Шибтоши, основатель торговой платформы SilentSwap, сохраняющей конфиденциальность, изложил несколько проблем, из-за которых учреждения не решаются принимать решения децентрализованных финансов (DeFi). Среди них конфиденциальность, отсутствие стандартизированных правил соответствия и юридическую ответственность.

Основатель проекта DeFi сказал, что высокая прозрачность транзакций в блокчейне представляет собой проблему для компаний, которые должны скрывать конфиденциальную информацию, включая торговые стратегии, информацию о заработной плате и соглашения между предприятиями.

«Основные проблемы — неопределенность регулирования, ограничения конфиденциальности и сложный пользовательский опыт — реальны, но решаемы. Инновации в протоколах сохранения конфиденциальности делают DeFi все более совместимыми с потребностями предприятий. Такие платформы, как SilentSwap, являются шагом в этом направлении», — сказал Шибтоши.

Неопределенность регулирования продолжает оставаться одной из самых больших проблем для DeFi и усугубляется фрагментарным подходом в правовых юрисдикциях, что препятствует институциональному принятию, добавил Шибтоши.

«Являются ли токены DeFi ценными бумагами? Что произойдет, если децентрализованная автономная организация (DAO) ошибется — и кто будет нести ответственность за это? Все это пока довольно неясно», — сказал основатель SilentSwap.

Шибтоши призвал к здравому смыслу в правилах, которые поощряют инновации и сохраняют ценностные предложения децентрализованных финансов, включая самостоятельное хранение, скорость и экономически эффективные транзакции.

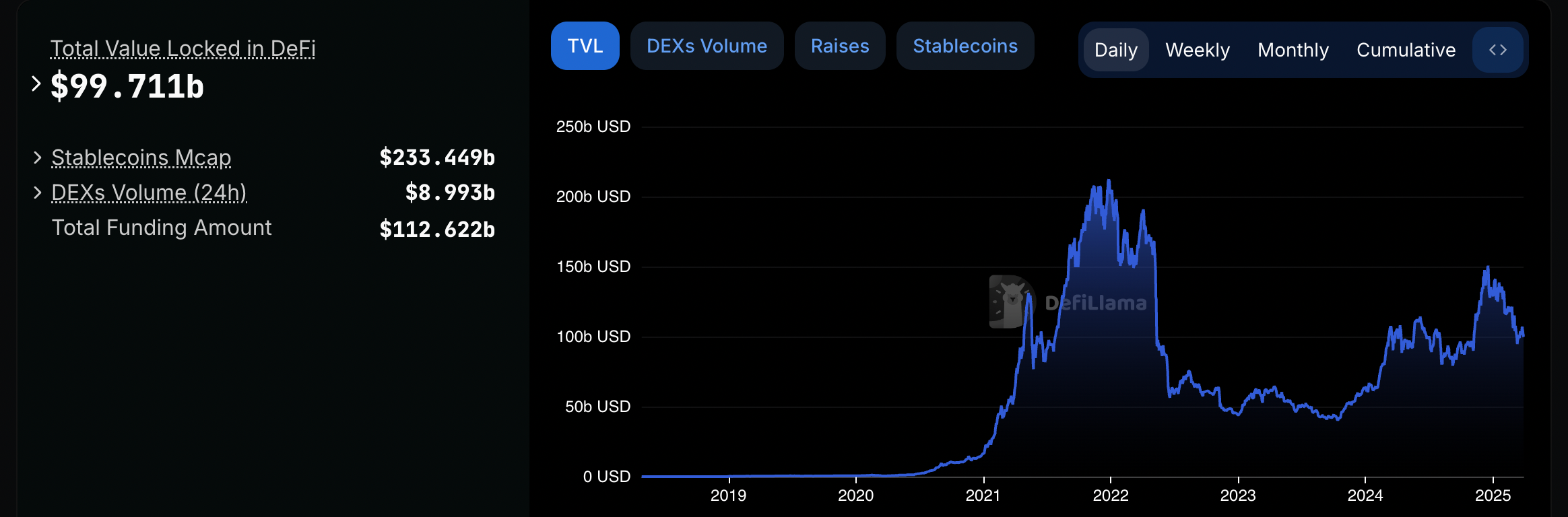

Общая заблокированная стоимость (TVL) в экосистеме DeFi, еще не вернулась к пиковым уровням, наблюдавшимся в 2021 и 2022 годах. Источник: DeFiLlama

Конгресс США отменяет архаичное правило DeFi, но сектор все еще в опасности

Обе палаты Конгресса США недавно проголосовали за отмену крайне непопулярного правила брокера DeFi, требующего от децентрализованных финансовых протоколов и платформ сообщать о транзакциях клиентов в Службу внутренних доходов (IRS).

Сенат США отменил правило брокера IRS 70 голосами против 27 4 марта, после чего члены Палаты представителей США проголосовали за отмену правила IRS 11 марта.

Несмотря на отмену архаичного правила, чрезмерное регулирование может в конечном итоге убить сектор, который родился как децентрализованная, более доступная и псевдонимная альтернатива традиционным финансам.

По словам криптопредпринимателя и инвестора Артема Толкачева, соблюдение нормативных требований подрывает децентрализацию в DeFi и разрушает ценностное предложение зарождающегося сектора.

Акцент на мерах соблюдения нормативных требований увеличивает потенциал цензуры и переносит контроль от пользователей к сторонним посредникам и крупным учреждениям, написал Толкачев.