with risks like data center power bottlenecks, accelerated GPU depreciation, and insufficient utilization, it's difficult for CAPEX growth to maintain its current pace.

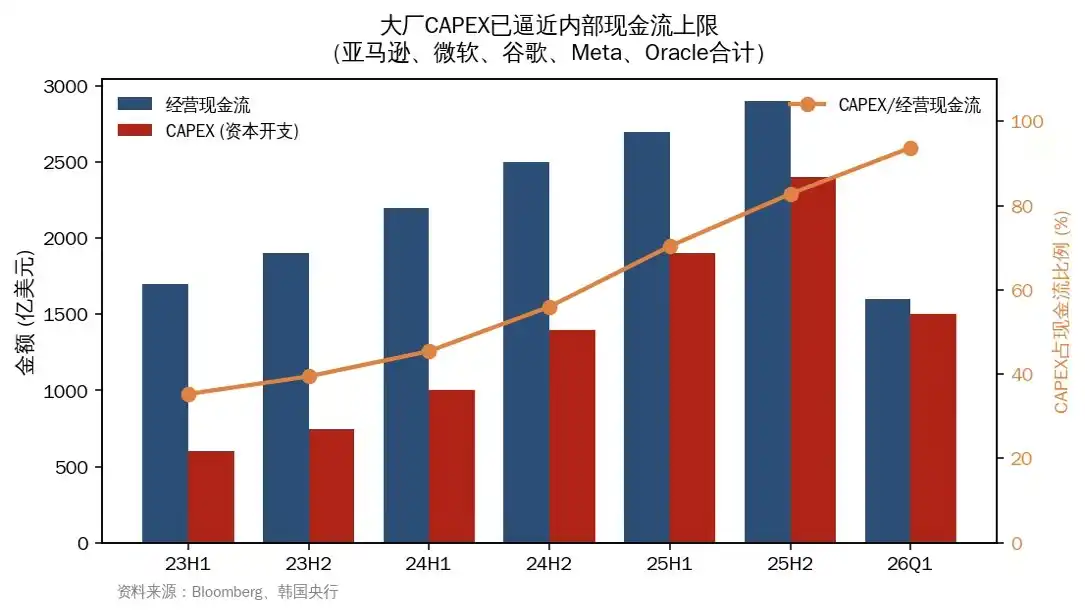

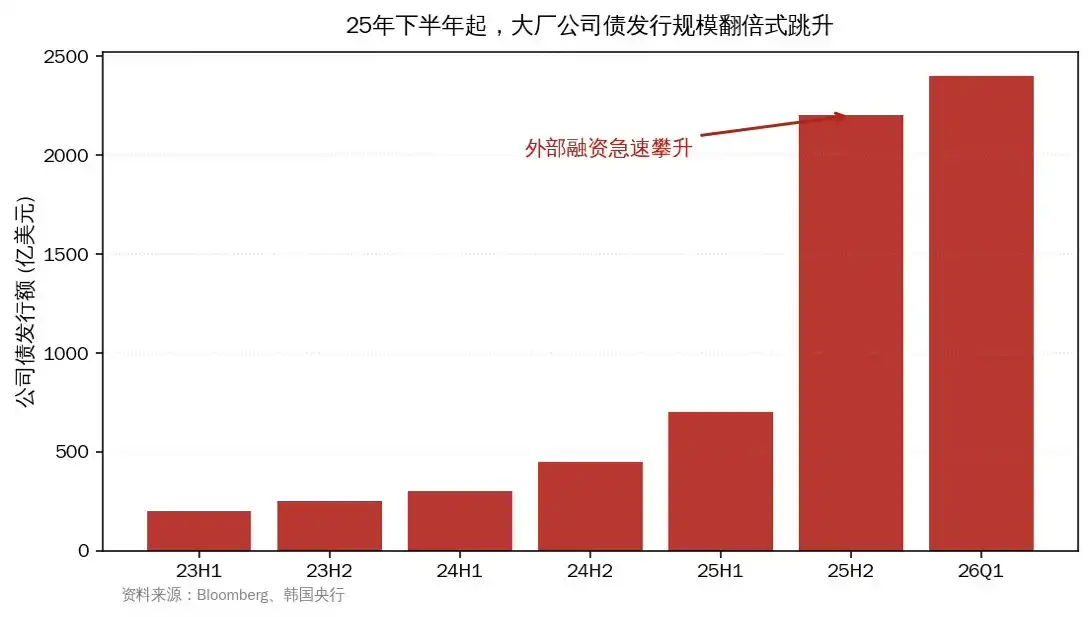

2. Whether Large Companies Can Continuously Raise Funds. This section is the most informative part of the entire report. BoK explicitly compares the present to the telecom bubble of the late 1990s and points out a worsening fact: the internal cash flow of large companies can no longer support CAPEX of this magnitude. Starting in the second half of last year, large companies reduced buybacks and significantly issued corporate bonds; the CDS spreads of some companies have already widened.

Figure 2: Large Companies' Operating Cash Flow Can No Longer Cover CAPEX, Ratio Soared from 25% to Nearly 100%

Figure 3: Corporate Bond Issuance Volume Jumped in H2 2025, External Financing Becomes Main Supplement

Even more alarming is the financing behavior itself. Neocloud companies (e.g., CoreWeave) are much smaller than large firms but must continuously procure GPUs and build AI data centers. Nvidia provides them with credit support to boost sales of its own GPUs. This structure is highly similar to the vendor financing provided by Cisco and Lucent to nascent telecom companies back then.

Another layer is off-balance-sheet financing. Meta's Hyperion data center, through SPVs and private credit, has $29.5 billion in liabilities not on Meta's balance sheet. Oracle's Stargate ($66 billion), xAI's Colossus ($20 billion) use similar structures. BoK mentions a detail: in February-March 2026, institutions like Blue Owl, BlackRock, Morgan Stanley, and Cliffwater suspended redemptions for some private credit funds due to AI disruption concerns. This is a crack.

3. Progress in AI Model Efficiency. After DeepSeek, memory-saving technologies like quantization compression, MoE, Mamba, Nvidia's CMX, Google's TurboQuant are rapidly emerging. BoK frankly admits the bidirectional impact is uncertain. Efficiency gains could either reduce unit demand or, due to Jevons Paradox, increase total demand. This factor is marked with a bidirectional arrow in BoK's overall assessment table, the only one among the five without a definitive direction.

4. Expansion Speed of Major Memory Manufacturers. This year, Samsung's P4 and SK Hynix's M15X have exhausted existing cleanroom space but it's still insufficient. The real supply release window is in the second half of 2027. SK Hynix's Yongin, Micron's new fab in 2027H2, Samsung's P5 in 2028. These are hard constraints on the supply side that can be calendared.

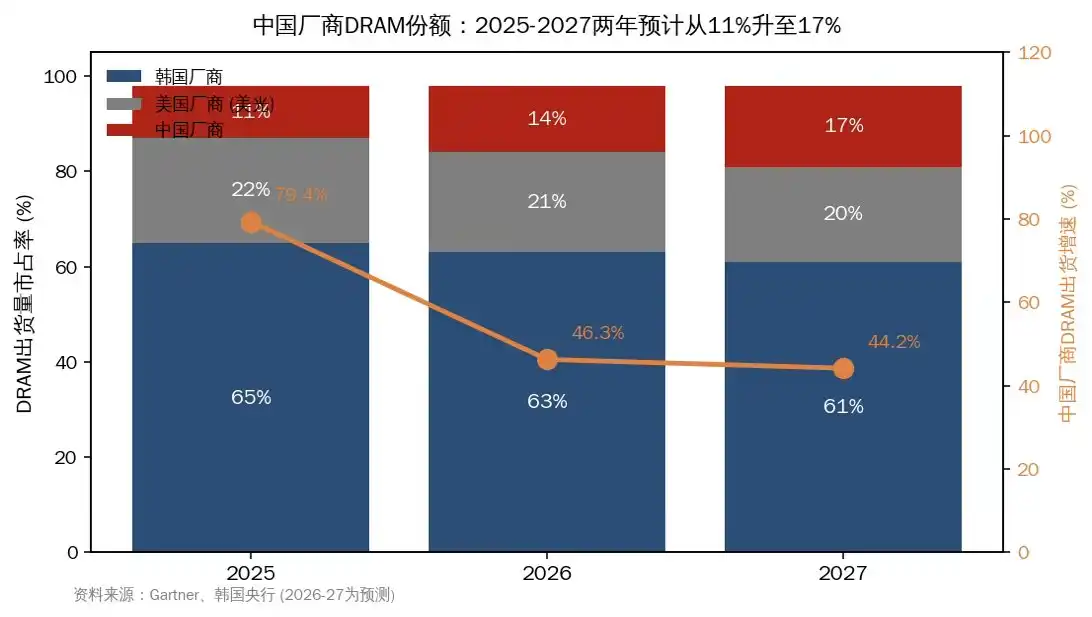

5. Catch-up Speed of Chinese Manufacturers. BoK assesses the technology gap between China and South Korea is about 4 years, for both HBM and general-purpose DRAM. So the high-end landscape remains stable short-term. But one number is noteworthy: the DRAM shipment share of Chinese manufacturers may rise from 10.5% in 2025 to 17% in 2027, with a growth rate over the next two years more than 3 times that of major memory makers. This share will pressure general-purpose DRAM prices, accelerating the timing of imbalance relief.

Figure 4: Chinese Manufacturers' DRAM Share Rises from 11% to 17%, Shipment Growth Far Exceeds Major Memory Makers

III. Regarding the Middle East War, BoK's Judgment is Calmer Than Expected

Currently, there are no signs of data center construction delays or memory supply slowdowns. The AI investment cycle is led by US companies, with 74% of data centers under construction in the Americas. The correlation between the global economy and semiconductors has significantly weakened in recent years.

But BoK lists several potential transmission channels. Rising oil prices increase data center operating costs, tightening financial conditions increase large companies' financing difficulties, supply disruptions of Middle Eastern raw materials and equipment (bromine, helium), and if Taiwan's energy issues affect system chip production, it would drag down memory. The most direct backlash is on the consumer side: Gartner already predicts that due to memory price increases, PC shipments will fall 10.4% YoY and smartphones 8.4% in 2026.

IV. Piecing Together the Timeline

BoK concludes with a color-coded matrix visualizing the impact strength of each of the five factors for the years 2026, 2027, and 2028. I translate the implications of this chart into a narrative timeline.

2026: The pattern of demand dominance and supply constraints continues. This is the most certain year.

2027: Contradictions begin to accumulate. Large company financing pressure rises, Chinese expansion accelerates, new fabs are not yet operational but vulnerabilities in financing end are exposed.

2028: Concentrated release from Samsung's P5, SK Hynix's Yongin, Micron's new fab. Risks on the supply side significantly amplify.

An Extension

The truly interesting part of this report is its narrative style. A central bank whose national foundation is memory did not cheerlead for its domestic industry. It spent significant篇幅 arguing the fragility of the financing structure, the bidirectional uncertainty of technological efficiency, and the微妙 inflection point in 2027 on the timeline. This restraint is an attitude in itself.

Its comparison to the telecom bubble is the part I reread several times. The script back then was: strong initial demand叠加competitive expansion,再叠加a technological innovation that arrived faster than expected (WDM - Wavelength Division Multiplexing), ultimately pushing the industry into rapid oversupply. Today's AI industry has all three conditions present, the difference is just that the critical technology equivalent to WDM hasn't appeared yet.

When domestic investors focus on the memory industry chain, their attention habitually falls on supply-side matters like HBM yield rates, CXMT progress. BoK's report pulls the focus back to the other side: the real variable in this cycle lies on the demand side, more precisely, hidden in the financing sustainability of the AI industry. Signals like Neocloud's vendor financing, off-balance-sheet leverage of SPVs, redemption halts in private credit funds—these deserve closer scrutiny than any expansion timetable.

At least until the first half of 2026, the story continues. The script thereafter depends on how the five variables above play out.