Memecoins have been under heavy selling pressure since December 2024, with many declaring the sector as good as dead. Prices collapsed across the board, liquidity dried up, and retail enthusiasm that once fueled massive rallies seemed to vanish. For months, memecoins have trended lower, underperforming most of the broader crypto market and leaving investors skeptical about their long-term survival.

Yet, despite the gloom, some analysts argue that dismissing memecoins entirely may be premature. As the market prepares for a new phase driven by shifting liquidity flows, institutional positioning, and macroeconomic catalysts, speculation could once again find fertile ground in this volatile sector. Top analyst Darkfost has gone as far as to suggest that the time to take a fresh look at memecoins may have arrived. According to him, data shows that the market is entering an area where memecoin dominance has historically regained strength, often sparking sharp rebounds.

While risks remain high—memecoins are still among the most speculative assets in crypto—the potential for explosive gains continues to attract attention.

Memecoin Dominance Signals Possible Rebound

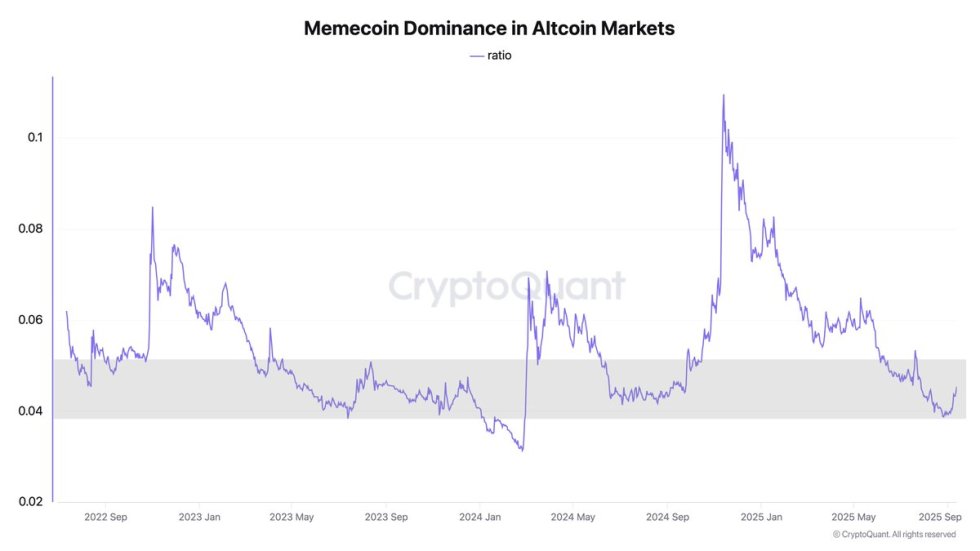

Darkfost highlights the importance of monitoring the Memecoin Dominance in Altcoin Markets chart, which compares the market capitalization of key memecoins against that of established altcoins. This ratio offers valuable insight into whether memecoins are gaining or losing influence relative to the broader altcoin sector.

Since the massive rush that peaked at the end of 2024, memecoins have been in a prolonged decline, steadily losing both valuation and investor interest. The frenzy that once drove parabolic gains gave way to exhaustion, with most of the sector retracing sharply.

Investors in memecoins understand the unique challenge of this asset class. Unlike Bitcoin or Ethereum, memecoins often lack fundamental backing, making them highly speculative. As a result, timing entries and, more importantly, exiting positions quickly to secure profits are essential strategies. Hesitation can easily turn short-term gains into significant losses.

Despite this, Darkfost observes that the memecoin dominance chart is signaling a potential turning point. The ratio has entered an area where memecoins have historically regained strength, marking the beginning of sharp rebounds. Early signs of reaction suggest that market sentiment may be shifting, with speculative capital slowly re-entering the space.

If the trend persists, the conditions could align for a renewed memecoin mania. While it may not replicate the extreme fervor of late 2024, a resurgence in speculative appetite could drive significant rallies. For traders watching closely, the data implies that memecoins may once again become a hot narrative in the crypto cycle, though managing risk remains paramount.

Market Cap Growth Analysis

The chart of the Memecoin Market Cap (Daily) shows how the sector remains highly volatile, reflecting speculative behavior that defines this corner of the crypto market. After rebounding strongly from the July lows near $64B, the market surged to a local peak above $88B in early September. However, that momentum quickly faded, with the cap now retracing toward $75B, down nearly 5% in the latest session.

The 50-day moving average at $68.7B has acted as a strong dynamic support throughout this recovery, showing that buyers continue to step in when valuations approach this level. Meanwhile, the sector’s ability to push above $80B and briefly test the $88B resistance highlights that speculative capital is still present, even if profit-taking remains aggressive.

For now, memecoins are consolidating after a sharp upswing, and the market appears to be searching for balance. If capitalization holds above the $72–74B range, a renewed attempt to reclaim $80B could follow, reigniting bullish sentiment. On the other hand, a breakdown below the 50-day average would suggest fading momentum and open the door for a deeper retracement. Ultimately, memecoins remain sensitive to liquidity flows and broader risk sentiment, making timing critical.

Featured image from Dall-E, chart from TradingView

Related Posts