近日,加密分析公司TokenUnlocks发布《2022年度报告》,其中回顾了2022年加密货币行业并对2023年的市场进行了分析展望,PANews将部分内容编译如下。

“”

2022年加密货币市场回顾

”“

据CoinGecko统计数据显示,2022年全球加密货币市值大幅下降,从2021年的2.3万亿美元暴跌至仅8270亿美元,跌幅高达64%。作为市值最大的两个加密货币——BTC和ETH过去一年也呈现出大幅下跌的态势,跌幅分别达到64%和67%。究其原因,还要归结于2022年发生的几个大事件:

”“

首先,Terra生态系统崩盘,该事件导致几家大型加密公司破产;

”“

其次,加密货币交易所FTX在2022年第4季度迎来了破产闹剧;

”“

最后,也是最容易被忽视的一点就是一些项目代币迎来到期解锁,由于解锁后投资者们开始转移代币,结果引发了市场流动性激增。

”“

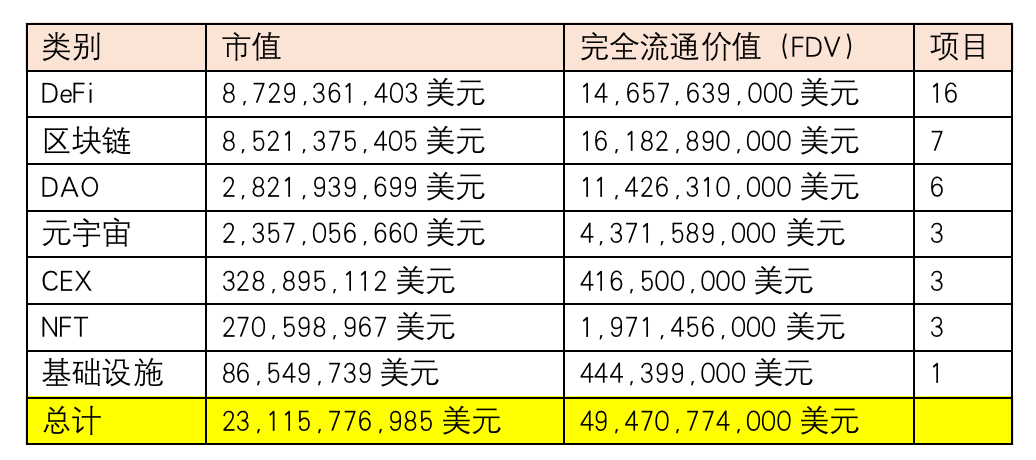

CoinGecko从2022年7月4日到2022年12月31日期间对143种协议进行了跟踪研究,包括DeFi、区块链、DAO、元宇宙、CEX、NFT、基础设施者7个主要项目类别,这些项目的总市值已经超过230亿美元,这一数字仅仅只是2023年初8720亿美元加密货币总市值的2.6%。

接下来,让我们再来看看代币解锁的情况。

”“

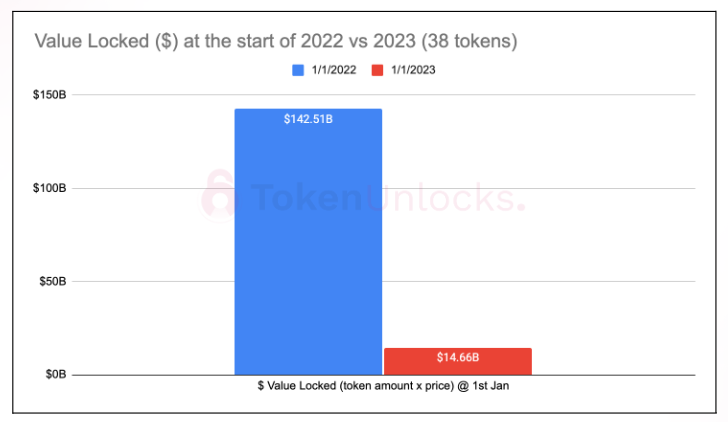

2022年初,我们跟踪了38个代币,其总锁定价值约为1425.1亿美元(注:仅仅是已分配代币,不包括质押、流动性挖矿、抵押等),令人大跌眼镜的是,2023年初这一数字已跌至146.6亿美元,这意味着代币锁定价值已下跌了89.7%。 究其原因,主要有两点:

”“

1、代币价格急剧下跌

”“

2、2022年发行的代币数量过多

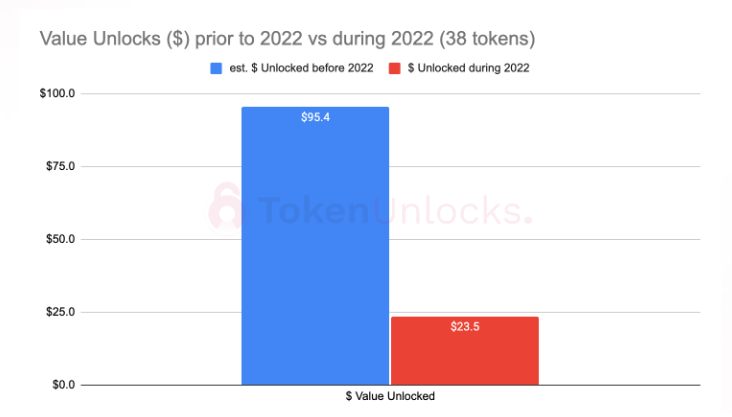

2022年之间解锁的38 个代币总估值约为954亿美元(按照截止到2021年12月31日的价格计算),而在2022 年期间解锁的代币价值为235亿美元。这意味着,仅在2022年一年内解锁的代币价值占到了之前所有年份解锁代币总价值的24.6%。当我们将锁定价值的逐年下降值与2022年解锁价值进行比较时,又发现了另一个有趣的现象:

”“

代币锁定价值的下降值为:1425亿美元–147亿美元= 1278亿美元,而解锁价值为235亿美元。

”“

想象一下,假如投资者在全年的解锁日期卖出所有头寸,那么他们平均获得的价值可能只有235美元/1278美元,即原本锁定价值的18.4%,而另外71.6%可能已经被公共市场所吸收。当然,这只是一个粗略的估计,实际上收益率还会涉及到当时的流动性、宏观效应、代币收益等其他各种因素。

不仅如此,我们还重点追踪了两种解锁机制,分别是:

”“

1、悬崖解锁(cliffunlock)

”“

2、线性解锁(linearunlock)

”“

下表列出了2022年悬崖解锁与线性解锁价值的对比。数据显示,悬崖解锁的代币价值占比约为61%(144亿美元/235美元),线性解锁的代币价值占比约为39%。与此同时,我们还可以看到,2022年解锁代币的总价值达到235亿美元,且上半年的解锁价值要比下半年高出两倍之多。

价格影响

”“

对于投资者而言,随着越来越多的代币从智能合约或钱包中解锁并在市场上流通,如果需求量保持不变,那么不难预料,这些代币价格将会下跌。

”“

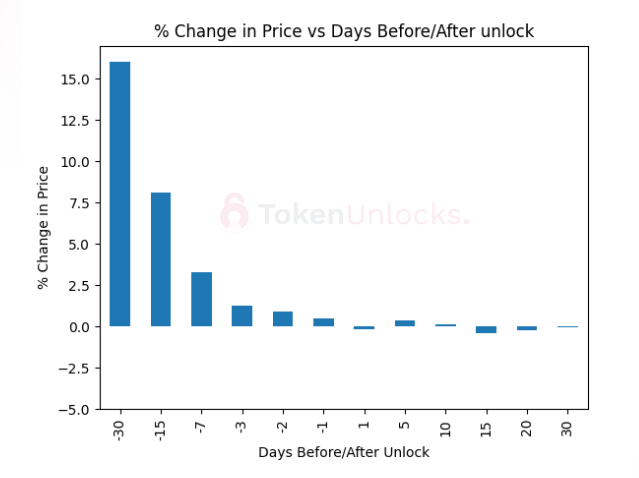

下图是对收集到的数据进行分析后的一些发现:其中x轴表示解锁前后的天数,负值表示解锁之前,正值表示解锁之后,y轴表示与解锁当天价格相比变化的百分比。正如趋势图展示的那样,随着解锁日期的临近,价格通常会下跌15%,而一旦解锁完成又将趋于平缓。值得注意的是,该分析参考了比特币价格,因此相对较为准确。

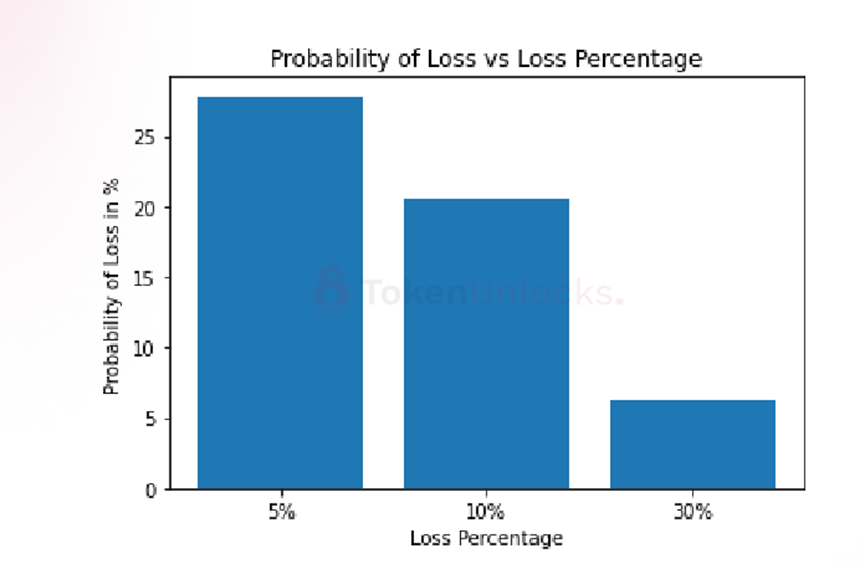

从上图中可以看出,与解锁前几天相比,代币价格在解锁日往往会下跌,因此我们想找出在解锁前30天、15天和7天做空时损失头寸的概率。

研究数据表明,代币价值损失5%的概率为27%,损失10%的概率为 20%,损失30%的概率为6%(需要注意的是,该分析考虑了比特币在短期内的价格行为)。

”“

2023年度展望

”“

报告还对2023年的加密市场进行预测,包括使用剩余市值和FDV对排名前300的加密项目进行代币解锁预测,以了解未来几年内的潜在解锁价值。为简单起见,该分析选取了2022年12月31日300个头部代币(固定供应)的统计数据,并且排除了无限量供应的代币。

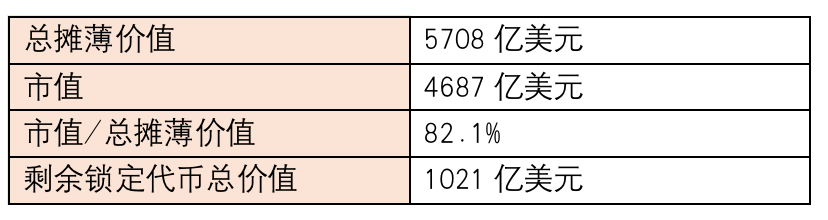

总体而言,总供应量固定的代币中已有82.1%的代币在市场上流通,而剩余的解锁代币价值约为1021亿美元。

”“

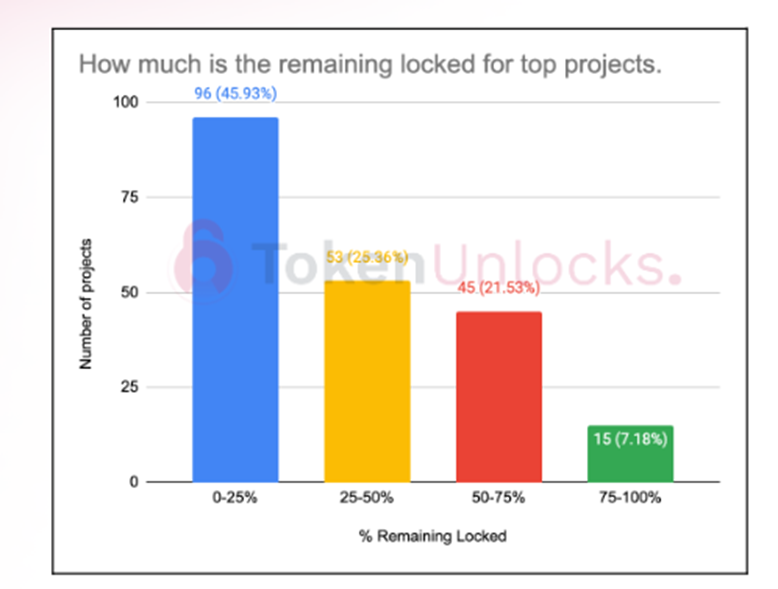

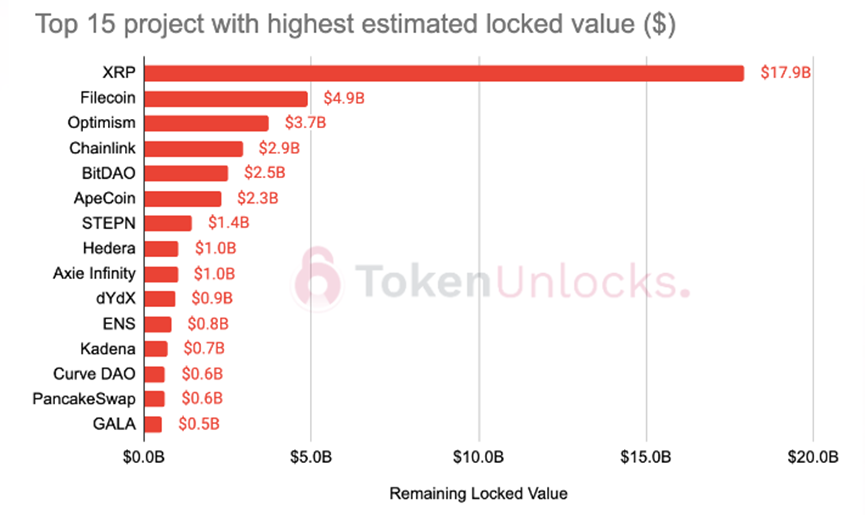

接下来,我们再看下剩余锁仓百分比(未来会在市场上进行流通),下面图表显示,96个加密项目锁定了不到总供应量25%的代币价值,其中有15个项目包含了超过75%的非流动性代币。平均而言,一个加密项目约有38.6%的总供应量需要解锁。最后一张图列出了预测剩余锁定价值最高的前15个项目,其中XRP位居榜首,代币价值高达180亿美元。

对于加密行业,2023年注定会是非常“有趣”的一年,因为许多在2021年获得融资的项目可能需要通过兑现其代币来支持运营。尽管大多数用户可能会选择离场,协议产生的收入也可能会直线下降,但相信随着越来越多分析数据的公布,加密行业的透明度在与日俱增,参与者也能够因此更深入地了解到每个项目的代币分配方式,并通过代币经济学和协议设计获得激励。

”“

相信在新的一年中,整个加密行业都能充满信心地继续前进,创造新的奇迹。