Author | Eastland

Header Image | Visual China

Changxin Technology is poised to list on the STAR Market, with its market capitalization highly likely to exceed 1 trillion yuan, and some optimistic voices even calling for 2 trillion yuan.

Changxin Technology has no actual controller. Its top five shareholders (including Hefei State-owned Assets, the National Integrated Circuit Industry Investment Fund) collectively hold approximately 58% of the shares. The "soul figure" Zhu Yiming holds less than 3% of the shares (indirectly), so even if Changxin's market cap rises further, it will be difficult for him to rank among the top tycoons.

Regarding Changxin Technology, the author already published an article on January 26, 2026 (published on Huxiu). This article introduces another excellent company founded by Zhu Yiming—GigaDevice (SH:603986), a storage chip giant with a market cap of 340 billion yuan.

The development history of GigaDevice is the "Prequel to Changxin Technology".

Diversification Born from "Finding Good Deals"

In April 2005, Zhu Yiming returned to China and founded "Beijing Xinjia Zhaowei Microelectronics Technology" (renamed GigaDevice Limited in 2010), with registered capital of 2 million yuan.

In December 2012, it completed its shareholding reform. After multiple rounds of capital increases, its registered capital reached 75 million yuan. Among them, Zhu Yiming held 16.292%.

In August 2016, it was listed on the Shanghai Stock Exchange, raising 517 million yuan.

In 2020, GigaDevice raised approximately 4.28 billion yuan through a private placement.

In January 2026, GigaDevice was listed on the Hong Kong Main Board (HK:03986), raising 4.68 billion Hong Kong dollars.

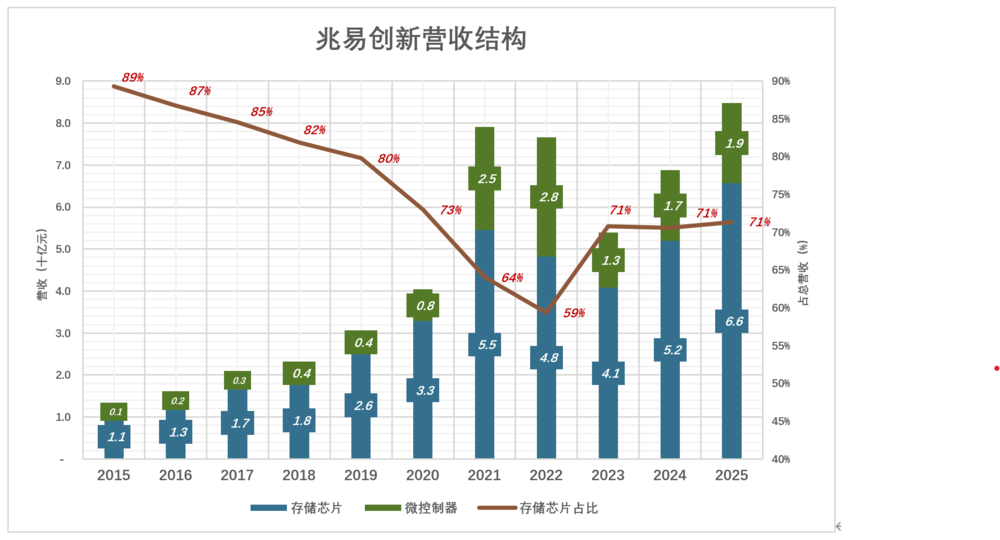

As financing channels opened up, GigaDevice's product structure diversified from a single storage chip through internal R&D and acquisitions, forming four product lines: storage chips, microcontrollers (MCU), sensors, and analog chips. However, the vast majority of revenue comes from storage chips and controllers.

NOR Flash

NOR Flash is GigaDevice's founding business, covering a variety of products with capacities ranging from 512Kb to 2Gb. Its global market share in 2025 was about 20% (ranking third globally and first in mainland China). In 2025, it achieved mass production of 45nm node SPI NOR Flash.

With the iteration of smartphone supply, the market for smaller-capacity NOR Flash has been declining—from $7 billion in 2006 to $1.58 billion in 2016. Samsung stopped developing new NOR Flash products as early as 2010. Although Micron did not completely exit, its market share fell from being the global leader in 2010 to fourth place in 2025.

AI computing power has no upper limit for storage chip capacity and transmission speed requirements. But in fields like automotive, consumer electronics, and industrial control, the requirement for storage chips is simply 'fit for purpose.' NOR Flash, with its fast read speed, high reliability, and low cost, has irreplaceability. A high-end electric vehicle equipped with an advanced intelligent driving system contains about 30 NOR Flash chips.

As international giants successively shut down mid-to-low-end DRAM and consumer-oriented NAND businesses, GigaDevice, in cooperation with Changxin Storage, gradually launched DDR3 and DDR4 products.

Low-end does not equal useless. GigaDevice seized the dividend from the giants' exit, gradually growing its storage chip business by "finding good deals." In 2024, its global market shares for NOR Flash, SLC NAND, and niche DRAM were 18.5%, 2.2%, and 1.7%, respectively.

Microcontrollers (MCU)

Before 2013, this market was dominated by European giants like STMicroelectronics. This was because the most critical component in an MCU is precisely the Flash memory chip.

After gaining a foothold in NOR Flash, GigaDevice did not rush into the high-end storage chip market. Instead, it entered the MCU market in 2013.

By 2024, it had mass-produced 63 series and over 700 products. In 2022, it entered the new energy vehicle market, providing specialized MCUs for application scenarios such as body domain control and chassis control.

Sensors and Analog Chips

In 2019, it entered the touch and fingerprint recognition sensor market through the acquisition of Silergy. In 2024, it acquired Suzhou Saixin, leading to explosive growth in its analog chip business.

From 2015 to 2018, the combined revenue from storage chips + microcontrollers accounted for 100% of total revenue.

In 2019, sensor revenue was 435 million yuan, accounting for 6.3% of revenue;

In 2021, storage chip revenue increased by 66% year-on-year to 5.45 billion yuan; but microcontroller revenue surged by 225%, causing the storage chip share to drop to 64%;

In 2022, storage chip revenue fell by 11.5% to 4.83 billion yuan; microcontroller revenue grew by 15.2% to 2.83 billion yuan; the storage chip share dropped to 59%;

......

In 2025, storage chip and microcontroller revenues were 6.56 billion yuan and 1.91 billion yuan, respectively, together accounting for 92% of total revenue; sensor and analog products combined revenue was 720 million yuan, accounting for 8% of total revenue.

Only 800,000 yuan in cash was in the registered capital (the rest was contributed as non-patented technology), which is barely enough to even open a small restaurant. Based on his capital and technical strength, Zhu Yiming precisely "found good deals," developing and growing in the cracks between giants.

A Rare High-Performer in the Storage Industry

1) Shipment Volume, Unit Price, and Gross Profit

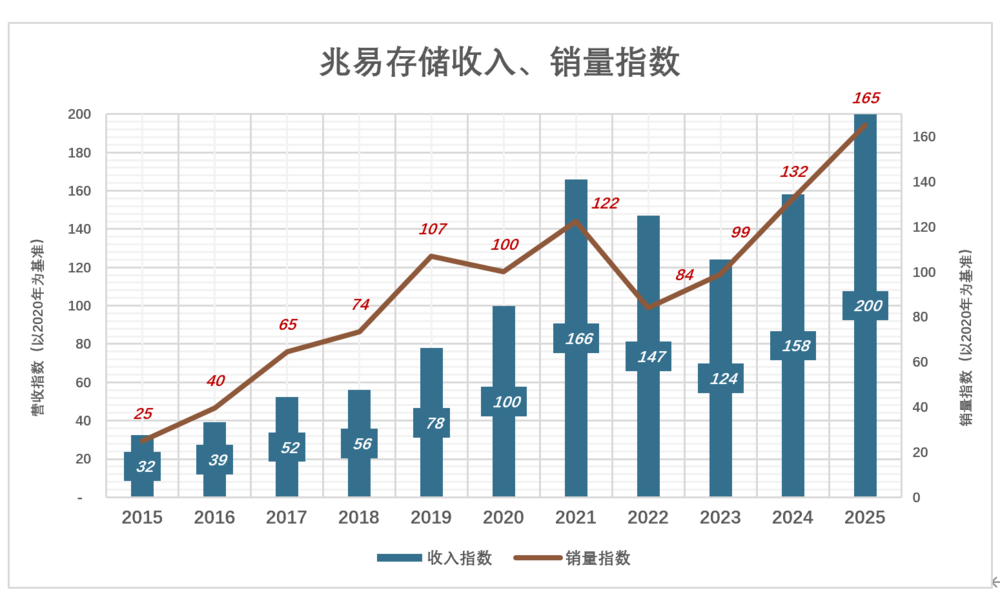

In 2025, the revenue index for storage chips was 200, and the sales volume index was 165 (with 2020 as the base year). The reason was an increase in the average selling price:

In 2020, storage chip shipments were 2.686 billion units, revenue was 3.28 billion yuan, with an average price of 1.22 yuan per unit;

In 2025, storage chip shipments were 4.436 billion units, and the average price rose to 1.48 yuan per unit, 21.1% higher than in 2020.

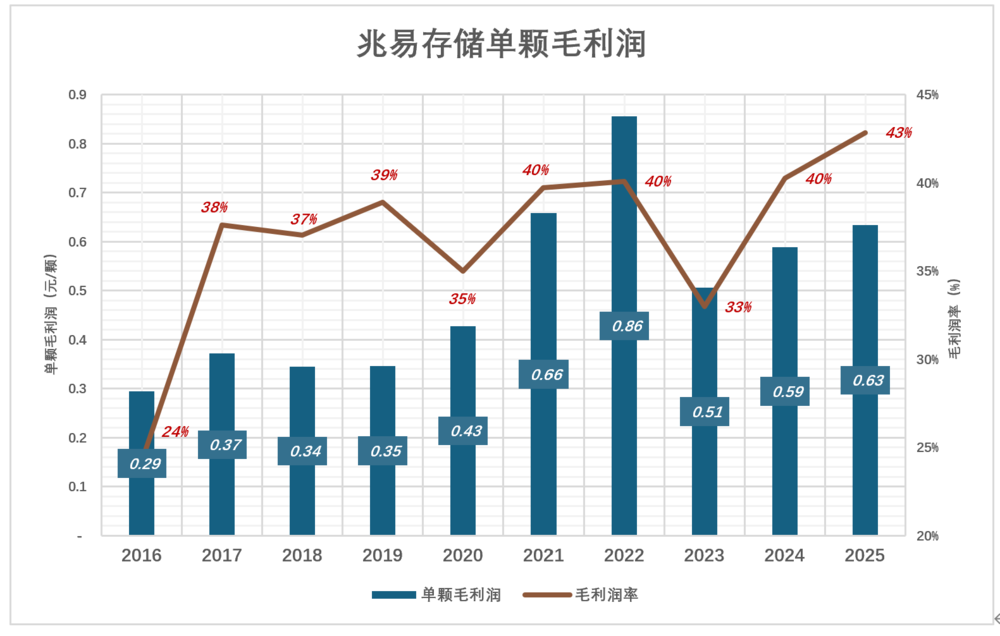

In 2022, demand for NOR Flash in the consumer, mobile phone, and PC sectors decreased. GigaDevice's storage chip shipments fell by 31.3% year-on-year. However, due to an increased proportion of mid-to-high-end products, gross profit per unit reached a record 0.86 yuan, with a gross profit margin of 40%.

In 2025, storage chip shipments reached 4.44 billion units, and gross profit per unit dropped to 0.63 yuan, 0.23 yuan lower than in 2022; but because costs decreased by 0.43 yuan, the gross profit margin actually increased to 43%.

GigaDevice's storage chips are primarily small-to-medium capacity. In 2025, the average selling price was only 1.48 yuan, which is not comparable to DDR5 or HBM chips that cost tens or even hundreds of yuan each.

2) Gross Profit Margin, Expense Ratio

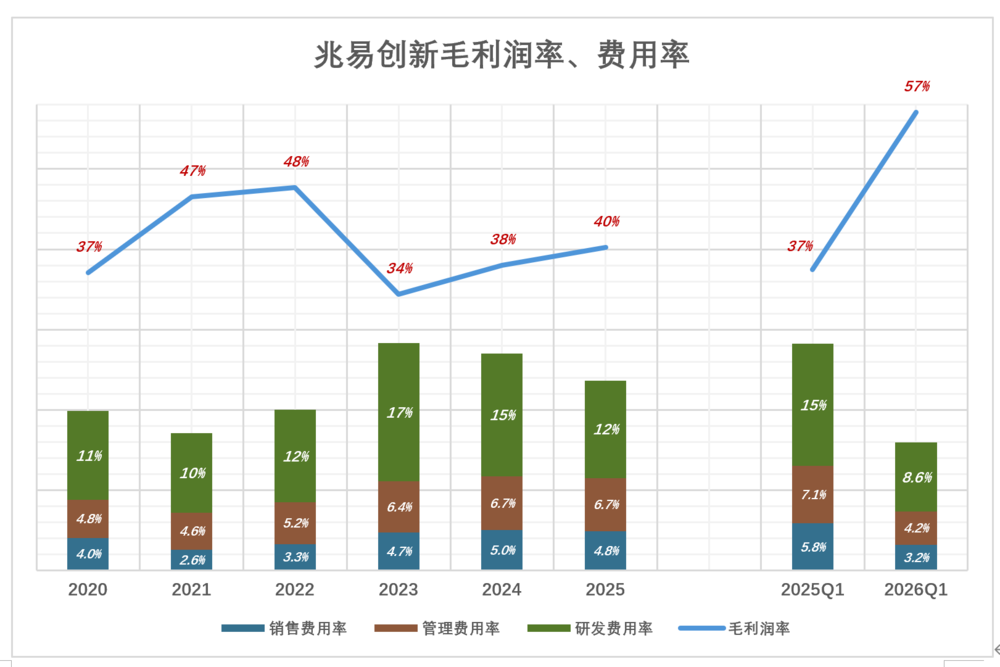

In the chart below, the blue line represents the gross profit margin, and the colored stacked bars represent the expense ratios. Operating profit is only possible when the blue "drowns out" the colors.

GigaDevice's blue line remains high above, demonstrating its strong high-performer credentials:

In the industry downturn of 2022, GigaDevice's gross profit was 3.88 billion yuan, with a gross profit margin as high as 47.7%; combined sales, management, and R&D expenses accounted for 20% of revenue; the gross profit margin was 28 percentage points higher than the total expense ratio!

In 2025, GigaDevice's revenue was 60% higher than in 2024; gross profit was 3.7 billion yuan, and the profit margin returned to above 40%;

In Q1 2026, performance exploded, with revenue increasing by 119% year-on-year; gross profit was 2.39 billion yuan, with a profit margin of 57.1%, 41 percentage points higher than the total expense ratio, far exceeding the profitability of 2022.

A 40% gross profit margin is not considered high for a light-asset company. It is quite remarkable for GigaDevice to control the total expense ratio below 30% while maintaining positive operating profit, especially at its revenue scale.

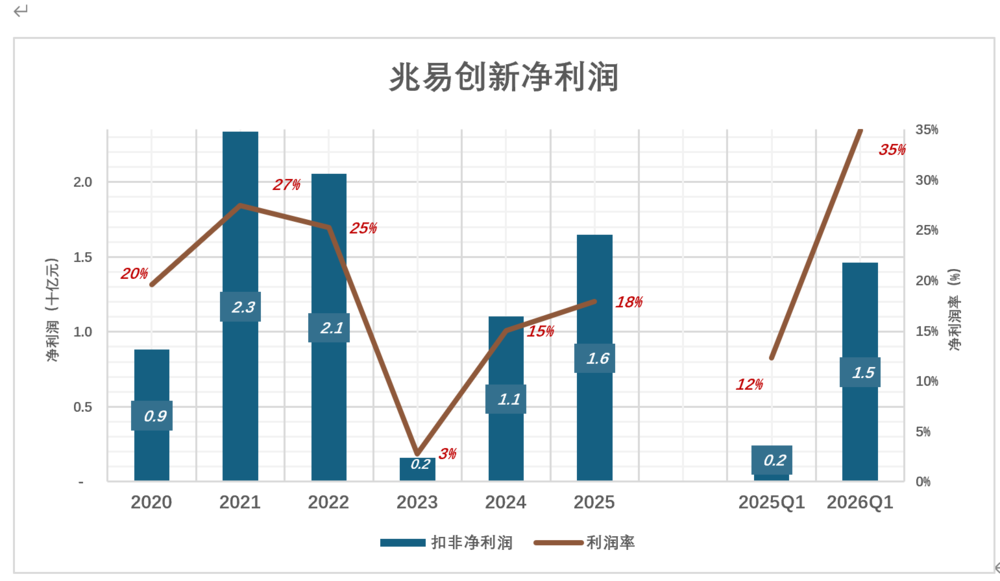

3) Cyclical Fluctuations in Net Profit

The storage chip industry exhibits strong cyclicality, and GigaDevice's performance clearly fluctuates with the industry cycle:

In 2021, net profit was 2.34 billion yuan, with a profit margin of 27.5%;

......

In 2023, net profit fell to 160 million yuan, with a profit margin of only 2.8%;

......

In 2025, net profit rebounded to 1.65 billion yuan, with a profit margin of 17.9%;

In Q1 2026, quarterly net profit reached 1.46 billion yuan, a year-on-year increase of 523%;

Binding with Changxin Forms the "Complete Entity"

Over the past 30 years, the storage chip industry has experienced four complete cycles:

1993~1996: Microsoft Windows drove DRAM demand to multiply, but overcapacity later emerged, causing prices to plummet;

2012~2015: Smartphones drove storage demand growth, but later this was completely offset by declining PC demand, leading to an industry downturn;

2016~2019: Android phone memory upgrades drove growth, but later this was completely offset by declining cloud computing demand, plunging the industry into deep losses;

2020~2023: The pandemic drove growth in mobile phone and PC shipments, and storage chip demand rose accordingly. Manufacturers, fearing shortages, overstocked. After the pandemic, the storage industry experienced a deep contraction;

In 2025, AI computing power created strong demand for high-bandwidth HBM chips. HBM uses a multi-layer chip stacking architecture, occupying about 3-4 times the wafer and packaging capacity of mid-to-low-end storage chips. The three giants—Samsung, SK Hynix, and Micron—allocated 90% of their capacity to high-end products like HBM and DDR5, leading to tight supply for mid-to-low-end products.

Semiconductor companies generally operate under four models: Vertical Integration (IDM), Fabless (Fablss), Foundry (Foundry),

and Outsourced Semiconductor Assembly and Test (OSAT).

IDM integrates chip design, manufacturing, packaging and testing, and product sales into one entity, representing a heavy-asset model.

The benefit is deep synergy between design and manufacturing, which helps optimize product yield, power consumption, and performance. The cost is high capital expenditure. Giants like Samsung, SK Hynix, and Micron adopt the IDM model.

The Fabless model allows companies to focus on chip design and R&D, outsourcing wafer manufacturing, packaging, and testing to specialized foundries, representing a light-asset model.

In a highly cyclical industry, does the light-asset model have a higher probability of success? In the storage chip field, the answer is no!

Taiwanese companies like ProMOS, Powerchip, and Inotera Memories adopted the Fabless model to avoid massive capital expenditure. When the storage chip industry was at a low point, these light-asset companies went bankrupt, were liquidated, or were acquired.

Heavy-asset giants engage in "counter-cyclical expansion"—investing huge sums to build factories and deploy advanced equipment; pouring fuel on the fire of overcapacity, accelerating price collapse, and speeding up the elimination of excess capacity.

Today's three storage chip giants (Samsung, Hynix, Micron) are all "survivors" of the industry's violent fluctuations.

Historical experience shows that counter-cyclical expansion is the "decisive move" in the storage chip field. The Fabless model is a light-asset model with no capacity to expand.

Due to the extremely high capital and technical barriers for R&D and manufacturing DRAM, GigaDevice found it difficult to achieve this on its own. In 2016, Zhu Yiming cooperated with the Hefei Municipal Government to establish Changxin Technology.

GigaDevice is not a complete entity and absolutely lacks the time and capital to evolve into an IDM model. Therefore, Zhu Yiming chose to cooperate with Hefei City.

In 2018, Zhu Yiming served as Chairman and CEO of Changxin Technology, explicitly stating he would not receive any salary before the company turned profitable. He also allocated half of the equity incentives he received (worth over 10 billion yuan) to reward employees.

In total, Zhu Yiming's shareholding proportion is slightly above 1% (post-listing). Zhu Yiming also voluntarily extended his lock-up period to 10 years.

Globally, it's not uncommon for founders of high-tech companies to make gestures like giving up salaries. Diluting equity often happens out of necessity (for financing), but control is the bottom line.

Zhu Yiming's series of actions made state-owned capital dare to invest heavily and banks dare to lend (long-term loans exceeding 100 billion yuan). As of the end of 2025, the original value of machinery and equipment at Changxin Technology reached 225.7 billion yuan, with accumulated depreciation of 55.2 billion yuan and a net book value of 169.3 billion yuan.

What does nearly 170 billion yuan worth of machinery and equipment mean? BYD has nine major production bases in China, with a double-shift capacity of about 8 million vehicles per year. Note, these are not simple assembly plants like a certain "super factory," but rather a vertically integrated industrial empire covering the entire new energy vehicle industry chain, from batteries to chips, producing over 75% of components in-house. As of the end of 2025, BYD's machinery and equipment had a net book value of 150.6 billion yuan, 18.7 billion yuan less than Changxin Technology's!

Assuming Changxin Technology's market capitalization reaches 2 trillion yuan, plus the value of his shares in GigaDevice, Zhu Yiming's net worth would not exceed 50 billion yuan, less than one-tenth of Zhong Shanshan's (According to the "2026 Hurun Rich List," the 20th-ranked Zhang Gang's family assets were 160 billion yuan).

*The above analysis is for reference only and does not constitute any investment advice!