A&T Capital 发布了《Web3 趋势报告 2023 》,对今年的创新赛道和应用做出以下 6 点 预测,本文为中文精华版。

1.市场和创新:Web3 正在打造新范式

Web3 一级市场基金管理规模达 500 亿美元;NFT 市场规模超过 200 亿,NFT 持有者超 300 万;

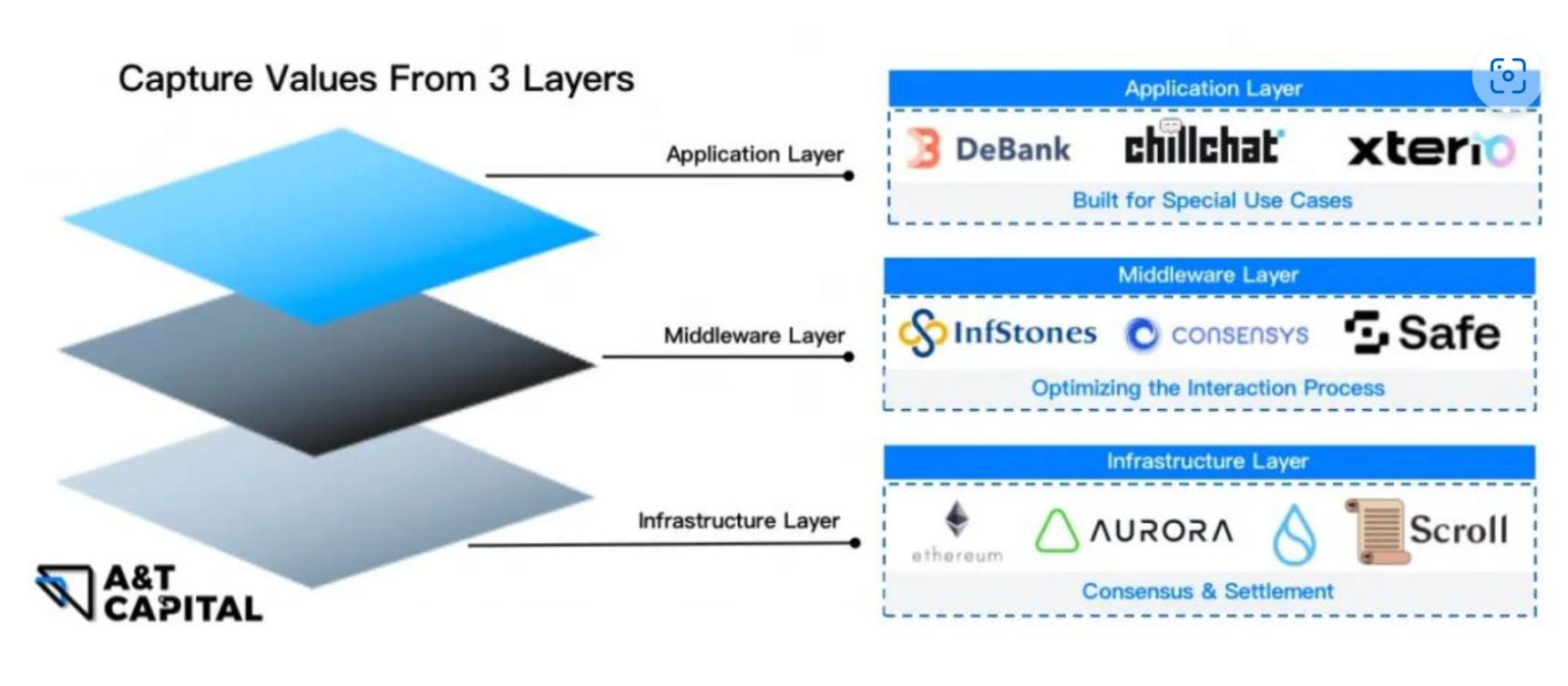

在各个技术层,都能看到 Web3 带来的革新,应用层为用户打造专门场景,中间层优化交互过程,基础设施层优化共识和结算;

2.零知识证明:零知识二层方案是以太坊扩展长期更好的选择

ZK L2:StarkNet、Scroll、zKSync 等主流 ZK L2 大概率能在 2023 年内上线主网,让以太坊扩容进一步加速;且会是多方案长期并存的市场,行业也将受益于这种的多样化。

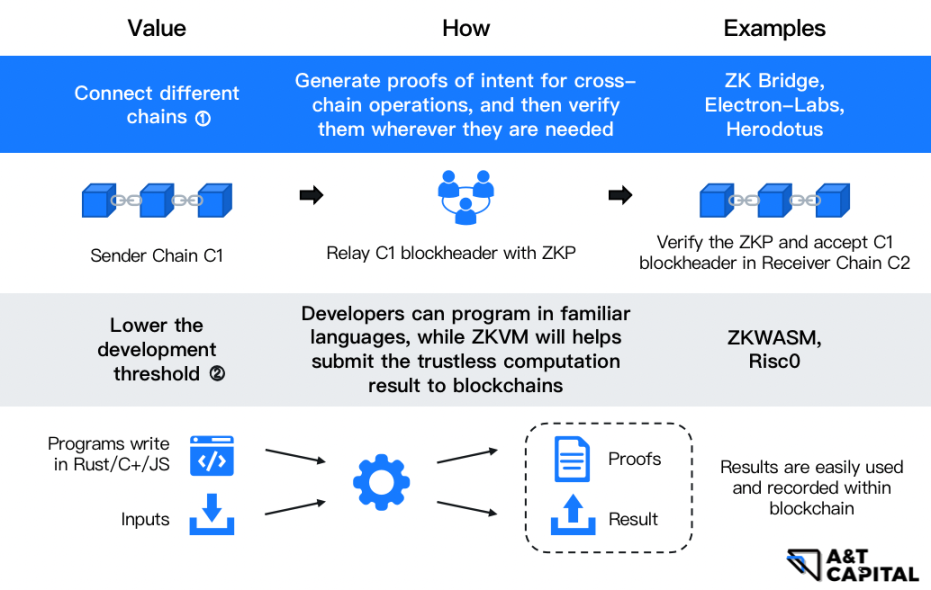

不止于扩容:ZKP 技术对区块链行业的不同部分的价值被越多的发掘。

ZKP + Light Client 的设计有望颠覆现有链间互操作性赛道;

ZKWASM、Rust 版 ZKVM 等虚拟机将让 Web2 开发者在尽可能不改变固有开发习惯的基础上进入 Web3.0;

用 ZKP 将链下执行结果以可验证的形态传递至链上,适用于各类不适于链上执行的内容,是 L2 之外又一种对区块链整体效能的提升;

3.公链关键词:并行计算、模块化设计、应用链

并行计算:作为在传统高性能计算领域已经被大范围采用的技术,并行计算近来被 Sui/Aptos/Fuel Network 等项目带入区块链行业的大众视野,将在更多的场景中成为将区块链网络计算能力推向更高的极限;

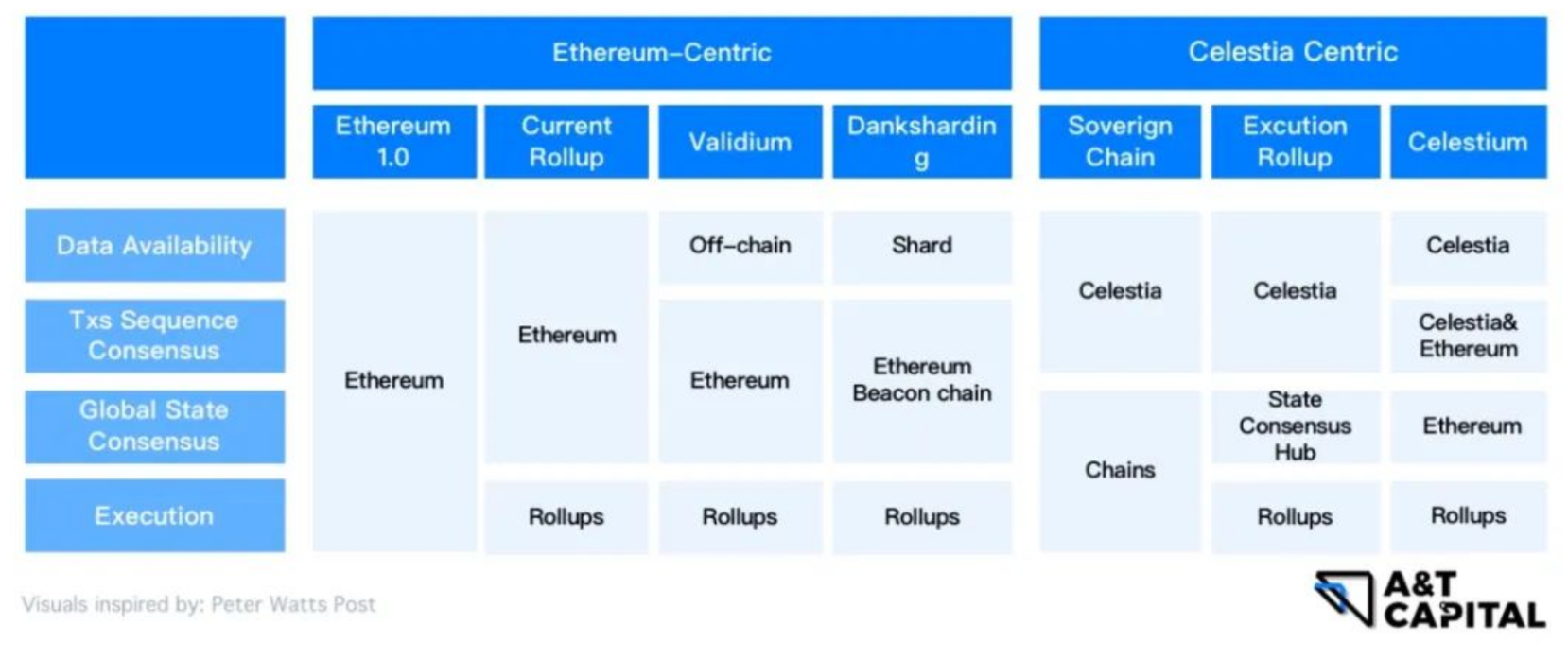

模块化设计:借助以太坊 +L2 组合的普及以及 Celestia 不懈的布道,模块化已逐步成为区块链主流设计理念:一方面通过不同模块的轻松充足满足不同需求,另一方面以单个模块为目标缩短开发周期、提升开发质量;

应用链:得益于在定制化、独享网络效能、更丰富的价值捕获等方面的优异表现,应用链将在 2023 找到确切的适用场景,并占据一定的市场份额,形态可多样化 例如:L1/L2/L3;

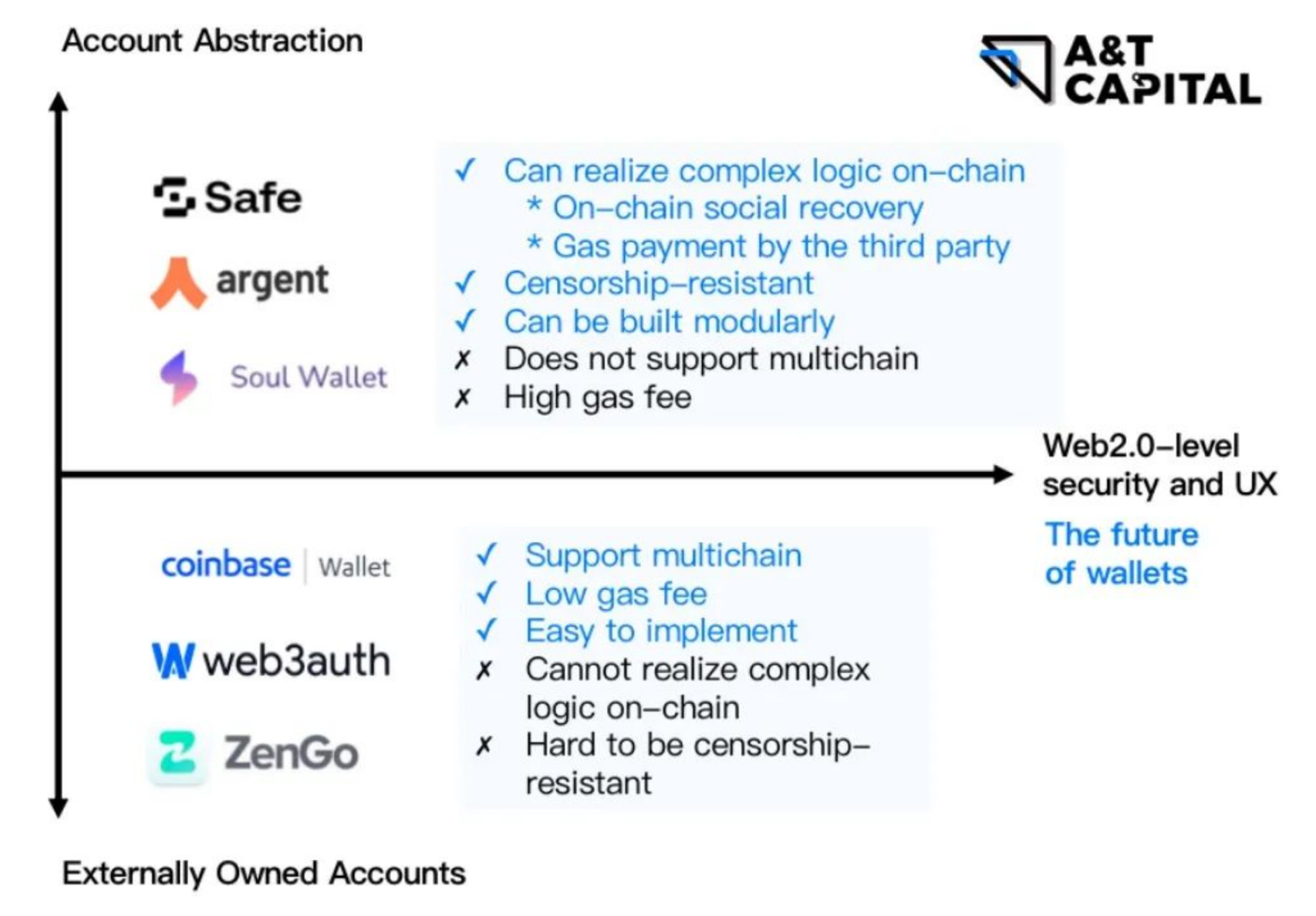

4.钱包:账户抽象(AA)钱包和外部拥有账户(EOA)钱包通过不同的权衡将实现更低的使用门槛和更优的交互体验。

钱包作为 Web3 的流量入口,目前普遍应用的助记词钱包存在安全门槛高、交互流程繁琐等导致的用户体验差的问题。为解决这一痛点、为十亿级新用户进入 Web3 铺平道路,账户抽象(AA)钱包能够借助链上智能合约实现;外部拥有账户(EOA)钱包能够借助链下 MPC 技术实现。

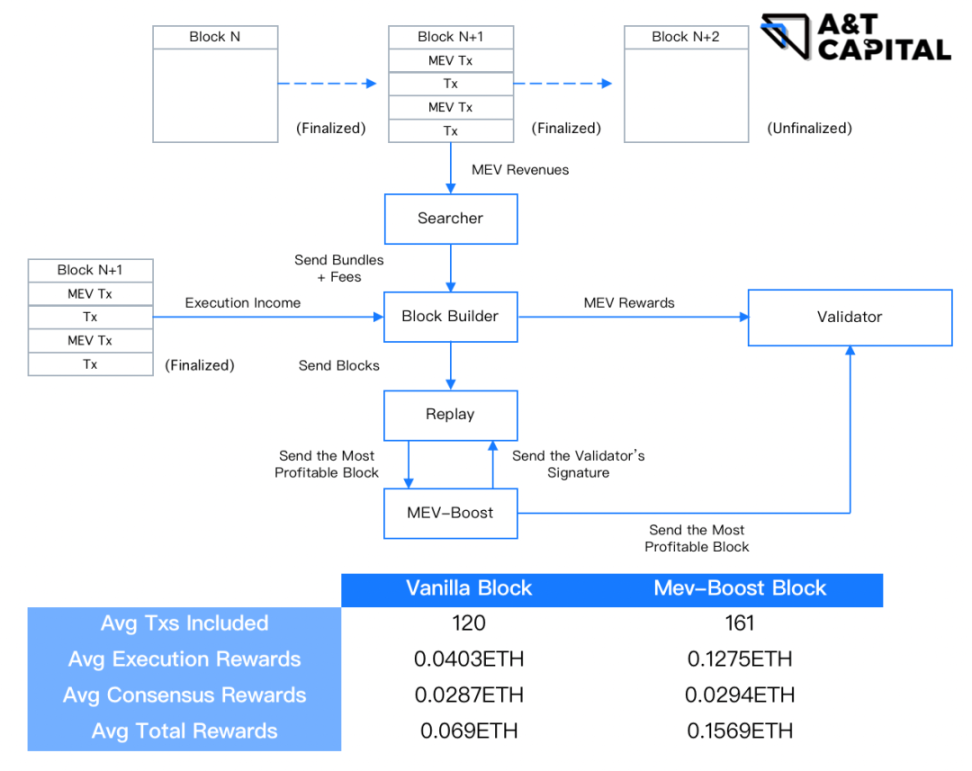

5.MEV:一个去信任、抗审查、无许可的 MEV 提取市场会取代现有方案

MEV-Boost 是现行的以太坊 MEV 提取解决方案。尽管接入 MEV-Boost 能为 Validator 带来更多收益,但它仍是一套受信任的、被审查的结构。

将「可编程隐私」带入 MEV 市场参与者的沟通网络中,会是实现更理想的 MEV 提取市场的途径。

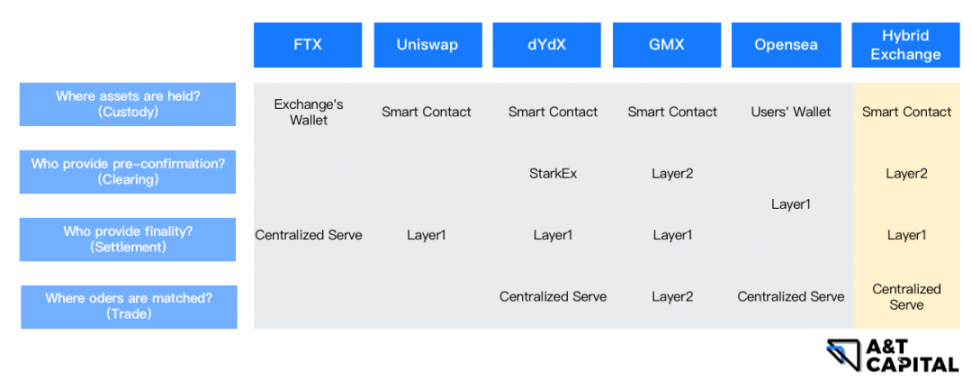

6.交易所:托管、交易、结算等职能分离是大势所趋

FTX 事件深深刺痛了市场,集托管、交易、结算于一身的中心化交易所有较高的道德风险。

交易所公布储备金证明只是一小步,想要从根本上解决这一痛点,要么拥抱监管,将客户资产存放在受信任的合规托管商,要么选择去中心化,将资产锁定在链上的智能合约中。

2022 年,加密行业经历了 FTX 溃败、Luna 崩盘,以太坊升级合并等重大事件。市场在调整,但创新的力量不曾停止涌入。我们期待 Web3 以更加创新、安全、高效、便捷的姿态走向大众。