Author: Arthur Hayes

Compiled by: Saoirse, Foresight News

The deities I worship manifest as adorable plush toys. Every year during the peak skiing season in Hokkaido from January to February, I pray to "Frowny Cloud"—the goddess who governs snowfall. The unique local climate pattern dictates that during seasons of abundant snowfall, the sky is perpetually overcast, with almost no sunlight. Fortunately, I also pray to the deity of vitamins (whose avatar is a cute little horse 🐴), which provides me with necessary supplements like Vitamin D3 tablets.

While I love snowfall, not all snow is of high quality and safe. The type of skiing I enjoy—unrestrained and free—requires a specific type of snow. Ideal conditions include low wind at night and temperatures between -5°C and -10°C. This allows new snow to bond firmly with the old snow, forming deep, soft powder. During the day, "Frowny Cloud" blocks certain wavelengths of sunlight, preventing south-facing slopes from melting under intense sun and reducing avalanche risks.

Sometimes, "Frowny Cloud" abandons us brave skiers at night. On cold, clear nights, the snow layer undergoes a process of warming and then cooling, forming a layer of ice crystals. This creates a persistent weak layer within the snowpack. This weakness remains for some time, and if a skier's weight transmits energy causing the weak layer to collapse, it can trigger a deadly avalanche.

As always, the only way to understand what kind of snowpack "Frowny Cloud" has created is to study history. On the slopes, we dig deep pits to analyze the types of snow that fell at different times. But this article is not about avalanche theory; in financial markets, we study history by analyzing charts and the interplay between historical events and price movements.

This article aims to explore the relationship between Bitcoin, gold, stocks (specifically the large-cap US tech stocks that constitute the Nasdaq 100 index), and US dollar liquidity.

Those who are neither bullish on cryptocurrencies nor believers in gold, or who are at the top of the financial world (dressed in luxury goods) and staunchly believe that "stocks are for the long term" (my GPA wasn't high enough to get into Professor Siegel's class at Wharton), are now rejoicing that Bitcoin has been the worst-performing major asset class in 2025. Gold believers scoff at crypto enthusiasts: if Bitcoin is truly a "protest tool" against the existing order, why hasn't its performance matched or exceeded that of gold?

And those who champion fiat currency stocks also mock crypto enthusiasts: they claim Bitcoin is just a high-beta version of the Nasdaq, yet in 2025 it didn't even achieve that; so, what justification is there for including cryptocurrencies in an investment portfolio?

This article will present a series of charts with my personal insights to interpret the context of these asset price movements. In my view, Bitcoin's performance is entirely consistent with its "nature"—it fell as fiat currency (especially the US dollar) liquidity decreased, because in 2025, the credit impulse brought by "Pax Americana" (referring to the relative stability and reduced conflict in the world or specific regions under US-led international order) was the most important factor affecting the market.

The surge in gold prices is due to price-insensitive sovereign nations hoarding gold heavily: they are worried about the safety of holding US Treasury bonds, especially after the US froze Russian bond holdings in 2022, and recent actions against Venezuela have further heightened concerns about dollar assets, leading them to choose gold as a reserve asset替代 US Treasuries.

Finally, the artificial intelligence (AI) bubble and all industries benefiting from it are not disappearing. In fact, US President Trump must increase government support for AI-related industries because AI is the biggest driver of US Gross Domestic Product (GDP) growth. This means that even if the growth rate of US dollar issuance slows, the Nasdaq index can continue to rise because Trump has effectively "nationalized" the AI industry. Those who have studied China's capital markets know that in the early stages of industry nationalization, related stocks often perform well, but as political goals take precedence over the return on equity for unpatriotic capitalists, these stocks eventually significantly underperform.

If the price movements of Bitcoin, gold, and stocks in 2025 confirm my market model, then I will continue to focus on fluctuations in US dollar liquidity. As a reminder to readers, my prediction is: the Trump administration will push the economy into "hot" operation by expanding credit. A booming economy will help the Republican party increase its chances of re-election in November this year. The expansion of US dollar credit will be achieved through three channels: expansion of the central bank's balance sheet, increased lending by commercial banks to "strategic industries," and lowering mortgage rates through "money printing."

Based on the above historical analysis, does this mean I can boldly invest my newly acquired fiat currency assets and maintain extremely high risk exposure, just like skiing freely on the slopes? I leave the answer to the readers.

The Decisive Chart

First, let's compare the returns of Bitcoin, gold, and the Nasdaq index during the first year of Trump's second term (2025), and the relationship between these asset performances and changes in US dollar liquidity.

I will elaborate later, but first, let me propose a hypothesis: if US dollar liquidity decreases, the prices of these assets should also fall. However, in reality, both gold and stock prices have risen, with only Bitcoin's performance meeting expectations—it's been a "disaster." Next, I will explain why gold and stocks managed to rise against the trend amid declining US dollar liquidity.

Chart labels: Bitcoin (red), Gold (gold), Nasdaq 100 Index (green), US Dollar Liquidity (magenta)

Gilded Exterior

My journey into cryptocurrency investment began with gold. From 2010 to 2011, as the Federal Reserve's quantitative easing (QE) policies intensified, I started buying physical gold coins in Hong Kong [1]. In absolute terms, the number of gold coins I held was not large, but relative to my net worth at the time, the proportion was extremely high. Ultimately, I learned a profound lesson in position management: in 2013, to conduct arbitrage trades on the ICBIT exchange, I had to sell my gold coins at a loss and buy Bitcoin instead.

Fortunately, things ended well. After all this, I still hold a significant amount of physical gold coins and bars in vaults around the globe, and gold and silver mining stocks dominate my stock portfolio. Readers might wonder: since I am a devout believer in the "great god Satoshi," why do I still hold gold?

The reason is that we are in the early stages of global central banks selling US Treasuries and increasing their gold holdings. Additionally, countries are increasingly using gold to settle trade deficits—even an analysis of US trade deficit data reveals this trend.

In short, I buy gold because central banks are buying gold. Gold has been the "true money" of human civilization for millennia. Therefore, if central bank managers distrust the current fiat currency financial system dominated by the US dollar, they will never choose Bitcoin as a reserve asset—they will (and are) choose gold. If gold's share in central bank foreign exchange reserves returns to the levels of the 1980s, its price could rise to about $12,000. Before you dismiss this prediction as "fantastical," let me prove it intuitively with data.

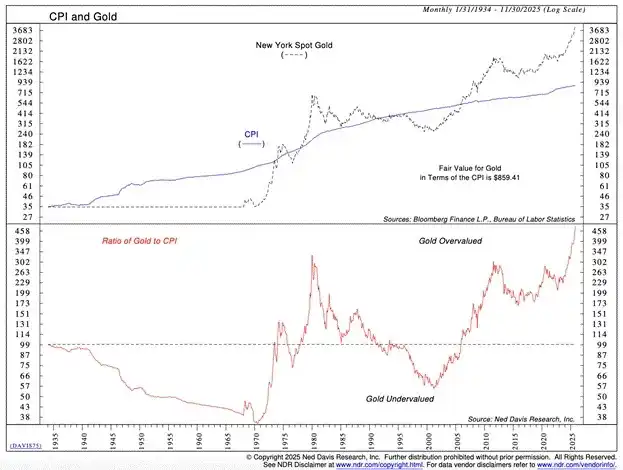

In the fiat currency system, the conventional wisdom is that gold is an "inflation hedge," so its price should roughly move in sync with officially reported Consumer Price Index (CPI) inflation data. The chart above shows that since the 1930s, the gold price has largely kept pace with the inflation index. But after 2008, and especially after 2022, the gold price has increased significantly faster than inflation. Is gold in a bubble that will cause heavy losses for investors like me?

Analysis chart of US Consumer Price Index (CPI) vs. Gold

If gold were truly in a bubble, retail investors would be flocking to it. The most popular way to trade gold is through exchange-traded funds (ETFs), with the "SPDR Gold ETF (GLD US)" being the largest [2]. When retail investors "go all in" on gold, the number of GLD shares outstanding increases. To compare this phenomenon across time and gold price cycles, we need to divide the number of GLD shares outstanding by the physical gold price. The chart below shows that this ratio is declining, not rising—meaning the real gold speculation frenzy has not yet arrived.

Chart label: Ratio of GLD US Shares Outstanding to Spot Gold Price

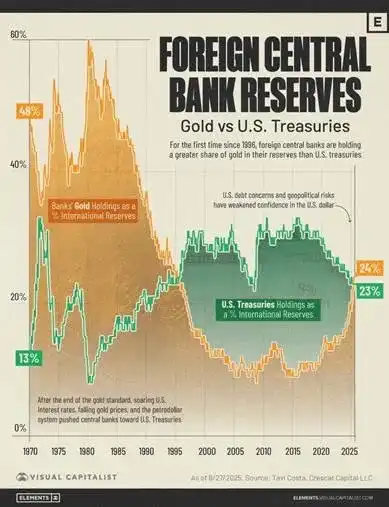

Since ordinary retail investors are not driving up the gold price, who are these "price-insensitive buyers"? The answer is global central banks. Over the past two decades, two key events have made these "monetary stewards" realize that the US dollar is no longer a reliable reserve currency.

In 2008, US financial giants triggered a global deflationary panic. Unlike the 1929 financial crisis (when the Fed largely did not intervene in credit contraction), this time the Fed abandoned its duty to maintain the purchasing power of the dollar and chose to "print money" to "save" some large financial institutions. This event became a "turning point" for the proportion of US Treasuries and gold held by central banks—the proportion of US Treasuries held peaked, while the proportion of gold held hit a trough.

In 2022, an action by US President Biden shocked the world: he froze Russia's Treasury holdings. Remember, Russia not only has the world's largest nuclear arsenal but is also one of the largest exporters of commodities. If the US dares to violate Russia's property rights, it could do the same to other, weaker or resource-rich countries. Naturally, other countries are reluctant to increase their holdings of US Treasuries to avoid the risk of asset seizure, so they have begun to accelerate their gold purchases. Central banks, as gold buyers, are price-insensitive: after all, if the US president orders your assets frozen, your loss is 100%; compared to that, the cost of buying gold to avoid counterparty risk is irrelevant.

Foreign Central Bank Reserves: Long-term Trend of Gold vs. US Treasuries

The fundamental reason for strong demand for this "ancient asset" from sovereign nations is that the settlement of global trade deficits is increasingly relying on gold. The record narrowing of the US trade deficit in December 2025 precisely proves that gold is re-emerging as the true global reserve currency—more than 100% of the change in the US trade deficit was due to increased gold exports.

"Data released by the US Commerce Department on Thursday showed the goods trade deficit shrank by 11% from the previous month to $52.8 billion. This deficit size is not only the lowest since June 2020 but also below the $63.3 billion predicted by economists surveyed by Reuters. From August to December, US exports grew by 3% to $289.3 billion, driven primarily by non-monetary gold exports; imports grew by 0.6%." — Source: Financial Times

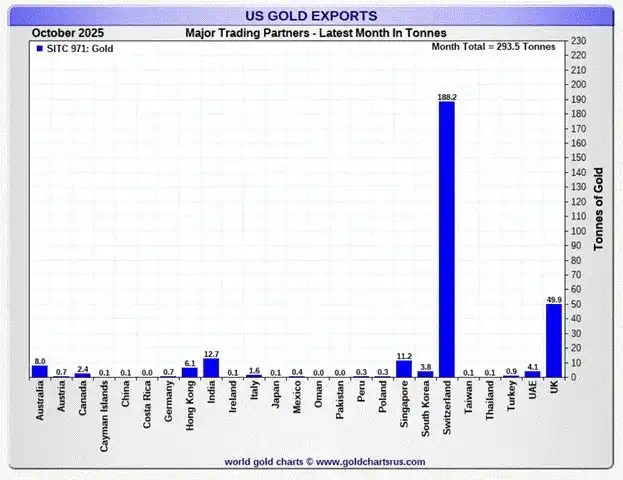

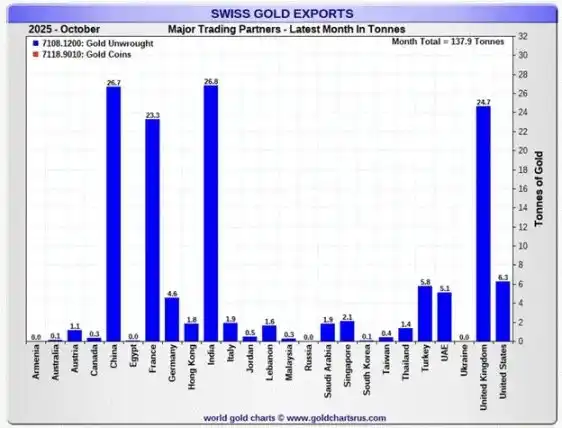

The flow of gold is as follows: the US exports gold to Switzerland, where it is refined and cast into ingots of various specifications, then shipped to other countries. The chart below shows that the main buyers of this gold are China, India, and other emerging economies—countries that are either good at producing physical goods or are commodity exporters. The goods produced by these countries eventually flow to the US, while gold flows to more "productive" regions of the world. "Productive" here does not mean these regions are better at filling out tedious reports or using the correct gender pronouns in email signatures, but that they can export energy and other key industrial commodities, and their ordinary people can produce steel, refine rare earths, and other physical products. Against the backdrop of declining US dollar liquidity, the reason gold prices can rise is that countries are accelerating the return to a global gold standard.

US Gold Export Data for October 2025

Swiss Gold Export Data for October 2025

Long-Term Assets Favor Liquidity

Every era has its hot tech stocks. During the US bull market of the 1920s, radio manufacturer RCA was the hot tech stock; in the 1960s and 70s, IBM, which produced new large computers, was all the rage; today, AI supercomputing companies and chip manufacturers are "riding high."

Humans are inherently optimistic and love to envision a bright future—as if the money tech companies are spending now will eventually create a social utopia. For those fortunate enough to "control the future" by holding these companies' stocks, wealth seems to fall from the sky. To make investors believe this "bright future" is inevitable, tech companies burn cash and take on debt. When liquidity is abundant (low financing costs), betting on the future becomes easy—because people believe these brave entrepreneurs will generate substantial cash flows in the future. Therefore, investors are willing to invest "worthless" cash now to buy tech stocks, hoping to obtain larger future cash flows, which also drives up the price-to-earnings ratios of tech stocks. Thus, during periods of excess liquidity, tech growth stock prices often rise exponentially.

Bitcoin is a "monetary technology." Its value is directly related to the degree of depreciation of fiat currency. The invention of Proof-of-Work (PoW) blockchain technology achieved a Byzantine fault-tolerant mechanism. This breakthrough is significant enough to ensure Bitcoin's value is greater than zero. But for Bitcoin's price to approach $100,000, continued depreciation of fiat currency is needed. The surge in the US money supply after the 2008 global financial crisis was the direct cause of Bitcoin's "asymptotic" price increase.

Therefore, my conclusion is:

When US dollar liquidity expands, Bitcoin and the Nasdaq index rise.

But the problem is that recently, Bitcoin's price has diverged from the Nasdaq index.

I believe the reason the Nasdaq index did not correct with the decrease in US dollar liquidity in 2025 is that both China and the US have "nationalized" the AI industry.

The "tech gurus" in the AI field have instilled in the leaders of the world's two largest economies the idea that AI can solve all problems—it can reduce labor costs to zero, cure cancer, increase productivity, "democratize" creativity, and, more importantly, allow a country to militarily dominate the world. Therefore, regardless of how vaguely "winning" is defined, whichever country "wins" in AI will rule the world.

China has long agreed with this view of a tech future, which also aligns highly with the Chinese Communist Party's top-down model of setting development goals through five-year plans. Chinese stock investors typically study every five-year plan and its annual revisions carefully to determine which industries and related stocks will receive cheap credit support from the government and policy倾斜 in market competition.

In the US, at least in this era, this kind of "policy-oriented investment analysis" is still novel. Industrial policy is actually a "common choice" for both the US and China,只是宣传方式不同而已. Trump has been captivated by the "charm" of AI, and now "winning in AI" has become a key part of his economic policy. The US government has effectively "nationalized" all segments of the AI industry deemed related to "winning": through executive orders and government investment, Trump has weakened free market signals, causing capital to flood into all AI-related areas regardless of actual return on equity.

This is why the Nasdaq index diverged from Bitcoin's price and US dollar liquidity trends in 2025 and managed to rise against the trend.

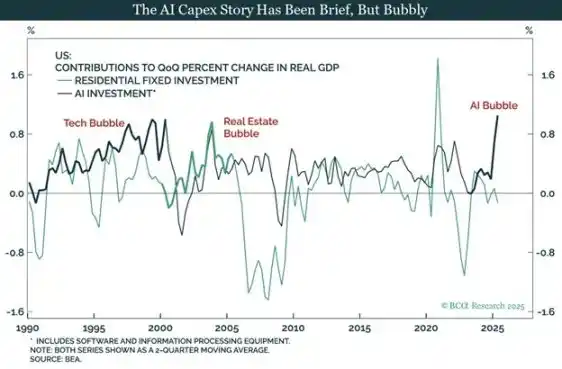

The Bubble History of AI Capital Expenditure

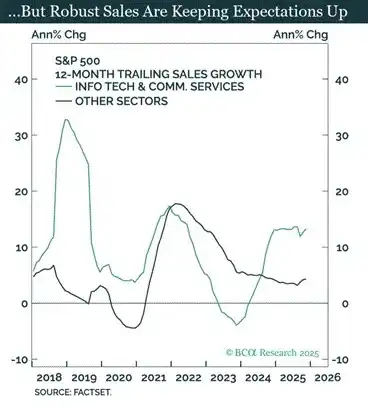

S&P 500 Sector Sales Growth Comparison: Tech / Communication Services vs. Other Sectors

Bubble or not, increased spending to "win the AI competition" is driving US economic growth. Trump promised during his campaign to run the economy "hot," so even if future retrospect shows that the return on equity for these expenditures is below the cost of capital, he will not stop now.

Chinese Strategic Industry Stock Prices (in CNY)

GDP Growth vs. Stock Return Relationship: Comparison of Global Economies

US tech investors should be cautious about their "expectations." The US industrial policy aimed at "winning the AI competition" is highly likely to make investors' capital "go down the drain." Trump's (or his successor's) political goals will eventually diverge from the interests of shareholders in companies deemed "strategic." Chinese stock investors have learned this lesson the hard way. Confucius said, "Learn from history." But judging by the Nasdaq's excellent performance, US investors have clearly not learned this lesson.

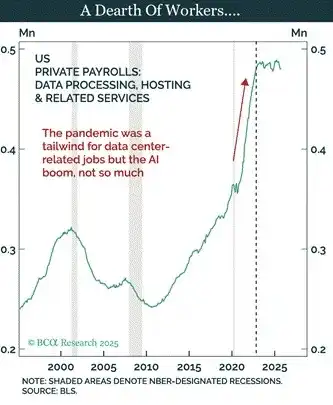

Change in US Data Processing / Hosting Industry Private Employment

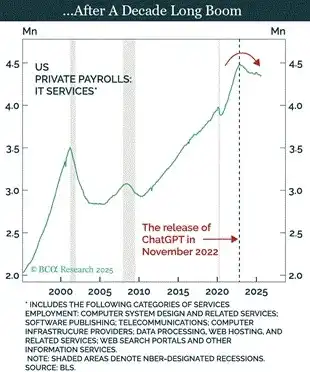

Change in US IT Services Industry Private Employment

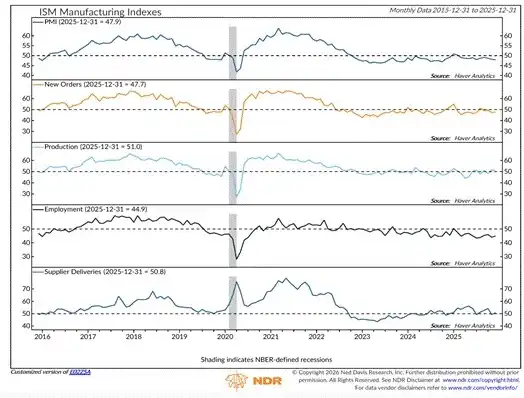

US ISM Manufacturing Index Sub-indicator Trends

Chart note: Values below 50 indicate economic contraction. GDP growth has not led to a manufacturing recovery.

I thought Trump was the "representative of the white working class"? Don't be silly, friend. Former US President Clinton "sold" your jobs to China; Trump brought factories back to the US, but now the factory floors are full of AI robots from Elon Musk. Sorry, you've been "fooled" again—but US Immigration and Customs Enforcement (ICE) is still hiring [3]!

These charts clearly show that the rise of the Nasdaq index is backed by the US government. Therefore, even if overall US dollar credit growth is weak or contracting, the AI industry can still get all the funding it needs to "win." This is why the Nasdaq index diverged from my US dollar liquidity index in 2025 and outperformed Bitcoin. I believe the AI bubble has not yet burst. This "outperformance of Bitcoin" will be a "norm" in global capital markets until the situation changes—most likely a turning point, as predicted by Polymarket, if the Democrats control the House of Representatives in 2026, or even win the presidential election in 2028. If the Republicans are the "futurists" (Jetsons style), then the Democrats are the "conservatives" (Flintstones style).

Since gold and the Nasdaq are "on a roll," how can Bitcoin "regain its vitality"? The answer is: US dollar liquidity must expand. Clearly, I believe US dollar liquidity will expand in 2026. Next, let's explore the specific paths.

Running the Economy "Hot"

First, I believe the significant expansion of US dollar liquidity this year (2026) will rely on three pillars:

- The Federal Reserve will expand its balance sheet through "money printing";

- Commercial banks will increase lending to strategic industries;

- The Federal Reserve will lower mortgage rates through "money printing."

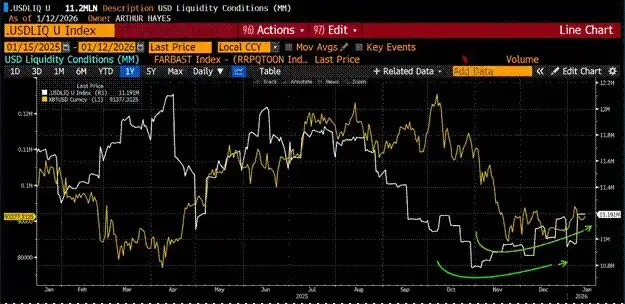

As shown in the chart above, in 2025, due to quantitative tightening (QT) policy [4], the size of the Fed's balance sheet continued to shrink. In December 2025, the QT policy ended, and the Fed introduced its latest "money printing plan" at its meeting that month—"Reserve Management Purchases (RMP)." I have detailed the mechanics of RMP in my article "Love Language." The chart clearly shows that the Fed's balance sheet size bottomed in December 2025. Under the RMP plan, the Fed injects at least $40 billion in liquidity into the market monthly; and as US government financing needs increase, this purchase size will expand.

The chart above is the weekly data on loan growth in the US banking system released by the Fed, called "Other Deposits and Liabilities (ODL)." I started following this indicator after reading Lacy Hunt's research. Starting in Q4 2025, banks began to lend more. The process of banks issuing loans is essentially creating deposits (i.e., creating money) "out of thin air."

Banks like JPMorgan Chase are happy to lend to companies directly supported by the US government—JPMorgan launched a $1.5 trillion lending facility for this purpose. The specific model is as follows: the US government injects capital (equity investment) into a company or provides a procurement agreement (promising to buy the company's products in the future), then the company applies for a loan from JPMorgan or other large commercial banks to expand production. The government's "backing" reduces the company's default risk (by guaranteeing demand), so banks are willing to "create money" to finance these strategic industries. This is exactly the same as China's credit creation model—credit creation shifts from the central bank to commercial banks. At least initially, the velocity of money increases significantly, driving nominal GDP growth above trend.

The US will continue to project its military influence, and manufacturing weapons of mass destruction requires financing from the commercial banking system. This is also why bank credit growth will show a long-term upward trend in 2026.

Trump comes from the real estate industry and understands the financing of real estate projects well. Recently, Trump issued a new policy requiring US government-sponsored enterprises (GSEs) Fannie Mae and Freddie Mac to use funds on their balance sheets to purchase $200 billion worth of mortgage-backed securities (MBS) [5]. Before Trump issued this directive, these funds were idle on Fannie and Freddie's balance sheets. Therefore, this policy will directly increase US dollar liquidity. If this policy proves effective, Trump is likely to introduce similar measures further.

Boosting the real estate market by lowering mortgage rates will allow many Americans to take out mortgages against record home equity. This "wealth effect" will make ordinary people satisfied with the economy on election day, leading them to vote for the Republican party (red team). For us risk asset holders, most importantly, this will create more credit funds to purchase various financial assets.

Bitcoin (gold curve) and US dollar liquidity (white curve) bottomed almost simultaneously. As mentioned earlier, as US dollar liquidity expands significantly, the Bitcoin price will also rise. Forget Bitcoin's poor performance in 2025—the liquidity then simply couldn't support a crypto portfolio. But we cannot draw the wrong conclusion from Bitcoin's poor performance in 2025: its price movement has always been closely related to liquidity changes, in the past and now.

Trading Strategy

I am an aggressive speculator. Although the Maelstrom fund is almost fully invested, given my firm belief in US dollar liquidity expansion, I still want to further increase risk exposure. Therefore, I have established long positions in MicroStrategy (stock code: MSTR US) and Metaplanet (stock code: 3350 JT), gaining leveraged exposure to Bitcoin through these stocks without trading perpetual contracts or option derivatives.

I divided Metaplanet's share price (white curve) by the Bitcoin price in JPY, and MicroStrategy's share price (gold curve) by the Bitcoin price in USD. The results show that the "Bitcoin ratio" for these two stocks is at a low point over the past two years and has fallen significantly from its peak in mid-2025. If the Bitcoin price can rebound to $110,000, investors will again prefer to gain indirect exposure to Bitcoin through these stocks. Due to the natural leverage in these companies' capital structures, their stock prices will outperform Bitcoin itself during a Bitcoin rally.

Additionally, we continue to accumulate Zcash (ZEC). The departure of developers from the Electric Coin Company (ECC) is not negative news. I firmly believe that these developers will develop better, more impactful products within independent for-profit entities. I am glad to have the opportunity to buy ZEC at low prices from those "panic sellers."

Speculators, charge ahead and climb upward. The outside world is full of risks, so be sure to protect yourselves. May peace be with you, and hail to the goddess "Frowny Cloud"!

Related Questions

QAccording to Arthur Hayes, why did Bitcoin underperform compared to gold and the Nasdaq 100 in 2025?

ABecause Bitcoin's price is directly tied to US dollar liquidity, which contracted in 2025. Gold's rise was driven by price-insensitive sovereign nations buying it as a reserve asset to replace US Treasuries, and the Nasdaq's rise was fueled by the 'nationalization' of the AI industry, which received government-backed funding despite the liquidity contraction.

QWhat are the three pillars Arthur Hayes believes will drive a significant expansion of US dollar liquidity in 2026?

AThe three pillars are: 1) The Federal Reserve expanding its balance sheet through 'printing money' (e.g., the Reserve Management Purchases program). 2) Commercial banks increasing lending to 'strategic industries' backed by the government. 3) Lowering mortgage rates through 'printing money' via government-sponsored enterprises like Fannie Mae and Freddie Mac.

QHow does Hayes explain the recent surge in gold prices, and who does he identify as the primary buyers?

AHayes explains that the surge is not due to retail investor speculation but is driven by central banks. These 'price-insensitive' sovereign buyers are accumulating gold as a reserve asset due to concerns over the safety of US Treasuries, a trend that accelerated after the US froze Russian assets in 2022. This is part of a move towards a de facto global gold standard for settling trade imbalances.

QWhat is the core reason Hayes gives for the divergence in performance between the Nasdaq 100 and Bitcoin in 2025?

AThe core reason is the 'nationalization' of the AI industry in the US. The US government, under Trump, made winning the AI race a key economic policy, directing capital and cheap credit into AI-related sectors regardless of traditional market signals or return on equity. This government backing allowed the Nasdaq to rise even as overall dollar liquidity shrank, while Bitcoin's performance remained directly correlated to that liquidity.

QWhat trading strategy does Hayes mention for gaining leveraged exposure to Bitcoin's expected price increase?

AHayes mentions taking long positions in the stocks of MicroStrategy (MSTR) and Metaplanet (3350 JT). He argues that these stocks, which trade at a low ratio to the Bitcoin price, offer a leveraged play on Bitcoin because their capital structures contain inherent leverage, meaning their prices would rise more than Bitcoin's during an upward move.

Related Reads

Trading

Hot Articles

What is $BITCOIN

DIGITAL GOLD ($BITCOIN): A Comprehensive Analysis Introduction to DIGITAL GOLD ($BITCOIN) DIGITAL GOLD ($BITCOIN) is a blockchain-based project operating on the Solana network, which aims to combine the characteristics of traditional precious metals with the innovation of decentralized technologies. While it shares a name with Bitcoin, often referred to as “digital gold” due to its perception as a store of value, DIGITAL GOLD is a separate token designed to create a unique ecosystem within the Web3 landscape. Its goal is to position itself as a viable alternative digital asset, although specifics regarding its applications and functionalities are still developing. What is DIGITAL GOLD ($BITCOIN)? DIGITAL GOLD ($BITCOIN) is a cryptocurrency token explicitly designed for use on the Solana blockchain. In contrast to Bitcoin, which provides a widely recognized value storage role, this token appears to focus on broader applications and characteristics. Notable aspects include: Blockchain Infrastructure: The token is built on the Solana blockchain, known for its capacity to handle high-speed and low-cost transactions. Supply Dynamics: DIGITAL GOLD has a maximum supply capped at 100 quadrillion tokens (100P $BITCOIN), although details regarding its circulating supply are currently undisclosed. Utility: While precise functionalities are not explicitly outlined, there are indications that the token could be utilized for various applications, potentially involving decentralized applications (dApps) or asset tokenization strategies. Who is the Creator of DIGITAL GOLD ($BITCOIN)? At present, the identity of the creators and development team behind DIGITAL GOLD ($BITCOIN) remains unknown. This situation is typical among many innovative projects within the blockchain space, particularly those aligning with decentralized finance and meme coin phenomena. While such anonymity may foster a community-driven culture, it intensifies concerns about governance and accountability. Who are the Investors of DIGITAL GOLD ($BITCOIN)? The available information indicates that DIGITAL GOLD ($BITCOIN) does not have any known institutional backers or prominent venture capital investments. The project seems to operate on a peer-to-peer model focused on community support and adoption rather than traditional funding routes. Its activity and liquidity are primarily situated on decentralized exchanges (DEXs), such as PumpSwap, rather than established centralized trading platforms, further highlighting its grassroots approach. How DIGITAL GOLD ($BITCOIN) Works The operational mechanics of DIGITAL GOLD ($BITCOIN) can be elaborated on based on its blockchain design and network attributes: Consensus Mechanism: By leveraging Solana’s unique proof-of-history (PoH) combined with a proof-of-stake (PoS) model, the project ensures efficient transaction validation contributing to the network's high performance. Tokenomics: While specific deflationary mechanisms have not been extensively detailed, the vast maximum token supply implies that it may cater to microtransactions or niche use cases that are still to be defined. Interoperability: There exists the potential for integration with Solana’s broader ecosystem, including various decentralized finance (DeFi) platforms. However, the details regarding specific integrations remain unspecified. Timeline of Key Events Here is a timeline that highlights significant milestones concerning DIGITAL GOLD ($BITCOIN): 2023: The initial deployment of the token occurs on the Solana blockchain, marked by its contract address. 2024: DIGITAL GOLD gains visibility as it becomes available for trading on decentralized exchanges like PumpSwap, allowing users to trade it against SOL. 2025: The project witnesses sporadic trading activity and potential interest in community-led engagements, although no noteworthy partnerships or technical advancements have been documented as of yet. Critical Analysis Strengths Scalability: The underlying Solana infrastructure supports high transaction volumes, which could enhance the utility of $BITCOIN in various transaction scenarios. Accessibility: The potential low trading price per token could attract retail investors, facilitating wider participation due to fractional ownership opportunities. Risks Lack of Transparency: The absence of publicly known backers, developers, or an audit process may yield skepticism regarding the project's sustainability and trustworthiness. Market Volatility: The trading activity is heavily reliant on speculative behavior, which can result in significant price volatility and uncertainty for investors. Conclusion DIGITAL GOLD ($BITCOIN) emerges as an intriguing yet ambiguous project within the rapidly evolving Solana ecosystem. While it attempts to leverage the “digital gold” narrative, its departure from Bitcoin's established role as a store of value underscores the need for a clearer differentiation of its intended utility and governance structure. Future acceptance and adoption will likely depend on addressing the current opacity and defining its operational and economic strategies more explicitly. Note: This report encompasses synthesised information available as of October 2023, and developments may have transpired beyond the research period.

363 Total ViewsPublished 2025.05.13Updated 2025.05.13

Meet ZetaChain: The Universal L1 for Apps That Work Everywhere — Even on Bitcoin

ZetaChain is the first ever Universal Blockchain to enable native connection across all blockchain ecosystems.

47.0k Total ViewsPublished 2025.06.16Updated 2025.06.16

Fractal Bitcoin: Scaling Bitcoin as a Recursive System

Fractal Bitcoin is a Layer-1 scalability solution built on the Bitcoin core code, enabling infinite scalability through a recursive approach.

46.5k Total ViewsPublished 2025.06.30Updated 2025.06.30